The Gold Report: At the end of 2014 you described yourself as a reluctant bear on the U.S. stock market. Why?

Joe McAlinden: I said "reluctant" because I really don't like being negative on U.S. equities. After all, stocks go up two years out of three, and so the odds are against betting on a big decline. Nevertheless, after five decades at this game, I have come to believe there are rare moments in market cycles when prudence dictates going against the crowd. And the conditions that I observed at the time had me very concerned about the sustainability of this rally without a big correction. For a while that position seemed out of touch as stock prices surged to all-time highs during the first five months of 2015, but the S&P 500's 12% correction from its peak in May now suggests otherwise. Based on extended valuations, lagging small caps and a more hawkish path toward the normalization of interest rates, the really big decline I have been looking for is, in my view, still lurking dead ahead.

TGR: If your prediction is true, how can investors protect themselves and their portfolios?

JM: There are always some things that go down in a rising market or up in a falling market. . .or at least go up or down by less. Value stocks, for example, have performed very poorly relative to growth stocks for eight years, but we believe this is in the process of reversing. More recently, there are sectors of the markets that have declined significantly more than the broad list of U.S. equities: Energy has been clobbered along with other industrial materials, and precious metals have been annihilated, with the price of bullion down 40% and gold miner stock prices down 80%.

TGR: When we talked in September, you said you were turning into a reluctant bull on hard assets, particularly precious metals and especially gold. Why?

JM: Decades of experience have taught me that trying to catch a falling knife is a dangerous undertaking. Nonetheless, there are a number of reasons why overweighting hard assets like gold looks to me like the right decision at this juncture. Here are four reasons:

Buy Low/Sell High: Gold has been in an almost continual downtrend for over four years, aggregating to a 40% decline while the S&P 500 has soared over 60%. That alone is enough to get an old, opportunistic "buy low" value shopper intrigued. The pattern is similar for other precious metals and, indeed, for oil and numerous other "hard" commodities. In this report, we will focus on gold, but most of the points pertain to other precious and even non-precious metals as well.

Fiat Money Debasement: Following the global financial crisis, major central banks around the world resorted to an unprecedented expansion of their balance sheets to prevent their respective economies from plunging into a deflationary spiral. In the U.S., the Federal Reserve more than quadrupled its balance sheet by buying U.S. Treasury bonds and lots of debt backed by real estate securities. Other major countries have followed suit in varying degrees, most notably Europe and Japan.

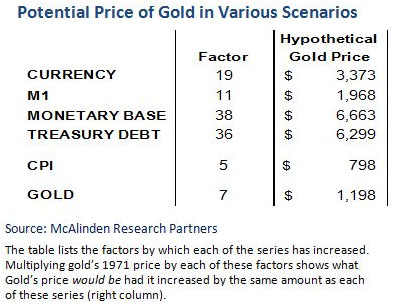

The hockey-stick explosion in central bank balance sheets has been an extension of a long-term uptrend. While gold's value has grown in the long term, along with other precious metals, since the U.S. Treasury moved off the gold standard in 1971, the value of gold has not grown anywhere as much as the quantity of dollars that it once legitimized. Gold is now priced at nearly seven times its 1971 price, while assorted measures of U.S. fiat money creation have exploded up to 38-fold over the same period.

The table also shows where gold would be if it had increased in proportion to the monetary, debt and inflation data over the past four decades. This is NOT a list of projections; rather, it is a hypothetical exercise. If gold experienced the same increase as currency in circulation, its price would be almost triple what it is today. Even more dramatic, gold's hypothetical priceif it had followed the trend of the monetary basewould now be a whopping $6,663 an ounce ($6,663/oz). The only series that has increased less than gold is the consumer price index (CPI).

The inflation that might have been expected to result from this massive money printing has not shown up, at least not yet. Meanwhile, one could say that if gold moves to converge with the CPI, it could fall by around $300/oz. But, if gold converges with these monetary and debt series, its price could rise to between $2,000 and $6,000/oz. For the moment, I am inclined to project that gold prices could at least double over the next few years. I like those odds.

Rising U.S. Rates: Conventional wisdom is that a hike in interest rates is going to hurt gold, but that is not borne out by past data. Indeed, most pundits who had been opining on the precipitous drop in the price of gold have cited the imminent tightening of monetary policy in the U.S. as a reason why gold may continue to decline. Even the very recent strength in gold has been attributed to postponement of the first rate hike. But that reasoning defies the lessons of history, which show that it is not axiomatic that when rates are hiked, gold slumps. Sometimes it has but sometimes it has not.

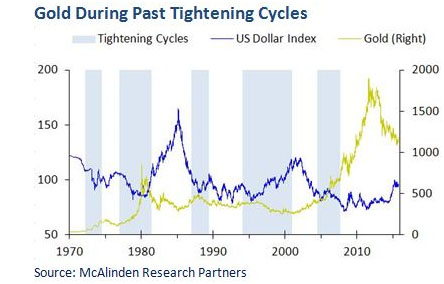

Also, it should be remembered that over the past four years, gold has lost almost half its value in the face of zero interest rates and the easiest monetary policy in history. Indeed, while perhaps counterintuitive, the historical evidence points at times in the opposite direction from conventional wisdom. Since gold was freed from its fixed value in 1971, there have been five major tightening cycles. Gold rose dramatically during three out of five rising rate periods. In the fourth, it rose then fell. Only in the fifth rising rate cycle, in the late 1990s, did it decline.

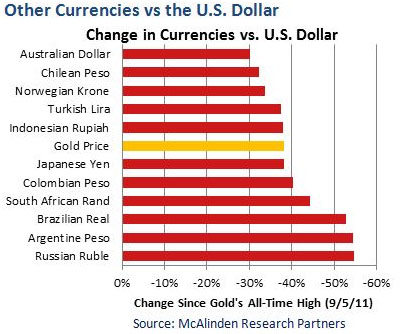

The FX Factor: Because U.S. investors tend to think of gold as priced in dollars, the four-year downtrend misses important trends elsewhere. One by one, major currencies have fallen in value relative to the dollar. Virtually all of the four-year decline of gold is a mirror reflection of the rise in the exchange rate of the U.S. dollar, orlooked at the other way aroundthe profound weakness of most currencies versus the dollar. If one looks at the price of gold denominated in certain other currencies, the bear market turns into a bull market. Some of the most glaring examples can be found among the BRIC and CIVETS, and even a major currency like the yen. Thus, in countries that have experienced the greatest weakness against the dollar, gold is actually at or close to an all time high!

The extraordinary period of strength in the U.S currency may now finally be ending, marking a bottom for gold and reversal of its performance going forward. The economic data for the Eurozone is slowly improving. China will undoubtedly resort to additional stimulus to bolster its economy. The supply-demand picture for energy may also be finally starting to reverse, and there is a positive feedback loop at work. Recent news that major oil producers are ready to meet to discuss global oil markets could be a turning point, and Russia's emergence as a new power player in the Middle East will likely strengthen OPEC's hand and resolve to reverse prices.

TGR: What does this mean for the equities related to the companies producing precious metals?

JM: Mining stocks have fallen over the past four years by twice the percentage decline of bullion. These are operating businesses, and like other commodity-related companies, most of their costs don't go down when the selling price of their product does. But the same should be true on the way back up. If miners move back to their 2011 highs, they would rise fourfold. We think it is time to add the gold miner equities to our list of active themes.

TGR: Thank you for your insights.

Joe McAlinden has over 50 years of investment experience. He is the founder of McAlinden Research Partners and its parent company, Catalpa Capital Advisors. Previously, McAlinden spent more than 12 years with Morgan Stanley Investment Management, first as chief investment officer and then as chief global strategist, where he articulated the firm's investment policy and outlook. He received a bachelor's degree cum laude in economics from Rutgers University and holds the Chartered Financial Analyst designation. McAlinden has served on the board of the New York Society of Security Analysts.