-- Published: Monday, 2 June 2014 | Print | Disqus

By George Smith

The culprit responsible for the Crash and the Great Depression can be easily identified: government. To protect fractional reserve banking and (later) provide a buyer for its debt, government in 1913 created the Fed, putting it in charge of the money supply. From about July, 1921 to July, 1929 the Fed inflated the money supply by 62%, with the result being the Crash in late October, 1929. Government, following an aggressive do something program for the first time in U.S. history, intervened in numerous ways throughout the 1930s, first under Hoover then much heavier under Roosevelt. The result was not an easing of pain or an acceleration of recovery, but a deepening of the Depression, as Robert Higgs explains in detail.

The preceding is not, of course, the generally accepted explanation. In conventional discourse, one of the main culprits for causing or at least exacerbating the Depression was the international communitys adherence to the gold standard. Economist Barry Eichengreen popularized this view, and the Wikipedia entry for Eichengreen includes Ben Bernankes summary of Eichengreens thesis:

[T]he proximate cause of the world depression was a structurally flawed and poorly managed international gold standard... For a variety of reasons, including among others a desire of the Federal Reserve to curb the US stock market boom, monetary policy in several major countries turned contractionary in the late 1920'sa contraction that was transmitted worldwide by the gold standard.

Why would a money policy that turns contractionary be harmful? Because it puts the fractional reserve house of cards at risk. When the inflation is exposed and the golds not there, bankers do the Jimmy Stewart scramble. In Bernankes words,

What was initially a mild deflationary process began to snowball when the banking and currency crises of 1931 instigated an international "scramble for gold".

The states classical gold standard

The classical gold standard that was in operation throughout the West for much of the 19th century was in fact a fiat gold standard, meaning it operated at the pleasure of the state. When the state was not pleased with its operation, it suspended it, allowing banks to break their promise to redeem paper currency and deposits in gold coin on demand.

But even under the auspices of the state, the classical gold standard kept a lid on inflation. Gold was money, and the national currencies were names for a certain weight of gold a dollar was a name for 1/20 of an ounce of gold, for example. A dollar was not a money backed by gold because a dollar was not money. It was a conditional substitute for the real thing. The only thing governments and their banks could directly inflate were their currencies, and if they inflated too much they would lose gold through arbitrage opportunities to countries that didn't inflate as much. In other words, they couldnt stay on the classical gold standard and print a lot of money.

Robert Murphy provides an example of golds check on inflation in his book, The Politically Incorrect Guide to the Great Depression and the New Deal: To give an extreme example, if the dollar depreciated to $10 per pound, then owners of gold could make a killing. They could sell an ounce of gold in England at 4.25 pounds (the legally defined value of the pound). Then they could enter the currency markets and receive 42.5 American dollars for the 4.25 pounds (because of our assumed $10 exchange rate). Then they could present the $42.50 in U.S. currency to the United States Treasury and demand the legally defined payment of roughly 2.06 ounces of gold (because one ounce of gold was defined as $20.67). Thus, absent shipping and other costs, the gold owners would be able to more than double their gold holdings through this arbitrage action. [pp. 93-94]

As gold was transferred to England, British prices would rise. But as the U.S. lost gold to England, it would be pressured to reduce the number of dollars it created, and prices in the U.S. would fall. Consumers would start buying less from English producers and more from American producers, reversing the trade imbalance, and the exchange rate would gradually fall from $10/pound to $4.86/pound.

With the advent of WW I the belligerent governments ordered their central banks to stop redeeming their currencies in gold. The gold standard wouldnt permit a long war there was not enough gold to pay for one. By inflating they not only killed millions of people, they killed the classical gold standard. Monetary stability was replaced with monetary chaos.

After the war, the inflated money supplies and price levels presented governments with a choice: return to the classical gold standard at lower exchange rates or return to the pars existing before the war. Britain, in an attempt to re-establish London as the worlds financial center, chose to go back to its old par of $4.86. One alternative would have been to impose a severe deflation but that was not a serious consideration, nor was it necessary. If the governments were determined to stay on the classical gold standard, they wouldve stayed with the post-war parities.

The new gold standard

At the Genoa Conference of 1922 and with the architecture of the monetary order firmly in governments hands, representatives from 34 countries met to discuss what to do about money. The problem was obvious. Just when governments had needed money the most to engage in war gold had let them down. It had proved exceedingly unpatriotic. On the other hand, paper money, like the girl from Oklahoma, couldnt say no. It saluted whatever plans government devised. The problem, therefore, wasnt too much paper the problem was too little gold.

Golds scarcity was now its fatal flaw. But the scientists in charge of its fate werent ready to announce that the money people had been using for 2500 years had suddenly become dangerous to their economic well-being. So, they gave it a small support role while displaying its name prominently on the marquee of their new scheme, the gold-exchange standard. Here was the deal they cut:

1. The United States would stay on the classical gold standard, meaning people could exchange $20.67 in currency and coin at the Treasury for one gold ounce coin.

2. Britain would redeem pounds in gold and U.S. dollars, while other nations would pyramid their currencies on pounds.

3. Britain would only redeem pounds in large gold bars. Gold was thereby removed from the hands of ordinary citizens, allowing a greater degree of monetary inflation.

4. Britain also pressured other countries to remain at overvalued parities.

In sum, the U.S. pyramided on gold, Britain on dollars, and other European countries on pounds. When Britain inflated, other countries inflated on top of their pounds instead of redeeming them for gold. Britain also induced the U.S. to inflate to keep Britain from losing its stock of dollars and gold to the U.S.

It was an international inflationary arrangement with gold brought along for the ride, to give it the appearance of stability and prestige. When it collapsed, as it was bound to, gold served as the scapegoat.

Gold gets a prison sentence

Keynesian and other monetary scientists claim to have a smoking gun.

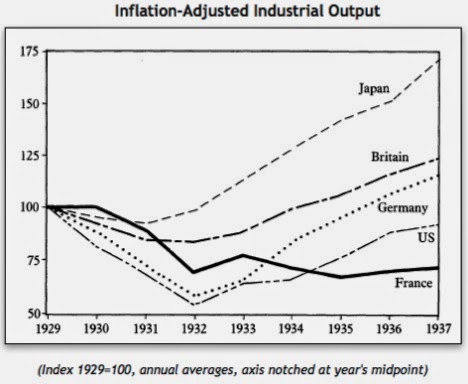

In this chart, taken from a paper by Barry Eichengreen and reproduced by Robert Murphy, the output for each country is set to 100, then subsequent measures are a percentage of its deviation from the 1929 benchmark.

In some chronologies the chart reflects the order in which the countries went off gold, with Japan first, then Britain, Germany, U.S., and finally France. In Germany and the U.S., industrial output experienced a significant rebound from 1932 to 1933. But the U.S. didnt go off gold until almost mid-1933, yet industrial output was already rising. Then it mostly flattened before rising when the dollar was again tied to gold.

As Murphy notes, whatever the discrepancies in the chart, it allegedly shows the beneficial effects that devaluation plays out over time. Yet the Depression lasted well beyond 1937, with double-digit unemployment rates persisting throughout the 1930s.

Previous depressions had been over in 2-3 years without confiscating peoples gold. Why did it suddenly become a major culprit in the 1930s?

And what did it mean to go off gold? It meant any U.S. citizen who didnt obey FDRs order to turn in his gold was subject to a $10,000 fine and a 10-year prison sentence this, for possessing the monetary choice of tens of millions of market participants. It meant anyone around the world holding dollar-denominated assets, thinking they could redeem them in gold, got stiffed. Is this how you build confidence in governments ability to restore prosperity?

Also, is it really surprising economic conditions improved after going off gold? Murphy likens this to an individual homeowner holding a 30-year mortgage on his house declaring hes going off his mortgage. He says to his mortgage holder, Im not paying you anymore. And I have more guns than you, so tough.

With no mortgage to pay its no surprise that the homeowners standard of living rises after going off his mortgage. Just because you achieve short-term prosperity by relieving yourself of certain contractual obligations doesnt prove those obligations were bad.

Conclusion

Government never wants to lose the ability to inflate. To surrender it would be to surrender sovereignty over money, and it will never do that. Not willingly. Its sometimes said that if people understood what government was doing they would rise up in protest. But when was the last time you saw average Americans rise up in protest on a national level? Most Americans are grateful they can pay their bills. If the digits they use pays the bills why should they care?

For the same reason people cared in the Great Depression. They had trouble paying their bills. So they accepted the governments new currency.

If the Austrian theory of the trade cycle is correct, that is, (quoting Murray Rothbard), if government depression policy has always

aggravated the very evils it has loudly tried to cure, then another crisis is in the works. And when the next one arrives, people will again have trouble paying their bills. Perhaps it will occur to them that not only are they being cheated and their liberty seriously diminished, they can do something about it.

Perhaps then books like Rothbards What Has Government Done to Our Money?, which Depression-era people did not have, will acquire the attention they deserve.

http://barbarous-relic.blogspot.com/

| Digg This Article

-- Published: Monday, 2 June 2014 | E-Mail | Print | Source: GoldSeek.com

{kind=link}