Chinas Economy Is Undergoing a Huge Transformation That No Ones Talking About

-- Published: Tuesday, 1 September 2015 | Print | Disqus

By Frank Holmes

The photo you see below was snapped recently in Beijing. It might not be that special to some readers, but in my 25 years of visiting the Chinese capital, Ive never seen a blue sky because its always been blotted out by yellow smog. Beijing is clearly undergoing a massive transformation right now. This might please proponents of the green movement, but its ultimately harmful to the health of China's manufacturing sector.

On the other hand, blue skies could be ahead for Chinas service industries.

Misconception and exaggeration are circling Chinas economy right now like a flock of hungry buzzards. If you listen only to the popular media, you might believe that the Asian giant is teetering on the brink of economic disaster, with the Shanghai Composite Indexs recent correction and devaluation of the renminbi held up as proof.

Dont get me wrong. These events are indeed significant and have real consequences. They also make for some great, sensational headlines, as I discussed earlier this month.

But what gets hardly any coverage is that Chinas economy is not weakening so much as its changing, much like Beijings skies. Take a look at the following two charts, courtesy of BCA Research:

You can see that the worlds second-largest economy has begun to shift away from manufacturing and more toward consumption and the service industries. While the countrys purchasing managers index (PMI) reading has been in contraction mode since March of this year, the service industrieswhich include financial services, insurance, entertainment, tourism and moreare ever-expanding. The problem is that the transformation has not been fast enough to offset the massive size of the manufacturing sector.

Just as a refresher, the PMI is forward-looking and resets every 30 days. It helps investors manage expectations. Consider this: The best-performing country in our Emerging Europe Fund (EUROX) is the Czech Republicwhich also happens to have one of the highest PMI readings. Coincidence?

In China, overseas travel, cinema box office revenue and ecommerce are all seeing explosive growth, according to BCA. The countrys once-struggling real estate market is also robust. The government just relaxed rules to permit more foreigners to purchase mainland property.

But youd be hard-pressed to come across any of this constructive news because its not particularly good for ratings.

A recent Economist article makes this point very clear:

The property market matters far more for Chinas economy than equities do. Housing and land account for the vast majority of collateral in the financial system and play a much bigger role in spurring on growth. Yet the barrage of bearish headlines about share prices has obscured news of a property rebound. House prices have perked up nationwide for three straight months. Two months after the stock market first crashed, this upturn continues.

Commodity Imports Have Actually Been Quite Strong

Again, Chinas transformation from a manufacturing-based economy to one that focuses on consumption has real consequences, one of the most significant being the softening of global commodity prices. As I told Daniela Cambone on last weeks Gold Game Film, golds Love Trade has become not a No Trade, but a Slow Trade. Weve seen demand cool along with a decline in GDP per capita, the PMI readings and Chinas M2 money supply growth.

Below you can see the relationship between Chinas M2 money supply growth and metal prices. Since its peak in late 2009, money supply growth has been dropping year-over-year, driving down metal prices.

Money supply growth tends to be a first mover. When it has contracted, the PMI has usually followed. Recently, this has hurt economies that depend on China as a net buyer of raw materials, including Brazil, which supplies the Asian country with iron ore, soybeans and many other commodities, and Australia.

When M2 money supply growth and the PMIs are rising, commodity prices can also rise. But thats not whats happening. Its important to recognize that when new orders for finished products fall, theres less consumption of energy to manufacture and ship. Again, this might make the greenies happy, but its ultimately bad for manufacturing.

Ive said several times before that China is the 800-pound commodities gorilla, and it continues to be so. The country currently consumes about a quarter of the total global output of gold. For nickel, copper, zinc, tin and steel, its around half of world consumption. For aluminum, its more than half.

These are huge figures. But investors should know that Chinese imports of these important metals and materials still remain strong. Tom Pugh, a commodities economist at Capital Economics, told the Wall Street Journal last week that the market has it wrong about China, that the drop in demand has been overstated:

If you look at Chinese commodity imports over the last few months, theyve actually been quite strong. A lot of it is just that people thought China would continue to grow at 10 percent a year, ad infinitum, and now people are just realizing thats not going to happen.

Reuters took a similar stance, reporting that there were at least 21 commodities that showed increases in imports greater than 20 percent in July this year, compared to the same month in 2014. Weakening demand has been caused by a number of reasons, including structural oversupply and the impact of the recent volatility in equity markets.

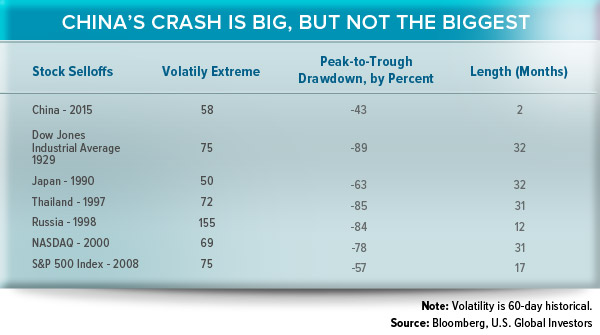

But its important to keep things in perspective. Compared to past major market crashes, Chinas recent correction doesnt appear that bad.

Any bad news in this case can be seen as good news. I think that in the next three months we might see further monetary stimulus, following the currency debasement nearly three weeks ago. We might also see the implementation of new reforms in order to address the colossal infrastructure programs China has announced in the last couple of years, the most monumental being the One Road, One Belt initiative.

Dividend-Paying Stocks Helped Stanch the Losses

As investors and money managers, its crucial that we be cognizant of the changes China is undergoing. With volatility high in the Chinese markets right now, weve raised the cash level in our China Region Fund (USCOX), and after the dust settles somewhat and the right opportunities arise, well be prepared to deploy the cash. Were also diversified outside of China.

We managed to slow the losses during the Shanghai correction by being invested in high-quality, dividend-paying stocks.

According to daily data collected since December 2004, the median trailing price-to-earnings (P/E) ratio for the Shanghai Composite Index constituents currently sits at 48.6 times earnings. If it reverts to the mean, risk is 32 percent to the downside for the index. Currently, the P/E ratio of our China Region Fund constituents sits around 16 times. This suggests that USCOX has less downside risk and is cheaper than the Shanghai Composite.

We seek to take advantage of the trend toward consumption by increasing our exposure to the growing service industriestechnology, Internet and ecommerce companies (Tencent is one of our top 10 holdings); financial services (AIA and Ping An Insurance); and enviornmental services (wastewater treatment services provider CT Environmental).

Rising sports participation among white collar workers in China is very visibile these days. Xian Liang, portfolio manager of USCOX, says that his friends back in Shanghai share with him, via WeChat, how they track their daily runs using mapping apps on their phones.

With that said, an attractive company is Anta Sports, an emerging, innovative sportswear franchise. Fans of the Golden State Warriors might recall that guard Klay Thompson endorsed its products earlier this year.

We believe the China region remains one of the most compelling growth stories in the world and continues to provide exciting investment opportunities.

Please consider carefully a funds investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting www.usfunds.com or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Distributed by U.S. Global Brokerage, Inc.

Foreign and emerging market investing involves special risks such as currency fluctuation and less public disclosure, as well as economic and political risk. By investing in a specific geographic region, a regional funds returns and share price may be more volatile than those of a less concentrated portfolio. The Emerging Europe Fund invests more than 25% of its investments in companies principally engaged in the oil & gas or banking industries. The risk of concentrating investments in this group of industries will make the fund more susceptible to risk in these industries than funds which do not concentrate their investments in an industry and may make the funds performance more volatile.

The Shanghai Composite Index (SSE) is an index of all stocks that trade on the Shanghai Stock Exchange. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Purchasing Managers Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

M2 money supply is a broad measure of money supply that includes M1 in addition to all time-related deposits, savings deposits, and non-institutional money-market funds.

Standard deviation is a measure of the dispersion of a set of data from its mean. The more spread apart the data, the higher the deviation. Standard deviation is also known as historical volatility.

There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time.

Fund portfolios are actively managed, and holdings may change daily. Holdings are reported as of the most recent quarter-end. Holdings in the Emerging Europe Fund and China Region Fund as a percentage of net assets as of 6/30/2015: Tencent Holdings Ltd. 6.52% China Region Fund, AIA Group Ltd. 1.92% China Region Fund, Ping An Insurance Group Co. 3.28% China Region Fund, CT Environmental Group Ltd. 0.52% China Region Fund, ANTA Sports Products Ltd. 0.57% China Region Fund.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

The content on this site is protected

by U.S. and international copyright laws and is the property of GoldSeek.com

and/or the providers of the content under license. By "content" we mean any

information, mode of expression, or other materials and services found on GoldSeek.com.

This includes editorials, news, our writings, graphics, and any and all other

features found on the site. Please contact

us for any further information.

Live GoldSeek Visitor Map | Disclaimer

The views contained here may not represent the views of GoldSeek.com, Gold Seek LLC, its affiliates or advertisers. GoldSeek.com, Gold Seek LLC makes no representation, warranty or guarantee as to the accuracy

or completeness of the information (including news, editorials, prices, statistics,

analyses and the like) provided through its service. Any copying, reproduction

and/or redistribution of any of the documents, data, content or materials contained

on or within this website, without the express written consent of GoldSeek.com, Gold Seek LLC,

is strictly prohibited. In no event shall GoldSeek.com, Gold Seek LLC or its affiliates be

liable to any person for any decision made or action taken in reliance upon

the information provided herein.