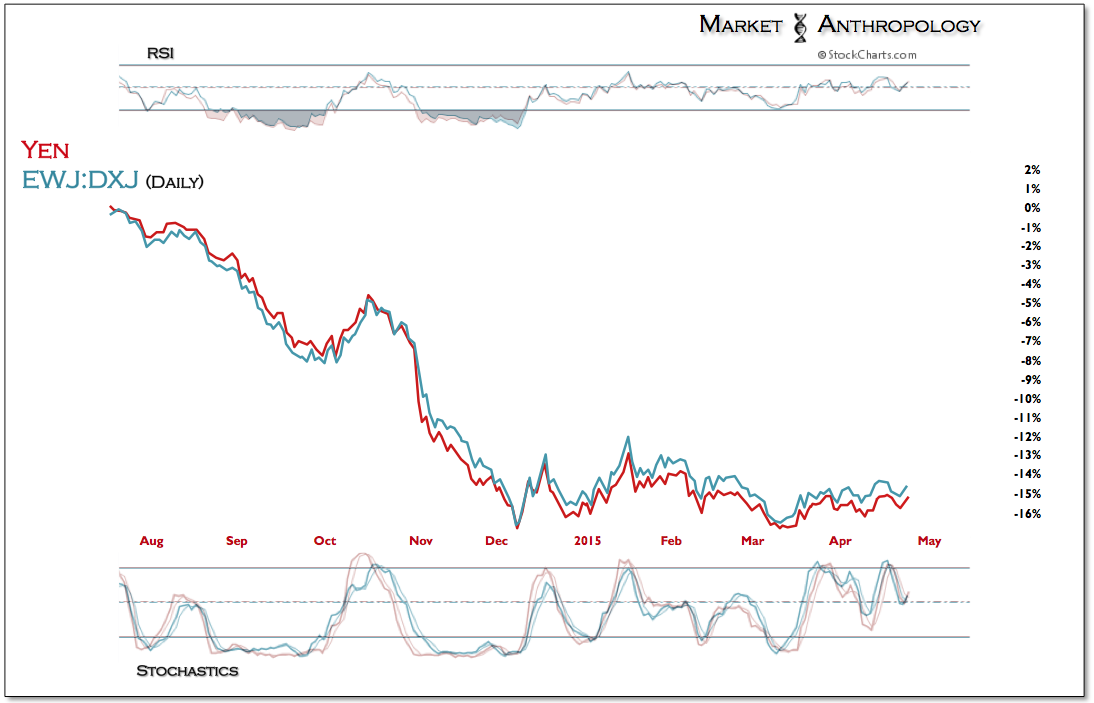

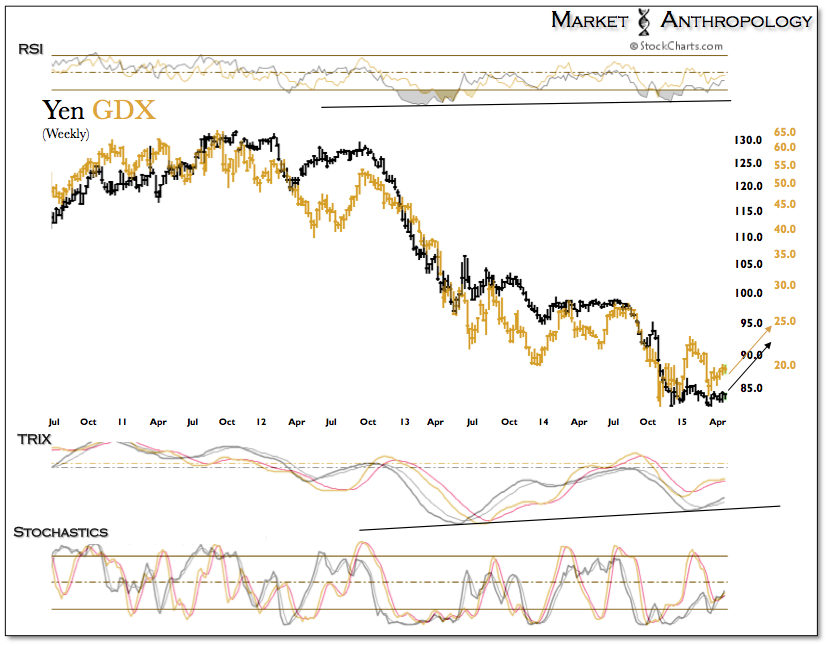

Over that same timeframe, the yen has fallen sharply, weakening ~15 percent and making currency-hedged ETFs, such as Wisdom Tree's Japan Hedged Equity Index - DXJ, widely outperform non-hedged equity indexes such as iShares - EWJ.

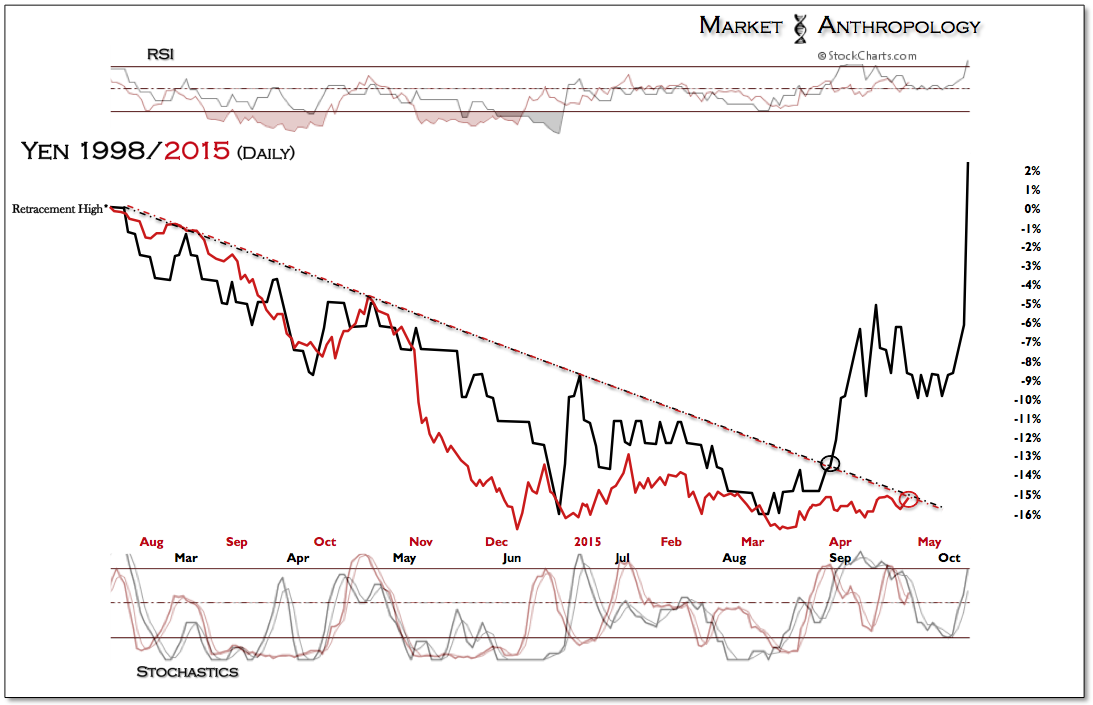

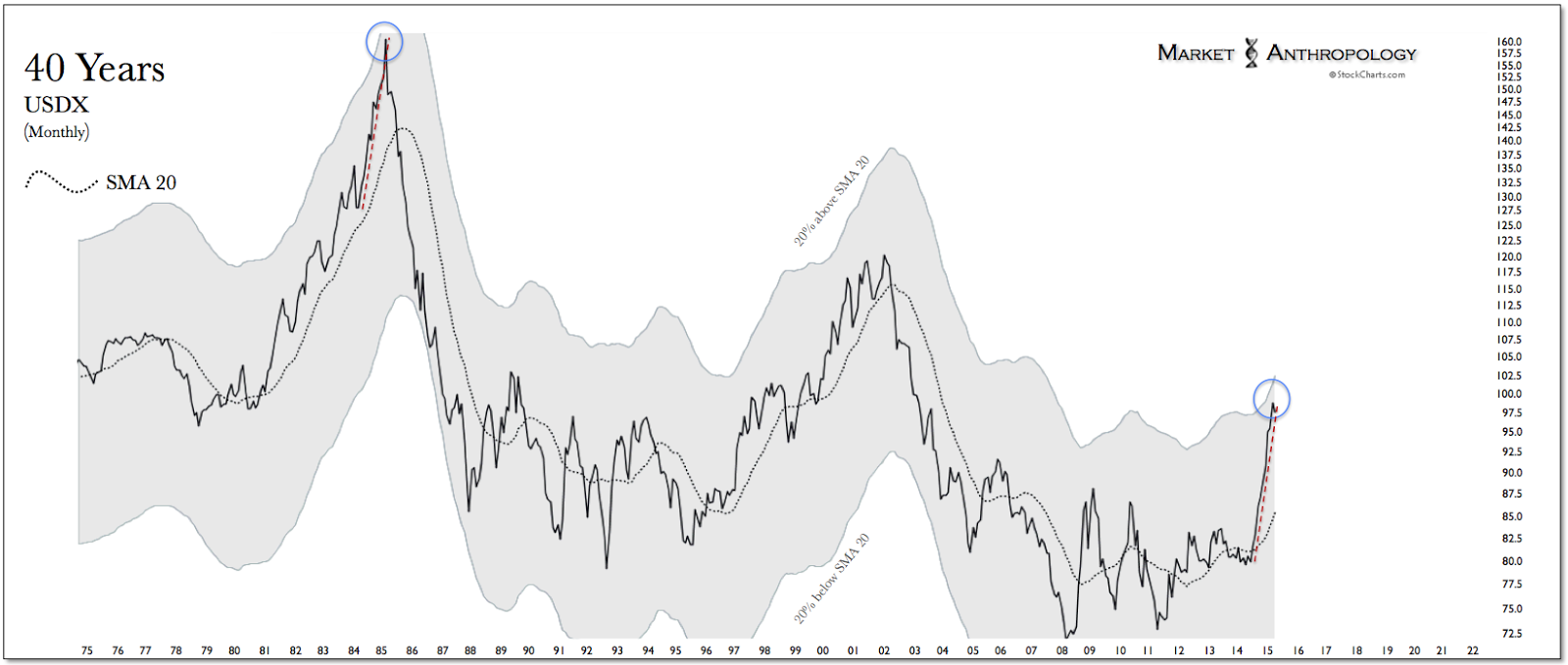

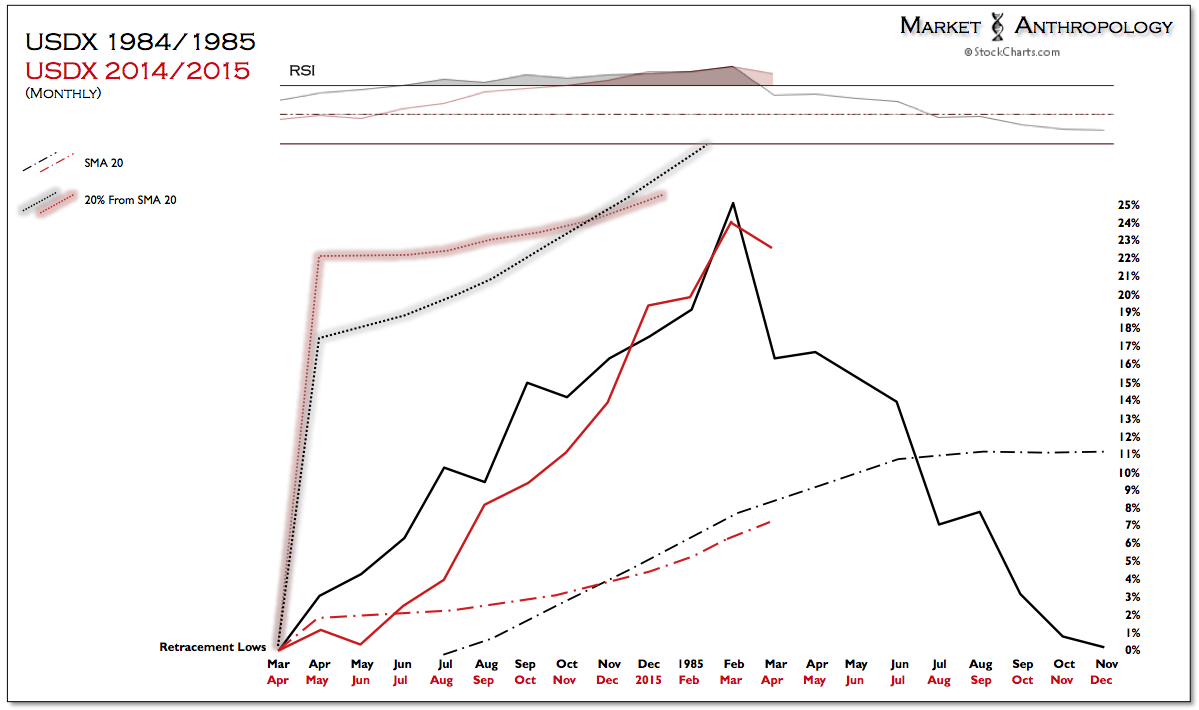

With a much anticipated April 30th Bank of Japan meeting on deck next week, we find the yen curiously situated near critical long-term support, while feathering a potential breakout from last summer's large leg lower.

Over the past few months, the drum-beat for expanding the BOJ's already significant quantitative easing program have grown louder, as inflation continues to miss their 2 percent target and as Prime Minister Shinzo Abe won a major political victory this past December. As such, respected members of Abe's ruling party - such as Kozo Yamamoto, have become outspoken proponents of further easing, recommending increasing asset purchases of government and corporate bonds as well as ETFs.

While we continue to remain bullish on Japanese equities over the long-term (especially relative to the U.S.), the BOJ's appetite for influence here with the yen remains suspect. Although further easing is more likely at some point later this year, the consequences of "beggar thyself" policies have had significant negative affects on the purchasing power of Japanese households and squeezed corporate profits in Japan.

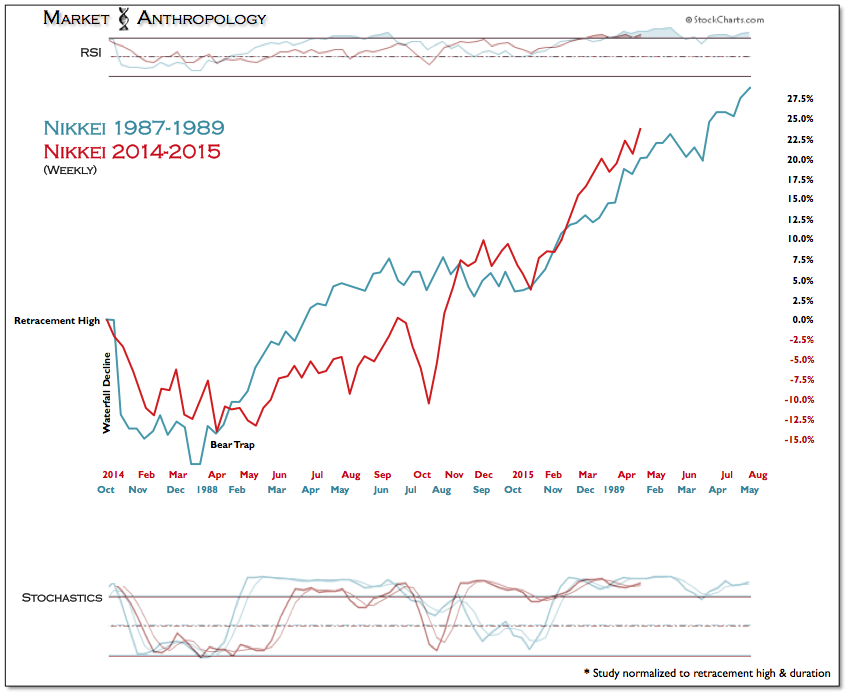

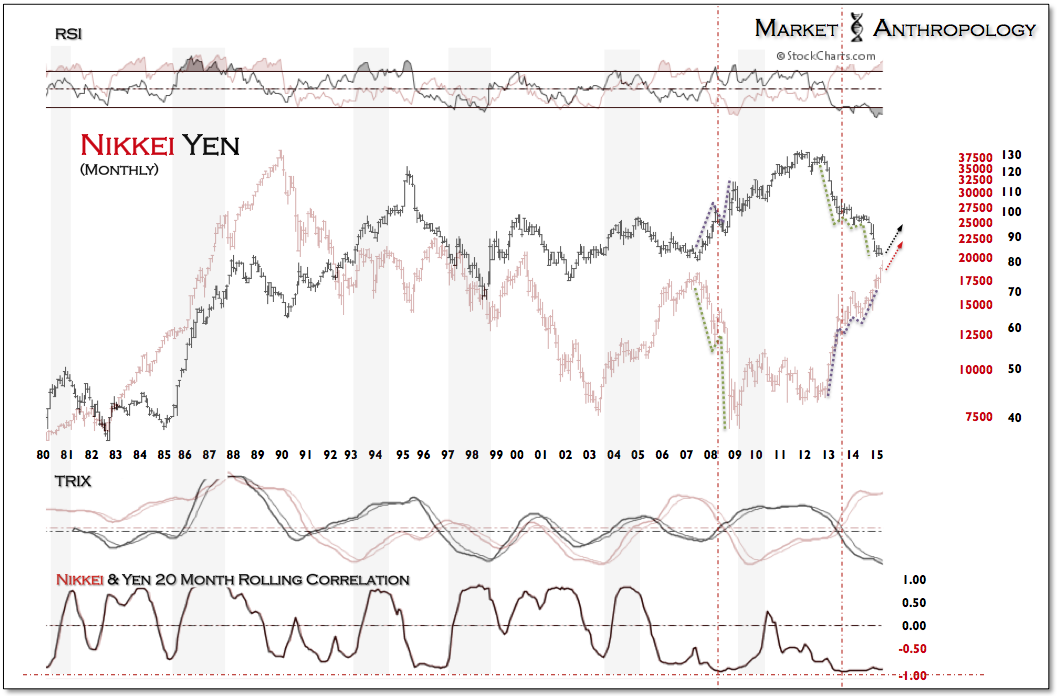

With the yen currently situated on long-term support, will the BOJ risk destabilizing the foreign exchange market if they surprise the markets next week? Our educated guess is no - and expect that the yen and Nikkei will continue to move out of the negative correlation extreme they have traded in over the past two years.

Because of this, we continue to favor an unhedged equity position in Japan and still like the prospects for gold - which have moved in lock-step fashion with the yen and broadly disappointed over the past year.

Click to expand image