-- Posted Friday, 30 August 2013 | | Disqus

Todays AM fix was USD 1,392.75, EUR 1,051.85 and GBP 899.19 per ounce.

Yesterdays AM fix was USD 1,406.25, EUR 1,059.96 and GBP 906.79 per ounce.

Gold fell $8.60 or 0.61% yesterday, closing at $1,407.10/oz. Silver fell $0.44 or 1.81%, closing at $23.85. Platinum fell $11.61 or 0.8% to $1,518.99/oz, while palladium was down $8.78 or 1.2% to $734.22/oz.

Gold is set for its second consecutive higher monthly close which is bullish from a momentum and technical perspective. Gold is nearly 5% higher for the month in dollars and euros, 2.5% in pounds and 12% in rupees after the rupee collapsed in August.

Gold Seasonal - Monthly Performance and Average (10 Years)

Gold quickly fell from $1,407/oz to $1,395/oz at 0800 London time despite no data of note and little corresponding movement in oil and stock markets. Profit taking and an increase in risk appetite may have contributed to the falls after the U.K. parliament voted to reject military action against Syria and fears over oil supply disruptions in the Middle East eased.

Oil prices are still heading for the largest monthly gain in a year, with Brent up more than 6% in August after unrest cut output in Libya by around 1 million barrels per day and production fell in Iraq, Nigeria and elsewhere.

The U.S. seems likely to proceed with a strike against Syria even after U.K. lawmakers rejected action which should support prices. The yellow metal reached $1,433.83/oz on August 28th, its highest since mid May on concerns that the U.S. will go to war with Syria.

Golds recent gains are primarily due to very strong physical demand globally and increasing supply issues, particularly in the LBMA gold bullion market. Syria and the increasing geopolitical uncertainty in the Middle East are creating real oil price and inflation risk which has contributed to the increased bullion buying in recent days.

As ever it is important to focus on the medium and long term drivers of the gold market:

Medium Term Market Drivers

The medium market themes guiding the market currently are as follows:

Seasonal

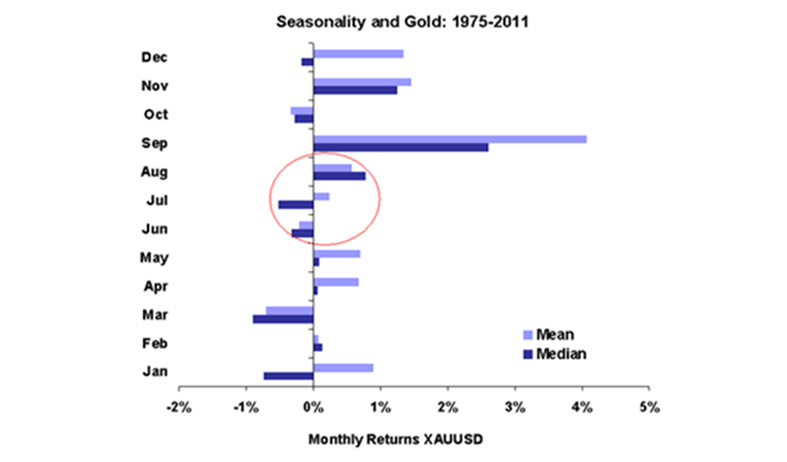

Late summer, autumn and early New Year are the seasonally strong periods for the gold market due to robust physical demand internationally.

This is the case especially in Asia for weddings and festivals and into year end and for Chinese New Year when China stocks up on gold. Gold and silver often see periods of weakness in the summer doldrum months of May, June and July.

This week will see the end of August trading and September is, along with November, one of the strongest months to own gold. This is seen in the charts showing golds monthly performance over different time frames - 1975 to 2011, 2000 to 2011 and our Bloomberg Gold Seasonality table from 2003 to 2013 (10 years is the maximum that can be used).

Thackray's 2011 Investor's Guide notes that the optimal period to own gold bullion is from July 12 to October 9. During the past 25 periods, gold bullion has outperformed the S&P 500 Index by 4.7%.

COMEX

Futures market positioning as seen on the COMEX is now very bullish.

Short positions held by hedge funds in the gold and silver markets remain very high and the stage is now set for a significant short squeeze which should propel prices higher in the coming months. Arguably we are in the early stages of this short squeeze.

Hedge funds have consistently been caught wrong footed at market bottoms for gold and silver in recent years and high short positions have been seen near market bottoms, prior to rallies in gold and silver.

Conversely, the smart speculative money, bullion banks such as JP Morgan have reduced their short positions and are now long in quite a significant way and positioned to profit from higher prices in the coming weeks and months.

Federal Reserve Tapering

The Federal Reserve has been suggesting for months, indeed years, that they would return to more normal monetary policies by reducing bond buying programmes and gradually increasing interest rates.

Talk is cheap, actions speak louder than words and it is always best to watch what central banks do rather than what they say.

Near zero interest rates and bond buying are set to continue for the foreseeable future.

Precious metals will only be threatened if there is a sustained period of rising interest rates which lead to positive real interest rates. This is not going to happen anytime soon as it would lead to an economic recession and possibly a severe Depression.

Chinese Demand

Chinese demand for physical bullion continues to be very high and continues to support prices and will likely again contribute to higher prices in the coming months. China gold purchases surged 54% to 706.4 metric tons in the first half of 2013 from the first half of 2012 - a year of record demand in China.

Demand surged 87% for bars and 44% for jewelry. China's gold demand should hit a record 1,000 tonnes this year and will almost certainly overtake India, the worlds largest saver in gold.

The Peoples Bank of China is almost certainly continuing to quietly accumulate gold bullion reserves. As was the case previously, they will not announce their gold bullion purchases to the market in order to ensure they accumulate sizeable reserves at more competitive prices. They also do not wish to create a run on the dollar thereby devaluing their sizeable foreign exchange reserves.

Expect an announcement from the PBOC, sometime in 2013 or 2104, that they have doubled or even trebled their reserves to over 2,000 or 3,000 tonnes.

India

Indian demand has fallen somewhat due to recent tariffs but will remain robust and should be as high as 1,000 tonnes this year.

Gold Forward Offered Rates (GOFO)

Gold forward offered rates (GOFO) or the cost to borrow gold remains negative. Negative gold borrowing costs is likely due to a lack of supply of large 400 ounce bars as mints, refineries and jewellers internationally and especially in Asia are scrambling to secure supply.

Gold Backwardation

Gold is in backwardation. Meaning that gold for future delivery is trading at a discount to physical market prices a rare situation that has occurred only after the Lehman Brothers collapse and near the bottom of the gold market in 1999. Spot prices or prices for delivery now are higher than prices for future contracts at later dates. This is very unusual and means that buyers are willing to pay a premium for physical. It also strongly suggests that there is tightness in the physical market.

Eurozone Debt Crisis

The Eurozone debt crisis is far from over and will rear its ugly head again - probably as soon as the German elections are over. Politicians and bankers have managed to delay the inevitable day of reckoning by piling even more debt onto the backs of already struggling tax payers thereby compounding the problem and making it much worse in the long term.

Greece, Spain, Portugal, Italy, Ireland, now Cyprus and even France remain vulnerable.

Japan, U.K., U.S. Debt Crisis

In Japan, the national debt has topped the ¥1 quadrillion mark. A policy of money printing pursued for a decade has failed abysmally and now politicians look set to pursue currency debasement in an even more aggressive manner with attendant consequences.

The U.K. is one of the most indebted countries in the industrialised world - the national debt continues to rise rapidly and is now at more than 1.2 trillion pounds ($1.8 trillion) and total (private and public) debt to GDP in the U.K. remains over 500%.

The U.S. government is once again on the brink of defaulting. At the start of the 'credit crisis' six years ago, U.S. federal debt was just $8.9 trillion. Today, U.S. federal debt stands at $16.738 trillion - 88% higher and increasing rapidly. This does not include the $70 trillion to $100 trillion in unfunded liabilities for social security, medicare and medicaid.

Long Term Fundamentals

The long term case for precious metals is based on the four primary drivers - the MGSM drivers that we have long focussed on.

Macroeconomic Risk

Macroeconomic risk is high as there is a serious risk of recessions in major industrial nations with much negative data emanating from the debt laden Eurozone, U.K., Japan, China and U.S.

Geopolitical Risk

Geopolitical risk remain elevated - particularly in the Middle East. This is seen in the serious developments in Syria and increasing tensions between Iran and Israel. There is the real risk of conflict and consequent affect on oil prices and global economy. There are also simmering tensions between the U.S. and its western allies and Russia and China.

Systemic Risk

Systemic risk remains high as few of the problems in the banking and financial system have been addressed and there is a real risk of another 'Lehman Brothers' moment and seizing up of the global financial system. The massive risk from the unregulated shadow banking system continues to be underappreciated.

Monetary Risk

Monetary risk or currency risk remains high as the policy response of the Federal Reserve, the ECB, the Bank of England and the majority of central banks to the risks mentioned above continues to be to be ultra loose monetary policies, zero interest rate policies (ZIRP), negative interest rate policies (NIRP), deposition confiscation or bail-ins, the printing and electronic creation of a tsunami of money and the debasement of currencies.

Should the macroeconomic, systemic and geopolitical risks increase even further in the coming months, as seems likely, than the central banks response will likely again be more cheap money policies and further currency debasement which risks currency wars deepening.

Conclusion

Absolutely nothing has changed regarding the fundamentals driving the gold market. We are confident that gold, and indeed silver, are still in long term secular bull markets likely of a 15 to 20 year duration.

Owning physical gold coins and/or bars in your possession and owning physical gold and silver in allocated accounts will continue to protect and grow wealth in the coming years.

NEWS

Gold Trade Most Bullish Since March on Syria Crisis - Bloomberg

Gold slips on stimulus fears, Syria uncertainty - Reuters

Gold Trims Weekly Gain on Tapering Bets as Syrian Tension Ebbs - Bloomberg

India considers buying back gold to bolster plunging rupee The Guardian

COMMENTARY

Jim Rogers Expects Higher Gold Prices, and Marc Faber Does Too Market Watch

Citi Asks How High Can Gold Ultimately Go? Zero Hedge

SocGen Bear Albert Edwards Repeats Call for $10,000 Gold Barrons

Bomb Syria, Get Cyberattacked Attacked The Daily Reckoning

-- Posted Friday, 30 August 2013 | Digg This Article | Source: GoldSeek.com

| Source: GoldSeek.com

{kind=link}

{kind=link}

{kind=link}