|

-- Posted Tuesday, 10 February 2009 | | Source: GoldSeek.com

Gold Investments Market Update

Profit taking saw gold fall yesterday but continuing very robust demand for physical bullion and gold ETFs for safe haven purposes means that this is likely another period of consolidation.

There is a dawning realization that we are in the early stages of a severe global recession and possibly even a global Depression. In this uncertain climate for the global financial system and the global economy itself, risk aversion is set to remain elevated and thus demand for physical gold bullion will also remain elevated. As it will for silver but less so for the purely industrial precious metals of platinum and palladium.

10-Feb-09 | | Last | | 1 Month | YTD | 1 Year | 5 Year | Gold $ | | 894.20 | | 4.82% | 1.59% | -3.10% | 120.08% | Silver | | 12.91 | | 14.96% | 14.24% | -24.82% | 102.66% | Oil | | 40.37 | | -1.12% | -9.48% | -55.98% | 19.19% | FTSE | | 4,264 | | -4.14% | -3.83% | -26.28% | -3.20% | Nikkei | | 7,946 | | -10.08% | -10.31% | -38.95% | -23.34% | S&P 500 | | 870 | | -2.29% | -3.69% | -34.65% | -24.06% | ISEQ | | 2,464 | | -8.28% | 5.13% | -62.31% | -51.81% | EUR/USD | | 1.2966 | | -3.77% | -7.21% | -10.61% | 2.25% | © 2008 Goldassets.co.uk | | | | |

In the short term gold awaits the possible passage of the Obama stimulus package. Obama himself has warned of catastrophe if the package is not passed. The real question is if this latest humungous $800 billion spending package will be sufficient to arrest the sharp decline in progress of the US financial system and economy. Even more pertinent is the real risk that while it may be another short term panacea, it will likely lead to significant inflation or stagflation in the coming months.

Bond markets are already sensing this and thus the 10 Year bond has fallen in value and seen its yield rise from 2% to over 3% since the start of the year. The dollar is also likely to come under severe pressure in the coming weeks as the ramifications of huge US government deficits, money printing and monetization of debt are realized.

The Financial Times reports today of continuing huge demand for physical bullion. The FT reports today that Investors are buying record amounts of gold bars and coins, shunning risky assets for the relative safety of bullion amid renewed fears about the health of the global financial system. The US Mint sold 92,000 ounces of its popular American Eagle coin last month, almost four times that which it sold a year ago and more than it shipped during the whole of the first half of 2007. Other countries mints have also reported strong sales.

Is FT's Lex Right to Favour Platinum Over Gold?

The usually excellent Lex column in the Financial Times has made a bold prediction regarding gold gold is already high and thus investors should look to platinum.

While Lex is normally excellent there is a peculiar irrationality, lack of knowledge and indeed ignorance that takes over when writing about gold as an asset class.

Lex has been very biased against and very wrong on gold for a number of years. In September 2005 it said gold was overvalued at $475/oz and may rally further, but it is driven by funds chasing price momentum. Such bets are often quickly reversed. How wrong it was.

For some reason Lex engages in a lot of unbalanced, pejorative language about irrational goldbugs being notorious zealots. Any rational observer now knows that those who prudently diversified into gold in recent years were very rational. The world of leveraged Ponzi finance had many adherents who were notorious zealots who were more than a little irrational and they have got us into this terrible financial and economic mess. Not prudent savers and investors who decided to diversify and not to have all their eggs in the stock and property baskets of the leveraged global casino.

Platinums fundamentals are interesting and we believe the precious metals component of a properly diversified portfolio should have an allocation to gold, silver and platinum. However, platinum is not a safe haven asset like gold and silver, and because it is an industrial metal its fundamentals are less certain.

As usual the old reliables of macroeconomic risk (in 2009 this includes deflation currently, inflation likely later, monetary/currency and systemic risk) and geopolitical risk will be the main drivers of the gold and silver market. The platinum group metals (not having the safe haven qualities of gold and silver) are likely to be more influenced by the decline of industrial demand and other supply demand issues.

Industrial and jewellery demand for platinum will fall this year. The question is whether investment demand might pick up considerably and negate the falling demand from industry and jewellery. ETF demand and investment demand for coins, bars, certificates and unallocated and allocated accounts is a wild card which will likely result in sharply higher prices in all precious metals, including platinum. But gold and silver will likely benefit more from safe haven demand.

Also, gold and silver have huge short positions that are being investigated by the newly invigorated Commodity Futures Trading Commission (CFTC) for possible market manipulation. There is now much evidence to suggest that there has been market manipulation by some of the large players in the futures market (more evidence then was presented to the SEC regarding Madoff prior to those revelations) and this could lead to a massive short squeeze in both gold and silver.

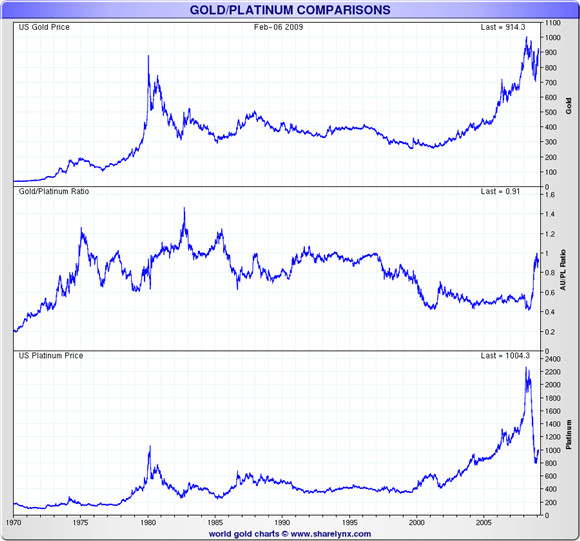

Lex says that the gold platinum ratio would suggest that platinum is cheap vis-à-vis gold:

Go back 20 years, and platinum has traditionally traded at 1.5 times the cost of gold. Now that ratio is 1.07 times; in relative terms, platinum is therefore cheap. Platinum also has a range of uses, in iPods, computers, car catalysts, anti-cancer drugs and spark plugs, to name a few. That also makes it a cheap option on economic recovery. The only metal fit for a king, Louis XV declared about platinum. And, perhaps, for investors too.

However, 20 years is a very short time frame and in these historic times with comparisons being made to the 1970s stagflation, the 1930s Great Depression, the 1920s Weimar hyperinflation, it would be wise to look back further than the recent past performance.

The last time that gold and precious metals were in a bull market was in the 1970s and during this period gold was often more valuable than platinum and indeed was as much as 1.2 times more valuable and for a very brief period over 1.5 times more valuable.

Todays ratio of around 1:1 is close to the average of the last 40 years (as seen in the chart above) a more representative sample as it includes the entire period since the U.S. went off the Gold Standard in 1971.

With increasing concerns about near zero percent interest rates, unprecedented money printing, quantitative easing, monetization of debt and debasement of currencies internationally, the safe haven, monetary metals of gold and silver look set to continue to outperform platinum. (As Milton Friedman pointed out The major monetary metal in history is silver, not gold.)

It has been shown in numerous academic studies including by the highly respected portfolio and asset allocation experts, Ibbotson and Associates, in a June 2005 study, Portfolio Diversification with Gold, Silver and Platinum, how gold, and indeed precious metals, are the only one of the seven asset classes with a negative average correlation to the other asset classes. It is also worth noting that the authors showed that, excluding cash, precious metals are the only asset class with a positive correlation coefficient with inflation, which is further evidence that precious metals act as a hedge not just against macroeconomic and systemic risk but also against the long term threat of inflation.

Indeed Ibbotson and Associates determined that holding between 7.1 percent and 15.7 percent in precious metals bullion reduces portfolio volatility and improves returns over the long term.

Ignore Lex and continue to diversify and remain diversified with gold, silver and some platinum bullion.

Data Protection: Gold Investments is committed to complying with the requirements of the Data Protection Act. This means that in the provision of our services, appropriate personal information is processed and kept securely. It also means that we will never sell your details to a third party.

The information you provide will remain confidential and may be used for the provision of related services. Such information may be disclosed in confidence to agents or service providers, regulatory bodies and group companies. You have the right to ask for a copy of certain information held by us in our records in return for payment of a small fee. You also have the right to require us to correct any inaccuracies in your information. The details you are being asked to supply may be used to provide you with information about other products and services either from Gold Investments or other group companies or to provide services which any member of the group has arranged for you with a third party. If you do not wish to receive such contact, please write to the Marketing Manager, Gold Investments, 63 Fitzwilliam Square, Dublin 2 marking the envelope data protection.

Disclaimer: The information in this document has been obtained from sources, which we believe to be reliable. We cannot guarantee its accuracy or completeness. It does not constitute a solicitation for the purchase or sale of any investment. Any person acting on the information contained in this document does so at their own risk. Recommendations in this document may not be suitable for all investors. Individual circumstances should be considered before a decision to invest is taken. Investors should note the following: Past experience is not necessarily a guide to future performance. The value of investments may fall or rise against investors interests. Income levels from investments may fluctuate. Changes in exchange rates may have an adverse effect on the value of, or income from, investments denominated in foreign currencies. Gold and Silver Investments Limited, trading as Gold Investments is a Multi-Agency Intermediary regulated by the Irish Financial Regulator.

(Irish Office)

Gold and Silver Investments Limited

63 Fitzwilliam Square

Dublin 2, Ireland

T:+ 353 1 6325011

F:+ 353 1 6619664

Web: www.gold.ie | | (UK Office)

Gold and Silver Investments Limited

No. 1 Cornhill

London, EC3V 3ND, UK

T:+ 44 (0) 207 060 4653

F:+ 44 (0) 207 8770708

Web: www.goldassets.co.uk |

-- Posted Tuesday, 10 February 2009 | Digg This Article | Source: GoldSeek.com | Source: GoldSeek.com

Previous Articles

|