|

-- Posted Sunday, 3 January 2010 | Digg This Article | | Source: GoldSeek.com | | Source: GoldSeek.com

The background noise has been considerable. The USCongress, the august body that often passes legislation without reading it, evaluates a new initiative to reinstitute the Glass Steagall Act. Pass it, don't read it! Great idea! In the wisdom from post-Depression seven decades ago, the same Congress imposed firewall separation among the commercial banks, the brokerage houses, and the insurance firms in order to prevent systemic financial sector failure. That is precisely what happened in the last two years, without proper recognition or diagnosis, except by this and some analysts. Insolvent systems do not spring back to life with grandiose infusions of phony money and complete covers for fraud. They remain insolvent. The bank woes will suffer massive relapse this year, from fresh commercial mortgage losses, from prime Option ARMortgage foreclosures, and from continuing overload of toxic losses from gargantuan residential property held on their books that they stubbornly refuse to put up for sale. If the US housing market shows any remote signs of price stability, it is due to a few hundred thousand foreclosed homes held by banks, floating on their ruined balance sheets, held back from dispatch to real estate brokers in auction. Keep price stable by erecting a banker dam on properties. It must release, but it might head straight into the Fannie Mae toxic pit.

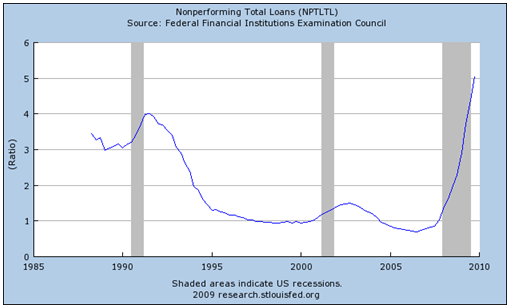

Another popular bizarre balance sheet item is the bank reserves held for interest yield within the safe confines of the US Federal Reserve. The USFed itself might desperately need such funds to ward off its own deep insolvency in the hundreds of billion$. They did after all, ramp up toward 50% their ratio of USAgency Mortgage Bonds, most of which are worth far less than the stated value on their cratered books. The ugly truth on this matter is that US big banks face additional huge losses, so the reserves held at the USFed should be regarded as Loan Loss Reserves, hardly robust assets. They are still insolvent. These big banks are so dead, that the only partners they attract are other vampires. Non-performing loans have soared to a record 5%, shown below. Now factor in that US banks carry over $7000 billion in commercial loans. The resultant $350 billion of non-performing loans on the books of banks is disclosed, but what is not disclosed is their additional toxic assets off balance sheet and other various credit derivatives like Interest Rate Swaps. These huge supposed bank reserves are not going anywhere, surely not the USEconomy. The big banks are still wrecked.

Quietly the USCongress has been working on new legislation to reform the financial system regulatory structure. It reads like a TARP to the sixth power. The House of Representatives has passed its version, the House Resolution 4173. The US Senate must next tackle the issue. The House version calls for up to $4 trillion in big bank aid if and when another banking system breakdown occurs. Despite all calls to reverse rescue for financial firms too big to fail, this bill does exactly the opposite. My pattern of analysis, successful for five years, has been to hear the words, to expect precisely the opposite in the action taken, and to regard the words as pure deception to calm the opposition and lull it into a moribund state. The people are easily fooled, and rarely comprehend new legislation once forged into law. Hear the words, anticipate the opposite. That tactical approach was honed in my work by observing Greenspan. Without any hint of doubt, the USCongress is a trained lackey for Wall Street and the bankers. The nation has lost control to bankers long ago. The end game is a shattering reality. BLANK CHECK TO FANNIE & FREDDIE Turn to the Eye-Popper this past week, an event that should have caused incredibly deep alarm, disgust, dismay, disconcertment, and consternation. Instead, the US financial markets have been so anaesthetized by nationalizations, big bank welfare, major fraud cases, outsized executive bonuses for failed bankers, prattle about recovery by political and bank leaders, and mindless federal programs that cost multiples more than benefits. So the news of an unlimited line of funds, not at all a credit line, comes to the viewing audience. This is a BLACK HOLE of unlimited diameter. One should be immediately suspicious, before reading any details. Fannie Mae & Freddie Mac (F&F) have been the source of at least $2000 billion (yes, $2 trillion) in missing funds from the Papa Bush and Clinton Administrations. Politicians love the Fat Fannie Freddie Duo, since it has served as a slush fund source for two decades. These missing, stolen, counterfeited, absconded funds are documented by the auditors to the USDept Housing & Urban Development. The follow-up stopped in its tracks, as officials in the USDept Treasury halted investigations, informing auditors that the funds are designed to fund black bag projects, including the Working Group for Financial Markets. This is all well documented, and not in dispute any longer. My theory from September 2008 onward has been that Fannie & Freddie were put under conservatorship within the USGovt in order to prevent investigations of fraud, to prevent discovery of Wall Street bond counterfeit, to prevent lawsuits on improper securitization of mortgage income streams (usage of single income with multiple bonds), and to prevent mortgage rates from rising as foreign creditors dumped mortgage bonds. The joke on Wall Street these days has been that Fannie Mae is a great firm to leave, since despite allegations of criminal activity, nothing happens on the legal side, and besides, the exit bonuses are in the multi-million$. Ex-CEO Franklin Raines, friend to all politicians, earned $62 million upon exit amidst controversy and shades of fraud. So next, the blank check is written for Fannie & Freddie, and one should suspect that the funds will flow freely. Any expectation of major home loan balance reduction for the benefit of the people might be misplaced. We shall see! Maybe it will come! The USDept Treasury announced last Thursday the removal of the $400 billion financial cap on the money line provided to keep the companies afloat. To date, US taxpayers have parted with $110 billion to the fat duo. All estimates submitted by the USGovt about loss magnitude have been laughable. My forecast over a year ago was for at least $2 trillion and possibly $3 trillion in losses ultimately, over 10 times what officials stated. My figure is looking better every passing week. Denials persist that the original $400 billion limit was nowhere approached. So why extend the line of funding to unlimited? The reasons are two-fold in my view. First, grandiose grotesque gargantuan losses are coming, since liquidation of bad home loans has been halted. A huge dam of toxic loans is on the Fannie & Freddie books. As Rich Santelli of CNBC said on Tuesday, "This move permits Fannie Mae to load on all kinds of additional pigslop onto their balance sheet, and to do so without end." He followed with some denigrating remarks about the wisdom of fiscal leadership. Second, the blank check will permit continued coverup of the mortgage bond fraud, along with rafts of broken credit derivative contracts. The coverup requires much additional papering over. The size of the Interest Rate Swap book on the F&F books must be greater than the global economy, maybe by a multiple. Next is large scale mortgage portfolio liquidations, mortgage portfolio writedowns, and possibly some actual loan balance reductions finally. Massive losses will be revealed by Fannie & Freddie, but the public and financial sector will applaud the cleansing process. An astonishing volume of backlog home loan constipation might be relieved by means of this official enema in the planning stage. Housing prices are certain to drop if F&F refuse to permit their managed home portfolio to grow without limit. If F&F dump homes on the housing market, the prices will drop another 15% to 20% easily. The alternative is more what my forecast has in store, a truly staggering shocking alarming home rental business by the USGovt as landlord. The Fat F&F Duo can mitigate the negative political reaction by reducing home loans in a substantial way and to a meaningful degree, which would help to stop the foreclosure parade and the reversal of the Ownership Society nightmare. MOTIVE FOR THE USGOVT HOME OWNERSHIP Fannie Mae and Freddie Mac provide vital liquidity to the mortgage industry by purchasing home loans from lenders and selling them to investors. Most investors lose heavily, but the bond brokers make out very well indeed. Together, F&F own or guarantee almost 31 million home loans worth about $5.5 trillion, almost half of all mortgages. Without USGovt aid, the firms would have gone bust long ago, leaving millions of people unable to obtain a mortgage. The biggest headwind facing the housing recovery has been the rise in foreclosures as unemployment remains high and the hidden bank inventory of foreclosed properties swells each month. The Obama Admin dare not disclose its long-term plans for the two agencies under conservatorship. Pardon me during outbursts of laughter at the mere word 'conservatorship' since nationalization was under that thin veil all along, as in all along. The formal steps were missing, but no longer. The Toxic F&F Duo will never return to their former power and influence, not to mention integrity, if they have had any for 20 years. The Obama Admin might do best to conceal its plans of federal residential property ownership, since it might read like a Communist Manifesto. In summer 2005, my forecast for Fannie Home Rentals has come true, with nary a peep of objection. Rentals are seen as a great solution. The F&F shareholders should face total ruin with share price at zero. Instead, Fannie Home Rentals should provide a massive revenue stream useful in justifying a stock share price. At the same time, the financial sector will likely applaud all initiatives that result in removing home supply from selling inventories. The federal landlord plan actually will permit some home price stability. Let's not even touch on executive bonuses and compensation packages for the current managers of these financial sewage treatment plants. My personal conjecture is that Fannie Mae is burning through money 5 times faster than the topline figures show. The USGovt will next be funding the Great Black Hole in a more visible fashion, if that is a positive development. One might even conclude that the blank check is not price inflationary, since it goes right into the toilet. This is Weimar Defecation. It will affect the USDollar and USTreasury global integrity. Worse, we are at the forefront of a blossoming of the USGovt emerging as a significant national landlord. What we have is the onset of precisely the opposite of the Ownership Society put forth by ex-President Bush II. What irony! Or was it the plan? Just like the Greenspan Project to undermine the US financial grid? One should harbor great suspicion that the USGovt has been collecting mortgages on a grand basis, as has been the USFed. My full expectation is that the USFed will dump their entire mortgage bond assets on the USGovt at the appropriate timely moment, despite any lack of value, and receive nearly full book value. The taxpayers inherit the sewage. Furthermore, gigantic tranches of home loans from the residential sector are likely to come from the commercial banks, heading directly to the Fannie & Freddie balance sheets. This flood will accelerate the disenfranchisement of the proletariat, as home foreclosures continue unabated, and the USGovt entrenches its property ownership. Those who fail to see the trend toward a communist state with military dictatorial powers are at best sleep and at worst blind. Numerous theories have been floating in the media and in internet journals, where the most responsible journalism exists, by far, bar none. Former HUD auditor Catherine A Fitts shared her opinion that the banks are going to take huge writedowns on the commercial side. To make room on their balance sheets to handle the commercial mess, the residential portfolios are going to be shifted to Fannie & Freddie in a manner that will protect the major banks. The F&F balance sheets are where residential mortgages will go to die, she expects. The market cannot handle the home sale flow from liquidations. And besides, the Federal Housing Admin and Ginnie Mae are too small and too logistically strained to move such volume so quickly. The sewage treatment plant is well equipped. All roads lead to F&F Processing Plant. The USGovt auditors will proclaim profits from Fannie Home Rentals, but hide the enormous losses. Dan Amoss of the Strategic Short Report shares his opinion on a trend. He said, "The market will eventually adopt the view that Fannie Mae and Freddie Mac have been nationalized. Last week's elimination of limits on Treasury's capital infusion into Fannie and Freddie is a defacto nationalization. In other words, there is no longer much chance of a re-privatization, but instead we will see a gradual transformation of these Frankensteins into new branches of government. They will implement the official government agenda for housing, without much regard for prudent lending. This will have huge consequences for the Treasury market. While the federal government will stick to its Enron-style accounting, and not officially consolidate Fannie/Freddie assets and liabilities onto the government balance sheet, the smarter foreign creditors will. These creditors will start viewing Fannie/Freddie liabilities as equal to Treasuries in terms of default risk. But this does not mean that spreads on Fannie/Freddie liabilities will tighten down to Treasuries. Rather, it will substantially increase the long-term default risk of Treasuries, and Treasury buyers will demand higher rates to compensate for this risk." Amoss anticipates the principal mortgage provider in the future is indirectly going to be the USGovt. Amoss also states that the USTreasury debt is to be mixed with the USAgency Mortgage debt in perception, no longer distinguishable since the former funds the latter. THE RISK OF USTREASURY DEFAULT HAS LEAPED HIGHER!! Since Fannie & Freddie are deeply insolvent, the new USGovt debt ratio also leaped higher. On the entire motive theme, ponder the following. The USTreasury Bonds are at risk of higher bond yields. They will likely not shoot up rapidly, since the JPMorgan machinery is still in operation, namely the Interest Rate Swaps. Check the Office of Comptroller to the Currency for basic evidence. A reversion to the mean, a reversal of the lopsided positions, a return to normalcy would clearly involve over a $1 trillion loss to the JPMorgan monster. The IRSwap contracts are firmly in place, ramped up, heavily fortified by Printing Pre$$ activity without scrutiny or bounds, never properly audited since done by venerable JPMorgan. While we all decry the rise of credit derivatives, few complain about low interest rates in today's age of speculation. Artificially low cost of money has fueled two decades of asset bubbles and the ruin of the US industrial base. My view is that the USFed is desperate to end their 0% rate, since they realize it caused the housing & mortgage bubbles in 2003-2007. But the USFed has returned to the scene of the crime with entrenched 0% rates, stuck for over a year. The USFed definitely does NOT want long rates to rise. They are scared witless of rising mortgage rates, since they would kill the housing market altogether, or at least put it under a massive wet blanket for an indefinite time. The IRSwap detonation could happen at either end, on the short rate or long rate, much like a stick of dynamite with a fuse at each end. Risk is acute if the USFed were to hike the FedFunds rate, since they would directly set off IRSwap explosions. The USGovt borrowing costs would triple also. RISK RISK RISK, MONETIZATION & INTEGRITY Harken back just a few weeks, when the USDept Treasury and USFed announced on a repeated basis the end of Quantitative Easing. Their words were laughable, intended to deceive, and were whole portions of propaganda. INSTEAD, THEY DID THE EXACT OPPOSITE, AND MADE THE FORMAL ANNOUNCEMENT BETWEEN THE CHRISTMAS AND NEW YEAR HOLDIDAYS. The move to permit unlimited Fannie & Freddie funding is an end-around maneuver to prevent long-term interest rates from rising, or at least to insulate the mortgage finance arena from higher long-term interest rates. IT COMES AT A COST, OF SYSTEMIC RISK, OF PERCEIVED DEFAULT RISK, OF USGOVT DEBT FOUNDATION RISK. The year 2010 might be characterized by a rise in the entire USTreasury bond yield spectrum, from short-term to mid-term to long-term. It is not just a bad thing, a risk filled development. It is a risk of game over! The monetization threat and deep monetary inflation to fund USTreasurys (indirectly Fannie & Freddie debt) are important parts of the vicious cycle displayed in the December 16th article entitled "Full Circle of Govt Debt Default" (CLICK HERE). The full circle (see the chart) starts and ends with the USDollar and the USTreasurys, from debts, monetization, and monetary inflation gone haywire. The toxic chickens come home to roost!! The credit markets must prepare for one of two undesirable outcomes. Either interest rates rise markedly in order to fund the USGovt federal deficits or else Printing Pre$$ output of phony money must escalate without bounds. Next comes debt explosion or Weimar inflation. The federal deficits must be securitized, in other words, converted into bonds and funded. The process so far has involved an incredible amount of hidden monetization. It is slowly being discovered, but not reported by the sleepy lapdog intrepid press & media. My articles have detailed some of the primary bond dealer monetization in Permanent Open Market actions, and some of the foreign central bank monetization of mortgage bonds to fund USTreasury bids. The year 2010 will feature monetization of USGovt debt and of mortgage losses out in the open to a much greater degree. The effect will be to place the USGovt debt viability at grave risk. It will be interesting to watch the debt ratings agencies (Standard & Poors, Moodys, Fitch) squirm. They are under tremendous pressure not to repeat their lackadaisical behavior in the past. They are downgrading European nation sovereign debt. They are denying openly the justification to downgrade both United Kingdom Govt and United States Govt debt. Their denials are damning in themselves, since why mention the lack of justification for such downgrade unless they should be downgraded by any reasonable measure. The USGovt short-term funding requirements are almost as great as their active monetization, the clear expedient. The USEconomy tolerates huge Ponzi Schemes from the inside, like Madoff, like Fannie & Freddie, like AIG, like Wall Street itself. Rather the USEconomy has become one huge Ponzi. Its expansion on the margin is uncontrollable, just like its appetite for new funds is uncontrollable. The blank check to Fannie & Freddie is testimony to the need to fund the Ponzi Scheme, but it is phony money entering a vast and widening Black Hole. USDOLLAR BOUNCE Last autumn 2008, one year ago, the USDollar embarked on what my analysis called a Dollar Death Dance. The bounce from the November depths last month at 74.5 to the hardly rarified air near 79 has been sudden. The rise in rebound has been built upon several factors. The Dubai debt mess has exposed European and London banks for further losses, leading to an exit from both the Euro and British Pound currencies. The US banks are more adept at hiding their losses, extended their toxic loans, pretending they will find eventual value. The Dubai shock has made vividly clear the heightened risk of a European Union fracture, a threat to the Euro currency, and a need for Germany to cut off the Southern Europe impaired limbs, debt and all. One must wonder with sinister thoughts if the Dubai debt was permitted to default, or orchestrated to default, precisely at the most promising season for gold, into the year end strength. It short-circuited the strong gold season. But one thing is for sure about seasonality issues. They have been widely destroyed in recent years in numerous asset classes. The late winter and spring for gold should be strong again, as the USDollar will expose its toxic fundamentals. The only thing making the ugly pig with lipstick look good is the unfavorable comparison to broken European national debt structures, which do not have the benefit of the Printing Pre$$ Privilege or the vast criminal sydicates supported by it. The Competing Currency Wars have heated up again from comparisons rather than open hostility to protect exports. Money departs the Euro harbors and enters the toxic USDollar pits, where the stench of Printing Pre$$ overdrive operation fills the air, where the shame of unlimited Fannie & Freddie black hole directed funds tarnishes the USDollar image, and where the unprosecuted Wall Street bond fraud festers like an open sore. This sudden US$ rebound has left the G-20 Meeting declarations a recent bad memory. The emerging nations had shown steady disrespect for the so-called developed nations, the deep debtors who long ago lost their industrial base. They transformed industry to debt, a miracle of modern central banking!! There is nothing like some debt liquidation to show how the USDollar still has remnants of a safe haven. Its security has only remnants, torn shreds adorned by stars and stripes once given respect. Let's not even touch the endless wars, the clandestine military business in narcotics, the private contractor fraud in the war effort, the missing $50 billion in Iraqi Reconstruction Funds that nobody is looking for. These activities smear and harm the US image in powerful ways, often without US awareness from inside the US Dome of Perception. Just what is the force to sustain the USDollar rebound? More European member nation debt woes. More credit derivative liquidation and payouts. The US$ rebound runs on noxious fumes. This is the Dollar Death Dance, part II. The long-term trend will remain down. The immediate activity could feature more of the same. The short covering of the Dollar Carry Trade has been clear. It will have to muster enough funds, courage, and wisdom to put that carry trade into second gear. It is inevitable. It is justified. It will be profitable. It certainly will be dangerous, since the USDollar is still the global reserve currency. That status is threatened though. Clearly, the USDollar rebound, a move of a mere 6% in the last few weeks, is the only factor pushing down the gold price. One can see that the gold price decline has run its course. The overbought condition has worked itself off. The risk of a move to 1060-1080 is apparent. However, the moving averages are rising. The stochastix are ready to cross over in a positive way. Last but not least, the fundamentals for the USGovt finances and the USDollar in particular could not be more acutely horrible, miserable, outrageously negative, and represent a palpable threat of a sovereign debt default down the road. At least we will see a monetary crisis centered upon the USDollar. That would pressure the eventual default.

The USDollar rebound and the reflexive gold correction have been rapid and thus are unstable. They are both nurtured by European and London weakness, rather than US strength. The long-term trend is solid and up for gold. With all the hubbub and gnashing of teeth, the gold price is still above its October highest level. My favorite question of US$ Bulls is "What has been fixed?" The answer is nothing. Much money has been spent, and huge deficits have been racked up, but to what end? No remedy, no reform, no structural imbalances corrected, no deficit reduction, no military expense curtailment, no end to banker welfare, no successful modification to home loans, no end to home foreclosures, no end to job cuts, no end to supply chain disruption, no end to the USGovt and USFed acting as primary lenders, not just lenders of last resort. The USDollar is running on fumes, and the end to its bounce is near. The gold bull will run again. Three to four steps up, one step back. THE HAT TRICK LETTER PROFITS IN THE CURRENT CRISIS. From subscribers and readers: At least 30 recently on correct forecasts regarding the bailout parade, numerous nationalization deals such as for Fannie Mae and the grand Mortgage Rescue. "Thanks for the quality of the information you put forth in your newsletter. I read a lot of newsletters, blogs, and financial sites. The accuracy of your information has been second to none over the past couple of years."

(MikeP in Missouri)

"Your October HTL was your best writing since I have been subscribing. It just amazes me how much you write each month, all top-notch stuff."

(DavidL in Michigan)

"I used to read your public articles, and listen to you, but never realized until I joined what extra and detailed analysis you give to subscription clients. You always seem to be far ahead of everyone else. It is useful to 'see' what is happening, and you do this far better than the economists! I can think of many areas in life now where the best exponent is somebody not trained academically in that area."

(JamesA in England)

"You seem to have it nailed. I used to think you were paranoid. Now I think you are psychic!"

(ShawnU in Ontario)

Jim Willie CB is a statistical analyst in marketing research and retail forecasting. He holds a PhD in Statistics. His career has stretched over 25 years. He aspires to thrive in the financial editor world, unencumbered by the limitations of economic credentials. Visit his free website to find articles from topflight authors at www.GoldenJackass.com . For personal questions about subscriptions, contact him at JimWillieCB@aol.com

-- Posted Sunday, 3 January 2010 | Digg This Article | Source: GoldSeek.com

Previous Articles by Jim Willie CB

|