-- Published: Tuesday, 8 December 2015 | Print | Disqus

By Frank Holmes

Among the endangered species in Sweden are the gray wolf, European otterand cash. Back in June, I shared with you the story of how, in 1661, the Scandinavian monarchy became the first country in the world to issue paper money. (It was an unmitigated disaster, by the way.) Now it might be the first to ban it altogether.

All across Sweden, cashthe physical kind, not cash in the bankis disappearing. Many if not most businesses have stopped accepting it. ATMs are now as uncommon as pay phones. Churchgoers tithe using mobile apps. Fewer and fewer banks even accept or dole out cash.

Heres the chart showing the decline in the average yearly value of Swedish banknotes in circulation:

click to enlarge

So whats going on?

For one, the Swedish people have enthusiastically embraced mobile payment systems. Even homeless newspaper vendors now carry card scanners.

But thats not the concerning part.

Cashs demise appears to be orchestrated by Swedens central bank, which of course stands to benefit from the switch. In a purely electronic system, every financial transaction is not only charged a fee but can also be tracked and monitored. Plus, taxes cant be levied on cash thats squirreled away in Johans sock drawer.

Since July, interest rates in Sweden have lingered in negative territory, at -0.35 percent, forcing accountholders to spend their money or else see their balances slowly melt away. Negative rates can also be found in Denmark and Switzerland, where theyre as low as -1.25 percent. The Swiss 10-year bond yield plummeted to -0.40 percent on Tuesday, which means people are paying the government to hold their investment.

Nick Giambruno, senior editor of Casey Researchs International Man, calls negative interest rates in a cashless society a scam. His perspective is worth considering:

If you cant withdraw your money as cash, you have two choices: You can deal with negative interest rates... or you can spend your money. Ultimately, thats what our Keynesian central planners want. They are using negative interest rates and the War on Cash to force you to spend and stimulate the economy.

The War on Cash and negative interest rates are huge threats to your financial security. Central planners are playing with fire and inviting a currency catastrophe.

Sovereign Man goes even further, writing:

Financial privacy has been destroyed. Banks are now merely unpaid spies of bankrupt governments, and they will freeze you out of your lifes savings in a heartbeat if some faceless bureaucrat orders them to do so.

Never-ending Regulations Suffocate Small Businesses and Investors

Over the years, weve seen corrupt, unbalanced fiscal and monetary policies wreak havoc in socialist countries all around the globe where governments often feel entitled to restrict and even confiscate their citizens assets. In 2008, Argentina nationalized approximately $30 billion in private pension funds. A little over two years ago, the Cyprus government ransacked citizens bank accounts to fix its own mistakes and mismanagement. Last year Venezuela put $700 credit card spending limits on vacationers visiting Florida. Limitations on how much someone can spend and save can be found in many countries, from Italy to Russia to Uruguay.

In example after example, peoples rights to save and freely hold cash have been disrupted, with tragic resultsand today were seeing these disruptions in first-world countries such as Sweden, Switzerland and Denmark.

I have faith that the dynamic American political system will not allow these things to happen, but we need to be aware of events in other countries and be vigilant in protecting our assets.

At the same time, many poor policies here at home have disrupted how we save and spend. For example, its easier to open a credit card account than a savings or investment accountwhich obviously doesnt encourage either of those things.

And a recent flood of new regulations passed down from the federal government continues to suffocate small businesses. Since 1960, the Code of Federal Regulations has grown from 22,877 pages to a bloated 175,268 pages in 2014.

click to enlarge

A 2014 study conducted by the National Association of Manufacturers found that these regulations came with a hefty price tag of $2 trillion in 2012 alone, an amount equal to 12 percent of GDP. The negative effects of these laws trickle down for years through various businesses and industries, costing jobs and opportunities at wealth creationand ultimately creating a downward multiplier effect on the countrys economy.

In December 2013, USGI made the decision to exit the expensive money market fund business because of the increasing regulatory cost of anti-money laundering laws and FATCA. It had become too costly to bear the expense of subsidizing yields so they didnt fall below zero. With zero interest rates and increasing regulatory costs, protecting the integrity of the $1 net asset value (NAV) had cost the money market fund industry nearly $24 billion in waived expenses between 2009 and 2013, according to the Investment Company Institute (ICI).

So what can we do to protect our wealth? One option is to store a portion of it in gold, which, compared to a basket of 24 commodities, has held on to its reputation as a long-term store of value.

click to enlarge

American consumers recognize golds resilience and took advantage of lower prices in November. The U.S. mint sold 97,000 ounces of gold coins, up 185 percent from October, after selling out. Meanwhile, American Eagle silver coins hit an all-time annual sales record of 44.67 million ounces.

I always recommend having 10 percent of your portfolio in the yellow metal5 percent in gold stocks, the other 5 percent in coins and bullion.

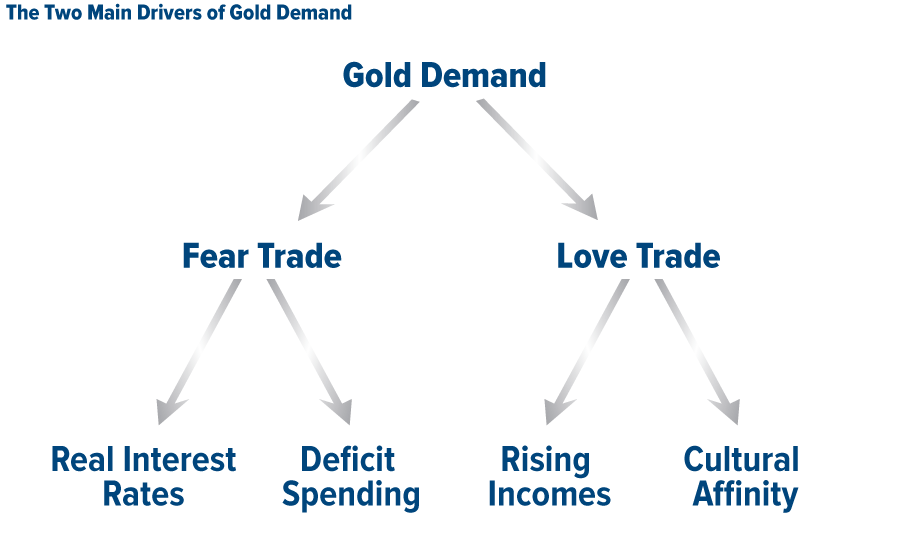

Gold has two pillars of demand: the Love Trade and the Fear Trade.

click to enlarge

The Love Trade is associated with traditional gift-giving during the Indian festival and wedding seasons, Christmas and the Chinese New Year. The Fear Trade, on the other hand, has to do with what were seeing in Sweden and elsewhere. Negative interest rates and poor government policies wipe out citizens ability to save. In such scenarios, investors have historically found shelter in gold.

The Chinese Renminbi Just Went Mainstream

Speaking of currencies, the International Monetary Fund (IMF), as expected, moved to include the Chinese renminbi in its Special Drawing Rights (SDR) currency basket last week, a decision that solidifies the Asian giants prominence in the global financial system.

This is indeed an historic milestone, not just for China but also emerging markets in general. The renminbi, also known as the yuan, is the first currency from such a country to join the elite ranks of the U.S. dollar, British pound, euro and Japanese yen. Global intelligence company Stratfor calls this the start of a new era in the global economic structure and an acknowledgment of economic power in new parts of the world.

Its worth pointing out that the inclusion is largely symbolic. Many analysts are pointing out that it will have little near-term benefit to China, especially since the change will not go into effect until October 2016.

But according to BCA, among the long-term implications of IMF inclusion is that the renminbi should eventually claim over 5 percent of global official reserves, or $400 billion, up from about 1 percent. Currently, the renminbi ranks seventh worldwide as a percentage of global reserves, behind the Australian dollar and Canadian dollar.

click to enlarge

To have the renminbi recognized as a reserve currency has been an important fiscal priority for Chinese leadership in recent years. This summer, the countrys central bank announced it had added to its gold reserves substantially, and later it devalued the renminbi 2 percent. That its finally been added to the SDR is a huge PR win.

It also means, though, that further economic reforms will need to be made. Country leaders are now charged with ensuring that the renminbi lives up to its status as a high-quality international reserve currency by maintaining its stability and ease of use.

Global Manufacturing Poised for a Strong 2016

Just as we head into the new year, global growth bounced back a bit, alleviating investors fears that we were sliding into a recession. Although the global manufacturing purchasing managers index (PMI) cooled somewhat in November, it stayed above the three-month moving average for the second month in a rowsomething it hasnt done in a year and a half.

click to enlarge

Chinas manufacturing stabilized in November after six straight months of declines. The Asian giant posted a 48.6 for the month, up slightly from 48.3 in October. Its still below the key 50.0 mark but headed in the right direction.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

The J.P. Morgan Global Purchasing Managers Index is an indicator of the economic health of the global manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P GSCI Enhanced Total Return Index reflects the total return available through an unleveraged investment in specific commodity components of the S&P GSCI.

| Digg This Article

-- Published: Tuesday, 8 December 2015 | E-Mail | Print | Source: GoldSeek.com