-- Published: Monday, 18 April 2016 | Print | Disqus

By John Mauldin

The World Is Slowing Down

Never Waste a Good Crisis

An Outside the Box Solution as Big as Our Nations Problems

Some Thoughts on a Convention of States

Dallas, Houston, Abu Dhabi, Raleigh, SIC, and Lemonade Day

I woke up this morning with the sundown shining in

I found my mind in a brown paper bag but then

I tripped on a cloud and fell-a eight miles high

I tore my mind on a jagged sky

I just dropped in to see what condition my condition was in

Yeah, yeah, oh-yeah, what condition my condition was in

Made famous by Kenny Rogers and the First Edition, 1968

For the past five weeks, Ive written an open letter to the next president (whoever it turns out to be) about the economic realities he or she will face in the Oval Office on the first day. It is a rather daunting set of challenges. I have been trying to provide a realistic assessment of what condition our condition is in. The song the lines come from was actually a semi-veiled warning about doing LSD. My letters have been overt warnings about the economic dangers the next president and the country and the world will face.

In this weeks letter we will take a quick look at the condition of a slowing global economy (the IMF just downgraded its own forecast this last week). Then well grapple with a Plan B scenario, because I have a confession of sorts: I am not entirely optimistic that Congress and the new president can get their act together, so I offer a proposal from former Oklahoma Senator Tom Coburn as to what we, the people, can do to actually change the countrys direction without having to depend on a Congress that may prove dysfunctional. Again.

The World Is Slowing Down

Jeffrey Snider of Alhambra Investment Partners sent out a note last week highlighting some of the current conditions. In his piece entitled Not Just Manufacturing, the Global Slowdown Is Monetary, Jeffrey cites a Wall Street Journal article that highlights the very serious slowdown in orders for new big rigs and other trucks. Inventories are at their highest level since before the financial crisis, and sales in March were down 37% from a year ago as fleets remained very cautious about expanding in this environment. Quoting:

Some of this reduction in 2016, as the Journal reports, is due to companies over-ordering in 2014 and 2015 based on the narrative that the economy was actually healing, or at worse would stay in its "new normal." It raises the issue as to whether these conditions and the manufacturing recession they reflect are cyclical or structural, or both.

As I wrote yesterday, the contraction in goods and the US economy's basis for them may or may not be heading toward recession. It is clear, however, that whatever the ultimate cycle reality, there are deeper imbalances that run back several years, likely traced to decades of financialization that is now overturning, and thus really supersedes cyclical discussion. What we see in the US is not limited to the US, however; it is a global phenomenon, which can only mean one possible explanation.

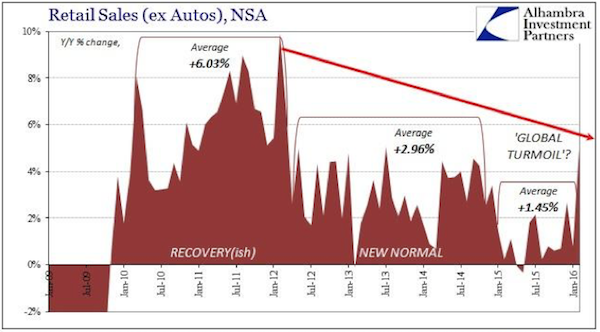

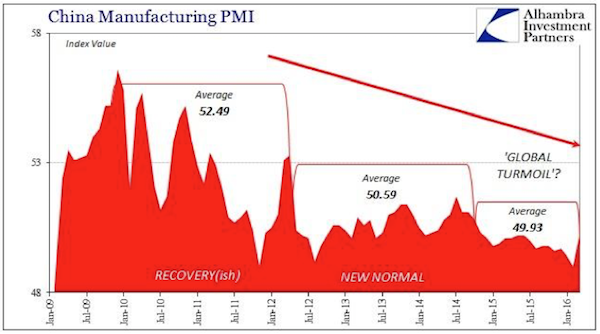

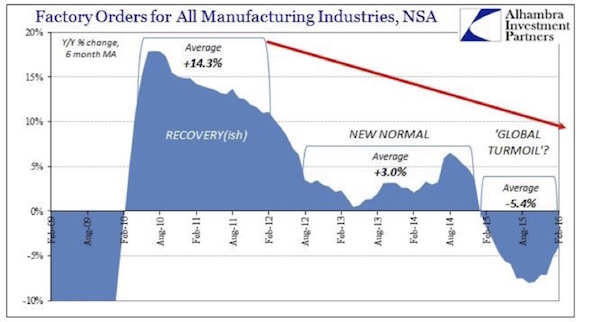

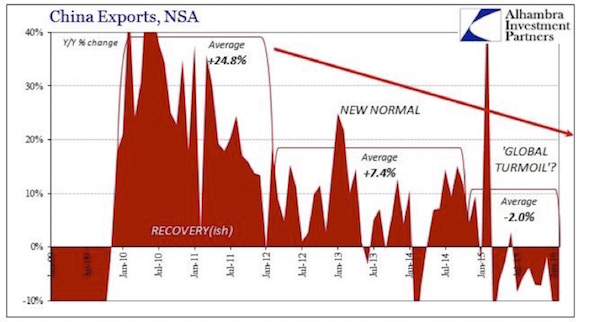

Jeffrey offers several charts that I think tell the story better than 1,000 words.

These charts have slowdown written all over them. And you can see the trend even more clearly when you look at factory orders on a non-seasonally adjusted basis over the years since the recovery:

The slowdown is not limited to the US. Look at what is happening to China exports:

The latest quarterly edition of the China Beige Book was out yesterday. The China Beige Book is just about the only true gauge of the Chinese economy. My good friend Leland Millers firm surveys 2200 Chinese companies every quarter and reports on their findings. Their work is a must-read in serious economic circles. Leland, one of the savviest experts on China there is, provided me with a summary:

Led by rising layoffs at private firms, job growth dropped notably for the second consecutive quarter, sliding to a four-year low. Expectations of future hiring took a similar dive. Overall, the share of firms hiring this quarter fell to half of what we reported in 2012.

This deterioration has wide-ranging implications. Despite the economy's overall deceleration, China has been able to defy calls to be more aggressive either via reform or stimulus because of the remarkable stability of its labor market.

This bought time, but Beijing hasn't used it wisely. If the weakness in employment continues, the credibility of government policy will be challenged by those who matter most: not financial commentators but ordinary Chinese.

Leland went on to point out that this slowdown in hiring has been brought about by two rather uncomfortable trends: First, the multiyear slowdown in capital expenditures is continuing, and now we have seen what almost amounts to a crash as the number of companies reporting capital expenditure growth has plummeted by 40%. Reduced capital expenditures, of course, affect hiring.

And companies, particularly private companies, are borrowing less. Money is available, but they simply dont want it. Theyre trying to square up their balance sheets. Other anecdotal evidence from private sources suggests that what borrowing there is, is being used to pay off dollar-denominated debt. The debt-fueled growth that has driven China for these past seven years, sputtering on fumes now, seems headed for an abrupt end. Likewise, the shift from manufacturing to services seems to have lost momentum.

The government still reports 6.7% GDP growth, but as Leland notes, Chinas weakness is not about GDP:

With perceptions about China likely to guide global markets again in 2016, it has become more important for investors to look beyond headline GDP numbers official or private. After all, Beijing didn't seem overly concerned when many indicators signaled weakness but job growth remained steady. If the opposite combination persists, China's purported restructuring and reform could lose the faith not only of markets, but also of the masses.

I will be writing a detailed letter on Europe in the near future, and quite frankly I view the European economy to be even more problematic than Chinas is.

Brazil is clearly mired in a recession, amid political turmoil. Commodity-market economies have recovered a little bit as prices have bounced off their lows. But the massive dollar-denominated debt in emerging markets is starting to come due, and most EM currencies are much weaker than they were when the debt was initially taken on. Major economic problems are brewing in a number of countries.

I know the equity markets are close to all-time highs, but I also see real interest rates negative out beyond 10 years and certainly below 1% even out to 30 years. Those are not conditions that you see in a dynamic, growing economy.

As Ive been saying for almost two years, the admittedly weak US data still doesnt give me any real conviction about a particular timeline for a recession in the US. But with the US economy barely growing at stall speed, an exogenous shock to the US economy could easily push us into recession. Whenever the next recession comes, it will not look like the last recession.

Never Waste a Good Crisis

In my last two letters I offered a prescription for how to avoid a recession in the United States and how to trigger a new era of growth. Doing so would allow (or perhaps force) the Federal Reserve to normalize interest rates, which would allow savers to benefit once again from their years of saving. Pension funds and insurance companies would actually regain the chance to provide the benefits they have promised.

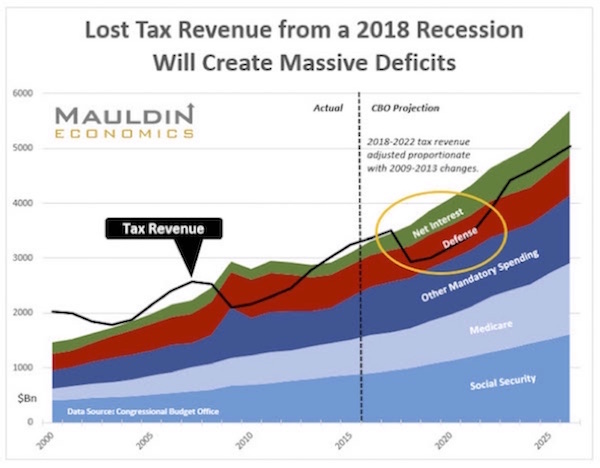

We may not see a recession this year, and hopefully not even next year though thats a hope and not a prediction but sooner or later were going to see one; and if we havent completely revamped our incentive and tax structures, allowing the Fed to normalize rates, monetary policy will be impotent during the next recession, and Congress will be facing $1.5 trillion deficits with very little room to provide any real stimulus. I know I have shown you the following chart in the last two or three letters, but I want you to burn this picture into your mind. This is what is going to happen to the federal deficit when we go into recession:

I have lived through six recessions in my business life and thats the point: we do live through them. This recent recovery has been the weakest we have seen in the last 40 years, and I will make you a side bet that absent any restructuring of the tax and incentive systems, the next recovery will be even weaker, with the real potential for the United States to catch Japanese disease.

But we will suffer the slow-growth, no-recovery symptoms of Japanese disease without the cushion that Japans massive savings and current account surplus provide. We wont have 20 years to muddle through as Japan has done. Unemployment will rise to uncomfortable levels, and I fear that the Federal Reserve will begin to experiment with extreme forms of monetary policy, including negative interest rates. I acknowledge that there are very smart economists who think that negative rates can deliver positive benefits, but I simply think they are wrong. The evidence Im looking at demonstrates that negative rates abuse savers and distort normal markets by obliterating the signals that the price of money (i.e., the interest rate) is supposed to send. The total financialization of the worlds reserve currency will not end well.

As I laid out in my last letters, our economic future doesnt have to end this way. And candidly, the proposals Ive suggested are not the only way that we can sort out our tax and incentive structures and achieve positive results. I can think of quite a few paths we could take. But just tinkering around the edges and more or less doing what were doing now is not going to get us where we need to go.

A recession is an avoidable dilemma, but averting the nasty economic storm that is brewing now will require leadership and compromise that havent been seen in Washington DC for some time. In general, the feedback Ive gotten from my letter to the would-be president series has been quite good much better than I expected. But the one real pushback from friends and readers is the very simple, skeptical question, John, you dont really think that this will happen, do you?

Sadly, I must admit that I dont. I am generally an optimistic person, and I would like to think that the people we elect this fall will do the right thing. But weve been saying that for about 16 years now. Our so-called leaders record on doing the right thing with regard the deficits and the economy is not cause for jubilation.

So, I think the more likely outcome is that well have a recession and $1.5 trillion deficits and mountainous deficits as far as the eye can see, because it is really quite an impossible task to balance the budget without new taxes and growth incentives and without the massive fiscal stimulus that could come by repurchasing the Federal Reserves balance sheet to invest in infrastructure that would create 2 million+ jobs.

It was Rahm Emanual, the beleaguered current mayor of Chicago (why on Gods green earth did he want that job?), who once said, Never let a good crisis go to waste.

While the next recession will surely plunge us into a crisis, that crisis will afford an opportunity that those who want to restructure our federal government. The attempt will, quite frankly, require an end run around Congress. Thankfully, the founders of the republic stuck a helpful little section for that purpose into the Constitution. Its called Article 5. It allows for 34 states to call a Convention of States to propose amendments to the Constitution, which then have to be sent back to the various state legislatures to win the approval of 38 states no small feat. I will readily admit that it will take a crisis to push some of the needed states into the lets just do it category. Getting 34 states to agree is a daunting task, but we might just get the crisis we need to accomplish that, and hopefully the country will not waste it.

The next section is a letter authored by former Oklahoma Senator Dr. Tom Coburn, one of my personal heroes. Tom was demonstrably the most fiscally conservative member of the Senate, constantly trying to figure out how to reform the process and get back to a balanced budget like the one we had in the later Clinton years. Unfortunately, Tom developed cancer (which is now apparently under control, thank God) and term-limited himself. We have corresponded and met off and on, and he is a personal inspiration as well as an enthusiastic believer that things can be changed. We need more like him, and I wish he were back in the Senate.

There are six states that have already passed the legislation necessary for calling a Convention of States. There will be another four or five that do so this year and perhaps between 10 and 12 next year. The organization pushing this issue will thus be able to focus their time and budget on getting the remaining states to make the call. So without further ado, lets look at how we can take the process of fixing the problems in Washington DC back to the people.

An Outside the Box Solution as Big as Our Nations Problems

By Senator Tom Coburn

Precision in numbers is critical to accountants and important to economists. But for most other people, there is a point at which a number gets so big that its increase seems irrelevant. This is a variation of the law of diminishing returns: the bigger the number, the less impact it has, because it is so far removed from anything people can relate to.

That is what has happened with the numbers reflecting our astounding national debt.

Nineteen trillion plus (and rising rapidly) dollars of debt on the books. One hundred forty trillion dollars of unfunded liabilities to boot. How many Americans can truly have any concept of what those numbers mean? If the deficit soon balloons to $1.5 trillion, the problem will become more severe.

And as the numbers continue to grow higher (what comes after a trillion?), ordinary Americans become inoculated to rational concern about the looming disaster they represent. We keep hearing these astronomical figures, but we go on about our business as usual and feel no impact of the predicted storm. Some people even dare to hope that if the right candidate is elected President this year, they will receive more goodies from an increasingly generous Uncle Sam who maintains every outward appearance of being flush with cash.

Unlike a natural disaster, which sometimes comes with little warning and always through no fault of our own, our nations impending financial crisis is completely predictable and is the outcome of a machine we created and continue to operate. It is an outcome of the federal government over which we, the people, have ultimate control.

We got into this mess because we have allowed the feds to operate far beyond their specific, enumerated constitutional powers. However well-intentioned the politicians who envisioned a national government program, policy, or regulation as the answer to every human need or problem, they were wrong. And now we are staring down the hard consequences of glossing over the original meaning of the Constitution, which never allowed for the type of plenary federal government we have today.

This is a hard truth and is difficult to actually process. But what we think is more important to grasp is that our responsibility for causing the crisis is just the flipside of the truth that we hold the power indeed the duty to make a course correction.

Having spent time in Congress, I am just as disillusioned as the next guy with the idea that there is some political solution to the situation that has any realistic prospect of succeeding. Every member of Congress knows that whichever Congress actually passes financial reforms that shut off the flow of money from D.C. will be fired. And politicians tend to want to keep their jobs.

The solution we need and can implement is not merely a political one. It has to be a structural one. It requires us to close the constitutional loopholes that allowed the feds to move beyond their proper, limited authority and initiate programs, engage in spending, and create agencies that are way outside federal jurisdiction under the original meaning of the Constitution.

The way we can realistically do this is through an Article V convention for proposing amendments to the Constitution. This is a state-initiated, state-led, and state-controlled process for proposing amendments that dont sit well with the power-hungry elitists in D.C. It requires two-thirds of the state legislatures (34 states) to pass applications for a convention to propose amendments on a given topic. States then appoint and instruct delegates to represent them at the convention. Any proposals that garner support from the majority of the states (on a one-state, one-vote basis) are then submitted to the states. Proposed amendments must be ratified by three-fourths of the states (38 states) in order to become part of the Constitution.

There is already a massive, nationwide effort underway to trigger an Article V convention for the states to consider proposing a series of very limited amendments that impose fiscal restraints on D.C., limit its power and jurisdiction, and set term limits for federal officials including federal judges.

Its called the Convention of States Project, and it has made huge strides in just a few years. Six states have already passed their applications. Approximately thirty-four more will take up the issue this year. Over 1.2 million people are engaged at some levelfrom volunteer leaders in all 50 states to Facebook followers.

The project has been endorsed by some of the greatest statesmen, economic experts, and legal minds in the country, including Sen. Marco Rubio, Governor Greg Abbott, Thomas Sowell, Mark Levin, Michael Farris, Randy Barnett, Robert P. George, Chuck Cooper, and countless others.

Imagine what America would be like if Congresss taxing and spending power could only be used in relation to its specifically enumerated powers in Article I, as originally intended.

Imagine if we had a robust, functioning federal system again, with the states deciding the lions share of the policies that govern their citizens rather than doing the bidding of Washington, D.C. as it holds their citizens tax dollars hostage.

Imagine if businesses and industries werent assaulted on every side by rules and regulations being crafted by unelected bureaucrats in ivory towers at a rate of over 80,000 new pages a year.

America could be, again, what the Founders intended and designed: a constitutional republic suited for a free, industrious, self-governing people.

Once we do realize that a natural disaster is coming, we take the concrete, necessary steps to prepare for it and protect the lives and property in its path. It must be no different with the national financial crisis we see on the horizon.

We must repair our constitutional levees by mobilizing the states to forcibly impose discipline on a fiscally irresponsible Washington, D.C. And we must ensure that this self-made storm can never be re-created.

Learn more and get involved in the Solution as Big as the Problem, at Convention of States Action. Senator Coburn can be contacted at SenatorTomCoburn@cosaction.com.

Some Thoughts on a Convention of States

The Convention of States Action website has a great deal of information, and I encourage you to look it over carefully. But let me give you some of the highlights. One of the criticisms is that a Convention of States could be a runaway convention. That is not the truth. To call an Article V convention, the states must all pass the same very specific legislation, which limits the agenda of the convention. The convention that is currently being proposed is not meant to deal with a social agenda; it is all about fiscal constraints and process.

What might come out of it would be a series of proposed amendments, such as a balanced budget amendment, a term limit amendment, a definition of what the general welfare clause of Article I of the Constitution actually means, and other amendments that would reduce the power of the federal government in favor of the states on fiscal and operating matters.

But a proposed amendment is just that, a proposal. It then has to be approved by the legislatures of 38 states. That is a tall order. I can see from looking at the proposed agenda for this Convention of States that among the amendments that would be proposed there are some that I would enthusiastically endorse and some about which I would be a little bit reluctant.

It is supposed to be difficult to amend the Constitution. That was by design. I can see a balanced budget amendment possibly getting passed by 38 states, but some of the other proposals might have more difficulty. The states would have the ability to pick and choose among the amendments. They would not have to adopt all in order to get one. That is the genius of the structure of the Article V convention.

When you talk, as I have, to the people who are driving this process, you see that they understand the need for any major change in the budget-control process to be phased in over time. You couldnt make the shift in just one year.

Term limits might have a more difficult time getting through some state legislatures, but I think the amendments to allow the states more control over their internal operations might have a great deal of bipartisan support in many states.

By its very nature, Congress is not going to discipline itself. If there is going to be any discipline, it will have to come from the states taking back control from Washington DC.

Right now, many of you are looking at the federal government and wondering, Wheres the crisis? Why the urgency? When the markets are in turmoil in a few years, when unemployment is high and rising, when Boomers who have retired can make almost nothing on their savings or investments, there is going to be a crisis and a demand for real change. I hope we dont waste that crisis.

The Convention of States Action organization needs your help. If you would like to get involved, they can put you in touch with the people who are already active in your state. As with any project this big, they need money; and in a year when we are going to spend billions on the political process, a few extra million invested here could actually make a difference. And when you meet or contact your state legislators, give them a heads-up on the Convention of States and tell them its something we need to do. Get them thinking about it now, as they will likely be voting on it if not this year then next year.

This convention wont be convened in time to help us avoid the next recession, but it can help change the economic reality of the recovery, and maybe that is the best we can realistically hope for. But the best we can more optimistically hope for is that Congress and the new president will see that the Convention of States process is beginning to snowball and decide together to go ahead and do the right thing.

Dallas, Houston, Abu Dhabi, Raleigh, SIC, and Lemonade Day

I will be speaking in Dallas on April 28 for the 14th annual Commerce Street Bank Conference. Then the next week I will again speak in Dallas for the seventh annual Inside Retirement conference, May 5-6. They have a great lineup of speakers, but I am most excited about getting to hear and maybe even speak to my personal writing hero, Peggy Noonan. I will admit that Im a total fan boy of anything she writes. Then the following week I fly down to Houston to speak at the S&P Dow Jones Art of Indexing conference on May 10. The conference is for financial advisors and brokers who are trying to understand how to manage risk while maximizing returns in the current environment.

I will be in Abu Dhabi the third week of May and then come home and almost immediately go to Raleigh, North Carolina, to speak at the Investment Institutes Spring 2016 Event. Im looking forward to hearing John Burbank and Mark Yusko (who will also be at my own conference the same week) and then being on a panel with them. Afterward, I make a mad dash for the airport, arrive back in the Dallas late Monday night, and start to prepare for the Strategic Investment Conference, where upwards of 700 of my closest friends will gather to discuss all things macroeconomic and geopolitical. It is really going to be a great week.

On a fun but also quite serious note, as many longtime readers are aware, Ive spent a bunch of time researching and thinking about the jobs of the future. One conclusion I've reached is that in our globalized, UBER-controlled, task-oriented marketplace, raising kids to understand entrepreneurship and financial literacy is of crucial importance. A really good friend of mine in Dallas (and a reformed hedge fund manager), Reid Walker, agrees with me and is co-founder of Lemonade Day Greater Dallas.

Lemonade Day is all about teaching kids these important lessons by encouraging them, with the support of caring adults, to open their very own businesses: lemonade stands. The kids who get involved are paired with mentors who help them to put together a business plan, get a loan from a local business or bank based on that plan, and then actually sell the lemonade and pay back the loan, keeping the profits. Here in Dallas last year I found all sorts of businessmen, investors, and other financial types working with the kids, who present their business plans at the Dallas Federal Reserve.

Lemonade Day, which was founded in Houston nine years ago, has spread to more than 58 cities across the US and is expanding around the world, with over 220,000 kids participating last year. Its not too late for you to register your child and join the movement on Saturday, May 7th. And if you go to the website and dont see your city involved, then maybe you should pick up the baton and see about starting to train the next generation of entrepreneurs. The photo below is from a recent Lemonade Day, with your humble analyst, Reid Walker, and Danielle DiMartino Booth surrounded by some of the kids who participated in Dallas.

It really is about building the future.

It is time to hit the send button. Recently, I havent been finishing the letter until later in the weekend, but this Friday afternoon I actually polished it off and sent it to the editing team. If I hurry I can make a movie or at least a fun dinner. So let me tell you to have a great week and move on down the road! And in the mood for a little nostalgia may want to watch a very young Kenny Rogers and the First Edition. This was from his TV show Rollin on the River in the early 70s. Hard to believe he is now 77. Where have the years gone?

Your hoping we can turn things around analyst,

John Mauldin

subscribers@MauldinEconomics.com

| Digg This Article

-- Published: Monday, 18 April 2016 | E-Mail | Print | Source: GoldSeek.com