-- Published: Tuesday, 22 December 2015 | Print | Disqus

By Frank Holmes

What were you doing in June 2006?

Thats when the Federal Reserve last raised interest rates, just a year after the last Star Wars flick hit theaters. The biggest movie at the time was Adam Sandlers Click, the hottest song, Shakiras Hips Dont Lie. The best-performing S&P 500 Index stock for the month was C.H. Robinson Worldwide. And as for Janet Yellen, she was president of the Federal Reserve Bankof San Francisco.

On Wednesday, Chair Yellen announced that, for the first time in seven years, easy money will become slightly less easy. The target rate will be set at between 0.25 and 0.50 percent, which doesnt sound like much, but its important that the Fed ease into this cycle cautiously and gradually. Plus, this comes at a time when fellow industrialized nations and economic areas around the globe are considering further monetary easing measures.

Effects and Possible Ramifications: Keep Calm and Invest On

Rising rates, of course, have a noticeable effect on mortgages, car loans and other forms of credit. Savers will finally start earning interest again.

The question on investors minds, though, is what effect they might have on their investments. After all, the last couple of days have been challenging for stocks, with the S&P 500 dropping 1.5 percent on Friday alone. Is the Fed decision to blame?

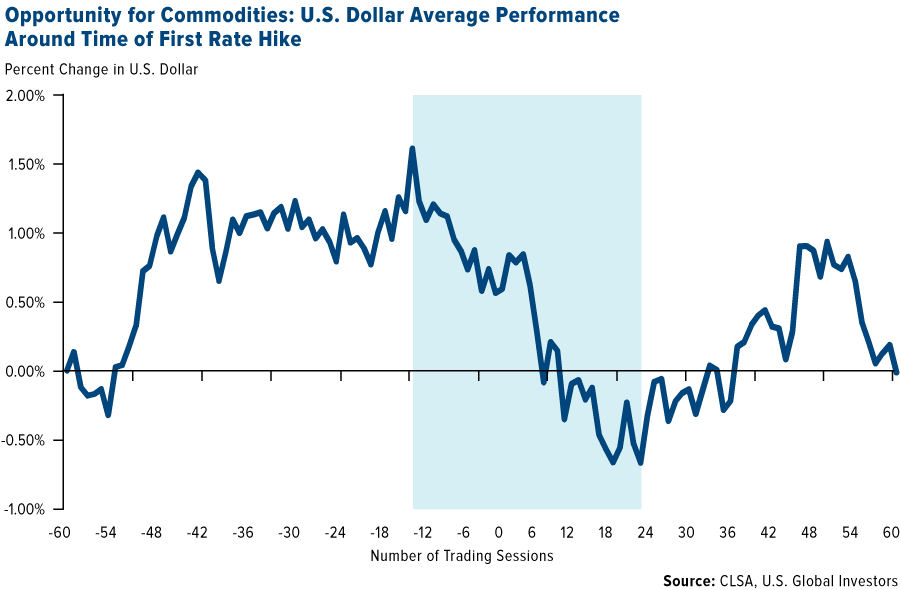

To answer this, CLSA analyzed what happened to the U.S. dollar and stocks in the S&P 500 Index 60 trading days before and after the initial rate hike in past cycles and then calculated the averages. Its important to keep in mind that, aside from rising interest rates, a multitude of unique factorsfrom geopolitics to economic conditions to the weatherplayed roles in influencing the outcomes. Nevertheless, CLSAs research is instructive.

The group finds that, on average, the U.S. dollar peaked 10 trading days before the rate hike, and then afterward slid lower for four to five weeks. This created an agreeable climate for gold and other precious metals and commodities, as their prices typically share an inverse relationship with the dollar.

But CLSAs analysis looks only at possible near-term scenarios. What about the long-term?

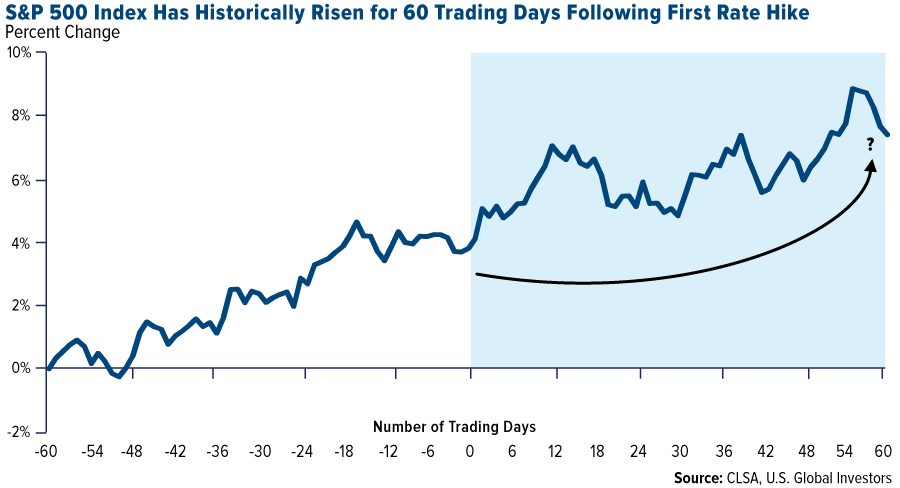

In the past, the results were just as reassuringmost of the time. Barrons records S&P 500 returns 250 and 500 days following the initial rate hike in six monetary tightening cycles going back to 1983. The findings suggest that the market went through an adjustment period, with average returns falling from 14 percent before the rate hike to 2.6 percent 250 days afterward. But by 500 days, returns returned to their pre-hike average of around 14 percent.

Equities Survived Previous Fed Rate Hikes S&P 500 Index Returns Before and After Rate Increases

Performance Before/After Initial Rate Hike

Date of Initial Hike

250 Days Before

250 Days After

500 Days After

5/2/1983

36.60%

-1.10%

12.20%

12/16/1986

19.10%

-5.90%

11.20%

3/29/1988

-11.40%

11.70%

30.60%

2/4/1994

5.30%

0.60%

34.10%

6/30/1999

19.70%

6.00%

-10.70%

6/30/2004

14.80%

4.40%

9.10%

Average

14.00%

2.60%

14.40%

Past performance does not guarantee future results. Source: Barrons, U.S. Global Investors

Again, many other factors besides interest rates contributed to market behavior in each instance. And this time is especially different, as the market was given an unusually long runway, allowing it to price in the full effects of the liftoff before it finally happened.

I cant say whether the same trajectory will be taken this time as before, but what CLSA, Barrons and others have found should be encouraging news for commodities and stocks.

I should also point out that according to the presidential election cycle theory developed by market historian Yale Hirsh, markets do well in a presidential election year.

The consumer price index came out this week and, with an inflation rate of 2 percent, the 5-year Treasury yield is now negative. (The real interest rate is what you get after subtracting inflation from the 5-year government bond.) This bodes well for gold. Also, the 10-year bond yield is lower than it was six months ago.

Investors Flee Junk Bonds and Defaulting Energy Companies, Find Comfort in Tax-Free Muni Bonds

In 2008, the Fed trimmed rates to historically-low levels in response to the worst financial crisis since the 1930s. Most people would agree that this helped put the brakes on the U.S. slipping further into recession.

But low rates were also partially responsible for driving many investors into riskier investments over the last few yearscorporate junk bonds among themas they sought higher yields.

Junk bonds, or high-yield bonds, are known as such because they have some of the lowest ratings from agencies such as Moodys and Standard & Poors. Because they carry a higher default risk than investment-grade bonds, they offer higher yields.

But with corporate default rates nearing 3 percent for the year, and at least one large high-yield bond fund cutting off all redemptions, investors are facing liquidity problems and learning the hard way why these equities are commonly called junk.

The week before last, it was announced that a high-yield bond fundwhose assets under management were worth $2.5 billion as recently as 2013would be closing after suffering nearly $1 billion in outflows this year. This sent the junk bond market into panic mode, with several similar funds experiencing near-record outflows. Fears intensified when legendary investor Carl Icahn tweeted: Unfortunately I believe the meltdown in High Yield is just beginning.

To make matters worse, high-yield bonds have fallen into negative territory, giving investors little reward for the risk.

Energy companies, highly leveraged since oil began to spill value in the summer of 2014, top the default list for the year. JPMorgan estimates that the industrys overall default rate might hit 10 percent next year.

Junk bonds will likely be dead money for at least several years, says Tony Daltorio, writing for Wyatt Investment Research. Put your money elsewhere.

But where, exactly, is elsewhere?

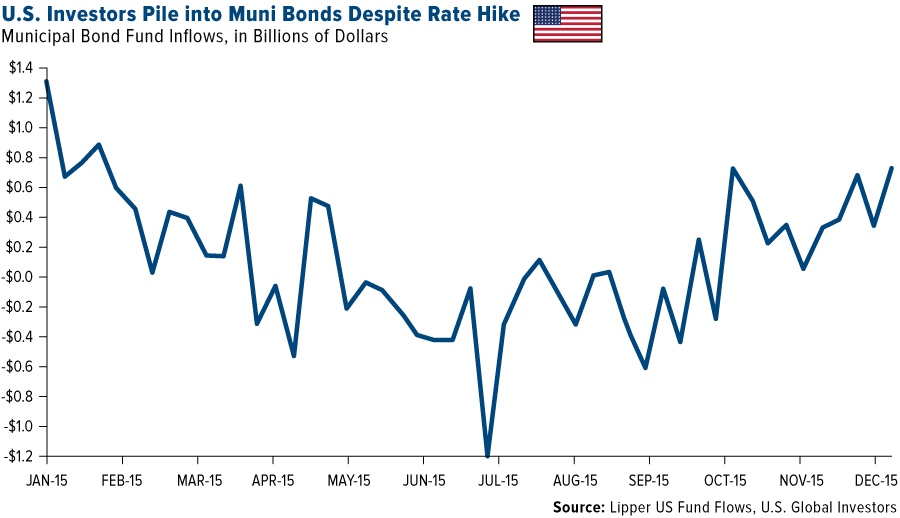

With rates now on the rise, many investors have turned to investment-grade, short-term municipal bonds, which have seen inflows at the fastest pace since January.

Savvy investors know that bond prices move in the opposite direction of interest rates, but shorter-term munis are less sensitive to rate fluctuations than longer-term bonds. Put another way, bonds that are more sensitive to changes in the interest rate environment will have greater price fluctuations than those with less sensitivity.

As municipal bonds head toward the strongest returns in the U.S. fixed-income markets this year, investors say the end of near-zero interest rates will do little to knock state- and local-government debt off its stride, Bloomberg writes.

Over the past seven years, low rates certainly contributed to one of the strongest bull markets in U.S. history. Now that easy money is coming to an end, we can expect to see more volatility. But as the CLSA and Barrons data show, theres still plenty of room for growth.

Its important, therefore, to stay diversified. Focus on high-quality, dividend-paying stocks; investment-grade, short-term municipal bonds; and, as always, goldfive percent in gold stocks, the other five percent in bullion.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The U.S. Corporate High-Yield Index covers the USD-denominated, non-investment grade, fixed-rate, taxable corporate bond market. Securities are classified as high-yield if the middle rating of Moodys, Fitch, and S&P is Ba1/BB+/BB+ or below. The index excludes emerging markets debt. The Barclays 3-Year Municipal Bond Index is a total return benchmark designed for short-term municipal assets. The index includes bonds with a minimum credit rating BAA3, are issued as part of a deal of at least $50 million, have an amount outstanding of at least $5 million and have a maturity of 2 to 4 years.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time.

None of U.S. Global Investors Funds held any of the securities mentioned in this article as of 9/30/2015.

The content on this site is protected

by U.S. and international copyright laws and is the property of GoldSeek.com

and/or the providers of the content under license. By "content" we mean any

information, mode of expression, or other materials and services found on GoldSeek.com.

This includes editorials, news, our writings, graphics, and any and all other

features found on the site. Please contact

us for any further information.

Live GoldSeek Visitor Map | Disclaimer

The views contained here may not represent the views of GoldSeek.com, Gold Seek LLC, its affiliates or advertisers. GoldSeek.com, Gold Seek LLC makes no representation, warranty or guarantee as to the accuracy

or completeness of the information (including news, editorials, prices, statistics,

analyses and the like) provided through its service. Any copying, reproduction

and/or redistribution of any of the documents, data, content or materials contained

on or within this website, without the express written consent of GoldSeek.com, Gold Seek LLC,

is strictly prohibited. In no event shall GoldSeek.com, Gold Seek LLC or its affiliates be

liable to any person for any decision made or action taken in reliance upon

the information provided herein.