-- Published: Friday, 23 May 2014 | Print | Disqus

Last week, our theme was the Feds failure to generate a recovery through six years of historically easy monetary policy. In 2.6% Nuff Said and The Most Damning Proof Yet of Fed Failure, we demonstrated how the entire world is rapidly becoming wise to the Feds ineptitude and thus, the complete collapse of whatever remaining credibility it still has is not just inevitable but imminent.

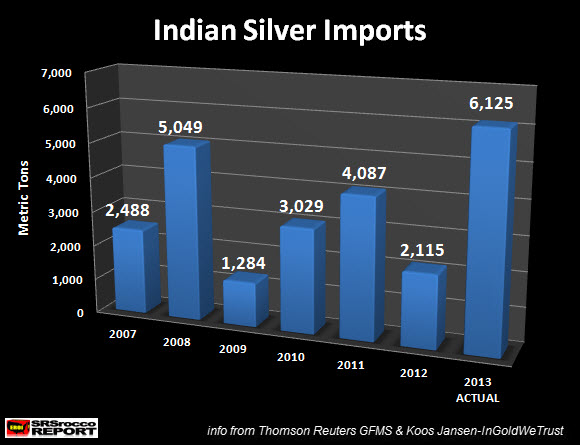

This week in Relax, Gold and Silver Owners This Is What Youre Up Against and Why Gold Cannot Lose In Simple Pictures, weve comforted readers that amidst the most heinous, blatant price suppression in modern history, gold and silver fundamentals have never been more powerful; particularly at current prices which are so far below the cost of marginal production it appears all but impossible to push them down much further. Oh yeah, that and the fact that global demand is surging from Russia, to China, to India the latter of which is on the cusp of seeing massive pent-up demand unleashed now that the gold-friendly Modi government is expected to reverse last years suicidal PM import restrictions which accomplished NOTHING but a proliferating black market.

SRS Rocco Report

As for the so-called reasons were supposed to fear PMs, lets take a ride through the wide world of horrible headlines starting with the Land of the Setting Sun, whose government may have perpetrated the biggest lie in history last week, in reporting 5.9% GDP growth in the first quarter. However, they clearly arent fooling anyone as by now the world is starting to realize the Bank of Japan is defending Nikkei 14,000 as zealously as the Fed is supporting interest rates in both cases to prove their hyper-monetary policies are working. Not to mention, that the Japanese economy is in FREEFALL as evidenced by this mornings reporting of a second straight contractionary PMI reading; which can only worsen significantly, now that the catastrophic national sales tax increase is in effect.

Meanwhile, China also reported a contractionary PMI this morning, whilst Europes was significantly lower than anticipated; i.e., on the cusp of outright contraction with key components like France deeply in recessionary territory already. Thus, with its gargantuan real estate/construction bubble is amidst an historic collapse, the PBOCs recent earth-shattering decision to weaken the Yuan will likely be maintained indefinitely causing a chain reaction yielding every imaginable economic misery from rising Chinese inflation to an acceleration of the final currency war. And as for Europe, its by now a fait accompli that Draghis Reckoning Day will be the ECBs June 5th meeting as nearly guaranteed by ECB board member Yves Mersche this morning.

And here in the United States of economic purgatory en route to hell once the Feds unprecedented globally destructive money printing, market manipulation, and propaganda scheme inevitably fails; the bad news stretches as far as the eye can see with no end in sight. But dont worry, all one has to do is repeat the word recovery over and over like theres no place like home and darn the facts, it must be so.

To wit, the Fed has been pronouncing recovery for 59 months now making it the third longest economic expansion in history, if only from the low water mark of the depths of the 2008 crisis; and yet, GDP growth was at best flat last quarter (yeah, I know, the weather was to blame). Not to mention, the Labor Participation Rate is at a 35 year low (and an all-time low for 20 somethings); median household income is at a 17-year low as prices of items we need versus want are at or near all-time highs threatening to explode care of generational droughts; and entitlements support more than half the population with horrific demographics guaranteeing a rapidly expanding dependency nation.

Zero Hedge

And oh yeah, the national debt has more than doubled in the past five years (including the off-balance sheet debts of Fannie Mae and Freddie Mac) with interest rates held at all-time lows via cancerous ZIRP and QE programs let alone, off balance sheet money printing like the swap programs the Fed openly admits to, per the below minutes of the April 30th FOMC meeting.

By unanimous vote, the Committee agreed to renew the dollar and foreign currency liquidity swap arrangements with the Bank of Canada, the Bank of England, the Bank of Japan, the European Central Bank, and the Swiss National Bank.

-Federal Reserve.gov, April 29-30, 2014

When propagandists are in charge everything is spun into the fraudulent fabric of recovery such as purporting a housing recovery, despite the fact prices are falling, inventories surging, mortgage applications at a 20-year low, household savings and equity at or near all-time lows, and even the nations largest benefactor of the Fed-generated echo bubble loudly disputing it.

BlackRocks Chief Executive Officer Laurence Fink said the U.S. housing market is structurally more unsound today than before the financial crisis because it depends more on government-backed mortgage companies like Fannie Mae and Freddie Mac.

-Bloomberg, May 20, 2014

This morning weve started the day with an unexpected negative reading of the Chicago Fed National Activity Index, a manufacturing PMI report featuring the weakest employment component of the year, existing home sales depicting the worst first trimester of the year since 2007, and a far higher than expected weekly jobless claims number; although, regarding the latter, if you read this brilliant article, youll realize weekly jobless claims improvements are in fact a fallacy with essentially no translation to the actual labor market. Then again, the aforementioned statistics regarding Labor Participation and median income let alone, the composition of such jobs currently focused on the temp, part-time, and minimum wage sectors scream this loud and clear. And for the coup de grace, heres a statement from Best Buy the worlds largest consumer electronics retailer.

As we look forward to the second and third quarters, we are expecting to see ongoing industry-wide sales declines in many of the consumer electronics categories in which we compete. Consequently, absent any major product launches, we are expecting comparable sales to be negative in the low-single digits in both quarters.

-24/7 Wall St, May 22, 2014

Which brings us to the third installment of this weeks comfort series i.e., the most foolish report ever written, so named in honor of yesterdays Fed Minutes which for the first time ever, I read fully.

Yes, I know its all about propaganda in convincing the market the Feds misinformation scheme regarding recovery and tapering is in fact true. As noted yesterday morning, such publications have become unrelenting key attack events; and yesterday was no different, as the PPT goosed stocks, the Fed supported Treasury yields, and PMs were attacked. That said, I figured Id actually read one of these reports to see what it is they actually do at these meetings; that is, before crafting said propaganda and organizing the accompanying market manipulations.

The propagandized headline was meeting participants discussed issues associated with the eventual normalization of the stance and conduct of monetary policy. However, it notes that decisions about the pace (of tightening) remain contingent on the outlook for the labor market and inflation

and

The Committee anticipates that, even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time warrant keeping the federal funds rate below levels the Committee views as normal in the longer run.

-FX Beat, May 21, 2014

And oh yeah, the Committees discussion of this topic was undertaken as part of prudent planning, and did not imply normalization would necessarily begin sometime soon.

And thus, despite MSM headlines blaring propaganda like Fed begins policy exit talks, the Fed made absolutely no change to its economic forecast, policy stance, or view of the risk factors or timing involved in making such decisions. Frankly, by undertaking such prudent planning though useless as an exit strategy can NEVER be implemented they were simply doing their job. Not to mention, with 73 people in the room and a world full of people watching their every move!

Frankly, reading the commentary behind the decision is like reading a bad science fiction article. To wit, a staff presentation outlined several approaches to raising short-term rates when it becomes appropriate to do so, and to control the level of short-term interest rates once they are above the effective lower bound, during a period when the Federal Reserve will have a very large balance sheet. Translation We killed hours theorizing how to manipulate markets once rates are no longer zero realizing that with a nearly $5 trillion bond portfolio held on massive leverage even the slightest rate increase will bankrupt us.

Better yet, how about this one written by people lauded as the nations top economic minds?

U.S. consumer prices

rose at a slow rate in the first quarter

and were about 1% higher than a year earlier. Many participants saw the recent behavior of food, energy, shelter, and import prices as consistent with a stabilization in inflation, and judged that the transitory factors that had reduced inflation, such as declines in administered prices for medical services, were fading. Most participants expected inflation to return to 2% within the next few years.

-FX Beat, May 21, 2014

So lets see here, with the U.S. Foodstuffs Index up 23% in the first quarter alone, gasoline prices up 5%, home rents at an all-time high (care of the Fed-created Wall Street engendered buy to rent boom), and the Shadow Stats alternate inflation index up 9%, were told inflation was up just 1%. Better yet, the behavior of said food, energy, and shelter prices was consistent with a stabilization of inflation. And best of all, the decline in administered prices for medical services which I certainly didnt experience at the doctors office is reversing. And thus, it is truly frightening that most participants anticipate price inflation returning to 2% within the next few years as if anyone has a clue what the world will be like in two years, let alone an institution with the worlds worst predictive track record.

Next up, the unemployment rate stayed at 6.7% in March, but both the labor force participation rate and employment-to-population ratio increased slightly. The rate of long-duration unemployment declined somewhat, but the share of workers employed part-time for economic reasons moved up; and both of these measures were still well above their pre-recession levels.

First off, the fact that labor force participation and employment-to-population increased slightly is misleading, considering both increased slightly from multi-month lows. And oh yeah, just one week after this report, both measures plunged to new lows in the April NFP report! As for the share of workers employed part-time for economic reasons moved up, Ill let you decide what this mumbo-jumbo means, as frankly, I havent a clue. And for the coup de grace, both of these measures were still above their pre-recession levels. Translation We continue to propagandize recovery from the 2008 crisis despite the fact that unemployment is significantly higher than before the crisis began!

And speaking of coup de graces, my all-time favorite pearl of Central banking wisdom

Federal Reserve communications garnered significant attention from market participants over the period. The communications following the conclusion of the March FOMC meeting were interpreted as somewhat less accommodative than expected. However, subsequent communications including the release of the minutes of the March FOMC meeting appeared to mostly reverse the earlier change in expectations.

-Federal Reserve.gov, April 29-30, 2014

In other words, an organization whose primary goal is price stabilization (whilst destroying 98% of the dollars value throughout its existence), which unilaterally changed this mandate to the paradoxical goals of price stabilization and full employment spends a great deal of time worrying about the stock market. In fact, the statement actually spoke of the Fed watching biotech and social media stocks specifically as if the price of Twitter was integral to their decision. And by the way, the reason the March meeting communication was subsequently seen as more dovish was because a fearful Whirlybird Janet gave a speech saying so just a week later!

Theres so much more of this foolish report such as their newfound obsession with the record low market volatility they have created through stock, bond, currency, commodity, and Precious Metal intervention. But instead, Ill simply summarize by stating that in reading the FOMC minutes of the April 30th meeting, I gained a new understanding of just how thin a tightrope TPTB are treading on. Such drivel exposes them as just as clueless as they are ineffective; and thus, our view that the Feds remaining credibility is on the verge of permanent collapse has only been strengthened.

Frankly, how anyone can avoid considering how their finances might look when this inevitable realization occurs is beyond me but fortunately, theres still time to make such decisions. And if you do, we hope youll give Miles Franklin a chance to earn your business!

Andrew C. Hoffman, CFA

Marketing Director

Miles Franklin Ltd.

ahoffman@milesfranklin.com

www.milesfranklin.com

| Digg This Article

-- Published: Friday, 23 May 2014 | E-Mail | Print | Source: GoldSeek.com

{kind=link}