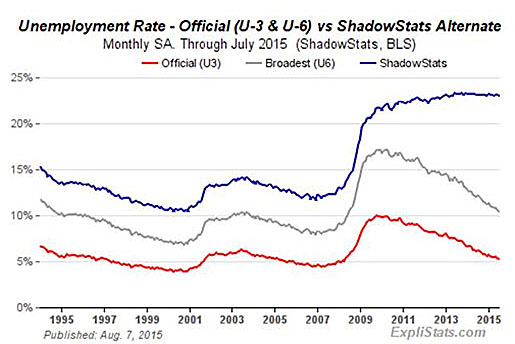

The Gold Report: In honor of Labor Day, let's discuss unemployment. You estimated that when all workers are counted, the unemployment rate in July was 23% compared to the government's reported rate of 5.4%. What is different about the job market today than before the recession?

John Williams: In a normal economic recovery, people who have lost their jobs start working again as the economy improves. That hasn't happened this time, at least not to the extent suggested by a 5.4% unemployment rate (U3), where the government's headline definition of "unemployed" is quite narrow. To be counted among the headline unemployed, you have to be out of work and actively to have looked for work in the last four weeks. If you want a job, but have given up looking, the government counts you as a "discouraged worker" or "marginally attached worker" and you don't show up in the headline number.

If you haven't looked for work in more than a year, even if you would like to work, then the government just doesn't count you in even its broadest measure of unemployment (U6); you just disappear from any of the unemployment measures. As a result, when the government says that 200,000 fewer people are unemployed in a month, and the headline unemployment rate drops, often there isn't an increase of 200,000 people who are re-employed. They just have been defined out of existence. My broad unemployment estimate includes those no longer tracked by the government, those who cannot find a job, who have given up looking for work for more than a year because nothing is available, yet they still would like to find a job, even though they may be doing other thingslike taking care of grandkids. That broader unemployment number is around 23%.

TGR: Have the types of jobs changed? Are we seeing fewer jobs in manufacturing and finance now than there were before? Are there other areas that are growing, like technology and service jobs?

JW: Generally, the government has done a great deal to encourage the offshoring of U.S. production and the growth in the U.S. trade deficit. On average, lower-paying jobs are the ones left behind domestically. Real average weekly earnings, adjusted for the consumer price index, peaked in the early 1970s. It's generally been downhill since then.

That is a challenge to a sustainable economic recovery because lack of income growth, and other constraints on consumer liquidity, inhibit healthy expansion in the consumption of consumer goods and services. We have a consumer-based economy. Seventy percent of our gross domestic product (GDP) relies on the consumer. If income is not growing, if consumer debt expansion is limited and if confidence is weak, then the consumer does not have the ability to fuel sustained growth in consumption. There's no way the economy has recovered, nor is it about to recover.

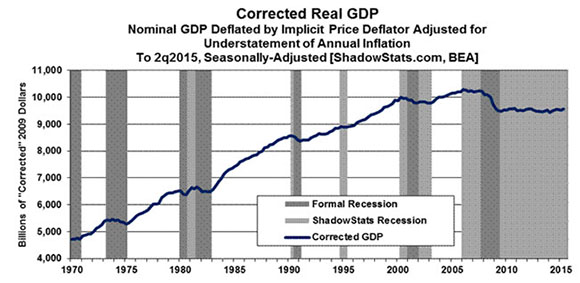

TGR: Unemployment is just one of the data points that show whether an economy is doing better. The revised GDP report shows that the U.S. economy grew at an annual rate of 3.7% in Q2/15. Is that a positive sign for the economy?

JW: The GDP numbers are nonsense. They're very heavily inflated. They're gimmicked. Government agencies long have put a little upside bias into the numbers to avoid the political embarrassment of understating actual economic activity. After a few years, those numbers usually get revised lower, as happened in this year's benchmark revisions to the GDP. The next big comprehensive GDP revision will be in 2018, so it may be that long before we start to see headline details approaching reality.

The patterns of revision show consistently that the economy has not been as strong as it's been reported. Effectively, we're seeing a broad, multiple-dip economic downturn that began in the housing industry in 2005. It's not a happy circumstance. Separately, headline GDP growth is overstated by the use of too-low an inflation rate in deflating the series. Use of understated inflation results in overstated real, or inflation-adjusted, growth. Corrected for the inflation issues, actual GDP plunged into 2008 and 2009 and has been in low-level stagnation since. Official GDP plunged into 2008 and 2009 and then fully recovered, despite a number of key related series not following suit.

Courtesy of ShadowStats.com

That said, the GDP is not the broadest measure of U.S. activity. Gross national product (GNP) is the better and broader indicator because it includes international flows in interest and dividend payments. In the most recent reporting, GNP was 3.2% instead of the GDP's 3.7% in Q2/15. Instead of being up by the GDP's 0.6% in Q1/15, it was down by 0.2%.

Gross domestic income (GDI) measures the economy on the income side of the national income balance sheet, definitionally the equivalent of the consumption side of the GDP, and yet the GDI showed growth essentially stagnant in H1/15. That same pattern was confirmed in several very important economic series, including industrial production, which showed a contraction in Q1/15 and Q2/15. We never get consecutive quarter to quarter contractions in production without a recession. Retail sales adjusted for inflation also contracted in Q1/15. It showed some growth in Q2/15, but it was flat for H1/15. Again, we never see patterns like that except in a recession. We're in a recession. It just isn't being formally recognized in the GDP statistics. I figure it will surface in formal recognition in the next six to nine months. We've been in a period of low-level stagnation, and now the economy is actually turning down again.

TGR: If the Federal Reserve is using the GDP number, what will the consequences be if it raises interest rates on an economy that is not growing?

JW: It actually might help it. The Fed here has not been fully honest with the American people. It didn't institute quantitative easing (QE) to stimulate the economy. The Fed has a mandate from the Congress to keep the economy growing and inflation under control, but the Fed's primary function in life is to keep the banking system afloat. The Fed did whatever it had to do in 2008 to keep the banks in business. It bought some time. But it did very little fundamentally to alter the factors that triggered the 2008 crisis. The dollars from QE3 never made it into the money supply to help the economy. The economy has not recovered, and the banking system still is not fully stable, even though it has been enjoying the risk-free income of storing that QE3 money at the Fed.

Now, the Fed wants to raise rates to begin restoring some sense of normalcy in the monetary system. On the plus side, it would give bankers a little extra margin for lending, possibly to higher-risk borrowers, which could help business activity. It also would help people living on fixed incomes to enjoy higher, safer returns in assets such as certificates of deposit. But because of the unstable global conditions and obvious lack of domestic growth, everyone is nervous about raising rates. The Fed probably will blame the employment numbers that come out at the beginning of September and leave open the possibility of raising rates in December.

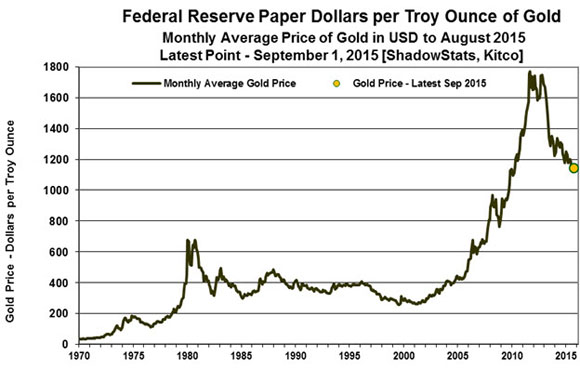

TGR: What impact would raising rates or deciding to delay raising rates have on gold? Gold Newsletter publisher Brien Lundin recently suggested to me that a rate hike could be a blessing for gold prices because the decision has already been priced in and investors are just waiting for the shoe to drop.

Courtesy of ShadowStats.com

JW: Interest rates affect gold because they affect the dollar. Higher relative interest rates attract capital into the markets, making a currency stronger. A delay in raising interest ratesor further easingwould effectively debase the dollar. That's a big positive for gold and also a big positive for dollar-denominated oil. Having the decision out of the way likely also would have its positive impact, where I agree that it's already discounted by the stock market, and, even if the rate hike comes, it will be small.

Nonetheless, the underlying problem is that the U.S. economy is not recovering. Again, we are looking at a new recession, although I'll contend it is an ongoing element of the economic collapse into 20082009. Once that becomes apparent, there will be massive dollar selling, a big spike in gold prices and oil prices will again move higher as the dollar weakens.

TGR: You warned in a special commentary that the world is increasingly out of balance and that dollar selling could be on its way. What are the triggers we should be looking for?

JW: The big issue still remains the long-term solvency of the U.S. The big spike in gold prices came when Standard & Poor's downgraded the Treasuries as Congress argued over the debt ceiling. That has never been resolved. Politicians in Washington are just burying their heads in the sand.

We are going to see increasing pressures to dump the dollar as the world's primary reserve currency. Who in the world is going to buy U.S. Treasuries? The Fed was a big buyer, but it has exited that part of QE3. China was a big buyer, but it has had to sell because of its market problems. Much of the rest of the world also has been moving out of the dollar.

TGR: Could a President Trump help the dollar and commodities?

JW: Donald Trump is talking about addressing problems that the political establishment has refused to address, ranging from fiscal conditions to the lack of actual economic recovery. From that standpoint, it well could be viewed as a positive for the dollar and commodities. Certainly, it would not be viewed as a positive by the establishment politicians unwilling to address the issues. How people will react remains to be seen. I wish Mr. Trump well, as I do anyone who looks to take on the mantle of control in an extraordinarily dangerous and unstable circumstance.

Main Street USA is suffering and it recognizes that it's suffering, and that is why there is such a negative political environment for incumbents. Of the presidential candidates, Mr. Trump appears to be the one drawing Main Street's support.

TGR: You mentioned China. We saw the U.S. market panic at the end of August when China's growth numbers came out. What is supporting the upward climb of the Dow, NASDAQ and S&P 500 based on the real numbers you've been talking about?

JW: Nothing that I can see as fundamental. I view the stock market as highly speculative, very heavily intervened in, manipulated and hyped. I don't think it's really an open market anymore. The issues from 2008 still overhang the markets. While people still hope that things are going to work out, none of the major underlying issues triggering the 2008 panic were addressed meaningfully. The measures taken then were all stop-gap and just pushed the problems into the future. Now the economy is out of control.

In prior times, the Fed wouldn't have debated back and forth for over a year whether or not it was going to raise interest rates. That's nonsense. It would have just done it, and if it made a mistake, it might address it later on. The Fed is trying to prevent a stock crash, but there is no fundamental strength underneath the economy, stocks or the U.S. dollar. In terms of economic reality, consider corporate revenues. Sales of the companies in the S&P 500 were down year-over-year in the first two quarters of 2015. Again, that doesn't happen outside of a recession. We're in a recession. The stock market will recognize it, along with the global financial community. That is why I am avoiding the market and the U.S. dollar.

TGR: What is an indicator you are watching that will signal a return to favor of commodities in general, gold and oil in particular?

JW: I'm not looking at a stable economy for some time. The U.S. dollar is the key indicator. I'm looking at inflation problems domestically as the dollar takes a hit. In the process, we will see a very sharp increase in the price of gold. Frankly, I would look at holding gold for the long term and riding out what's going to be a terrible financial storm. Physical gold will retain the purchasing power of the assets invested in it and will have the liquidity that you might not have in other assets.

TGR: Thank you, John, for your time.

Walter J. "John" Williams has been a private consulting economist and a specialist in government economic reporting for more than 30 years. His economic consultancy is called Shadow Government Statistics (www.ShadowStats.com). His early work in economic reporting led to front-page stories in The New York Times and Investor's Business Daily. He received a bachelor's degree in economics, cum laude, from Dartmouth College in 1971, and was awarded a master's degree in business administration from Dartmouth's Amos Tuck School of Business Administration in 1972, where he was named an Edward Tuck Scholar.