-- Published: Monday, 13 October 2014 | Print | Disqus

By Arkadiusz Sieron

Teaser: Many investors believe that the federal funds rate is adversely related to the gold price. Interest rate cuts are perceived as a sign of cheap money policy a bullish signal in the gold market. Similarly, the rise of the federal funds rate is considered as detrimental for gold prices. However, it seems that real interest rates are more important than nominal ones. Are changes in the federal funds rate a good predictor of gold prices, then?

Gold and Federal Funds Rate

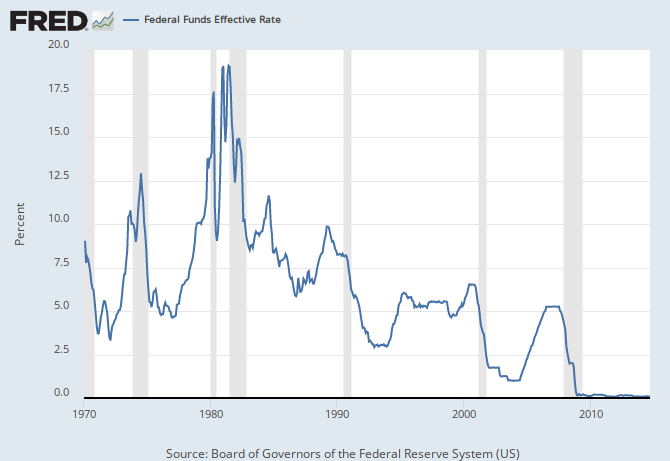

Many investors believe that the federal funds rate is adversely related to the gold price. Interest rate cuts are perceived as a sign of cheap money policy a bullish signal in the gold market. Similarly, the rise of the federal funds rate is considered as detrimental for gold prices. Recent events are the best example. The last drop in the gold price was contributed to by expectations of faster hikes of the federal funds rate. Although this relationship may often hold, investors should be skeptical about this rule of thumb. There are many cases when an increase in this rate was accompanied by parallel moves in the price of gold. From 1971 through 1974, the federal funds rate rose from 5 to 10%, while the gold price flew from $35 to $200 per ounce. Similarly, between summer 2004 and 2006 the funds rate soared from 1 to 5.25%, while the gold price rose from $400 to $700.

Graph: Gold price (red line, right scale) and effective federal funds rate (blue line, left scale) from 1970 to 2014

Source: research.stlouisfed.org

Why the changes in the federal funds rate are not the best predictor of gold prices? First, real interest rates are more important than nominal ones. This is why the federal funds rate soared from 1977, peaking at more than 20 percent in 1980, and gold reached a peak of $850 per ounce in the same period. Though nominal interest rates soared, the real interest rates remained negative (because of the stronger rise in the inflation rate), causing the rise in gold prices.

Second, a low federal funds rate enables commercial banks to borrow cheap money from the central bank to buy assets yielding higher interest rates, i.e. bonds and stocks, or to lend them to consumers or entrepreneurs. When the federal funds rate falls, the interest-bearing assets seem to be more attractive than precious metals. When borrowing at 1%, it is better to buy bonds bearing 1.5% than gold (at least most investors will very likely see it this way). Similarly, when the federal funds rate rises, gold becomes relatively more attractive than many interest or dividend bearing assets. In other words, the rise of the interest rates lowers the price of bonds and stocks. Therefore, when the bond or stock bubble bursts, investors may reallocate their funds from equity and bond markets to the precious metals market.

Third, the rise in the federal funds rate, which means a higher price for shorter-term credit, does not guarantee a deceleration in money supply growth, which is more important for the gold market. The current period of extremely low interest rates has shown that the money supply can be raised (remember quantitative easing?) without changing the federal funds rate.

Even with a raised rate of federal funds, the price of gold does not have to fall. This is because the changes in the interest rates cannot be analyzed in isolation from the economic context, especially the movement in the real interest rates. Therefore, if CPI inflation remains at around 2%, real rates will stay negative or extremely low, unless the nominal rates rise to more than 2% (the current 1 year Treasury bill yield is 0.1%), which still seems to be a matter of the rather distant future (with the federal funds rate at 0.25%).

Summing up, the real interest rates are much more important for the gold market that sole changes in the federals funds rate. We analyze both factors in our Market Overview reports and we discuss events important for short-term traders in our Gold & Silver Trading Alerts for traders. We encourage you to stay updated on the latest free essays that we publish in both areas by joining our gold newsletter. Its free and you can unsubscribe in just a few clicks.

Thank you.

Arkadiusz Sieron

Sunshine Profits Market Overview Editor

| Digg This Article

-- Published: Monday, 13 October 2014 | E-Mail | Print | Source: GoldSeek.com

{kind=link}