-- Published: Friday, 6 June 2014 | Print | Disqus

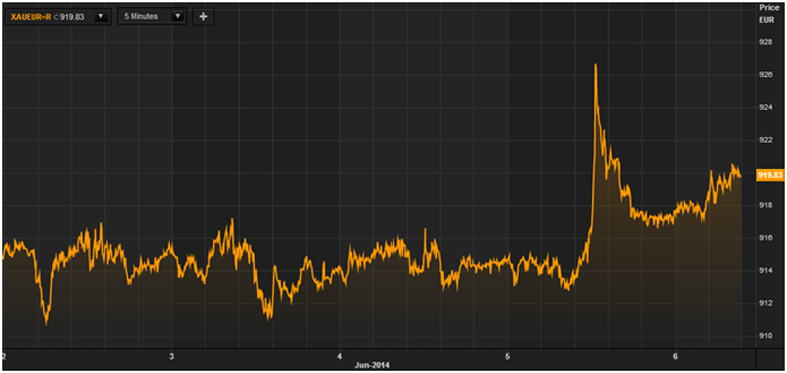

Gold surged 1.6% in euros to 928 per ounce after the historic ECB announcement to adopt negative interest rates. Gold subsequently gave up those gains but was still 0.8% higher on the day to 919 per ounce. In dollars, gold climbed $9.40 or 0.76% yesterday to $1,253.10 per ounce.

Gold in Euros -This Week - (Thomson Reuters)

Overnight, Singapore gold traded in a tight range between $1,252/oz and $1,257/oz and in London, gold has held yesterdays gain. Gold is heading for a weekly increase of 0.5%.

Todays AM fix was USD 1,254.00, EUR 919.96 and GBP 745.90 per ounce.

Yesterdays AM fix was USD 1,244.75, EUR 914.45 and GBP 742.69 per ounce.

Futures trading volume remains lacklustre and was 42% below the average for the past 100 days for this time of day, according to data compiled by Bloomberg. This week gold bullions 60 day historical volatility fell to the lowest since April 2013.

Today, markets await the U.S. jobs number for clues regarding the strength of the struggling U.S. economy. The consensus is that the government data today may show the U.S. added 215,000 jobs in May.

Gold touched session highs near $1,250/oz on Wednesday and the dollar and U.S. stock index futures fell after the poor ADP jobs number. The poor ADP number may indicate todays jobs number could also be weaker than expected.

As ever, a better than expected jobs number, could see gold come under pressure and see further gold liquidations. Conversely, a worse than expected number should lead to a safe haven bid today and could be a catalyst contributing to gold getting out of its recent funk.

Yesterdays ECB decision is actually much more important to the long term outlook for gold.

The ECB made a historic decision and became the first major central bank to take the extraordinary step of charging interest on deposits. ECB President Mario Draghi cut the deposit rate to minus 0.1% and lowered the key interest rate to a record 0.15%.

While the euro strengthened against the dollar by the end of trading, it fell against gold. This suggests the move may not have the desired effect of lowering the value of the euro. Market participants may realise that competitive currency devaluations are set to continue and no major nation is, at this time, willing to see its currency appreciate versus another major trading partner.

The ECBs move should lead to the euro further weakening against gold and increase demand for gold in Europe as investors move to hedge their euro exposure. Hard pressed savers may also allocate some of their non yielding savings to gold.

Ultra loose monetary policies, negative interest rate policies (NIRP) and the possibility of the ECB printing euros to buy bonds will make the gold shorts nervous and should contribute to a pickup in demand for gold - especially in Europe.

European stocks and bonds rose today, buoyed by the ECB's promise of another tidal wave of money.

Benchmark 10 year yields on Italian, Spanish and Irish government bonds all plunged to their lowest ever in early trading on Friday, with the Irish yield almost 10 basis points below comparable U.S. borrowing costs.

The global bond bubble just got more bubbly

it is unlikely to end well.

Stock markets, following Wall Street's march to yet another record peak on Thursday, rose too, with high risk bank shares leading the way. The pan European index of Europe's leading 300 shares is on track for its eighth consecutive weekly gain as irrational exuberance continues in global markets.

Gold in Euros -2 Years - (Thomson Reuters)

Germany saw loud criticisms of the recent move, both from the political spectrum but also from the industry, finance, banking and pension sectors. German saver and pension groups expressed their fear, long echoed here, that hitting banks profits would merely prompt them to cut their interest payments to ordinary savers.

A senior member of German Chancellor Angela Merkels coalition joined banks, insurers and pension companies in denouncing the ECBs historic gamble.

Critics of the ECB President Mario Draghi said he is debasing the currency and expropriating German savers. Ralph Brinkhaus, the finance spokesman in parliament for Merkels Christian Democrats, said in an e-mailed statement that the ECB has to watch out that it doesnt exceed the limits of its mandate, according to Bloomberg.

Draghis decision, reopened a rift between Merkel and German economists and lawmakers who are concerned about currency devaluation and the risk of inflation.

The ECBs decision will go down in the history books as ineffective, the Berlin-based VoeB state banks federation said. The historic low interest rate will undermine efforts of millions of Germans to save for retirement, said the GDV, which represents Allianz SE and Talanx AG.

The bill is being footed by all of those who are investing money for the long term, the savers and holders of life insurances, Sinn said.

Alternatively for Germany, the growing anti-euro protest party that won 7% of the vote in European elections this month, renewed its call to dismantle the single currency.

Draghi is exclusively concerned with holding the euro area together at any price and his policy amounts to expropriation of savers, Joachim Starbatty, a University of Tuebingen economist, said in a statement from the party.

Starbatty was among plaintiffs who lost a bid in 2011 to get Germanys constitutional court to stop German participation in the first bailout for Greece, the country that set off the euros debt crisis in 2009.

And Germans have to pay the bill once again, he said today.

GoldCore Conclusion

It is not just Germans that are paying the bill of the ECBs policies. Mr Starbatty should go and meet hard pressed taxpayers in Ireland, Cyprus, Greece, Spain, Italy and Portugal. He should also go and meet hard working savers in all countries who are being penalised by the ECBs ongoing financial repression.

Struggling taxpayers have been lumbered with the huge debts of reckless and insolvent banks.

The challenge across Europe is massive levels of debt across all stratas of society. This challenge of huge debt levels will not be addressed by reducing interest rates to zero or negative interest rates. The scale of the debts is too great for this.

The only long term sustainable solution is to have a comprehensive debt restructuring and debt forgiveness programme in the EU and indeed globally.

The key problem today is not the cost of money or borrowing, it is the scale of the debts. Printing euros to buy bonds will only compound the problem as more debt is piled upon existing debt. When interest rates eventually rise, which inevitably they will, the increased levels of debt and the impaired ECB balance sheet will see a problem of greater magnitude than the one seen in recent years.

A failure to address this and adopt a programme of debt restructuring and debt forgiveness will lead

to the failure of the monetary union. As periphery nations will be left with no choice but to revert to their national currencies in order to prevent economic dislocations and collapse.

Ultra loose monetary policies have not worked in the U.S. since 2008 or in Japan where interest rates have been below 2% for more than 13 years, since 2000.

Why on earth should this gamble work in the EU?

The Germans have long been vocal about the risks that this would not work and it would lead to currency debasement. However, the consensus view amongst many experts and much of the media has been to ignore the Germans as their historical experience makes them paranoid about inflation.

But, what if the economic consensus is wrong again? As it was prior to the financial crisis.

And what if the Germans are right? We have long said that we believe the Germans are right to look to their history and learn the lessons of the past.

Maybe the cosy consensus that the panacea to this crisis is more cheap money, competitive currency devaluations and currency debasement is wrong?

Gold in Euros - 5 Years - (Thomson Reuters)

As we said yesterday, cheap money, financial repression and currency debasement are classic recipes for short term financial and economic gains. Throughout history, they have been the easy options for emperors, kings, queens and governments. They are the easy option of central banks today.

However, throughout history currency printing and money debasement have never been a recipe for creating jobs and for long term sustainable economic growth and prosperity. Indeed, they inevitably lead to the general populace suffering the ravages of inflation.

The ramifications of todays extreme ultra loose monetary policies, that are being seen internationally, are yet to be realised. Complacency abounds.

Will banks respond by beginning to charge savers an interest rate for their deposits? Savers, the backbone of the our capitalist system, are already suffering from negative real interest rates with bank deposits generally yielding less than government headline inflation in many countries.

Further financial repression, could be the last straw which breaks the laden camel's back.

Indeed, it could lead a minority of depositors to remove some their cash from already vulnerable banks and deposit them in less risky banks internationally that offer a yield. It could also lead them to invest in safer assets that offer a yield such as AAA rated government and corporate bonds - thereby weakening an already fragile banking system.

Gold has always been criticised due to its lack of yield, unlike stocks, bonds and deposits. However, given the ECBs historic decision yesterday and the continuation of ultra loose monetary policies, many investors and depositors will now rightly see non yielding gold as an increasingly attractive diversification.

| Digg This Article

-- Published: Friday, 6 June 2014 | E-Mail | Print | Source: GoldSeek.com