-- Published: Sunday, 22 November 2015 | Print | Disqus

By John Mauldin

The Dysfunctionality of Europe

The Euro: A Suboptimal Currency Union

The Economic Impact of Evil

Merkels Gate Redux

Hollande Shuts the EuroDoor

A Disunited Europe

Hong Kong, Hollywood (Florida), and the Cayman Islands

Political leaders still think things can be done through force, but that cannot solve terrorism. Backwardness is the breeding ground of terror, and that is what we have to fight.

Mikhail Gorbachev

... Europe exemplifies a situation unfavorable to a common currency. It is composed of separate nations, speaking different languages, with different customs, and having citizens feeling far greater loyalty and attachment to their own country than to a common market or to the idea of Europe.

Professor Milton Friedman, The Times, 19 November 1997

There is no example in history of a lasting monetary union that was not linked to one State.

Otmar Issing, chief economist of the German Bundesbank in 1991

The world can change quickly, and last week it did. The most immediate and heartbreaking impacts of the Paris attacks were suffered by the victims themselves and their families, but from there the ripples of terror spread outward around the world.

The Paris events didnt happen in isolation. Recent bombings in Lebanon, Iraq, Mali, and Nigeria, plus the Russian airline disaster, showed us how far evil can reach. It isnt just ISIS: al-Qaeda is getting stronger in some places; Boko Haram continues to strengthen in West Africa; there is a resurgent Taliban in Afghanistan; and the list goes on

In addition to the catastrophic human cost it exacts, terrorism has economic impacts. It misallocates resources, distorts prices, and prompts adverse government policies. We all feel these effects, even if we live far from the terror zones.

Terrorism is global. So is the economy. We cant separate them. Im sure you have spent time reading about the reaction to the terrorist attacks in Paris. I have been reading and thinking a great deal about the effects of recent events on the European Union. Much of what Ive read seems to miss what I think is the larger context and what may be the real longer-term economic and geopolitical implications of these attacks. It should make for an interesting, and somewhat sobering, letter.

The Dysfunctionality of Europe

The European Union works marvelously as a free-trade zone of separate nations, but the visionaries who launched the EU wanted it to be a political union, not just a free-trade zone. They felt that if they could create a political union, then even though the economic problems would be immense, the member countries would eventually come together on the economic front as well. That has not happened. In fact, a fitful political union has made the EUs economic problems worse.

Europe has three basic economic problems, which Ive dealt with at length over the years:

- Capital and goods flow from the peripheral countries of Europe to the core. This huge trade imbalance has no way to resolve itself. The peripheral countries were able to borrow money at German rates for many years, while the politicians in those countries exhibited no discipline in their budgeting process and ran up huge debts and deficits. Then the bill came due.

In the modern world, the normal way to resolve trade imbalances is through currency fluctuations. But in the Eurozone there is now just a single currency, and one size does not fit all.

- Many Eurozone countries have run up unsustainable debts relative to their potential growth. Unsustainable, that is, under a normal interest-rate regime. After the collapse of Greece, the European Central Bank, worried about contagion effects, lowered interest rates dramatically; and countries like Italy took on large amounts of additional debt. What is now nearly a 140% debt-to-GDP ratio in Italy is manageable when interest rates are only a few points. That ratio would be a disaster at 6 to 8%, and Italy would soon be Greece. It should be noted that, even with the low rates, the Italian debt-to-GDP ratio increases each year.

As you may recall, I visited with a senior economist at the Italian central bank a few years back and confronted him about the logic of the countrys debt level and the question of potential interest rate increases. I came away with the distinct impression that the answer was [ECB President Mario] Draghi has our back. I remember remarking to you on the Bank of Italys confidence in the sustainability of what was then a 125% debt-to-GDP ratio.

Draghi gives at least one speech every few months begging the peripheral countries to reform their labor markets and fiscal budgets during this low-interest-rate regime he has given them. He knows it cant last forever and that without market and labor reforms the peripheral nations cannot grow their way out of the debt problem.

- As bad as the entitlement situation is in the US, it is worse in most of Europe, especially in the problem countries (including France!). Given the demographics involved, these countries simply cannot sustain their governments promises. They have no room to increase taxes without severely damaging their economies even further.

The Euro: A Suboptimal Currency Union

Lets deal briefly with the first problem: trade imbalances in the currency zone.

Many of us take our national currencies for granted, and we assume there have always been dollars, pounds, or yen. In fact, for a long time individual banks issued notes promising the holder to exchange the notes for gold upon demand. The concept of a national currency is actually one that came about very late in history.

Before the euro was created, the economist Robert Mundell wrote about what made for an optimal currency area. His work was so important that he won a Nobel Prize for it. He wrote that a currency area is optimal when it has

1. Mobility of capital and labor

2. Flexibility of wages and prices

3. Similar business cycles

4. Fiscal transfers to cushion the blows of recession to any region.

Europe has almost none of these. Very bluntly, that means it is not a good currency area.

As Otmar Issing, chief economist of the German Bundesbank stated in 1991, There is no example in history of a lasting monetary union that was not linked to one State. And that state has to be a fiscal union, which the Eurozone and the EU in general are not. Further, there are significant differences among the economies of the various countries composing the Eurozone.

The United States is a good currency union. The same currency serves just as well in Alaska as it does in Florida and as well in California as it does in Maine. If you look at economic shocks, the US has absorbed them pretty well. If you were unemployed in Texas in the early 1980s after the oil boom turned to bust, or in Southern California in the early 1990s after post-Cold War defense cutbacks, you could pack your bags and head to a state that was growing. And that is exactly what happened. That doesnt happen in Europe. Greeks dont pack up and move to Finland. Greeks dont speak Finnish (no one does, outside Finland). And if unemployed Americans stayed in Texas or California, they would have received fiscal transfers employment benefits and various forms of welfare from the central government to cushion the blow. There is no central European government that can make fiscal transfers. So the US works because it has mobility of labo r and capital as well as fiscal shock absorbers.

There are other good currency unions around the world. China comes to mind, as does Canada. There are numerous countries that work very well as currency unions but are in fact amalgamations of various regions with historically different identities. But those currency unions evolved over time and did not simply turn up one bright New Years day, as the Eurozone did on January 1, 1999, an ostensible union among countries with very disparate economies and wealth.

The euro works like a gold standard. Obviously the euro isnt exchangeable for gold, but like the gold standard, the euro forces adjustments in real prices and wages instead of exchange rates. And, much like the gold standard, it has a recessionary bias. Under a gold standard or the euro regime, the burden of adjustment is always placed on the weak-currency countries, not on the strong countries.

Under a classical gold standard, countries that experience downward pressure on the value of their currency are forced to contract their economies, which typically raises unemployment because wages dont fall fast enough to deal with reduced demand. Interestingly, the gold standard doesnt work the other way. It doesnt impose any adjustment burden on countries seeing upward market pressure on currency values. This one-way adjustment mechanism creates a deflationary bias for countries in recession. The deflationary bias also makes it likely, at least by historical measures, that a gold-standard regime will see a higher average unemployment rate than will a freely floating currency regime.

In the Eurozone, Greece cant simply devalue its currency, or even let the markets do it. So it suffers 25% unemployment (50% youth unemployment) as it tries to bring its trade balance back into equilibrium. The same thing is happening in Spain and the other peripheral countries. To receive the fiscal help they need, they must turn to Germany and the other Eurozone core countries, which impose draconian austerity on the countries receiving help. As I wrote four years ago, the necessary rebalancing process will take at least a decade. Greeces debt will be larger and more unsustainable at the conclusion of that process than it is today. The question is not whether Greece will default on its debt, but when and at what cost.

It is ironic that during the first ten years after the creation of the euro, the European periphery experienced large increases in wages and prices compared to the core. While prices and wages were stagnant in Germany, they grew rapidly at the periphery. This dynamic made the periphery very uncompetitive relative to Germany and the rest of the core. The result? Peripheral countries imported a lot more than they exported and ran large current account deficits. The only way to turn this trend around is through real cuts in wages and prices, resulting in internal devaluations and deflation. This approach is hugely contractionary and has clearly created tremendous problems in the European periphery, starting with massive unemployment. Because there was no available quick fix of actual currency devaluations, the process has been long and ugly, especially if you are a worker in a peripheral country.

All these pressures have created an intense political debate over the policies that should be adopted. In numerous countries we are seeing rising political parties on both the right and the left begin to take market share from the more centrist parties that have been in control for decades. Portugal seems to be in outright revolt, as was Greece for a period of time.

My friend and geopolitical expert George Friedman is pessimistic about the viability of the Eurozone and has said for a long time that he thinks immigration issues will be the final wedge that splits the union. I have been somewhat more sanguine, because the political leadership of Europe, both left and right, is very committed to the idea of a political union. They will do, as Mario Draghi has said, whatever it takes. I think the European Union still has a chance, if only a small and expensive one, to be viable.

The European Union is a wonderful political idea but not a good economic idea. It was politics that created Europe, and it is politics that holds Europe together. The EUs political leaders and other elites are committed to holding it together. Understand, the idea of a United Europe is an article of faith, imbued with all the ferocity and fervor of any religious belief with which Im acquainted.

There are many True Believers in a vision of a United Europe. I believe that, to hold their union together, the leaders at the core will ultimately be willing to absorb all the debts of all the various member nations and put them on the balance sheet of the European Central Bank, basically nationalizing all the debt. They will then be willing to sacrifice their individual countries fiscal autonomy on the altar of the European Union.

All of the problems I mentioned above can be solved by political decision making, but it must be understood that the solutions will come at an unimaginably high cost, running to many trillions of euros. The longer Europe puts off the day of reckoning, the bigger the bill will be. Whatever the ultimate bill is, the euros to pay for the transition will not exist, so they will have to be manufactured; and ultimately the value of the euro itself will be considerably reduced on world markets, just as the current manufacturing of Japanese yen is diminishing that currencys value. If you are a True Believer, you might be willing to pay the price.

Either the Eurozone will be re-forged as a true political union, or it will break up. When you come to the end game, there is really no middle ground. Oh, I suppose that Mario and his successors can print and monetize for another decade, but they cant do so without the euros suffering a large reduction in value. There are going to have to be major reforms, or the euro will continue to adjust. Right now, Europe seems quite comfortable with the idea that the euro will eventually fall to parity with the US dollar. But what happens when the euro is at $.80 to the dollar? Does Europe want to go down that rabbit hole another 25%?

Into that volatile mix of politics and economics, lets now throw in terrorism, immigration, and the refugee crisis.

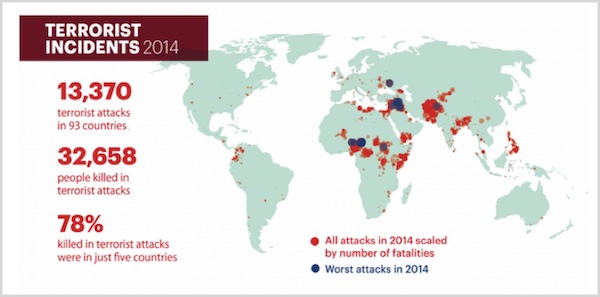

The Economic Impact of Evil

I saw a report referenced on Bloomberg last week that said 2014 was the costliest year for terrorism since 2001, in both financial terms and human lives lost. That assertion seemed remarkable, so I went to the source. The Institute for Economics and Peace is an Australian nonprofit think tank. I cant vouch for their expertise, but their Global Terrorism Index is still interesting.

Their report calculates that the worldwide economic cost of terrorism was $52.9 billion in 2014, an all-time peak. Thats the GDP of a small country, gone up in smoke (literally).

IEP arrives at that number by adding up property damage along with medical costs and lost income for victims. They do not include the indirect costs of preventing or responding to terrorist acts.

How much money does the world spend to cope with the mere possibility of terror attacks? The US Transportation Security Administrations 2014 budget was $7.4 billion. TSA is only one of several agencies focused on terrorism, and the US is only one country.

Think about all the private security guards, construction costs of hardening office buildings, executive and staff time spent dealing with the inevitable headaches and delays, and much more. Pick a very large number. Whatever that number is, you can bet the cost will go much higher after what happened last week. For instance, how much did it cost to shut down Paris for a weekend?

Merkels Gate, Redux

Looking back at my past newsletters is always interesting (and frequently humbling). Its a bit like entering a time machine. Reading what I said in the past underlines how the world has changed in the meantime.

Only two months ago (Sept. 20), in Merkel Opens the Gates,a I looked at Europes refugee crisis. Germanys Angela Merkel had just promised to accept 800,000 refugees this year, and was pushing other countries to help.

I dont often quote myself, but the following excerpt from that letter helps set the stage for what we will discuss below.

And while Merkel says Germany can take 800,000 immigrants, notice that they are instituting border controls to stem the flow. Its is all well and good to say you can absorb nearly a million immigrants, but where you going to put them? How will you feed them or school them? That effort takes planning and time, planning and time that have not been much in evidence the past few years in Europe.

Just as the Grexit crisis showed us the underbelly of European monetary integration, the refugee crisis highlights the huge difficulty of political integration. Hungarians, Slovaks, and Czechs do not want Brussels telling them how many Syrians they must admit and support. I dont blame them.

Ambrose astutely points out that Europe must now deal with an east-west split on immigration along with the still-unbridged north-south economic chasm. Yet EU leaders push blithely on, thinking they can roll right over their opposition. To them each crisis presents another opportunity to impose structure and an artificial unity from the top down.

Read that last sentence again. Have we seen EU leaders pushing top-down solutions to the ISIS-inspired attacks? No. We see the opposite. Countries all pledge cooperation, but they want it on their terms. The EU central command all but disappeared in the aftermath of the Paris attacks. I think this is significant, like the dog that didnt bark in the venerable Sherlock Holmes story.

European unity was already wearing thin before last week. Just two months ago, Merkels German government, along with the EU authorities, thought they could impose their desire to accept more immigrants on the entire union. Eastern European states (and many individuals all over Europe) didnt like that idea at all. They refused to cooperate.

Look what happened next. The German publics initial generosity faded quickly as people grasped the magnitude of the task. Merkels political allies began peeling away. Her grip on power started looking shaky.

Elsewhere in Europe

- Protests again erupted in Greece over EU-imposed austerity measures.

- A left-wing coalition brought down a euro-friendly Portuguese government just two weeks after it took power.

- Spains Catalan region moved forward with its secession effort.

- Brexit sentiment grew in the UK.

The European problem was not improving even before Paris. Then the shooting started.

Hollande Shuts the EuroDoor

You might think all the minor issues would fall by the wayside in a true crisis. Francoise Hollandes first impulse was to reach out to his EU neighbors for help, right?

Wrong. Within hours, he issued orders to close Frances borders with its EU neighbors. There was real fear that more attacks would follow, and Hollande essentially decided that France would stand alone. And indeed, there are reports from the hacker group Anonymous that ISIS plans to strike all over the world today [Sunday].) Yes, Hollande subsequently relaxed, but his initial reaction tells us something important. So does the way Merkel and her EU friends blended into the woodwork when Paris was hit. This isnt what you expect to see in a healthy alliance.

Thats because the EU is not a healthy alliance. Different countries have radically different views of national sovereignty and responsibilities. If they cant put their heads together on handling refugees and fighting terrorism, how can they possibly cooperate on fiscal policy? How can they maintain a common currency? Or maintain enough political support from very nervous voters?

On Monday, Hollande formally invoked the European Union Treatys mutual defense clause, which says member states must help any other member facing armed aggression. What does this mean? No one knows. This is the first time any EU member asked for aid.

It does not sound as though EU leaders are anywhere near a united European response. They have simply agreed to talk about the problems. Meanwhile, ISIS is planning its next attack. This is why Hollande acted alone that first chaotic night and why the euro currency is now several steps further down the path wending toward oblivion.

A Disunited Europe

George Friedman sent around some private thoughts last week. I convinced him to let me share them as an issue of Outside the Box, which you can read here. I think Georges assessment of European unity, or lack thereof, is right on the money. The immigration crisis was already coming to a boil ahead of the Paris attack. Heres George:

Had Europe been functioning as an integrated entity, a European security force would have been dispatched to Greece at the beginning of the migration, to impose whatever policy on which the EU had decided.

Instead, there was no European policy, nor was there any force to support the Greeks, who clearly lacked the resources to handle the situation themselves. Instead, the major countries first condemned the Greeks for their failure, then the Macedonians, as the crisis went north, then the Hungarians for building a fence, but not the Austrians who announced they would build a fence after the migrants left Hungary.

Between the financial crisis and the refugee crisis, Europe had become increasingly fragmented. Decisions were being made by nation-states themselves, with no one being in a position to speak for Europe, let alone decide for it.

Exactly. This is Europes core financial problem as well as its political barrier. The EU nominally speaks for the whole alliance, but it never says much because it takes forever for all the members to decide anything. All it takes is one holdout to bring the whole apparatus to a halt and someone always holds out.

ISIS is not, as Obama said, the JV team. They are the real deal. All the talk Ive read about dislodging ISIS is just that talk. They have 100,000 battle-hardened soldiers, are relatively well-financed, and are remarkably adept at utilizing social media. Paul Kagan estimates that it would take 50,000 troops to create a safe zone for Syrian refugees in Syria and simply to contain ISIS to the territory it holds today.

I think that estimate significantly underestimates the zealotry and ambition of ISIS. They are intent upon establishing a caliphate. They recruit additional psychopathic soldiers every week. They have a functioning government, albeit one that we dont like and one as barbarous and backward as any government the world has seen for centuries. Seriously, they have published manuals explaining that it is perfectly within their religious law to have sex with pre-pubescent girl slaves. And to stone women for offenses against Sharia law, etc. etc.

That Obama said we have contained ISIS is now almost laughable. They may not be growing their territory, but they are not ceding any, either. Twenty thousand pairs of US boots on the ground would not even come close to being enough. And the ability of ISIS to strike deep into the heart of Europe has not been contained at all.

Lets turn to the US for a moment. The exchange between Senators Rand Paul and Marco Rubio in the last Republican debate was illuminating. There is a very clear divide on what military budget priorities in this country should be. There are lots of ideas, but none of them are palatable.

Lets examine just one notion. There are several Republican candidates who would like to arm the Kurds. Okay, lets say we create an army of 250,000 Kurds that is as well-armed as any group in the Middle East. They would be a formidable force; and with US intelligence and airpower, along with that of the rest of our allies in the Middle East, they could lead the attack to roll back ISIS. Seems like a simple enough plan, right?

Well, not exactly. Turkey and Iran would be extremely uncomfortable if not outright hostile to such a scheme. Iraq, such as it is, would be rendered completely incapable of keeping the Kurds from forming their own country and then beginning to absorb more of what we now think of as Iraq. At that point, whats to keep them from absorbing the part of Syria that is Kurdish? Can we even assume that the Kurds would give up any of the territory they took from ISIS? There are large parts of Turkey and Iran that are heavily Kurdish. How would those countries be affected? In addition, there are severe divisions among the Kurds themselves. Arming the Kurds sounds good in theory, but in practice it could be like arming the Taliban in the 1980s to fight the Russians. Then again, it might be a brilliant idea. No one really knows.

Donald Trump wants to stand off and bomb the hell out of ISIS. Okay, that doesnt cost a great deal of US blood, but how many videos of women and children being killed along with ISIS troops are this country and the world willing to stomach? How much blood and treasure are we willing to spend to go back into the Middle East? The free world was willing to go along with massive bombing of mostly civilian cities in World War II, but I doubt there is anywhere near that much resolve today. Most of the cities occupied by ISIS they are sometimes characterized as strongholds are actually heavily civilian, and the citizens have no option to relocate.

There are no good solutions, or at least no attractive ones, for dealing with ISIS. And that reality means they and their terrorist cohorts around the world will continue to be free to operate. Hollande can talk about massive reprisals, but Im not sure reprisals will solve Frances problem of homegrown terrorists.

We should recognize that the terrorists in the recent Paris attacks were basically French citizens growing up in the Muslim ghettos (lets call them what they are), where youth unemployment is 40 to 50%.

The reality is that there are going to be more terrorist attacks in Europe, and every one of them is going to make more European voters increasingly uncomfortable. With each terrorist act, voters are going to grow increasingly restless and increasingly willing to listen to politicians who will promise to control borders and make people safe.

There is already a great deal of economic distress in Europe, and a great deal of political unrest as a result. Throw in a few more terrorist acts, which are almost a certainty given homegrown terrorists and the porous nature of European borders, not to mention the refugee issue (which is going to be massively expensive in the short term), and we may see the centrist parties lose control of the political process. It is no longer outside the realm of probability that anti-EU political parties will take control of major countries in Europe. Marine Le Pen is riding high in the French polls.

If Marine Le Pen is the answer, France is asking the wrong question. I wonder what kind of working partner she would be with Angela Merkel. And thats assuming that Angela Merkel can stay in power. I have to wonder where the political leader who will take the EU forward is going to come from.

Please understand that I am actually pro-immigration, for economic reasons, leaning against the grain of many of my political friends. Europe actually needs immigration, but the kind of immigration they are getting is making their citizens very uncomfortable.

The problems in the Eurozone are already massive and can be managed only with considerable political coordination. There has been precious little political coordination and agreement in the European Union lately. Toss into the mix the current refugee and terrorist crises, and it becomes significantly more difficult, if not impossible, to achieve positive outcomes in Europe. I have no particular love for any of the centrist parties in Europe. And they may well deserve to be voted out. Then again, look how well that turned out for Greece. And the center-right doesnt appear to be doing all that well in Portugal, either.

I dont see how the situation in Europe ends well. And that is sad, because Europe, the Europe I know and love, deserves better.

Hong Kong, Hollywood (Florida), and the Cayman Islands

The schedule in the subhead above sounds hectic, but its not really. Im not scheduled to fly until early January, when I will spend five days in Hong Kong. More on that in future letters. In late January I will be the keynote speaker at the big ETF conference (ETF.com), where a few thousand people will gather to talk about portfolio design in the world of ETFs. Im really looking forward to that. Then Ill return to the Cayman Islands for a speech in early February. I know I have to get to New York and maybe Washington DC sometime betwixt and between; but for me that is a rather sedate travel schedule, which is good, because I need to be spending most of my time researching and writing.

The letter is coming to you a little later than usual because I was able to spend more time than I had originally planned with my friend and Hall of Fame science fiction writer David Brin. David is a fount of knowledge and ideas and a true expert on the issue of privacy in the future. He does a great deal of consulting with various national security agencies on the topics of cybersecurity and privacy. It turns out science fiction writers can actually come up with plausible scenarios that government agencies tend not to come up with.

David and I spent quite a bit of time talking about the nature of privacy. We both expect that what my fellow Baby Boomers think of as their right to privacy will be continually eroded in the future. The recent terrorist attacks will only accelerate that trend. David points out that to think that major government agencies dont already have all the encryption-decoding ability they need is laughable. The whole privacy debate is basically for show.

His solution? Recognize that we are losing our privacy and that the government will have more information about us than any of us are comfortable with. What we have to do is pass very firm laws regarding what they can do with that information and then create far more strict oversight of the various government agencies involved to make sure they dont breach those laws. A few congressional committees will not be not enough.

I saw a poll today that said that 40% of Millennials are actually okay with limiting free speech if it is racist. And we think that our kids are going to be worried about a little invasion of privacy? David says its almost as though there is a conspiracy among all the Millennials to post everything they do on Facebook so that in the future everybody will agree to ignore whats on Facebook when evaluating people. Maybe that is indeed their rationale, because they all do it, though I still get on my kids about what they post on Facebook, even if its generally down the middle.

Its time to hit the send button. In a short while I will be going to the theater to watch the fourth and final movie in the Hunger Games series. I have found the acting of Jennifer Lawrence to be absolutely captivating, as well as that of Donald Sutherland and others in the cast. The films are a stark reminder of what can happen when security becomes more important than liberty. And with that thought, Ill wish you a very good week. We all have much to be thankful for.

Your thinking about how the future will unfold analyst,

John Mauldin

subscribers@MauldinEconomics.com

| Digg This Article

-- Published: Sunday, 22 November 2015 | E-Mail | Print | Source: GoldSeek.com