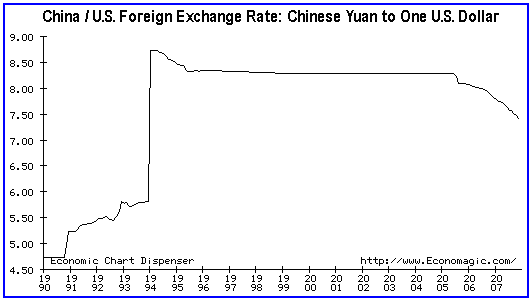

Over the past few years China's government has come under considerable international pressure -- primarily from the US -- to upwardly re-value its currency. China has acquiesced to this pressure to a certain extent and has allowed its currency (the Yuan) to rise from a rate of around 8.2 per US$ to the current level of around 7.4 per US$, equivalent to a gain of approximately 10%. A 10% change in the Yuan-per-US$ rate is significant, but with reference to the following chart notice that the Yuan's recent gains pale in comparison to the losses it incurred during the first half of the 1990s. In fact, the Yuan will have to gain another 23% just to get back to where it was 13 years ago. This, perhaps, is an indication of the currency's additional upside potential.

We think the political posturing over the Yuan's foreign exchange value borders on the ridiculous because the US is a net beneficiary of the Yuan's artificially low value while China's economy is disadvantaged by the Yuan's cheapness, and yet the US has been agitating for a stronger Yuan while China has been resisting the political pressure to upwardly re-value. The posturing is, however, understandable because the politicians involved in the dispute are focusing on the effects of exchange-rate movements on only one part of their respective economies and ignoring the overall effects. Specifically, the US government is fixating on the adverse effects of cheap Chinese imports on some US manufacturing businesses and ignoring the benefits received by a much larger section of the US economy due to lower prices on consumer goods. China's government, for its part, is fixating on the competitive advantages gained by its exporting industries thanks to the artificially cheap Yuan whilst, up until recently, ignoring the burden that maintaining the Yuan's low exchange value places on the economy as a whole.

We said "up until recently" in the above sentence because it seems that China's government has become aware of the 'dark side' of maintaining an unrealistically cheap currency. The 'dark side' is the inflation problem that will inevitably result from attempts to create a trade advantage via currency devaluation.

An inflation problem is the inevitable result of a currency policy such as the one that has been run by China for many years because the only way to keep the exchange rate of a currency at an unrealistically low level over a long period is to rapidly increase the supply of the currency. In China's case this has involved the central bank using newly-printed Yuan to purchase US dollars.

For a while the domestic price-related effects of China's currency manipulation were confined to financial assets and imported commodities, but China is now experiencing rapid BROAD-BASED price increases. Or, to put it more aptly, the Yuan's purchasing power has begun to fall at a rapid rate (China's government admits to a 6.9% year-over-year purchasing power loss, but the true rate is probably at least 10%). If this situation is allowed to continue then even the export-oriented industries -- the industries that are the main beneficiaries of the cheap Yuan -- will get hurt due to their costs rising faster than their revenues.

Proving that it can be just as dumb as most other governments when it comes to inflation issues, one of the tactics used by China's government to combat the upward pressure on prices has been to cap the price of gasoline. Not surprisingly this has led to widespread gasoline SHORTAGES, necessitating rationing, as refineries that aren't under the direct control of the government have reduced their rates of production in order to cut their losses. China's current situation is proving, yet again, that price capping is a particularly insidious method of tackling an inflation problem because it simultaneously reduces the incentive to produce and increases the incentive to consume.

In addition to doing things that create shortages of important commodities without actually addressing the underlying causes of the price rises, China's government is also taking steps that could slow the rate of money-supply growth and could thus get to the heart of the issue. For example, the reserve requirement for banks has just been lifted from an already-elevated 13.5% to a 20-year high of 14.5%. This could crimp the rate of credit expansion and therefore address the underlying problem, although if the Yuan remains pegged way below its fair value then China's central bank will have to keep printing reams of new Yuan to maintain the peg; in which case the steps being taken to rein-in the expansion of credit will effectively be counteracted by the money-printing that stems from the exchange-rate policy.

In other words, to significantly reduce its inflation problem China will have to let the Yuan appreciate at a faster pace.

-- Posted Friday, 14 December 2007 | Digg This Article | Source: GoldSeek.com

Regular financial market forecasts and analyses are provided at our web site. We arent offering a free trial subscription at this time, but free samples of our work (excerpts from our regular commentaries) can be viewed at:

http://www.speculative-investor.com/new/freesamples.html

The content on this site is protected

by U.S. and international copyright laws and is the property of GoldSeek.com

and/or the providers of the content under license. By "content" we mean any

information, mode of expression, or other materials and services found on GoldSeek.com.

This includes editorials, news, our writings, graphics, and any and all other

features found on the site. Please contact

us for any further information.

Live GoldSeek Visitor Map | Disclaimer

The views contained here may not represent the views of GoldSeek.com, Gold Seek LLC, its affiliates or advertisers. GoldSeek.com, Gold Seek LLC makes no representation, warranty or guarantee as to the accuracy

or completeness of the information (including news, editorials, prices, statistics,

analyses and the like) provided through its service. Any copying, reproduction

and/or redistribution of any of the documents, data, content or materials contained

on or within this website, without the express written consent of GoldSeek.com, Gold Seek LLC,

is strictly prohibited. In no event shall GoldSeek.com, Gold Seek LLC or its affiliates be

liable to any person for any decision made or action taken in reliance upon

the information provided herein.

Chinas Currency Problem

Chinas Currency Problem