-- Posted Friday, 8 July 2011 | | Disqus

By Daniel R. Amerman, CFA

Overview

The eventual insolvency of many or most state and local governments in the United States, as well as of many major corporations, can be relatively easily shown to be the necessary mathematical byproduct of current US federal monetary and economic policy.

For decades, state and local governments were encouraged to make binding pension promises which relied heavily upon the (deeply flawed) academic theory that the lucrative compounding of investment wealth over the long term was close to guaranteed. Employee and sponsor contributions by themselves have never been enough to pay pensions, and unless investment profits deliver most of the money, then pension assets come up woefully short of being able to meet pension obligations.

However, Federal Reserve and United States government policy for the last ten years has been to knock interest rates down to near historic lows, even while propping up the prices of investment assets. This policy has simultaneously knocked out both of the mathematical pillars that long-term pension fund investments relied upon (as well as destroying the heart of conventional individual retirement planning). Because investment yields have been driven so low by the government, the pension plans are already in dire straits.

Public employees have enjoyed a guaranteed retirement age, and the numbers of boomers reaching retirement age is rapidly increasing. This means financial pressure is also building rapidly, and in order to avoid insolvency, state and local government pension plans must radically increase investment yields. The problem is that current federal policy is to effectively make these higher yields near mathematically impossible for the states to obtain, at least while following conventional strategies. And, as we will cover herein, this is likely to lead to a massive transfer of even more power from the state to the federal level, as states must meet the requirements of federal level politicians in order to avoid insolvency.

Pension Fund Mechanics: Contractually Promising The Future

The central absurdity underlying traditional (defined-benefit) pension funds is the assumption that economists and financial professionals know the future, and that they know it with such certainty that society can legally guarantee it. Governments and major corporations hire financial analysts and actuaries, and these professionals estimate that "x" will be the money coming in, they estimate that "y" will be the investment rate, they estimate that "z" is how long people will live after retirement, and then they run the equations and say that everything covers. Then the states, cities, school boards and major corporations of the United States - and their equivalents overseas - contractually obligate themselves to make payments to their pensioners that are based on these estimates.

("Defined benefit" means that the pension plan promises to pay retirees a certain amount of dollars per month, regardless of investment performance, and while now no longer available for most private and public workers, defined benefit plans are still in force and legally binding for tens of millions of current and future retirees.)

An elaborate jargon permeates the investment world, but behind all the alphas, betas, ratios, regressions, binomial distributions and option-adjusted pricing models, let me suggest that there are only two words that matter when it comes to long-term pension fund investing: "exponential compounding". What matters more than anything else is not so much the amount of money that is saved, but the amount of time that the money is invested and the rate at which we assume the money is invested.

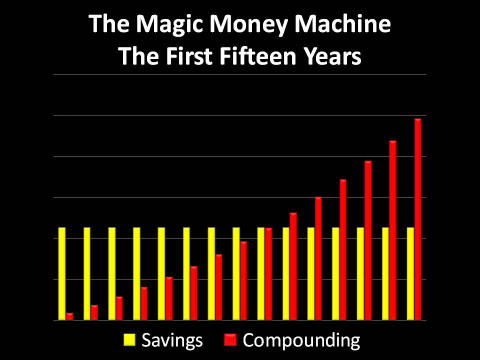

For a very quick overview of the real heart of pensions and conventional financial planning, consider the two graphs below from my fundamentals of retirement investment article, "The Mythical Magic Money Machine":

http://danielamerman.com/Video/MMM.htm

The yellow lines are assumed savings / pension contributions and the red lines are the assumed earnings on those savings. If we assume an 8% initial investment rate - and much more importantly, a never-ending 8% reinvestment rate - then by year nine, the importance of assumed earnings (the red bar) has reached the importance of actual savings. By year fifteen, our reinvestment income is assumed to be generating more than twice the cash flow than what is coming in from actual savings contributions.

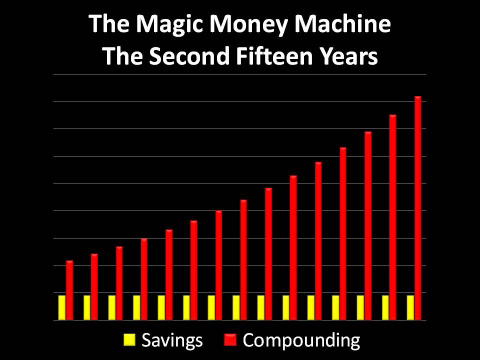

The real "magic", however, is not in the first 15 years at all, but rather in the second 15 years of investment, whether the investor be a pension fund or individual. By this time, according to the models that drive virtually all public and corporate pension funds, earnings upon earnings upon earnings are required to be dwarfing actual savings - or the numbers fall apart, and the money isn't there to pay the pensioners what they have been promised. This second 15 years is also particularly important because the average Boomer is over 50 years old now, and we have this "bulge in the python" in the US and other sections of the world, as the number of "Boomers" with pensions who have reached retirement age swells with each year.

The graphic above is the numerical summary of the red and yellow bars, and is intended to be as generic as possible. If someone saves $377 every month for 30 years, and we assume they can earn an average return of 8%, then when we feed the numbers into our money machine / pension investment model, it says those savings will support a retiree for 17 years with an annual income of $56,000. As shown in the chart above, the assumption is that if we save about a hundred thousand dollars over 30 years, then because we know the future and are assured that we will be able to invest and then compound at a long term average of 8%, we can then take out almost $1 million.

With the pension fund, this future income is not only assumed, but it becomes a contractual obligation. The state, county or city each effectively say that based upon the best available professional advice, they know that they will have $956,000 to pay out, and they therefore pledge their future taxpayers' full faith and credit that those dollars will be paid. So that $956,000 is based on $820,000 in assumed investment earnings, and the government unit or corporation is fully on the line for the difference if the exponential compounding doesn't occur.

Reality Check: Pension Fund Investing Hasn't Worked In 10 Years

There is a minor technicality with this wonderful (assumed) wealth creation machine, and many financial professionals are very well aware of it. When it comes to pension funds - as well as individual retirements in the United States - the "machine" hasn't worked in the last 10 years. The Dow Jones today is only about 10% higher than the early summer of 2001, and has actually fallen in inflation-adjusted terms. Dividend levels have been very low and have essentially covered expenses. So to the extent that pensions and individual retirement accounts have been depending upon equity earnings to rapidly ratchet up wealth - the earnings simply haven't been there, particularly on an after-inflation basis.

The other key issue (as covered in several of my articles) is that when it comes to bonds and interest rates, we have had very low and sometimes even negative interest rates (on an inflation-adjusted basis) as a direct result of government policy for the last 10 years. That is, the Federal Reserve and Federal government made a very deliberate decision in the aftermath of the collapse of the tech bubble, and of September 11, 2001, to drop interest rates to some of the lowest levels in our lifetimes, and to keep them there indefinitely. Initially this was to try and stimulate economic growth. However, the larger result was to help create the real estate bubble.

The predictable price paid for keeping interest rates artificially low is the destruction of pension and individual retirement returns. Look again at those graphs for the expected compounded earnings that were supposed to be there the last 10 years. The "red bars" haven't been there. This more than any other reason is why the state and corporation pensions are in terrible shape (and are in fact in much worse shape than is commonly publicly presented). The pensions and their sponsors bet their futures that the academic theorists and investment professionals knew what the investment future would hold - only to be blindsided when the federal government then intervened to drop the floor out from underneath their yield assumptions.

The Desperate Need For Yield Even As The Federal Government Destroys Yields

This brings us to 2011 and what is going on right now. The Federal Reserve and the federal government are dedicated to interrelated policies. Number one, they're attempting to keep the interest rates paid on huge government borrowings down to almost nothing, as well as keeping home mortgages affordable, in order to support the housing market. They have successfully forced short-term interest rates down to virtually zero, well below even the stated rate of inflation, let alone the true rate of inflation. Long-term interest rates are also very low. This is all absolutely essential to keeping deficits from getting far worse than they are right now, and let me suggest that it is also part of a deliberate government policy of Financial Repression, as covered in my previous article "Financial Repression: A Sheep Shearing Instruction Manual".

http://danielamerman.com/articles/2011/RepressionA.htm

The federal government is also doing everything it can to prop up stock market asset values. Now without considering pension fund investments or retirement accounts, this may seem like a very logical goal, even an exceptionally good idea. Indeed, if you were to allow stock values and other assets to find their true market levels, it would seem that the pension funds would be in much worse shape than they are right now because the value of their assets would be much less.

But this is overlooking what the heart of pension fund investing - as well as conventional financial planning in general - is all about. Take a moment and scroll back up to the previous graphs. Preserving asset values in the form of maintaining investment values, as represented by the yellow bars, just doesn't hack it. All that does is lock in insolvency for the pension fund sponsor.

In order for pension funds and individual retirement accounts to have even a chance at strong financial performance in real terms over the coming decades, they desperately need those red bars. Without strongly positive returns, coupled with the exponential compounding of those returns, then the mathematical underpinnings of pension investing and conventional financial planning shatter into little pieces.

The divergence between economic growth rates and assumed exponential wealth compounding rates that forms the foundation of pension fund investing never would have worked over the long term anyway, not when too large of portion of the population (the boomers) started trying to cash out their compounded paper wealth into real goods and services simultaneously. These are among the reasons why I went on the record almost 20 years ago in explaining why the nation's retirement investment models were "patently absurd".

The situation got much worse in 2001 when the Greenspan-led Federal Reserve decided their collective monetary genius was such that the business cycle could be overridden, and recessions put in the dustbin of economic history through forcing interest rates to levels far below what a free market would demand. The easy credit and low interest rates were designed to push asset prices higher, and this policy was indeed "successful" in rapidly re-inflating stock prices even as real estate prices began to climb.

This massive government intervention in the investment markets was enormously popular, particularly among those who would more typically oppose government interventions, because the short term effect was to increase the paper wealth of the nation. However, the short term manipulations necessarily carried a long-term price, which was the crushing of the wealth creation mechanism that was necessary for the long-term retirement standard of living for millions of people, along with forcing the eventual insolvency of the nation's defined benefit sponsors - particularly the state and local governments.

Oh, the intention was likely to walk away at some undefined point in the future and let market forces regain more importance. But in practice - what time was that? The problem with pursuing short term benefits through massive artificial manipulations is that when you withdraw the manipulations, interest rates rise and asset values fall, the recession likely returns worse than ever - and from a political perspective, when is that ever convenient? Of course, this dilemma persists today, and is indeed far worse than it used to be. Metaphorically, the longer and deeper the addiction, the worse the withdrawal can be.

Even the mainstream financial press is beginning to speak of 2001-2011 as being a "Lost Decade" for investments, and this is nowhere more true than it is for the pensions, which were already in growing trouble by 2008. However, the years since 2008 have been particularly catastrophic.

For pension funds (and the conventional investor) to have any chance at all, it isn't just that rates of return need to rise on your current portfolio, but every new dollar that you put in as you scramble to catch up has to be invested at a higher rate. If the ending value of your stock share is $100 in ten years, and you buy at $100 today because asset prices are propped up - then you earn nothing. However, buy at $70 this year, then $73 next year, then $76 the year after that, then add in the reinvestment (compounding) of interim investment earnings, and keep the assumption of cashing out at $100 a share - and all of a sudden, you are building real wealth again.

So we have set up an environment where as a matter of government policy, interest rates are near zero, and asset values are artificially high. Because of government policy, yields are going to be much lower both for funds currently invested, and, crucially - funds remaining to be invested over the next 10 to 15 years. The policy effectively deliberately annihilates reinvestment income. It annihilates exponential compounding - the very heart of pension planning and financial planning. And when you have a pension whose solvency absolutely requires the exponential compounding of investments and as a matter of government policy there is no exponential compounding - then absent any other major rule changes, the insolvency of the pension plan is more or less mathematically guaranteed. If the pension fund sponsor does not have the ability to make pensioner payments without the wealth created by compounding and they often can't - then the sponsor is forced into insolvency. Thus many states, cities and counties are likely to be bankrupted by their public employee pension plans.

The Federal Government's Deliberate Financial Destruction Of The States

It's really fairly straight forward if you have a knowledge of how finance and financial compounding works. It is strongly in the short term interests of politicians who are trying to win elections in two year election cycles, to massively intervene in the markets for the purportedly public good of keeping interest rates low and asset values high. Which is exactly why political pundits who know virtually nothing about economics and finance jump on the wagon and say, "yes, this is good for all of us!"

A lot of people do know better, however, particularly at the Treasury Department and the Federal Reserve.

By deliberately having set a policy of keeping interest rates far below market for the last 10 years, as well as maintaining asset values at artificially high levels, the pension funds of the country are being systematically destroyed as a matter of federal policy. In other words, the feds are more than willing to throw every state government "under the bus" and destroy their long-term financial prospects, as long as it serves the short term interests of the federal politicians currently in power. This is a bi-partisan consensus, as it truly kicked into gear with a Republican administration and is being taken to all new levels by a Democratic administration, when it comes to massive monetary interventions to keep interest rates and asset prices at artificial levels.

Now let's consider another angle, and the eventual logical destination. Most states go bankrupt, as do many of the major corporations, unless a deal is worked out with the federal government for a bailout. The natural end result is that the power of the federal government (and the politicians who wield that power) rises to all new levels, as there is a consolidation of power.

Eventually, then, every major pension plan sponsor who would otherwise go into bankruptcy must more or less come hat in hand to the federal government, so the federal government will bail them out of the financial destruction that was inflicted upon them by the federal government itself.

Groupthink & Individual Action

What is presented in this article has been true and building for a very long time now. The pension fund crisis was not caused by events in 2008, although the damage was brought forward and accentuated by the overall financial crisis. However, for the intelligent and well-intentioned financial professional (as well as for long-term investors in general), it also presents a fundamental conundrum. Everyone was taught that if you put your clients in a blend of equities and bonds where the mix changed with the age of the client, then things were more or less guaranteed to work out, even if the fine print of the legal disclaimers were careful to make clear that nothing was actually guaranteed.

So deep was the groupthink was that there was no Plan B, and only a few financial professional "radicals" like myself were stepping outside the box and saying things like: "What happens to pension funds and retirement investors if it turns out we don't actually know the future? What about what's happening in Japan? What if the 21st century doesn't turn out to be another American century? Do these numbers really add up, or are they catastrophically wrong? Has this ever really been done before, with this many retirees cashing out the markets for real goods and services without even interrupting the assumed never-ending exponential increase in paper wealth?"

None of those quite reasonable questions were allowed to be considered within the models, rather they were excluded by definition. There was no ability to adapt to the government's deliberately destroying investment yields for short term benefit, it did not fit within the models. There was no ability to adapt to the rise of Asia, or the hollowing out of America's economy and other Western economies, it simply wasn't in the models. There was no consideration of the effects of an aging population on economic growth or investment returns - even when investing for unprecedented growth in the older population was the whole point of the investments in the first place.

The conventional wisdom has collapsed, because it never was valid, no matter how uniformly accepted the groupthink was among academic economists, financial planners, pension advisors or politicians. Unfortunately, however, the powers that be haven't accepted that yet, so the nation's pension funds rush towards their appointment with mathematical destiny, with the predictable devastation of the states and local governments, while both parties in the federal government hold down the accelerator in an attempt to gain political advantage.

The salient question for you is - will your financial security and future standard of living collapse along with the pension funds? Whether you are in line for a pension or have your own investment portfolio (or both) - what is the source of your personal financial paradigm?

I'm not a pessimist by nature, but rather I belong to the contrarian investment school of thought. One way of defining contrarian philosophy would be that it is devoted to finding the opportunities inside of problems.

When I looked into the conventional financial "wisdom", I found that not only are its assumptions deeply flawed, but it holds no realistic solutions for a world where interest yields were kept artificially low and asset prices are kept artificially high.

However, when we step outside the "conventional wisdom" box - everything changes. If we take an investment approach that is specifically designed to benefit from mispricings, then the current situation becomes a target-rich opportunity for determined investors.

There are indeed practical ways for individuals to take below market interest rates - that are deliberately held below the rate of inflation by governments - and turn them into extraordinary personal wealth. With the right strategy, instead of destroying your future, below market interest rates are the equivalent of handing you money.

Artificially high asset prices and the resulting asset deflation in inflation-adjusted terms is a much tougher nut to crack than monetary inflation but it can be done for individuals, and the rewards can be even greater. Indeed the heart of some of my recent work has been educating people about the practical methods for turning asset deflation into greater wealth opportunities than those that can be found through reversing monetary inflation. For understanding simultaneous asset deflation and monetary inflation is the essential key to unlocking the most profitable precious metals investment strategies. As I discuss in my Gold Out Of The Box materials, gold is not generally a particularly good monetary inflation hedge when inflation taxes are taken into account but it can be a spectacularly successful systemic asset deflation play.

The collapse of the conventional wisdom will be catastrophic for most, including too many states and local governments. However, for those who see the full implications, it also has the potential to become one of the greatest wealth creation opportunities of our lifetimes.

There are a number of distinct but intertwined solutions. But they all start with the same first step: education.

To get out of step with your generation, and have wealth redistributed to you even as your peer group is being devastated by this extraordinary destruction of wealth, you need to start with education. You need to gain the knowledge you will need to turn adversity into opportunity. Ultimately, you will need to look at the simultaneous destruction of the value of assets and the value of money and see a once in several generation personal wealth creation opportunity. An opportunity that can be accessed through a multi-component strategy that anticipates the stages of monetary crisis and then moves with the stages, with a relentless focus on systematically protecting and building after-tax and after-inflation net worth.

Do you know how to Turn Inflation Into Wealth? To position yourself so that inflation will redistribute real wealth to you, and the higher the rate of inflation the more your after-inflation net worth grows? Do you know how to achieve these gains on a long-term and tax-advantaged basis? Do you know how to potentially triple your after-tax and after-inflation returns through Reversing The Inflation Tax? So that instead of paying real taxes on illusionary income, you are paying illusionary taxes on real increases in net worth? These are among the many topics covered in the free Turning Inflation Into Wealth Mini-Course. Starting simple, this course delivers a series of 10-15 minute readings, with each reading building on the knowledge and information contained in previous readings. More information on the course is available at DanielAmerman.com or InflationIntoWealth.com .

Contact Information:

Daniel R. Amerman, CFA

Website: http://danielamerman.com/

E-mail: mail@the-great-retirement-experiment.com

This article contains the ideas and opinions of the author. It is a conceptual exploration of financial and general economic principles. As with any financial discussion of the future, there cannot be any absolute certainty. What this article does not contain is specific investment, legal, tax or any other form of professional advice. If specific advice is needed, it should be sought from an appropriate professional. Any liability, responsibility or warranty for the results of the application of principles contained in the article, website, readings, videos, DVDs, books and related materials, either directly or indirectly, are expressly disclaimed by the author.

-- Posted Friday, 8 July 2011 | Digg This Article | Source: GoldSeek.com

| Source: GoldSeek.com