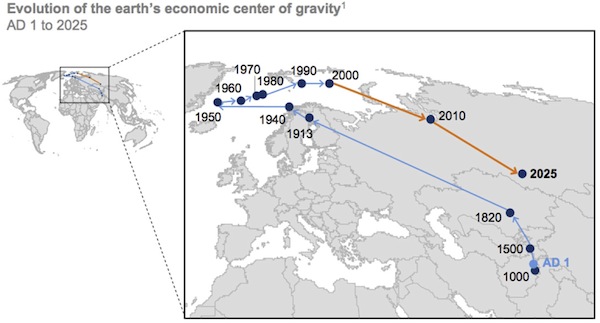

It wasnt that many centuries ago that China was the absolute economic center of the world. That center gravitated to Europe and then towards North America and has now begun moving back to China. My colleague Jawad Mian provided this chart showing the evolution of Earths economic center of gravity from 2000 years ago to a few years and into the future:

Most investors are well aware of the enormous impact China has had on the modern world. Thirty-five years ago Chinas was primarily an agrarian society, with much of the nation trapped in medieval technologies and living standards. Today 500 million people have moved from the country to the cities; and Chinas urban infrastructure is, if not the best in the world, close to that standard.

The economic miracle that is China is unprecedented in human history. There has simply been nothing like it. Deng Xiaoping took control of the nation in the late 70s and propelled it into the 21st century. But now the story is changing. Those who think that all progression is linear are in for a rude awakening if they are betting on China to unfold in the future as it has in the past.

Among the most important questions for all investors and businessmen is, how will China manage its future and the problems it faces? There are many problems, some of them monumental and at the same time there is an amazing amount of opportunity and potential. Understanding the challenges and deciphering the likely outcomes is itself an immense challenge.

A Brand-New Book Available Online

My colleague Worth Wray and I have been investigating and writing about China for some time now. Today Im announcing a book that we have written and edited in collaboration with 17 well-known experts on China. The book is called A Great Leap Forward? Making Sense of Chinas Cooling Credit Boom, Technological Transformation, High Stakes Rebalancing, Geopolitical Rise, & Reserve Currency Dream, and we think it will help you to a solid understanding of both Chinas problems and its opportunities. I know, the subtitle is a tad long, but the book does really cover all those aspects of todays China.

Notice that there is a ? after the title A Great Leap Forward. The first Great Leap Forward, initiated by Mao Tse-tung in the early 60s, was an utter disaster. It devastated the nation, bankrupted the economy, and caused the deaths of tens of millions of people. Lets review a little history from the introduction to the book:

When Chairman Mao decided in 1958 to transform Chinas largely agrarian economy into a socialist paradise through rapid industrialization, collectivization, and a complete subjugation of the market to Chinese Communist Party (CCP) central planners, the widespread misallocation of resources led to the worst famine in recorded history and the outright collapse of Chinas economy.

With very little capital at Chinas disposal after its long civil war and even longer subjugation to foreign colonialists in the nineteenth and early twentieth centuries, Mao decided the best way to fund the countrys rapid industrialization was for his government to monopolize agricultural production, use the nations bounty to support industrializing urban populations, and finance fixed-asset investments with crop exports.

1959 Prosperity brought by the dragon & the phoenix

Seeing grain and steel production as the essential elements of Chinas rapid development, Mao boasted in 1958 that China would produce more steel than the United Kingdom within fifteen years.

1959 Smelt a lot of good steel and accelerate socialist construction.

Mao had very limited knowledge of agriculture or industrial production, yet he ruled China with an iron fist and silenced even well-intentioned opposition. Chinas rural peasants were forced into collectives; households were torn apart; and private property rights were completely abolished. Mao ordered agricultural collectives to produce more grain while forcing farmers to employ less productive methods; he mobilized farmers to kill off pests like mosquitos, rats, flies, and sparrows (a campaign that upset the ecological balance in Chinas farmlands); and insisted on a doubling of steel production to be achieved by diverting farmers with no industrial skill into operating poorly supplied backyard furnaces (which could not burn hot enough to produce high-quality steel).

1959 Unskilled workers smelt steel in Chinas backyard furnaces.

Steel production surged, and the economy appeared to boom

but at least half of that new production was unusable. A proliferation of crop-eating locusts (after the sparrows had been killed off) and the diversion of farm workers to industrial and public works projects led to a collapse in crop yields. Still, local officials all over China falsified their production figures in an effort to win favor with Beijing (and to spare themselves Maos wrath), which led to larger and larger grain shipments to Chinas cities

and smaller and smaller rations for those living in its agricultural collectives.

Instead of taking a Great Leap Forward to a harmonious industrial society

1959 The commune is like a gigantic dragon, production is noticeably awe-inspiring.

Maos command-and-control system dismantled the Chinese economy, ruined millions of lives, and left an enormous share of Chinas population disillusioned.

Industrialization failed. From 1958 to 1961, millions died of starvation and exhaustion across Chinas countryside (independent estimates range from 30 million to 70 million, while the CCP still insists the death toll was only 17 million), and the Peoples Republic remained a net exporter of grain. As Harvard economist Dwight Perkins remembers it, Enormous amounts of investment produced only modest increases in production or none at all.... In short, the Great Leap was a very expensive disaster.

As production and productivity collapsed along with the CCPs social contract, Mao struggled to retain power as a number of influential officials sought to implement more market-oriented policies in response to the Great Famine. Fearing that growing opposition could lead the Party to reject its Marxist spirit (as the Soviet Union had done under Nikita Khrushchev a decade earlier), in 1966 Mao and his Red Guards launched the Cultural Revolution a decade-long series of purges intended to root out enemies of Communist thought lurking within the Party, cleanse Chinese society of many of its traditional values, eliminate elitist urban social structures, and renew the spirit of Chinas Communist revolution.

1967 Scatter the old world, build a new world.

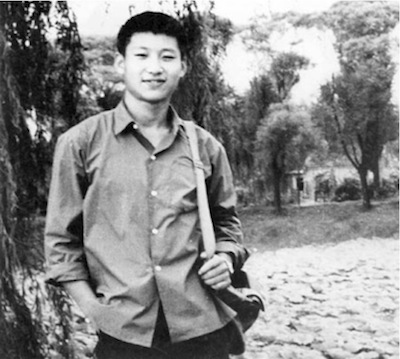

Under Maos leadership, the Party destroyed cultural artifacts, banned the vast majority of books, dismantled the educational system, and silenced millions for thought crimes against the Party. In a devastating blow to Chinas human capital, Mao ordered children of privileged urban families including current President Xi Jinping, when his father, Xi Zhongxun, was purged to relocate far away from their families to be re-educated through manual labor in Chinas countryside. What may have been the most promising youth of that Lost Generation were deprived of their educations and forced into hardship.

1972 President Xi Jinping during the Cultural Revolution

Considering the legacy of the Great Leap Forward, the Great Chinese Famine, and the Cultural Revolution, it is an understatement to say that Maos hardline policies devastated the economy and left deep scars at all levels of Chinese society. After Maos death in 1976, it didnt take long for the pragmatic Deng Xiaoping to win control of the Party and take China in a new economic direction though with essentially the same repressive political system.

And now young XI Jinping has come from experiencing the Cultural Revolution, getting ready to embark upon what we believe is something as equally as revolutionary as the first Great Leap Forward. The question mark is whether it will be another disaster or a decisive leap into a new future, perhaps even a new world order.

My friend Woody Brock reminds us in his latest PROFILE that the theory of growth in emerging markets dates from 1960, with the publication of Walt Whitman Rostows book The Stages of Economic Growth. Rostow gave us a description of five different stages that mark the transformation of traditional, agricultural societies and modern, mass-consumption societies.

The first three stages can be accomplished just as readily in a top-down economy as in a bottom-up economy, and there are historical reasons to believe a command economy might have some advantages. The tricky part is in the evolution from a society that is industrializing and building infrastructure into an economy that is consumer-driven and thus by definition must be bottom-up and entrepreneurial.

Command economies, with their crony capitalism and unequal rule of law, simply will not develop into full-fledged, economically successful nations. Further, there has to be both explicit and implicit permission for entrepreneurial achievements. Crony capitalism, which is a false capitalism, seeks to keep the profits from an economy in the hands of a small group. And that dynamic limits the growth of the overall economy. To achieve a full consumer society there must be open admission for everyone into the halls of business and private property ownership.

What Xi Jinping is attempting in China is no less revolutionary than what Deng Xiaoping did in 1980. In many ways it will be harder, because Deng was embarking on a phase in which a top-down economy might thrive. Xi has to change the very nature of the current system in spite of entrenched forces that do not want to give up their privileges.

There is reason to believe that Xi understands exactly what needs to be done. The question is, can he pull it off? If he does, China will for a time grow at a much slower rate, and the nature of its economic progress will shift. He understands that he cannot continue to grow the economy on debt forever. Or at least it appears that he does. One way to look at the current anticorruption effort is to see it as a way to demonstrate to deep-rooted crony capitalists that their time is at an end and that its time to figure out how to work in the new China that Xi is trying forcefully to pull the nation towards.

A number of our contributors to the book are optimistic about the potential for China to succeed. Others the clear majority see little hope. What we have tried to do in the book is give you a sense of all sides of the argument. For the optimists to be right we will need to see certain events unfold in a reasonably timely fashion. If they dont, it will be time to take a more pessimistic view. We have tried to be evenhanded and open-minded in our selection of authors and topics. And while we have our own views, we have let our contributors present theirs as forcefully as possible.

Im immensely proud of this book and believe it will become one of the definitive expositions on modern China. And it should be, considering the breadth and depth of the contributing authors, many of whom you will recognize and others whom you will be glad to have met. Take a glance at the list of contributing authors (in alphabetical order), all first-rate experts in their fields:

Andrew Batson, Ian Bremmer, Ernan Cui, Jason Daw, Ambrose Evans-Pritchard, Louis-Vincent Gave, David Goldman, Mark Hart, Neil Howe, Simon Hunt, George Magnus, Jawad Mian, Leland Miller, Raoul Pal, Michael Pettis, Sam Rines, Jack Rivkin, Nouriel Roubini, Gillem Tulloch, Logan Wright, and Wei Yao. Plus an introduction and editing by Worth Wray and your humble analyst.

The book is available (for now) only in an e-book format. You can get it on Amazon Kindle, iTunes Books, and Barnes & Noble Nook. If you want to know more about the book and the authors, you can go to this page on my website.

Amazingly, and thankfully, there have been a number of very positive reviews before weve even announced the book. (It has been live for a few days just to make sure that all the technology was working right.)

And one last detail. We have set the price of the book at $8.99. That is not a typo. If we tried to do the book in a print format, we would have to set the price closer to $50. There are at least 100 full-color graphs and charts in the entire book, and it would just not be the same to publish them in a black and white format. At the end of the letter, in my personal section, I will comment on the process of self-publishing an e-book and how one goes about marketing in this brave new Internet world. Some of you might find those thoughts interesting, but for now lets look at a key section from the introduction to the book:

The Peoples Republic of Debt

Its no secret that China has a massive debt problem. Raoul Pal (Chapter 1: Theres Something Wrong in Paradise) warned back in 2003 that there was something amiss in Chinas success story. Since that time, foreign capital chasing a bullish growth story and nervous central planners in Beijing acting to maintain rapid GDP growth post-2008 have conjoined to enable one of the largest credit booms in history.

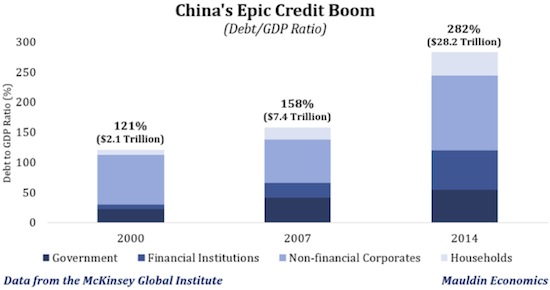

According a recent report from the McKinsey Global Institute, Chinas total debt stock more than tripled between 2000 and 2007 and nearly quadrupled from 2007 to 2014 as private-sector and local-government borrowers added more than $26 trillion in new debt. That explosion in domestic credit lifted the countrys total debt-to-GDP ratio from 121% in 2000 to 158% in 2007 and to 282% by the end of 2014; and Chinas $21 trillion in net new debt incurred between 2007 and 2014 accounted for more than 36% of the $57 trillion in cumulative global debt growth following the global financial crisis.

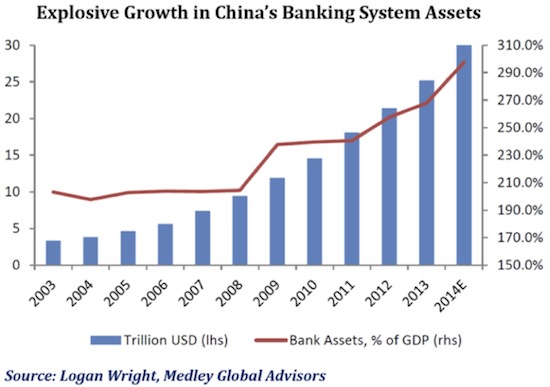

By another measure, the explosive growth in Chinas financial system is literally unprecedented, with total assets (outstanding loans) standing around $27 trillion or roughly one third of global GDP. According to Medley Global Advisors Logan Wright, Chinas banking assets have grown by roughly $17 trillion since 2008, while nominal GDP has grown to $4 trillion. As Wright explains in Chapter 3 (Deliquification & Chinas Deflationary Adjustment), There are no available comparisons for a country adding around 20% of global GDP in new bank assets over such a short period; the Japanese banking system peaked at around 20% of global GDP in total assets. And we know what happened in Japan.

Not only is this kind of credit boom unsustainable, its also inherently destabilizing. The harder and faster that credit growth runs, the higher the chance of broad-based misallocation, which eventually exerts a drag on economic activity just as powerful as the boost it provided in previous years, and sometimes moreso. As GMT Researchs Gillem Tulloch explains in Chapter 2 (The Tyranny of Numbers), Bubbles start on the back of vast quantities of cheap credit, are fed by the creation of ever greater quantities of it, and collapse when the taps are turned off.

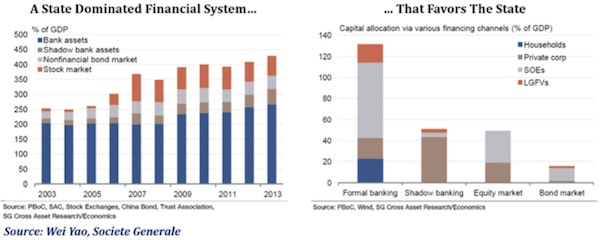

This maxim may prove especially true for a financial system like Chinas, where state-perpetuated distortions in the cost and availability of financing have (1) funneled huge amounts of capital toward increasingly unproductive, state-favored firms

and (2) pushed household and private business borrowers literally into the shadows (with the very recent development of the now-massive shadow banking system), where the burden of substantially higher interest rates drags on household consumption and raises the odds of borrower defaults.

Now that Chinas banking system has become deliquified, the threat of deflation is looming in a very real way.

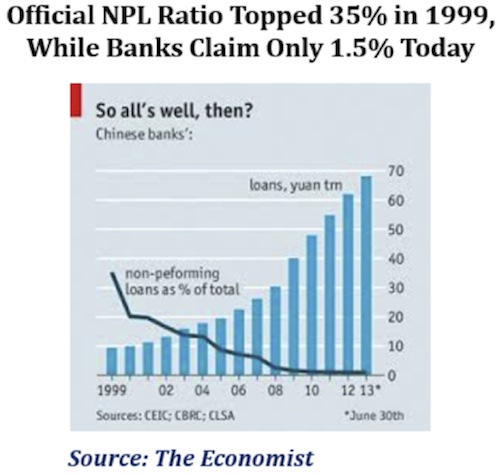

As Chinas credit boom slows, the risk of borrower defaults and the burden of bad debts will weigh heavily on the countrys lenders. Its important to note that no one really knows how large that burden is today. While the official nonperforming loan [NPL] ratio reported by Chinese banks has risen by 50% since early 2014, the countrys regulated lending institutions continue to claim the NPLs are only 1.54% of all loans.

We have a very hard time believing that nonperforming loans are only 1.5% (or even limited to the high single digits), considering how quickly the Peoples Bank of China loosened credit conditions and mandated its banks to lend when the global financial crisis hit. Underwriting standards tend to go out the window during periods of state-mandated rapid credit growth, particularly in times of crisis.

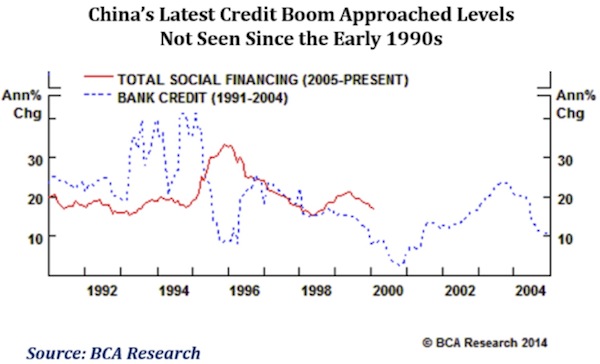

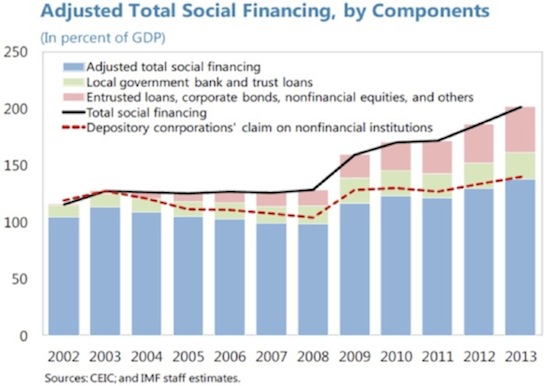

For example, just look at the change in total social financing growth since 2005 (red line below) versus Chinas bank lending boom from 1991 to 2004 (blue line). While some analysts would argue the economy was even more beholden to the state sector in the 1990s and that lending practices then were far less efficient, we doubt that Chinas lenders have improved their underwriting practices to the point that nonperforming loans would dramatically differ between the two episodes.

As you can see in the chart below from The Economist, it is widely believed that Chinas nonperforming loan ratio peaked somewhere between 30% and 40% by the late 1990s; although some analysts (like Societe Generales Wei Yao) argue that the true number was more like 50% higher than Russias in 1995, Chiles in 1981, or Malaysias in 1997, and twice that of Mexicos in 1994. The bottom line is that Chinas last comparable lending boom produced a nonperforming loan burden at least 20x larger (as a percentage of total loans) than the figure Chinese lenders are reporting today (and perhaps 30x!).

If you talk with the management at major Chinese banks, as China Beige Book Internationals Leland Miller (Chapters 8 and 19) does on a regular basis, they all confess that nonperforming loans are a MAJOR problem in China

but ask if nonperforming loans are a problem at their particular banks, and the managers consistently report that their banks are in perfect health. That dynamic is uncomfortably reminiscent of Japan in the late 1980s, which serves as a chilling reminder that manageable rot within a largely state-controlled banking system can explode into higher-than-expected NPLs in the event of a real crisis.

Heres what Leland Miller has to say about Chinas NPL problem:

The NPL situation is completely opaque it's the deepest and darkest of Beijing's state secrets. But we can be very confident of a few things:

a. The level of reported NPLs is completely unrealistic (take, e.g., China Development Bank's sub-1% NPL level for many years... despite a portfolio of borrowers that includes Central Asian kleptocrats, unprofitable Chinese SOEs [state-owned enterprises], African small businesses, and Latin American energy plays);

b. NPL levels have always been kept artificially low simply by rolling over the debt, so that the debt never technically becomes nonperforming; and

c. NPLs are recorded as part of a 5-level classification system, but the levels are subject quite easily to mass manipulation simply by tweaking the particular classification of the loan. If you have too many level 3 loans, e.g., then just move a bunch of them to level 2 as an administrative matter.

With all that in mind, the official NPL numbers are simply not believable

and the true burden of bad debts may not be manageable.

While Beijing had the wherewithal to clean up its banks in the early 2000s by recapitalizing major lenders and shifting the bad assets to asset management companies (AMCs), it hasnt actually resolved the bad debts, even after more than a decade. According to The Economist,

NPLs [the worst of the worst bad loans] were hived off into four new AMCs: Huarong, China Orient, China Great Wall and Cinda. From 1999 to 2004 loans worth over 2 trillion yuan ($242 billion) were transferred. Though mostly bad, the loans were usually sold at full face value. They were paid for with ten-year bonds, backed by the finance ministry, that the AMCs issued to the big state-owned banks. But since most NPLs failed to recover in that time, these bonds were extended another decade. In short, the bail-out is still going on. What the AMCs have done with their assets is unclear, as they have not released proper accounts. Some NPLs have been sold but reportedly at only 20% of face value.

A comparable NPL problem (or even a true NPL rate one third of the size) would be far more difficult to manage fifteen years later because, while Chinas GDP has grown nearly eightfold since the year 2000, growth in banking system assets has dramatically outstripped the countrys economic growth. If, as we suspect, NPLs are closer to 11% (at a minimum) than to the official 1.54%, China may have a mountain of bad loans equal to more than 20% of its GDP

and maybe more than 40% of GDP. We are now talking trillions of dollars. Even for China, that is a great deal of money.

Recapitalizing Chinas lenders would likely require a massive transfer of toxic private-sector assets directly onto the states balance sheet; and as weve seen in Japan since the late 1980s and across the developed world since 2008, major public-sector bailouts tend to drag heavily on economic growth (as do the longer-term headwinds of Chinas demographic decline, which Saeculum Researchs Neil Howe outlines in Chapter 4: A Crisis Looms in China.)

But as Logan Wright explained to us recently, Beijing doesnt have as much incentive to clean up its banks today as it did in the early 2000s, with the intent to issue bank equity to the rest of the world. The CCP leadership is more interested in making sure the NPL secret stays hidden. For now, the problem remains unconfronted, to the detriment of Chinas financial system. As Logan explains in Chapter 3 (Deliquification & Chinas Deflationary Adjustment), the banks are forced to pretend that this mountain of bad assets is performing; but that pretense doesnt change the fact that impaired cash flows from the banks loan portfolios what Logan calls deliquification are forcing many of the banks to scramble to borrow cash from one another or from the PBoC just to stay liquid.

Its a recipe for inevitable deleveraging and deflation, if not disaster.

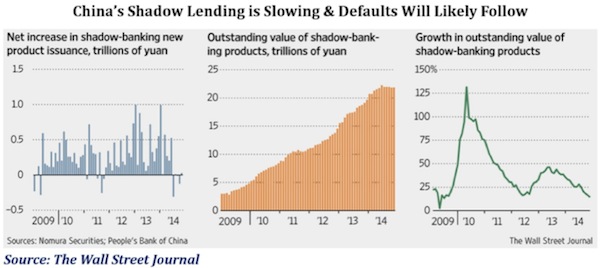

But the problem is not fully contained within Chinas regulated banking system. Weve also seen substantial growth over the past few years in shadow lending. The sums involved could, according to Nomura Securities, stand at more than $3.5 trillion. A lot of these loans made through wealth management products and trusts are actually off-balance-sheet assets of Chinas banks, but very little is known about their asset quality. Defaults in the shadows could cast a cloud of negative confidence on the entire financial system, which in turn increases the risk that Beijing could lose control.

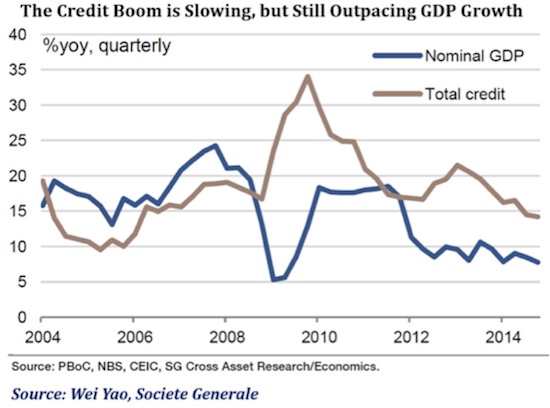

For now, credit growth is slowing as Chinas inherently deliqufied banking system scrambles to stay liquid, and it is having a material impact on economic activity. As you can see in the chart below, Chinas year-over-year credit growth is still outpacing the countrys GDP growth rate; but both are slowing materially. And since it does not seem possible for rapid credit growth to continue for much longer without triggering some nasty consequences in Chinas financial markets, growth should slow substantially more.

Our concern at this juncture is that a material slowdown in both credit growth and economic activity does not seem consistent with Beijings immediate plans. Premier Li Keqiang has adamantly maintained that Beijing will hit its 7.1% growth target in 2015 and insists that the State Council is committed to both managing credit growth and maintaining medium- to high-speed growth while making sure that the Chinese economy achieves a medium-to-high level of development (in terms of real GDP per capita). As former UBS Chief Economist George Magnus outlines in Chapter 10 (The Contradiction at the Heart of Chinas Growth Strategy), these goals are in direct contention with one another.

Until President Xi Jinping and his reformers move forward with meaningful reforms to rebalance Chinas economy to a healthier growth model (which we will discuss shortly, but suffice it to say it will require at least a substantial slowdown to actually work), there is no chance of maintaining 5%+ growth, much less the State Councils 7.1% GDP target, without relying on credit expansion.

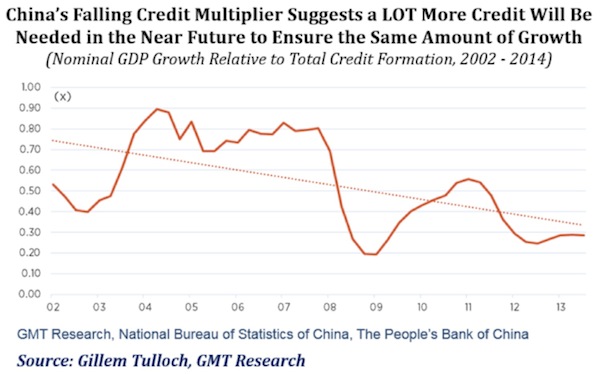

Therein lies the problem, as you can see in the graph below from GMT Researchs Gillem Tulloch (Chapter 2: The Tyranny of Numbers). Chinas private sector is taking on more and more debt with less growth to show for it every year. And as that credit multiplier continues to fall, more and more credit growth will be needed just to meet Beijings target... or even to support a gradual slowdown over the next several years.

Gillem elaborates:

In order to achieve the 7% [annual] real GDP growth target over the next five years (2014-2018), the banking system will need to create RMB106 trillion (US$17 trillion) of new credit. This assumes nominal GDP growth of 9% [per year] and based on the 2013 credit multiplier of 0.3x. This is the equivalent of replicating the balance sheet of Citigroup nine times over. More to the point, it means almost replicating the entire listed US financial sector in just five years, a feat that took the worlds richest, largest and most sophisticated economy 200 years to achieve

[If China continues at this rate,] by 2018 it will have built enough new apartments over the previous 15 years to potentially rehouse 55% of its population [and] will command 65% of the worlds cement production and 59% of its steel.

If the credit boom that led to an outright explosion in Chinas debt from $2.1 trillion to $28.2 trillion in 14 years was unsustainable, the kind of credit growth required to meet the Chinese Communist Partys growth target over the next five years is literally impossible. This dynamic could set up a crisis of confidence in the coming years if Beijing does not materially lower its growth target and take urgent steps toward reform moves that represent a major but necessary risk for a dangerously overleveraged economy.

That risk begs the most important question of all: is Chinas debt burden manageable without disastrous consequences? Analysts broadly disagree, as you will see in this book, but its a conversation we need have. The answer to this question will have a profound impact on global growth and your investment portfolio. There are few more important questions in the macroeconomic world.

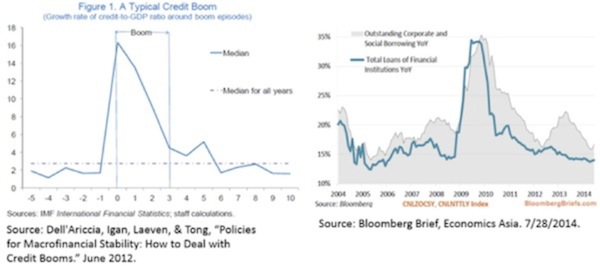

Whats more, there are NO examples of ANY countrys adding banking assets as quickly has China has over the past several years and certainly not on this scale. There are simply no good historical precedents; but if we make a simple comparison to the largest five-year debt booms in modern history, Chinas explosive growth in Total Social Financing from 2009 to 2013 (when credit growth was the most intense) ranks in the top five.

Looking at a sample of 43 major economies over the last 50 years, IMF economists Giovanni DellAriccia, Deniz Igan, and Luc Laeven found only four other cases of comparable lending growth; and each of those countries experienced a banking crisis and/or a sharp recession within three years of their respective booms.

In other words, there are no cases in modern history where an economy has managed to avoid an outright bust after experiencing rapid lending growth anywhere in the neighborhood of Chinas ongoing credit boom. None. And even if we look to the 48 instances over the last 50 years where lending measures expanded by as little as 30% over five years (less than half the magnitude of Chinas credit explosion), there is still a 50% chance of a banking crisis or an abrupt fall in growth during the post-boom period.

Moreover, the model for a typical credit boom (outlined in DellAriccia, Igan, Laeven, & Tongs 2012 paper Policies for Macrofinancial Stability: How to Deal with Credit Booms) suggests that painful post-boom adjustments tend to occur when the pace of credit growth simply cools back toward its long-term median. That cooling process is already well advanced in the Peoples Republic, which means we have to consider what the lack of cheap and indiscriminate funding will reveal about the quality of loans (and the value of the underlying collateral mostly real estate but also commodity stockpiles) made in previous years. Its not a pretty picture.

Aside from the clear and present danger that each of these vulnerabilities poses to Chinas future growth, the situation in the Peoples Republic does stand out from past credit booms in one way. The Peoples Republic has substantial buffers or at least the outward appearance of buffers, based on official data to supposedly defend against capital flight, absorb sudden losses in a banking crisis, and commute a hard landing into a longer period of subdued growth (which Beijing might or might not allow to be shown in its headline GDP figures). According to official data sanctioned by the Chinese government and outlined by the IMF in its latest annual China staff report, Total public debt is relatively low; public sector assets are large (including foreign exchange reserves); domestic savings are high, and foreign debt exposures low; capital controls limit the risk of capital flight; and the government retains substantial levers to control economic and financial activity.

The legitimacy and adequacy of these buffers in a real crisis is certainly up for debate, but it is hard to argue that the Chinese government does not have at least some resources to contain an imminent crisis and buy more time.

Judging from an IMF podcast released in August 2014, these buffers are one of the only reasons for optimism, even if Beijing does make the hard decision to expedite its high-stakes reform agenda. Though the IMFs China mission chief, Markus Rodlauer, is a generally optimistic quasi-government staff economist, hes clearly sounding the alarm:

Our assessment after careful analysis is that the near term risk of a hard landing really is low. And we come to this judgment because we see an economy that still has substantial buffers both in terms of the real economy and the way the government can manage the economy in the near term, and therefore prevent a hard landing....

By the same token, we need to say that given the way the economy is growing, given the way the risks have been accumulating and are continuing to accumulate in the economy, unless reforms are implemented to redirect the economy to a somewhat safer growth path, the risk of a hard landing will continue to increase.... Generally these sorts of rapid credit growth do lead to either a banking crisis or a sharp slowdown of growth [emphasis ours].

If past performance is predictive of future outcomes, growth miracles built on credit booms always end the same way. An epic bust may not come as quickly as it might have otherwise, but a bust will ultimately be difficult to avoid if Beijing refuses to accept a lasting slowdown. Broad-based, debt-fueled overinvestment may appear to kick economic growth into overdrive for a while; but eventually disappointing returns and consequent selling lead to investment losses, defaults, and banking panics. China can defy history a bit longer, but not forever.

New York, Denver, Maine, and Boston

Tomorrow I leave for New York, where I will spend the next four weeks working and trying to play tourist when I can. Business requires that I spend a month in Manhattan, but I have to admit that Ive always wanted to spend a month in The City That Never Sleeps, living in one of the neighborhoods and absorbing the culture and spending somewhat more casual time with friends. Duty calls, but I dont think its going to be hard duty, even for this Texas boy.

Later in the month I will go to Denver to be with my partners Altegris Investments at a Financial Advisor magazine conference on alternative investing, where I see I will be with my friend Larry Kudlow. Then I and my youngest son, Trey, will once again go to Grand Lake Stream, Maine, for the annual Camp Kotok (a.k.a. The Shadow Fed) migration. This will be the ninth summer that Trey and I have been to the fishing and economics fest. He is now 21 years old, and it will technically be legal for him to participate in the wine drinking, although a few of my fellow fisher economists have indulged him here and there over the years. Later in August I intend to spend some time with Woody Brock and other friends in Massachusetts before resuming my peripatetic ways this fall.

I mentioned that I would say a word or two about the quandaries of publishing A Great Leap Forward? as an e-book. Choosing a traditional publisher would of course get me a reasonable advance, and there is certainly no assurance that this book will bring in the same sort of income without a print version. It might surprise readers to know that authors really dont get all that much from a book sold by a traditional publisher in an e-book format. Maybe 10 to 15%. Technically, we will be getting 70%. I say technically because

(1) We have to assume all the cost of editing and formatting, which is not inconsequential if youre trying to do it right, which is the only way I will do it. And,

(2) This book is actually fairly graphically dense. And the various formats (Kindle, iTunes, and Nook) actually charge for the extra bandwidth that it takes to download a book above a few megabytes. And believe me, we are above a few megabytes. Depending on the format and the quantities, our authors share can easily drop to 50%.

A lot of people assume that today the majority of books are sold as e-books. Not true. While the e-book format is still growing, the rate of growth now is nowhere near its trajectory in earlier years. There are a lot of people (and I expect to hear from you) who still want their books in physical form. As one reviewer said, he wished he could underline and dog-ear the pages.

But as a former Luddite who thought he would never give up his physical books, let me offer this thought. I now almost always refuse to read a book if I cant find it on Kindle. I can still highlight everything in Kindle with my finger, make notes in the margins, and do cross-references that I could never do in printed form. Further, and amazingly, Amazon offers me at absolutely no cost the ability to check and cross-reference all of those highlights on my personal Amazon Kindle page. I think back over my last 50 years of book reading and realize that all the paragraphs I underlined and notes I wrote are essentially lost. If I dont have the book and cant remember what page something was on, I cant find it. Now, with Kindle, I can; and I find that ability remarkably liberating and empowering. While I despair over what time and an imperfect memory have cost me, I can now spend a pleasant afternoon reviewing my highlights and notes and reminding myself of what I thought was important at the time.

And since I can read on any electronic device (you dont need a Kindle or iPad or Nook) and I can now read the same book on multiple devices, I enjoy the freedom of not having to carry 10 pounds of books with me through an airport in order to have something to read.

And so let me close (its time to hit the send button) with a blatant marketing moment: if you havent already embraced what technology can do for readers, you should see our new book as your impetus to launch your foray into the world of electronic books. Again, you can get the book at Kindle, iTunes or Nook, or check us out at Mauldin Economics.

You are going to thank me not long after you begin reading. And dare I point out that $8.99 is not a huge price to pay for exploring a new technology. You can download all those book apps on whatever computer or other device you may have. For what its worth, I have my Kindle on my iPhone, my iPad, and my brand-new MSI computer. (A few of you might be surprised at my choice of boxes, as MSI is a hard-core gaming computer; but it just has so much power packed into such a small format that I thought the extra few hundred dollars was worth it. But then, ask me again in a few months. I thought my Microsoft Surface Pro tablet computer was going to be a good investment and it had its advantages but at the end of the day I just found it to be too underpowered for me to work on.)

Have a great week. I see a lot of politics and fun dinners and writing in my near future. I dont want to even think about the next book Ill write, but I have to admit, there are three or four projects brewing in the back of my head. At some point this summer I will have to let one of them into my forebrain. Until then, I will concentrate on my weekly letter and giving you the best of what I come up with.

Youre hoping China can leap the chasm analyst,

John Mauldin

subscribers@mauldineconomics.com