Gold demand resilient in 2015 as central banks and consumers spur strong H2-2015 recovery - Infographic

-- Published: Thursday, 11 February 2016 | Print | Disqus

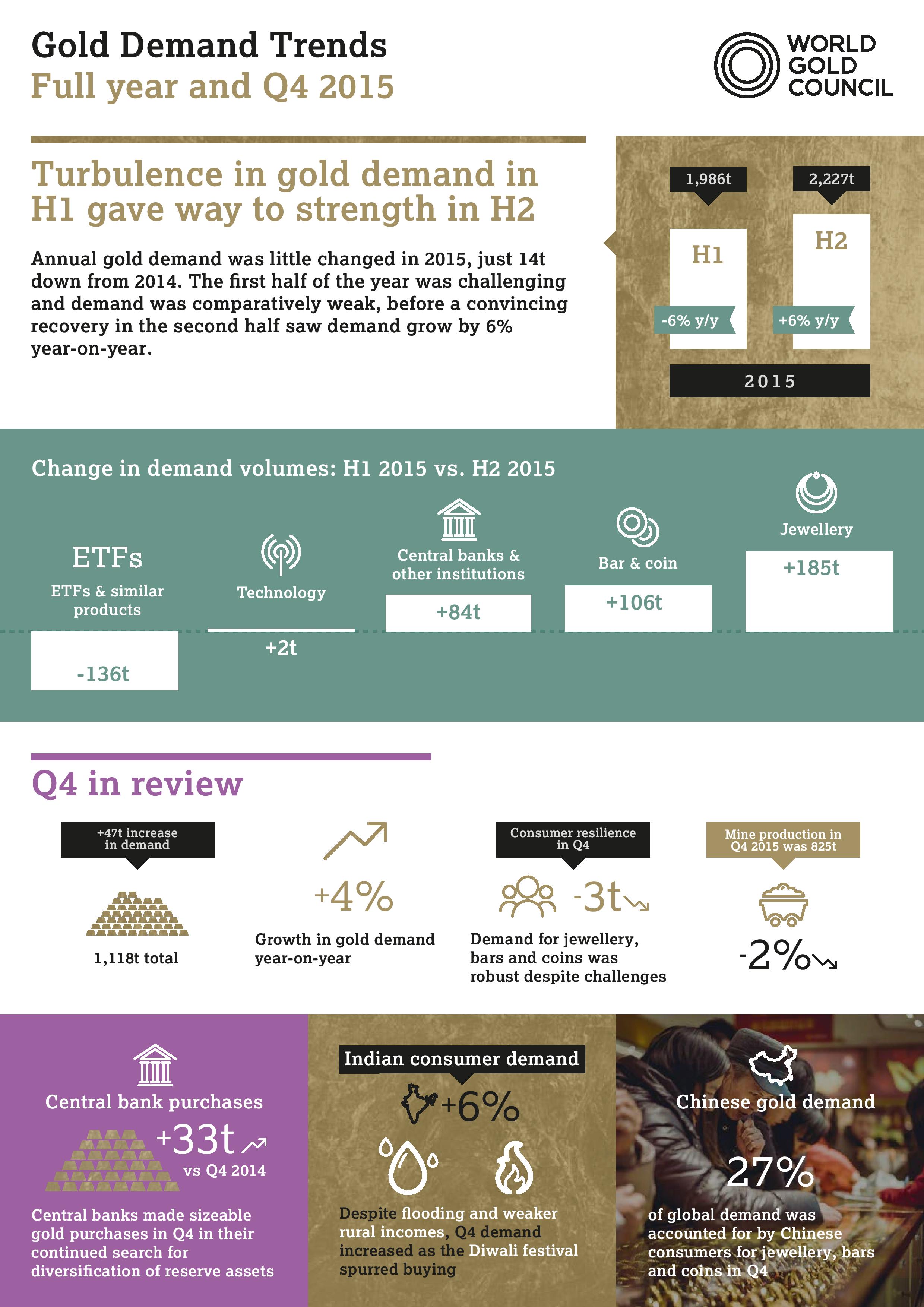

Global gold demand in 2015 was virtually flat compared to 2014 at 4,212 tonnes (t), according to the World Gold Councils latest Gold Demand Trends report. Despite a challenging start to the year, gold demand rebounded in the second half of 2015 as a result of sustained buying from central banks and a strong second half from China and India.

This was particularly evident in the retail investment sector, where bar and coin purchases were led by China and Europe, with strong support from the US, as investors took advantage of weaker prices amid a softening economic backdrop, financial turbulence and ongoing geopolitical tension.

Global investment demand for the full year 2015 grew by 8% to 878t from 815t in 2014. Bar and coin demand remained steady in 2015 as investors took advantage of a weaker price in Q3. The ETF market saw a slowdown in outflows: 133t in 2015, compared to 185t in 2014. Q4 2015 witnessed a continuation of these trends with a number of key regions experiencing double digit growth.

Overall jewellery demand for the full year 2015 was down 3% to 2,415t from 2,481t in the previous year. Following a slower start to the year, the third and fourth quarters combined produced the strongest second half-year total for gold jewellery in 11 years. Q4 2015, saw steady levels of jewellery demand, at 671t compared to 677t in the same period last year, with retailers reporting an increase in sales around the Indian festival period.

Central Bank demand for the full year 2015 saw a small uptick from 584t in 2014 to 588t in 2015 as the need for further diversification was reinforced by a tumbling oil price and reduced confidence in the global economy. Demand in Q4 continued to be strong, up 25% to 167t from 134t in Q4 2014, making this the 20th consecutive quarter of net purchasing.

Gold demand in Q4 showed further positive signs, following a strong third quarter. In India both the investment (60t) and jewellery (173t) sectors were up 6%, boosted by the festival season. In China, which has witnessed economic turmoil, consumer uncertainty and currency weakness, gold demand held up well, particularly in the investment sector up 25% to 48t for the quarter.

Alistair Hewitt, Head of Market Intelligence at the World Gold Council, said:In a year that saw global economic and stock market turmoil, the first US interest rate rise in nine years and falling oil prices, demand for gold remained resilient, coming in at 4,212 tonnes for the full year. Official sector purchases, combined with strength in the Asian markets and continuing momentum in the US and Europe, reinforced golds credentials as a portfolio diversifier, a wealth preservation tool and a hedge against a range of risks.

Looking ahead, physical demand will continue to be supported by strong central bank purchases, and continued buying of jewellery, bars and coins by households across the world, led by India and China. If we just look at the year to date, the investment case for gold is as strong as ever. While stockmarkets have wobbled, gold has performed well.

Full year 2015 saw China (985t) and India (849t) continue their dominance in the global gold market, accounting for close to 45% of total global gold demand during 2015, with annual consumer demand in both up 2% and 1% respectively.

Total supply for the year experienced a drop of 4% to 4,258t for the Full Year 2015 compared to 4,414t in 2014. This is reflective of both recycling hitting multi-year lows and mine production growth falling to its lowest level since 2008. Mine production contracted in Q4, the first quarterly contraction since 2008, as cost cutting took effect. Q4 2015 reported a more substantial decline of 10% to 1,037t compared to 1,152t in the same period last year as primary production slowed as a result of weaker gold prices, mine closures and project delays.

Overall demand was 4,212t, virtually flat when compared to the 2014 figure of 4,226t

Total consumer demand was 3,427t, a 2% decline compared to 3,481t in 2014

Global investment demand was 878t a growth of 8% from 815t in 2014

Global jewellery demand in 2015 was down 3% to 2,415t from 2,481t in 2014

Central bank demand was virtually flat at 588t compared to 584t in 2014

Demand in the technology sector was down 5% to 331t from 346t in 2014

Total supply was down 4% to 4,258t compared to 4,414t in 2014 with total mine supply down 2% to 3,165t from 3,244t in 2014

Q4 2015

Overall demand increased 4% to 1,118t compared to 1,071t in Q4 2014

Total consumer demand was virtually flat at 935t compared to 938t in Q4 2014

Global investment demand grew by 15% to 195t from 169t in Q4 2014

Global jewellery demand softened to 671t down just 1% from 677t in Q4 2014

Central bank demand grew 25% to 167t compared to 134t in the same period last year

Demand in the technology sector fell 7% from 90t in Q4 2014 to 84t in Q4 2015

Total supply slipped to 1,037t in Q4 2015 compared to 1,152t in the same period last year a decline of 10%, with total mine supply also decreasing by 9% to 810t from 893t in Q4 2014

The World Gold Council is the market development organisation for the gold industry. Our purpose is to stimulate and sustain demand for gold, provide industry leadership and be the global authority on the gold market. We develop gold-backed solutions, services and products, based on authoritative market insight and we work with a range of partners to put our ideas into action. As a result, we create structural shifts in demand for gold across key market sectors. We provide insights into the international gold markets, helping people to understand the wealth preservation qualities of gold and its role in meeting the social and environmental needs of society.

The content on this site is protected

by U.S. and international copyright laws and is the property of GoldSeek.com

and/or the providers of the content under license. By "content" we mean any

information, mode of expression, or other materials and services found on GoldSeek.com.

This includes editorials, news, our writings, graphics, and any and all other

features found on the site. Please contact

us for any further information.

Live GoldSeek Visitor Map | Disclaimer

The views contained here may not represent the views of GoldSeek.com, Gold Seek LLC, its affiliates or advertisers. GoldSeek.com, Gold Seek LLC makes no representation, warranty or guarantee as to the accuracy

or completeness of the information (including news, editorials, prices, statistics,

analyses and the like) provided through its service. Any copying, reproduction

and/or redistribution of any of the documents, data, content or materials contained

on or within this website, without the express written consent of GoldSeek.com, Gold Seek LLC,

is strictly prohibited. In no event shall GoldSeek.com, Gold Seek LLC or its affiliates be

liable to any person for any decision made or action taken in reliance upon

the information provided herein.