-- Published: Friday, 1 July 2016 | Print | Disqus

Last Thursday, as I was coaching my sons little league team on their improbable quest to Williamsport

I glanced at the headlines rapidly breaking in Britain: the vote was swelling towards the Brexit. My first thought was to discount the panic tone of the initial reports, as it was still early in the tally with much of the vote outstanding. In retrospect, my instinct to qualify the hyperbole spoke to a larger fallacy at play. In truth, the writing had been on the walls for some time.

As investors, weve all been influenced by the range of emotions that can lead you to and from the trough, with greatly varying results. With experience, you typically become more pragmatic when it comes to sizing up the markets, as seeking returns influenced from more idealistic persuasions is often a costly trip down an uncharted rabid hole. Although there have been a few sizable global brush fires since the financial crisis peaked in 2009, central banks have largely succeeded at mitigating widespread collateral damages in the markets, primarily by enacting aggressive monetary policy where private industry and public markets had been heavily impacted. And while a dystopian haze has remained hanging on the horizon over the past seven years, by and large, central banks have overrode the worst-case forecasts by intervening in concerted and extraordinary ways.

The crux, however, is aggressive monetary policy has not addressed and arguably even worsened the publics perception of the widening chasm between the halves and the have nots. From this perspective, the free lunch went squarely to the wealthiest at the expense of the taxpayers. Here in the US, it was the Fed and Treasurys Hobsons choice a pragmatic prescription aimed primarily to save the system during the throes of the crisis.

One of the few silver linings of the Great Depression was the enormous gap in income inequality leading up to the peak in 29, was narrowed by the massive public works programs that infused earnings to what eventually became a broad and sturdy middle class. Moreover, those wealthy had their influence hobbled through lightened pocketbooks, because markets did not rebound nearly as spritely as they did this time around. That said, in Bernankes calculus and as he articulated years before the crisis, central banks helped cause the Great Depression by not acting swiftly and magnanimously in easing monetary policy in the wake of the crash. From his perspective, you bail out the banks and you bail out everyone by saving the system. Without functioning markets, the health of the middle class is greatly endangered, and before long you have the same global economic instabilities that contributed to the social upheaval that made nations turn inward, brought fascism to power in Europe and war to shores worldwide.

The rub today is that while the system was saved during the crisis and markets rebounded strongly, wealth and income inequality has greatly expanded mostly at the expense of public trust. No public trust no political capital to govern and enact responsible fiscal policy. No real fiscal policy and the health of the economy and public markets are left primarily to the broad and imperfect influence of the central bank. In this environment, where theres widespread perception that the government has mostly failed its citizens and only served the wealthiest and most powerful parts of society, the natural tendency for the nation is to collectively turn inwards and towards those political ideologues pointing out the obvious flaws in the system, with at times incendiary solutions.

- Enter the likes of Donald Trump, Bernie Sanders, Nigel Farage, Boris Johnson, Marine Le Pen, Pedro Sanchez, Pablo Iglesias, Frauke Petry ... etc.

Although they certainly dont fall on the same side of the political continuum or share similar ambitions, what they all collectively tap into is the tangible rage in the middle class that has felt abandoned by their respective governments in the wake of the financial crisis. What happened last Thursday was the ideologues triumphed over the pragmatists. And while the counterfactual arguments of how the financial crisis was handled will go on in perpetuity just as they have for generations since the Great Depression, the reality is last Thursdays results will not be the last victory for the ideologues and is testament of the dangers that inevitably will impact markets with unknown consequences. Considering that Britain was a relative outlier to the broader economic travails within Europe, it also suggests that even if the vote had failed or comes to pass without them leaving the EU, participants (myself included) have underestimated the underlying political frictions that have been butting up against the limitations of central banks worldwide.

________________

Postscripts

From an intermediate-term perspective, the market reaction from the British referendum may provide a discerning catalyst for commodities and those markets tangentially correlated. As nominal yields likely remain suppressed at or near historic lows and the post-Brexit market environment gives greater cover from future rate hikes, real rates that began moving lower subsequent to the Feds initial rate hike in December should continue to trend down.

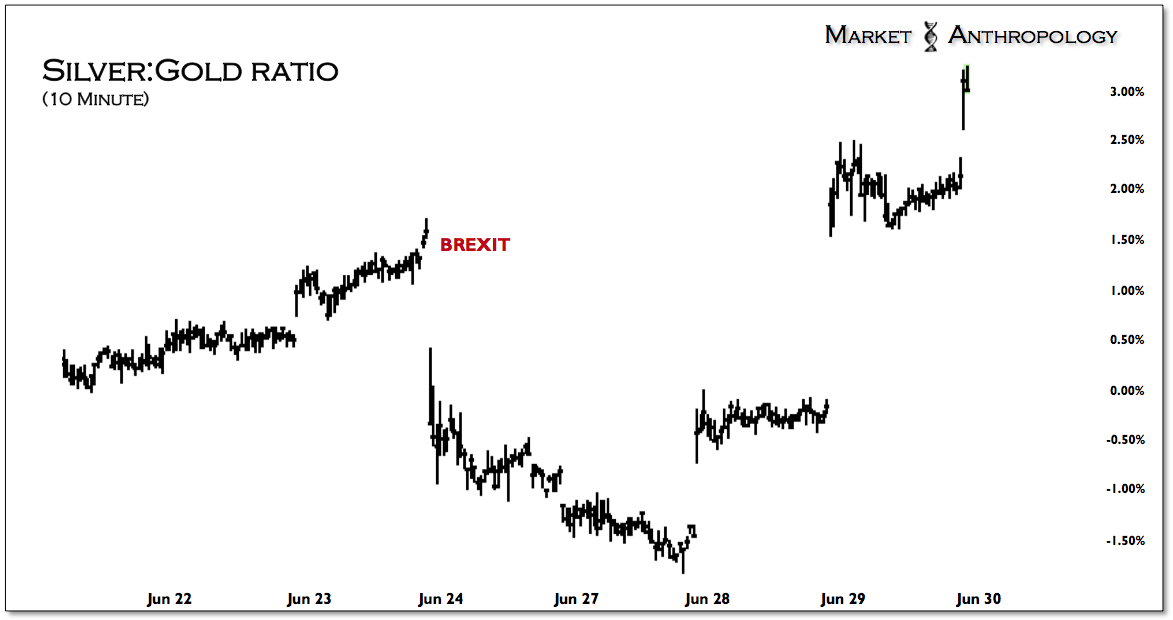

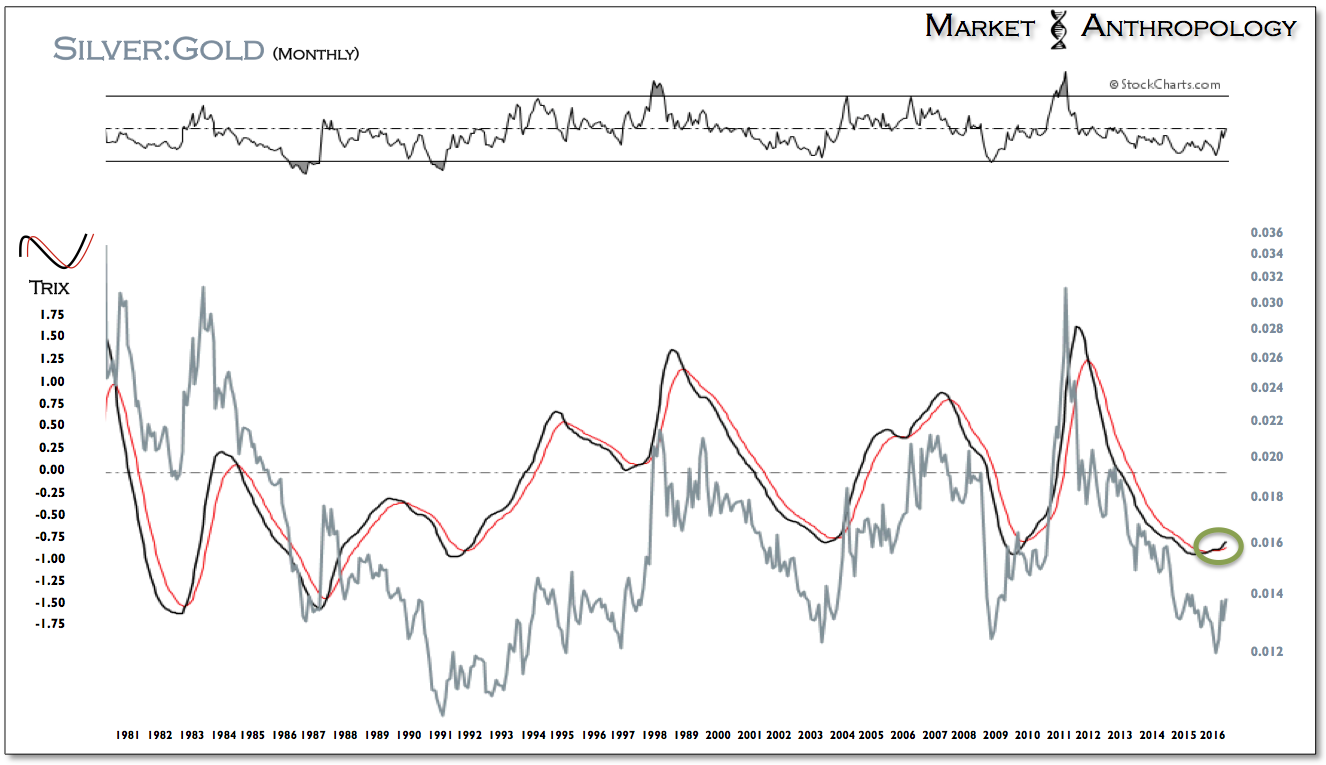

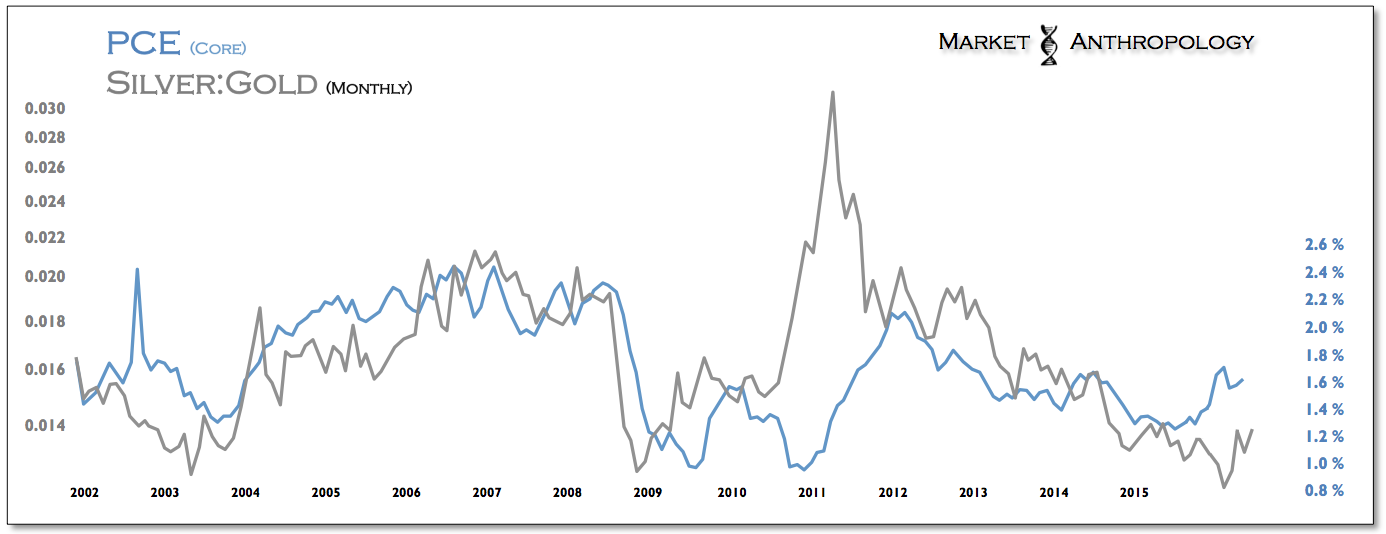

Despite some renewed deflationary concerns from the Brexit punditry, the silver:gold ratio that we follow as another reflationary barometer, has recouped the initial retracement decline from the Brexit vote and continues to trend higher. As we pointed out towards the end of last year, the rare positive momentum signal in the ratio bodes bullish towards the long-term prospects of precious metals and commodities, as well as those assets that benefit from rising inflation.

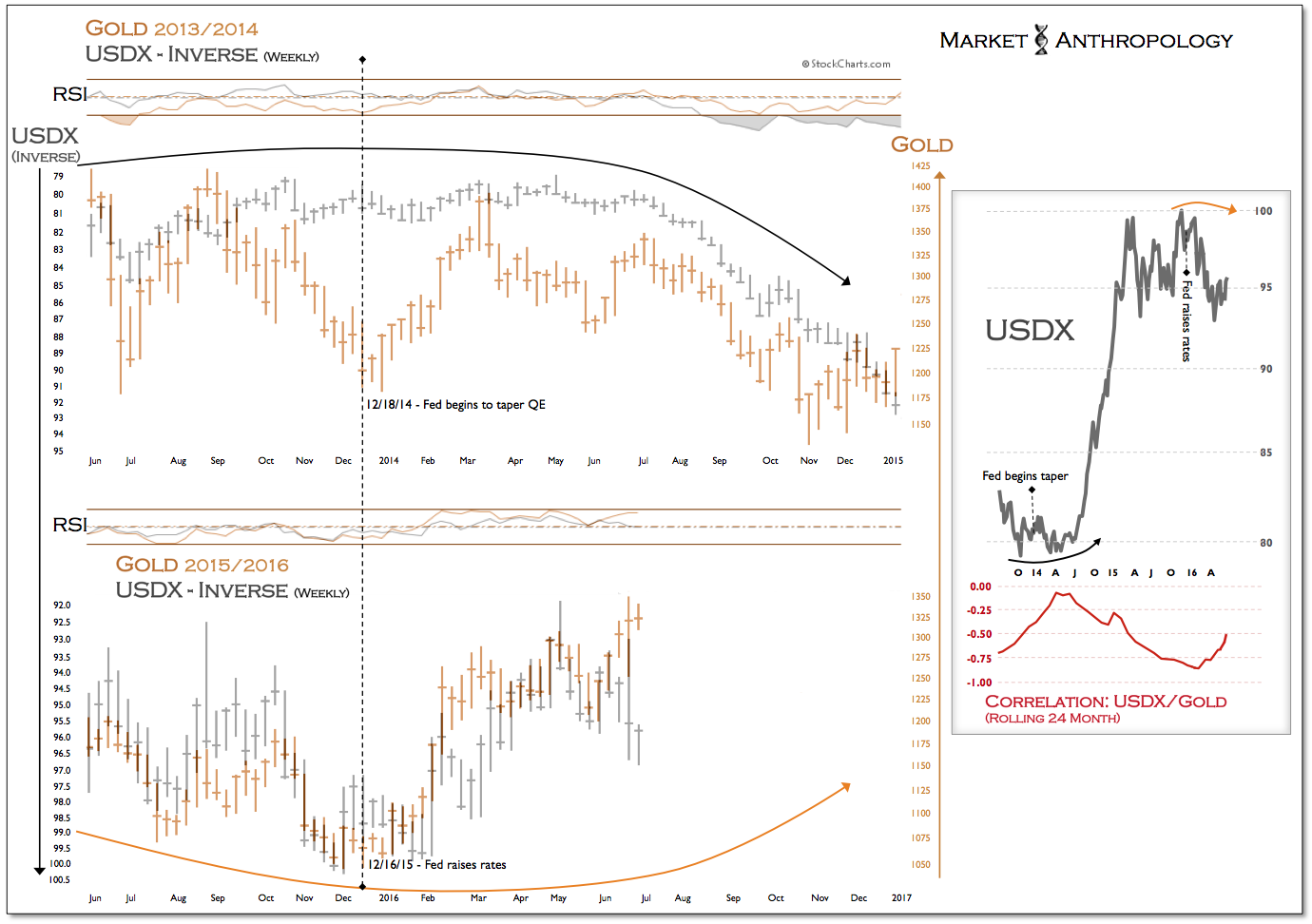

While the referendum did generate immediate disinflationary pressures that supported the dollar, we believe those forces will be greatly curtailed by the weakening appetite for further rate hikes by the Fed this year and the loosening of credit conditions that supports the positive domestic trend in inflation. All things considered, we expect the reflationary trend that began in gold last December and broadened throughout the commodity sector this year to continue.

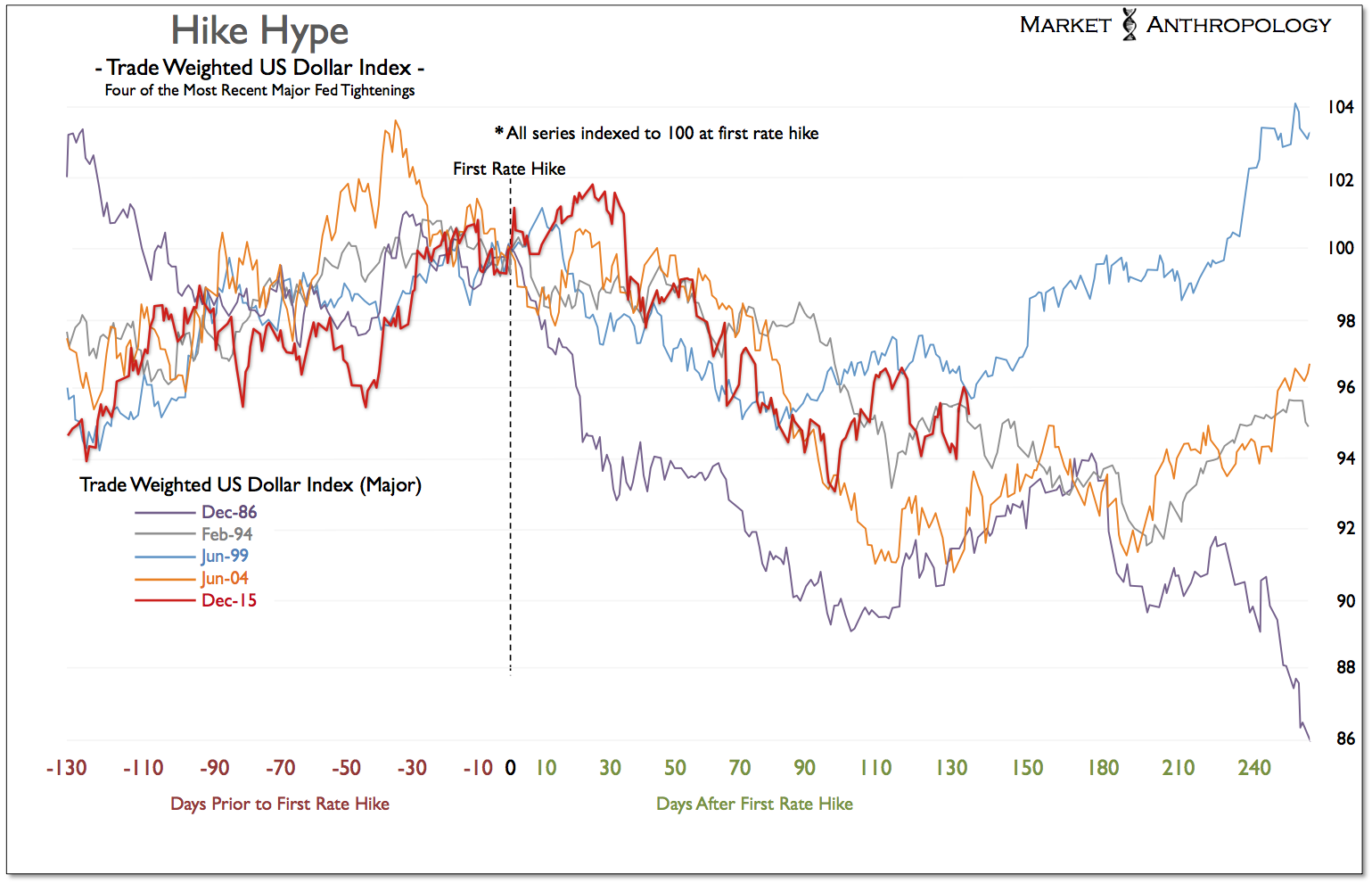

Should the dollar resurrect its dormant uptrend from last year, all bets are off with commodities; which might also suggest a more severe market dislocation is a foot. For now, we continue to closely watch the dollar and its relative performance to gold, for indications that our buy-the-rumor (taper) and sell-the-news (rate hike) suspicions towards the dollar is misplaced or adversely impacted by the recent events in Britain.

Whats interesting to note, is in the chart that we constructed at the beginning of the year to frame our bullish gold/bearish dollar thesis, gold is now seasonally trading around the same level from 2014, despite the dollar (USDX) strengthening by nearly 20 percent. This isnt that surprising to us, however, since major lows in gold have typically led pivots in the dollar, which we have speculated is on the back side of completing a cyclical high last year. While over the near-term it wouldnt surprise us to see the shine come off precious metals and on to other commodities like oil (i.e. similar to March), underlying market conditions continue to support the trend higher.

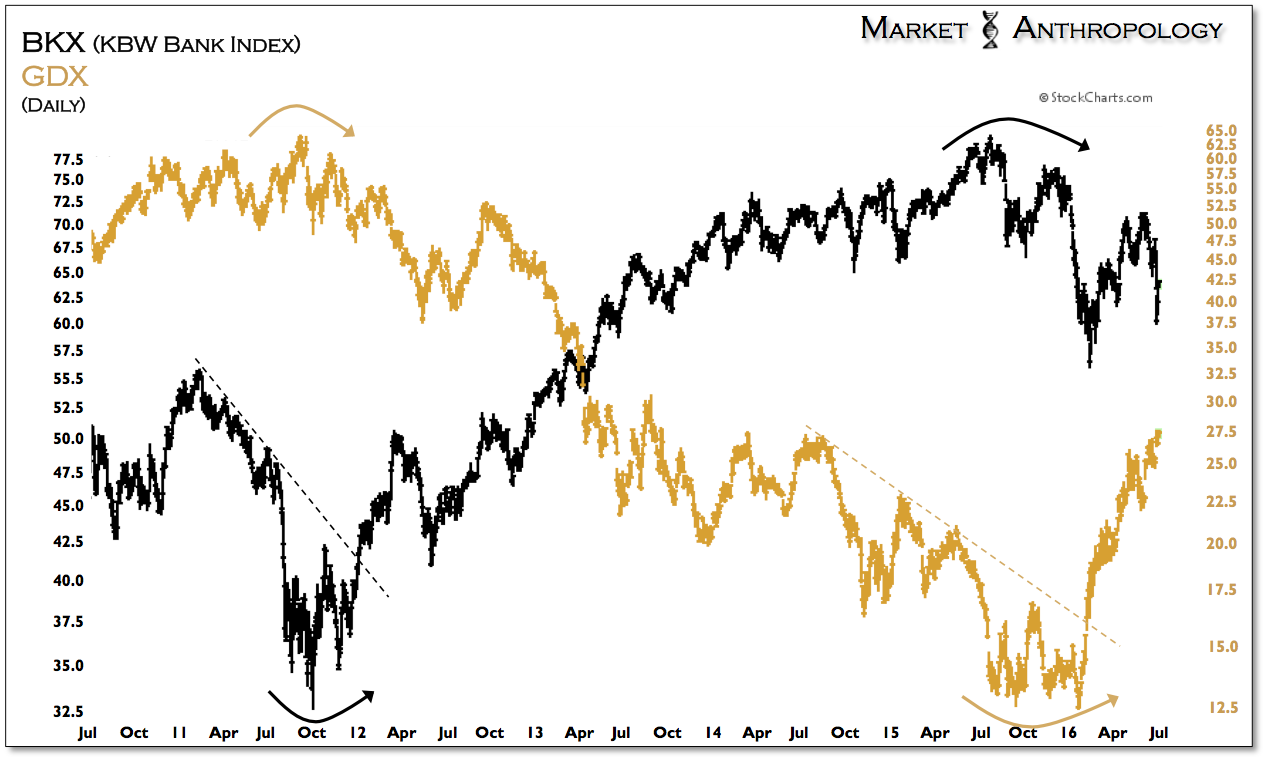

Sizing up the move in gold relative to the US equity markets, you continue to see that gold has not only led the broader reflationary trend, but pivots in the equity markets as well. Weve speculated, however, that a principal distinction in longer-term market structure is as commodities have put in a cyclical low with inflation, US equities are distributing across a now broad cyclical top.

That said, this weeks strong rally in equities continues to follow the leading footprints in gold, which may suggest that the SPX would again test the top of its broad two-year range.

| Digg This Article

-- Published: Friday, 1 July 2016 | E-Mail | Print | Source: GoldSeek.com