Its one of the greatest ironies of history that gold detractors refer to the metal as the barbarous relic, when in fact the abandonment of gold has put civilization as we know it at risk of extinction.

The gold coin standard that had served Western economies so brilliantly throughout most of the 19th century hit a brick wall in 1914 and was never able to recover, so the story goes. Europe turned from prosperity to destruction, or more precisely, to the prosperity of a few and destruction of others, as the Great War got underway. The gold coin standard had to be ditched for such a prodigious undertaking.

If gold was money, and wars cost money, how was this even possible?

First, people had been in the habit of using money substitutes instead of money itself - paper bank notes instead of the gold coins for which they could be redeemed on demand. People found it more convenient to carry paper around in their pockets than gold coins. Over time the paper itself came to be regarded as money, with the gold it represented a clunky inconvenience from the old days.

Second, banks had been in the habit of issuing more bank notes and deposits than they had gold in their vaults and would on occasion arouse the suspicion of the public that the notes were making promises the banks couldnt keep. The courts sided with the banks and allowed them to suspend note redemption while otherwise staying in business, thus strengthening the government/bank alliance. Since the deposits really belonged to the banks once they were deposited said the courts bankers could not be accused of embezzlement. The occasional bank runs that erupted were interpreted as a self-fulfilling prophecy. If people lining up to pull their money out believed their banks were insolvent, the banks soon would be. Most people had no idea their banks were loaning out most of their deposits. They didnt know fractional reserve banking, a form of counterfeiting, was the norm.

We need to remember that a counterfeiter is not criminal because hes printing his own notes; hes criminal because the notes he prints dont represent real money though they are accepted as such. To expose the criminality of a counterfeiter and lay the blame on those who expose him is where the mainstream economics profession has stood for a long time. But there are solid reasons for their position.

The requirement of gold coin redemption put limits on the extent of fractional reserve banking. Such limits are not welcomed by the banks. Since the banks can loan to the government, it means a limit on government spending. Government doesnt like the limitation of gold coin redemption either.

The war [in 1914] came as a great shock, not only to the masses of the American people, but also to most well-informed Americans and, for that matter, to most Europeans. [Ch. 2]

And yet, Germany, Russia, and France began accumulating gold prior to the war with Germany starting first, in 1912.Gold was taken out of the hands of the people and carried to the reserves of the Reichsbank, the German central bank.People were given paper notes to take the place of gold in circulation.

When war broke out in August, 1914, Gary North explains, the pre-World War I policy of gold coin redemption was

independently but almost simultaneously revoked by European governments . . . They all then resorted to monetary inflation. This was a way to conceal from the public the true costs of the war. They imposed an inflation tax, and could then blame any price hikes on unpatriotic price gouging. This rested on widespread ignorance regarding economic cause and effects regarding monetary inflation and price inflation. They could not have done this if citizens had possessed the pre-war right to demand payment in gold coins at a fixed rate. They would have made a run on the banks. Governments could not have inflated without reneging on their promises to redeem their currencies for gold coins. So, they reneged while they still had the gold. Better early contract-breaking than late, they concluded.

Without breaking their promise to redeem paper notes for gold coins, governments would have had to negotiate their differences rather than engage in the deadliest war in history at that point.Abandoning the gold coin standard, which had always been under control of governments instead of the free market, was the deciding factor in going to war.

Though the U.S. didnt formally abandon gold during its late participation in the war, it discouraged redemption while roughly doubling the money supply. From War and Inflation, Blanchard Economic Research:

"In World War I, the American people were characteristically unwilling to finance the total war effort out of increased taxes. This had been true in the Civil War and would also be so in World War II and the Vietnam War. Much of the expenditures in World War I, were financed out of the inflationary increases in the money supply." (See "American Economic History," Scheiber, Vatter and Faulkner)

Wikipedia: missing in action

Its more than strange that Wikipedias entries for World War I and the gold standard make no mention of the connection between an easily inflatable currency and war. Under their entry for gold standard, for example, Wikipedia says, By the end of 1913, the classical gold standard was at its peak but World War I caused many countries to suspend or abandon it. This is wrong. Governments had a choice: fight a long, bloody war for specious reasons or retain the gold coin standard. They chose war. U.S. leaders found their decision irresistible. It wasnt J.P. Morgan, Woodrow Wilson, Edward Mandell House, or Benjamin Strong who would be fighting in the trenches.

Of course, the war was only the first of many government catastrophes resulting from the abandonment of gold. In their entry for 20th century, Wikipedia tells us that Terms like ideology, world war, genocide, and nuclear war entered common usage. Nor was it uncommon to hear terms like fiat money, central bank, Federal Reserve, debt, and accommodation, but the article makes no mention of these.

Its true, the gold standard utterly fails when governments want to kill selected populations and control the rest. Gold is an honest money, a value offered in exchange for another value, but governments by nature are not honest because they acquire their resources by theft and intimidation. In light of what weve witnessed since the rejection of gold, its difficult to imagine an honest humanitarian regarding the precious metal as barbarous.

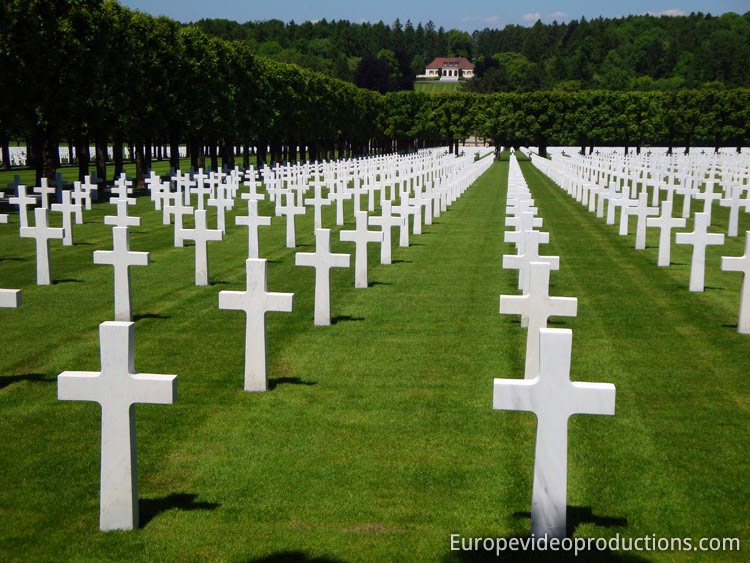

When we hear about going off gold as a prerequisite to peace and harmony among men, we should remember places such as the Meuse-Argonne American Cemetery in France, where grave markers seemingly extend to infinity. These are the graves of mostly young men who died for nothing but the lies of politicians and the profits of the politically-connected. Gold wanted no part of the slaughter. But politicians and bankers knew a paper fiat standard is the monetary means to accommodate it.

Conclusion

John Maynard Keynes, who coined the term barbarous relic in reference to the gold standard, wrote about the world that was lost when gold was abandoned:

What an extraordinary episode in the economic progress of man that age was which came to an end in August, 1914! . . . The inhabitant of London could order by telephone, sipping his morning tea in bed, the various products of the whole earth, in such quantity as he might see fit, and reasonably expect their early delivery upon his doorstep. . . He could secure forthwith, if he wished it, cheap and comfortable means of transit to any country or climate without passport or other formality, could despatch his servant to the neighboring office of a bank for such supply of the precious metals as might seem convenient, and could then proceed abroad to foreign quarters, without knowledge of their religion, language, or customs, bearing coined wealth upon his person, and would consider himself greatly aggrieved and much surprised at the least interference. But, most important of all, he regarded this state of affairs as normal, certain, and permanent, except in the direction of further improvement, and any deviation from it as aberrant, scandalous, and avoidable.

If Keynes had read what he wrote he mightve been a better economist. And we might be living in a better world today.

The content on this site is protected

by U.S. and international copyright laws and is the property of GoldSeek.com

and/or the providers of the content under license. By "content" we mean any

information, mode of expression, or other materials and services found on GoldSeek.com.

This includes editorials, news, our writings, graphics, and any and all other

features found on the site. Please contact

us for any further information.

Live GoldSeek Visitor Map | Disclaimer

The views contained here may not represent the views of GoldSeek.com, Gold Seek LLC, its affiliates or advertisers. GoldSeek.com, Gold Seek LLC makes no representation, warranty or guarantee as to the accuracy

or completeness of the information (including news, editorials, prices, statistics,

analyses and the like) provided through its service. Any copying, reproduction

and/or redistribution of any of the documents, data, content or materials contained

on or within this website, without the express written consent of GoldSeek.com, Gold Seek LLC,

is strictly prohibited. In no event shall GoldSeek.com, Gold Seek LLC or its affiliates be

liable to any person for any decision made or action taken in reliance upon

the information provided herein.