-- Published: Thursday, 23 January 2014 | Print | Disqus

Black Swans, Yellow Gold

by Michael J. Kosares

(The following is the second of a five-part series on how gold performs during periods of deflation, chronic disinflation, runaway stagflation and hyperinflation. The second installment examines golds safe-haven role during a disinflationary breakdown like the one in 2007-2008.)

The inability to predict outliers implies the inability to predict the course of history. . .But we act as though we are able to predict historical events, or, even worse, as if we are able to change the course of history. We produce thirty-year projections of social security deficits and oil prices without realizing that we cannot even predict these for next summer our cumulative prediction errors for political and economic events are so monstrous that every time I look at the empirical record I have to pinch myself to verify that I am not dreaming. What is surprising is not the magnitude of our forecast errors, but our absence of awareness of it.

- Nicholas Taleb, The Black Swan The Impact of the Highly Improbable, 2010

Having been mugged too often by reality, forecasters now express less confidence about our abilities to look beyond the immediate horizon. We will forever need to reach beyond our equations to apply economic judgment. Forecasters may never approach the fantasy success of the Oracle of Delphi or Nostradamus, but we can surely improve on the discouraging performance of the past.

- Alan Greenspan, The Map and the Territory, 2013

Introduction

This short study examines golds performance under the four most commonly predicted worst-case economic scenarios a 1930s-style deflation, chronic Japanese-style disinflation, a 1970s-style runaway stagflation, and a Weimar-style hyperinflation. That men do not learn very much from the lessons of history, Aldous Huxley once wrote, is the most important of all the lessons of history. Though I agree with Huxleys assessment when applied to contemporary policymakers and central bankers, I do not agree with it when applied to their counterparts in the private sector, i.e., the individual investors. As justification, I offer the ongoing (and long-term) success of the USAGOLD website as well as the soaring statistics of late on private gold ownership both here and abroad, most of which has been accumulated for safe-haven purposes. Individually, we can and do learn the lessons of history even if we do not always do so collectively.

Black Swans, Yellow Gold is dedicated to those who believe, like Nicholas Taleb, that it is just as important to prepare for what we cannot foresee as what we can. Some might put their money on the latest Oracle of Delphi or the contemporary reincarnation of Nostradamus or even an all-seeing eye plug-in that can be downloaded from the internet but in the end, such notions are the dreams of government planners and retired central bankers. For the rest of us, a solid hedge in gold coins, as your are about to read, is the more sensible and reliable alternative a wealth haven for all seasons.

We invite you to return to these pages periodically for the third installment in this series which we plan to publish next week.

Gold as a disinflation hedge (United States, 2008)

JUST AS THE 1970s REINFORCED GOLDS EFFICIENCY as a stagflation (combination of economic stagnation and inflation) hedge in the modern era, the 2000′s decade solidly established golds credentials as a disinflation hedge. Disinflation is defined as a decrease in the inflation rate over time (or a constant low inflation rate), and should not be confused with deflation, which is an actual drop in the price level. Disinflations, as pointed out above, are close cousins to deflations and can evolve to that if the central bank fails, for whatever reasons, in its stimulus program. Central banks today are activist by design. To think that a modern central bank would sit back during a disinflation and let the chips fall where they may is to misunderstand its role. It will attempt to stimulate the economy by one means or another. The only question is whether or not it will succeed.

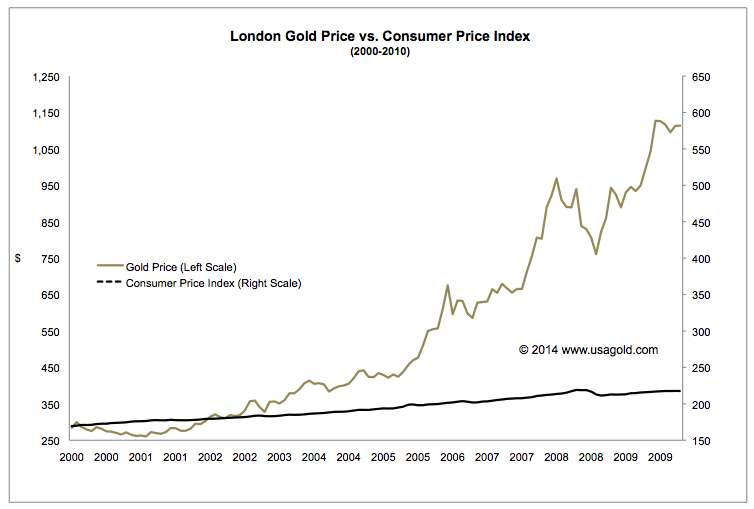

Up until the double oughts, the manual on gold read that it performed well under inflationary and deflationary circumstances, but not much else. However, as the decade of asset bubbles, financial institution failures, and global systemic and sovereign debt risk progressed, gold marched to higher ground one year after another. As events unfolded, it became increasingly clear that the metal was capable of delivering the goods under disinflationary circumstances as well. The fact of the matter is that during the 2000s even as the inflation rate hovered in the low single digits, gold managed to rise from just under $300 per ounce in the early 2000s to just over $1900 per ounce by 2011 a gain of over 600%. Since then, gold has taken a breather. As this essay is written, it is trading in the $1250 per ounce range still up over 400% in the new century.

In the aftermath of the 2007-2008 financial crisis something else happened to the yellow metal: It firmly re-established itself with private investors and nation states as perhaps the ultimate asset of last resort. As the economy flirted with a tumble into the deflationary abyss in recent years, it encouraged the kind of behavior among investors that one might have expected in the early days of a full deflationary breakdown with all the elements of a financial panic. Stocks tumbled. Banks teetered. Unemployment rose. Mortgages went into foreclosure. Nation states defaulted on their debts. Disinflation globally became chronic and debilitating.

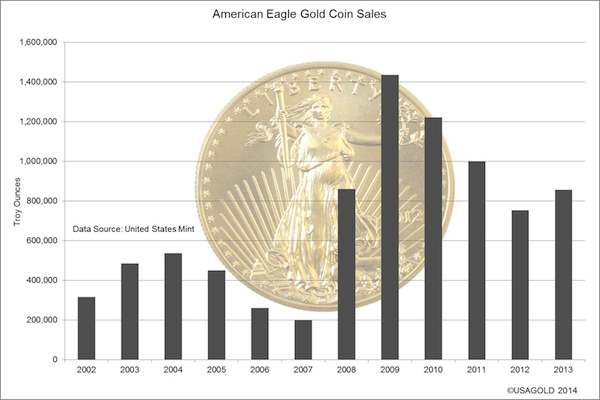

As it became evident that the economic and financial malaise could become a permanent fixture (the new normal), gold came under accumulation globally. In 2009, U.S. Gold Eagle sales, a bellwether for public interest in the metal, broke all records by a wide margin, and the pace of accumulation has remained at high levels ever since. The worlds central banks, historically at odds with each other with respect to currency policies, have teamed up to deliver ever larger doses of monetary stimulus that goes far beyond ordinary tinkering with interest rates. Money printing has become a global undertaking a phenomena the consequences of which are yet to be determined.

Meanwhile, the disinflationary crisis that began in 2007-2008 is still with us, and through it all, gold demand has gone undeterred. Though many thought the price correction would dampen interest, the opposite has happened: It encouraged a new wave of investment interest particularly in the East where low prices were greeted with a wave of public demand. In 2013, China reportedly imported nearly the equivalent of the world annual gold mine almost 2700 tonnes, and other emerging and developed nation states alike have experienced their own versions of a rush to own.

All in all, as the two graphs immediately above amply demonstrate, the 21st century ushered in a new era for gold, one in which it filled a hole in its resume. Now gold has come to be viewed as an effective hedge against one of contemporary economies most nettlesome problems chronic disinflation and the systemic financial risks it periodically imposes.

The content on this site is protected

by U.S. and international copyright laws and is the property of GoldSeek.com

and/or the providers of the content under license. By "content" we mean any

information, mode of expression, or other materials and services found on GoldSeek.com.

This includes editorials, news, our writings, graphics, and any and all other

features found on the site. Please contact

us for any further information.

Live GoldSeek Visitor Map | Disclaimer

The views contained here may not represent the views of GoldSeek.com, Gold Seek LLC, its affiliates or advertisers. GoldSeek.com, Gold Seek LLC makes no representation, warranty or guarantee as to the accuracy

or completeness of the information (including news, editorials, prices, statistics,

analyses and the like) provided through its service. Any copying, reproduction

and/or redistribution of any of the documents, data, content or materials contained

on or within this website, without the express written consent of GoldSeek.com, Gold Seek LLC,

is strictly prohibited. In no event shall GoldSeek.com, Gold Seek LLC or its affiliates be

liable to any person for any decision made or action taken in reliance upon

the information provided herein.