-- Published: Tuesday, 5 January 2016 | Print | Disqus

By Frank Holmes

Earlier, I reflected back on 2015 by revisiting the 10 most popular posts of the year. Today Id like to look ahead to 2016 by pinpointing three asset classes that I believe hold opportunities for investors.

Gold

Going forward, gold prices will largely be affected by U.S. monetary policy. The Federal Reserve began its interest rate-normalization process with a small but significant 0.25 percent increase, and unless the Fed has reason to mark time or reverse course in 2016, rates should continue to rise steadily.

This will bump up not just the U.S. dollarwhich historically shares an inverse relationship with gold, since its priced in dollarsbut also real interest rates. As Ive discussed many times before, real rates have a huge effect on the yellow metal.

Real interest rates are what you get when you deduct the rate of inflation from the 10-year Treasury yield. For example, if Treasury yields were at 2 percent and inflation was also at 2 percent, you wouldnt really be earning anything. But if inflation was at 3 percent, youd see negative real rates.

When gold hit its all-time high of $1,900 per ounce in August 2011, real interest rates were sitting at negative 3 percent. In other words, if you bought the 10-year, you essentially lost 3 percent a year on your safe Treasury investment. Since gold doesnt cost anything to hold, it became more attractive, and the metals price soared.

But today, the U.S. has virtually no inflationthe November reading was 0.5 percentso real rates are running at less than 2 percent.

Across the Atlantic, many investors are now realizing that Europes quantitative easing (QE) programs have failed to improve market performance in any substantial way. Earnings per share growth estimates in the European stock market have not budged. The lack of real growth in this market is a compelling argument for global investors to own gold for the long term.

Low interest rates, higher taxes and tariffs and more labyrinthine global regulations since 2011 are all contributing to the global slowdown. Neither QE3 in Europe nor QE3 in the U.S. has led to a marked improvement in growth. What markets need now to ignite growth are fewer taxes, tariffs and regulations and smarter fiscal policies.

click to enlarge

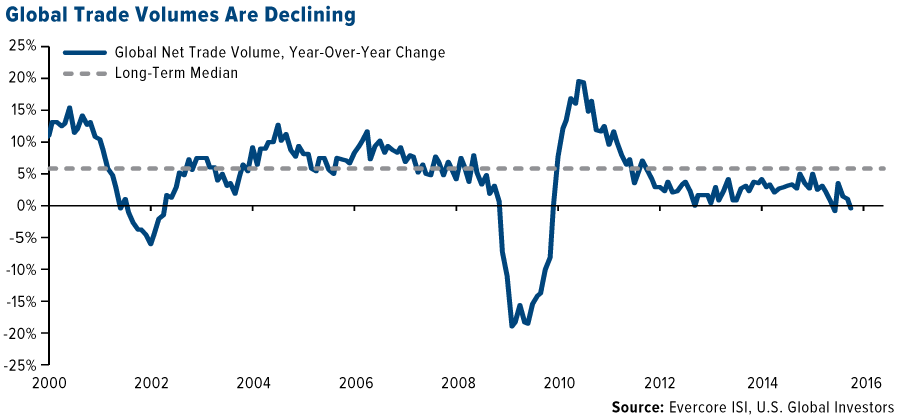

The chart below, courtesy of Evercore ISI, helps to illustrate some of the challenges weve faced in 2015 in terms of the investments we manage. Growth remains scarce globally. M2 money supply in the U.S. also looks dim.

click to enlarge

Looking forward, were hopeful that these two indicatorsglobal trade volume and money supplywill turn up. Both are necessary to improve commodity and emerging market investments.

On the upside, gold demand in China remains strong. Its important to remember that more than 90 percent of demand comes from outside the U.S., in China and India in particular. Precious metals commentator Lawrie Williams reports that Chinese gold withdrawals from the Shanghai Gold Exchange (SGE) crossed above 51 tonnes for the week ended December 18.

Already Chinese demand is higher than the previous annual record set in 2013, and if total withdrawals for 2015 climb above 2,500 tonnes, as Lawrie expects, this will be equivalent to around 80 percent of total global annual new mined gold production. We expect demand to rise even more as we approach the Chinese New Yearhistorically a key driver for golds Love Tradewhich falls on February 8 in 2016.

click to enlarge

Oil

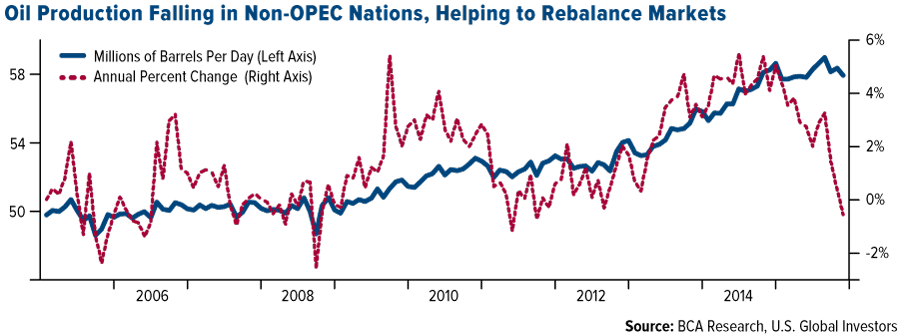

BCA Research believes oil markets will rebalance in 2016, not because of a price collapse but because production will continue to slide and consumption, grow. Most of these adjustments are being made in nonmembers of the Organization of Petroleum Exporting Countries (OPEC). In the U.S. alone, over 600,000 barrels per day have fallen out of the market as the rig count falls.

click to enlarge

Russia, however, is unwilling to cut its production in a bid to compete with OPEC. In November, the country hit a post-Soviet record of 10.8 million barrels produced per day. And even more oil is expected to come out of Iran in 2016 once international sanctions are lifted.

For these reasons, Moodys recently trimmed its 2016 oil forecast. West Texas Intermediate (WTI) crude will average $40 per barrel, down from $48, according to the ratings agency. The projection for Brent was slashed even more significantly, from $53 to $43.

To put this in perspective, oil averaged $55 per barrel in 2015, compared to $85 in 2014.

In all likelihood, then, oil prices probably need to remain lower for longer in order to rebalance the market.

Airlines

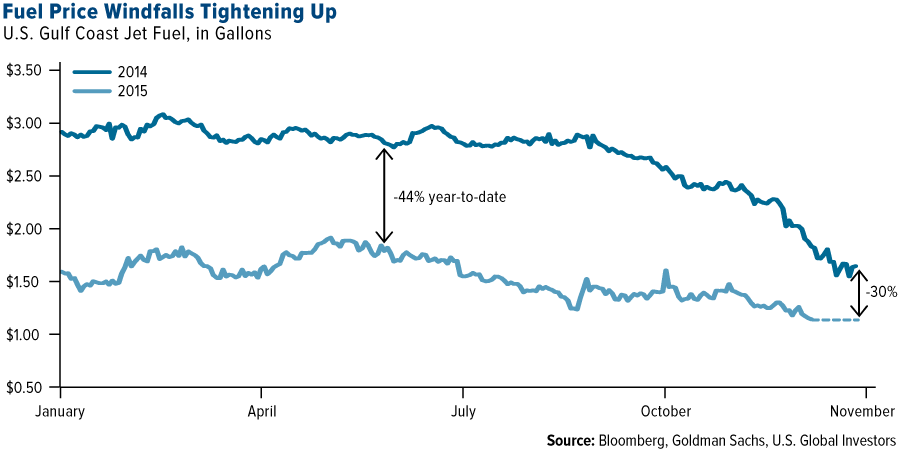

Last month I shared the latest report from the International Air Transport Association (IATA), which states that global airlines will post record net profits of $33 billion for 2015. Because fuel prices are expected to stay low, airlines could very well hit another record at the end of 2016$36.3 billion, according to the IATA.

Savings from lower fuel prices are partially to thank for these profits. Goldman Sachs points out, however, that we shouldnt expect prices to fall at the same magnitude as they did in 2014 and 2015.

click to enlarge

As a result of lower fuel prices and airlines improved discipline in capacity growth and capex spending, the group is poised to see increased operating margins in the coming years, according to Morgan Stanley.

click to enlarge

In short, operating margin tells you what percentage of every dollar made the company keeps as revenue before taxes. The higher the operating margin, the better off the company is.

Ancillary revenue is also contributing more to airlines bottom line. Such revenue comes from non-ticket fees such as baggage and handling, cancellations, seat upgrades, meals and the like. According to ancillary revenue expert IdeaWorks, the total global amount generated from these fees is estimated to rise to a whopping $59.2 billion in 2015, up from $49.9 billion in 2014. That accounts for 7.8 percent of global airline revenue, an improvement from the 6.7 percent in 2014.

The increased revenue is helping to boost domestic airlines free cash flow. Bank of America Merrill Lynch has forecast that airlines will see the highest free cash flow in years, one of the best indications of a companys ability to generate cash.

click to enlarge

Managing Expectations in 2016, a Presidential Election Year

As we reflect back on 2015, its important to remember that everything happens in cyclesfrom the presidential election cycle to the gold seasonality cycle and even to weather patterns. Similarly, every asset class has its own DNA of volatility.

By recognizing these cycles and patterns, it becomes easier to manage your expectations and become more proactive than reactive. With that in mind, Id like to focus specifically on opportunities and threats for the coming year.

1. 2016 is the fourth year of the presidential election cycle. According to research by market historian Yale Hirshand later his son Jeffreymarkets have tended to perform well in presidential election years. Between 1833 and 2012, the Dow Jones Industrial Average rose on average 5.8 percent during election years.

2. After a flat year, 2015 being one of them, the market has historically been up, as you can see in the table below:

3. The Trans-Pacific Partnership (TPP) should help spark a light under global trade by eliminating thousands of tariffs and other barriers that currently stand in the way of foreign investment.

4. China, an essential market for commodities demand growth, continues to stimulate its economy with low interest rates and financial stimulus.

5. As for potential threats, the biggest one in the new year continues to be global terrorism. Aside from the fact that it has increasingly made society feel less safe, terrorism reportedly cost the world $53 billion in 2014 alone, according to the latest data from the Institute for Economics and Peace. Thats the highest amount since 9/11.

I want to wish all of our readers and shareholders the very best in 2016! I would also like to invite each of you to subscribe to our free, award-winning Investor Alert newsletter and share it with family and friends.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

M2 Money Supply is a broad measure of money supply that includes M1 in addition to all time-related deposits, savings deposits, and non-institutional money-market funds.

The Dow Jones STOXX 600 Index is an index of 600 stocks representing large-, mid- and small-capitalization companies in the developed countries of Europe. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

| Digg This Article

-- Published: Tuesday, 5 January 2016 | E-Mail | Print | Source: GoldSeek.com