-- Published: Thursday, 13 August 2015 | Print | Disqus

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

He might be leading in the polls right now, but Donald Trump is unlikely to be elected president in 2016, if a time-tested election forecast turns out to be accurate.

Since 1980, Moodys Analytics has been predicting presidential election results, and for each of the nine contests, its been on the money. It manages to do this by using a sophisticated model that measures the economic health of each state leading up to the election. Some of the factors it captures are household income growth, house price growth and percent change in gasoline prices. It also looks at political preference county-by-county.

The model has become scarily precise. In 2012, it accurately predicted each states election outcome and nailed the Electoral College vote. Thats like calling not just which football team will win the Super Bowl but also the scores.

Now, Moodys Analytics has released its forecast for the 2016 presidential election, and it looks as if itll be a nail-biter. In the end, though, the victor will be the Democratic nominee, winning by only two electoral votes, according to the model. That would exclude The Donald.

click to enlarge

Of course, forecasting an election thats more than a year away, when we dont even know who the nominees will be, is tricky business. A lot can happen between now and Election Day. But again, the Moodys model has never been wrongyet. It will be interesting to see if the record holds.

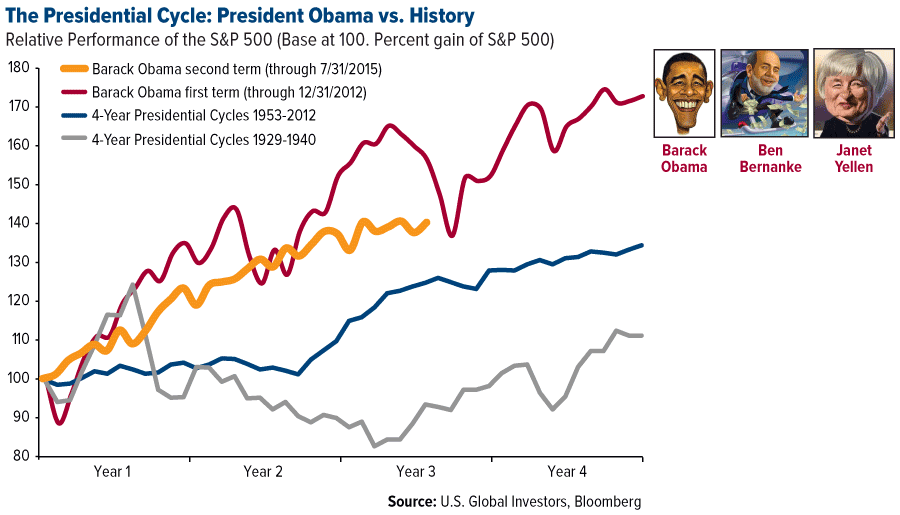

Investors might wonder how this could affect the stock market and their portfolios. Whats most relevant here is the four-year presidential cycle, a topic I wrote extensively about last year in my whitepaper, Managing Expectations.

Focus on the Policy, Not the Party

Its 2015, which marks the third year of President Barack Obamas second term. Also called the pre-election year, the third year in past presidential terms has historically been the best for stock returns when compared to the post-election, mid-term and election years. This is a phenomenon first described by Yale Hirsch, founder of the Stock Traders Almanac, which is now edited by his son Jeffrey. As you can see, the annual gains for pre-election years have averaged over 10 percent, ahead of the other three years.

We have to go all the way back three quarters of a century to 1939, during Franklin Roosevelts presidency, to find the most recent down pre-election year as measured by the Dow Jones Industrial Average. The other negative years are much fresher in memory: 2005 (post-election year, down 0.60 percent), 2002 (mid-term year, down 16.80 percent) and 2008 (election year, down 33.80 percent).

Right now the Dow Jones is off more than 3 percent year-to-date, while the S&P 500 Index is flat. This raises the possibility that 2015 will be the first pre-election year since 1939 to end in negative territory.

What is it about the pre-election year that seems to benefit stocks? The answer might be more intuitive than you think. In a 2012 peer-reviewed essay that appeared in The Graziadio Business Review, authors Marshall Nickles and Nelson Granados postulate that incumbents typically implement new policies or push for lower taxes a year or two before a presidential election in an effort to pump up the economy. Often the president will work with the Federal Reserve to align its monetary policy with his fiscal policy. If results are favorable, stock prices are more likely to rally.

This validates one of U.S. Global Investors main tenets, that government policy is a precursor to change. More so than which political party the incumbent belongs to, its important to know what policies might help or hinder growth.

click to enlarge

Nickles and Granados refer to the period between January 1 of the first year of a presidential term through September 30 of the second year the least favorable period (LFP). The remainder of the termOctober 1 of the second year through December 31 of the fourth yearis what they call the most favorable period (MFP).

Through back testing, the two found that if you had invested an initial, completely hypothetical $1,000 during the LFPs starting in 1953, you would have seen only a 519.8-percent gain by 2012. If, however, you would have invested the same $1,000 during the MFPs, the returns could have reached as high as 20,468 percent.

Put another way, thats a difference of $199,491!

So no matter who ends up in the White HouseRepublican, Democrat or Independentthe four-year presidential cycle is a constant that has a real, documented effect on stock performance.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.

| Digg This Article

-- Published: Thursday, 13 August 2015 | E-Mail | Print | Source: GoldSeek.com