-- Published: Friday, 22 July 2016 | Print | Disqus

By Market Anthropology

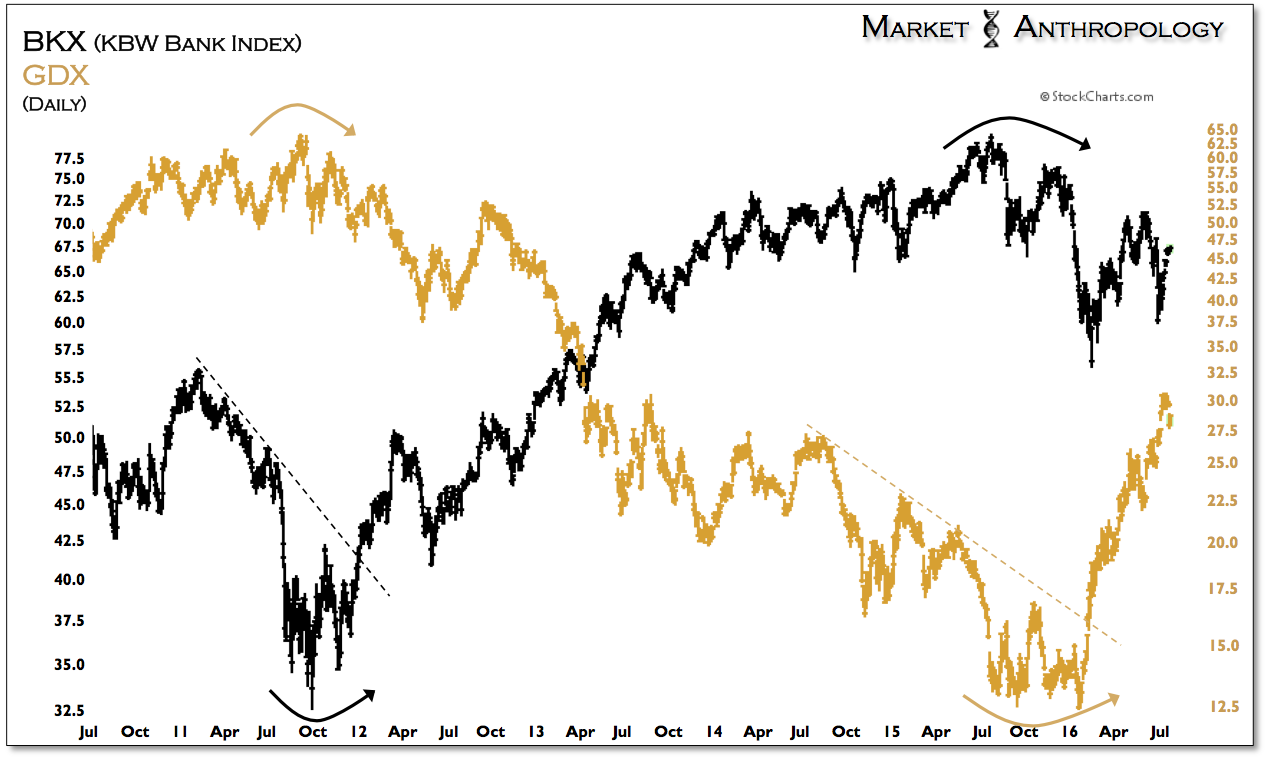

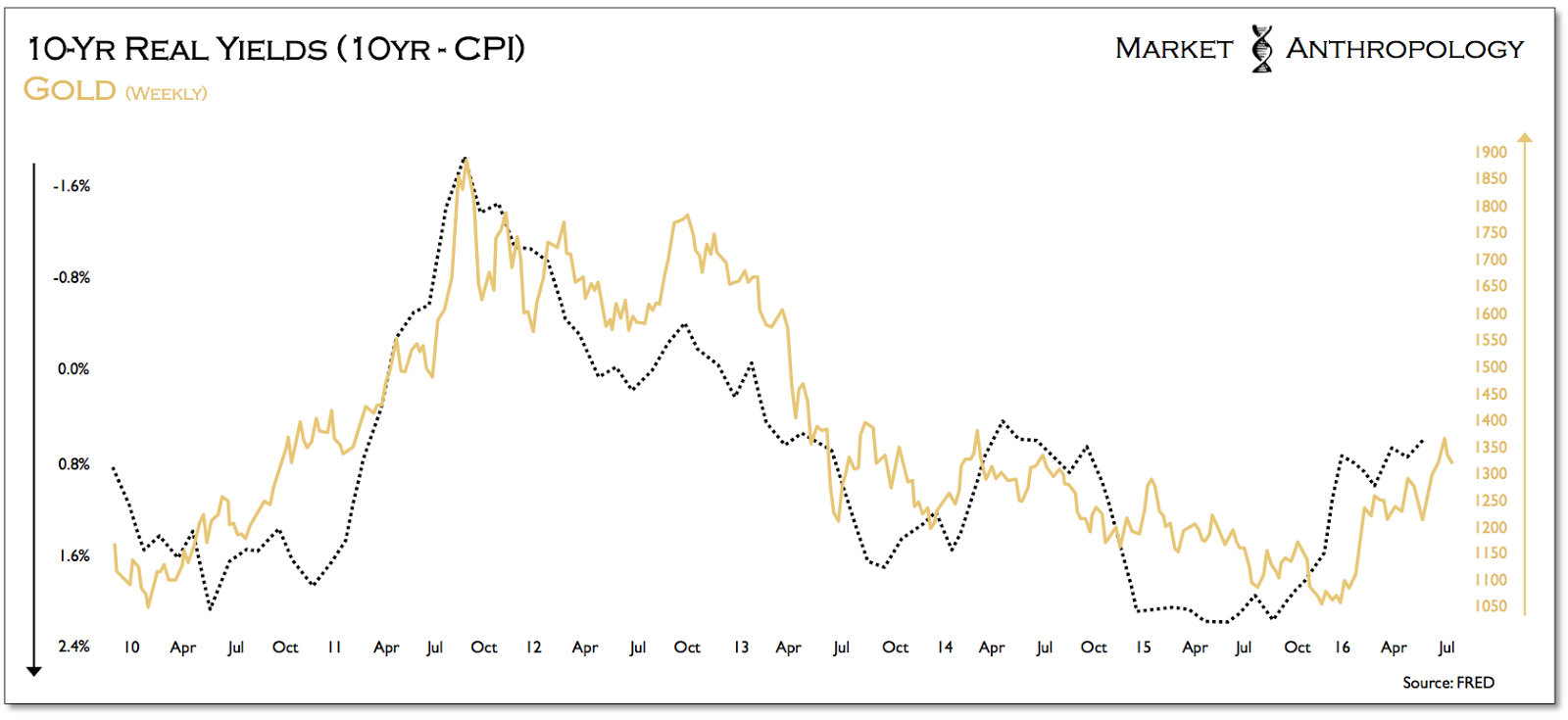

Throughout the year Ive referenced the chart below, which now reflects a large performance differential between the banks and the gold miners, as yields both nominal and real - have fallen. Although the banks have had a difficult time performing in this environment, gold mining stocks have done exceptionally well, as gold has benefited robustly from both safe-haven demand and from the retracement in real yields, which has made it attractive again from a real return perspective.

Not surprisingly, banks have strongly underperformed even the equity market indexes, as exceptionally low yields reflect the contentious business environment for the banks, and more importantly their customers. Bank profits are inherently hurt in the current market environment through the compression in net interest margins and more broadly through weaker demand for banking services and products as demonstrated by investors willingness to accept certain exceptionally low and even negative returns, rather than the prospect of potentially much larger and uncertain losses. The later also reflects greater deflationary expectations by investors, as exceptionally low and negative bond yields can still produce positive real returns if, inflation remains below said bond yields.

Essentially, even though the S&P 500 made an all-time high yesterday, the performance in the banking sector and the bond market do not reflect long-term confidence or investment in growth even as the economic data in the US remains firm, inflation appears to be on an uptrend and the prospects for a recession are low. Moreover, these dynamics have created a feedback loop in the fixed income market that could/has sustained market inertias longer than even we had suspected. And while we were open to the possibility going into this summer that the Treasury market could break down, that window appears to have closed with the Brexit vote moderating policy expectations that once again have buttressed bonds. That said, from our point of view, theres still a much greater probability that real yields will fall further over the next year, as inflation continues to rise which ultimately is a loosing proposition for those fixed income investors seeking a positive real return from these more safe-haven positions.

One of our long-standing suspicions has been that the 2011 cycle lows for real yields would eventually be broken on the next leg down. This belief has largely maintained our interest in the precious metals sector that exhibits a strong inverse correlation to real yields. From our perspective, the probability that inflation would eventually outstrip the reach of nominal yields was more likely, than a continuation of the atypical market dynamics engendered by the Fed during the taper-tantrum, where real yields spiked on greatly overblown fears of higher rates but inflation wilted on the vine. In a more typical and organic market environment where monetary policy was not enacted at ZIRP or after extended periods of large-scale quantitative easings, real rates begin to rise when benchmarks and expectations of improving growth is followed by tighter policy and a decline in inflation expectations. At secular cycle lows, real rates surge as the inflation cycle crests and retreats and after nominal yields remain supported.

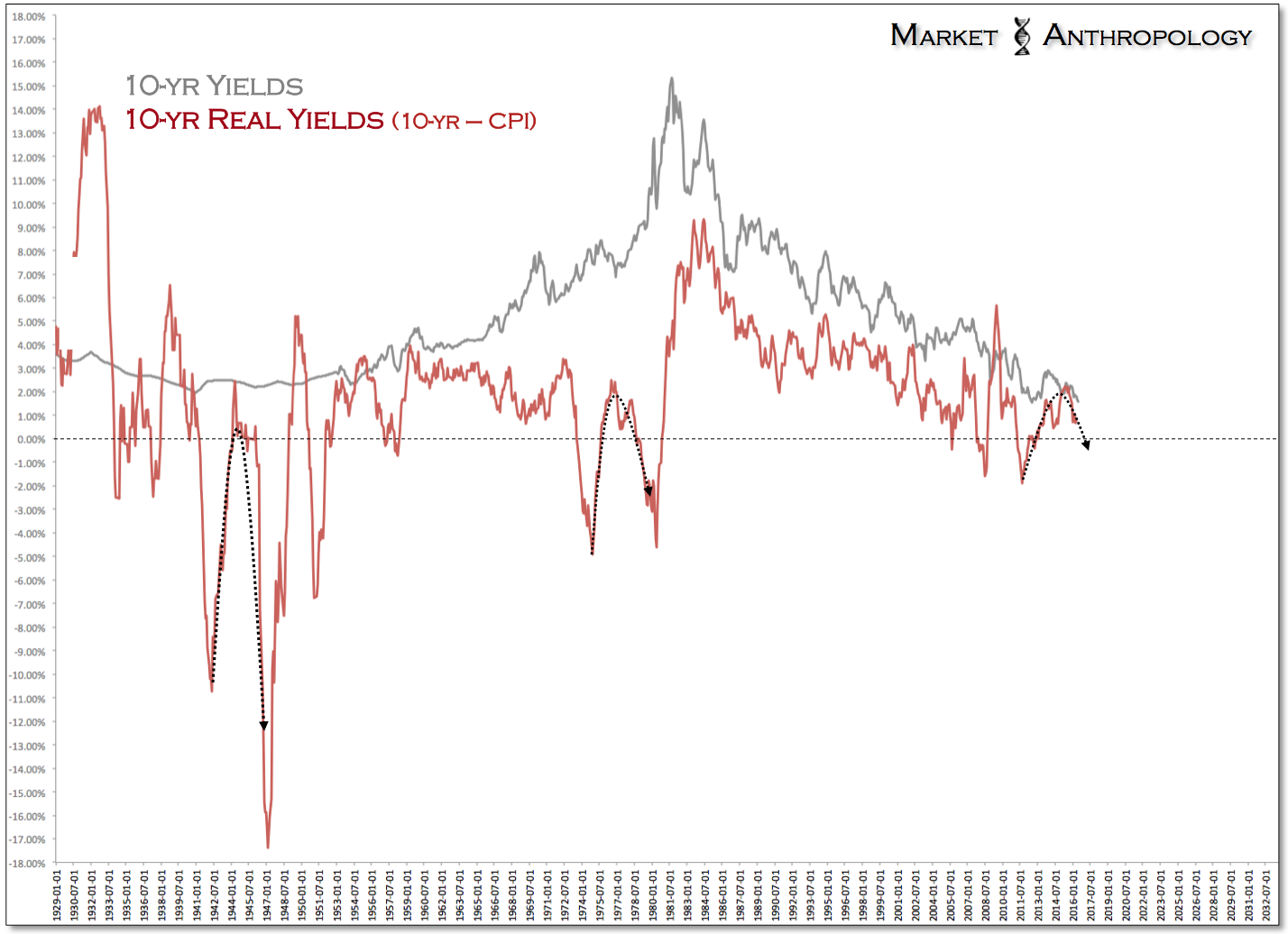

Our outlook for new lows in real yields has also been guided by our historic studies of the long-term yield cycle (see Here), that shares similarities with the last time yields fell and formed the protracted trough of the cycle through the 1940s. As frequently mentioned in previous notes, this time period also shares a certain likeness with the last time the Fed and Treasury extended extraordinary support to the markets between 1942 and 1946, with large-scale asset purchases aimed to prop up the financial system, as markets and participants recovered from the long tail of the Great Depression and the colossal price tag of World War II.

Ultimately, there were latent effects from the historic accommodations extended, as participants and regulators struggled with normalizing policy, as strong pulses of inflation worked through the system, while investors remained concerned that another deflationary tide of the Great Depression was about to unfold. As such, investors didn't flee the bond market as if inflation would maintain its trajectory higher, but took shelter in the perceived safe-haven of the Treasury market, likely because of what they had lived through over the past two decades.

Despite the extent to which the public and government officials were exercised about inflation, the public acted from 1946 to 1948 as if it expected deflation. - Milton Friedman and Anna Schwartz, A Monetary History of the United States, 1963

Sound familiar?

In essence, policy makers might have succeeded at supporting the markets through considerable attenuating circumstances in the economy, but broader market psychologies were still entrenched and impaired from what participants had been through in the Great Depression. The net effect was a collapse in real yields that eventually made a cycle low in 1947; a year after nominal long-term yields retested the lows from 1941 and began to stabilize through 1946. Although the upswing in inflation did not upset the Treasury market as policy makers refrained from tightening, equities went nowhere between 1946 and 1950, until investor confidence returned and monetary conditions broadly normalized and reset with the Fed and Treasury Accord in 1951.

Overall, we remain steadfast bulls on precious metals and expect the performance gap over equities to continue to widen, as real rates target the 2011 lows next year. Over the short-term, it wouldnt surprise us to see the global rally in equities resume into August. However, the performance in the financials over the past year does not support those expectations of a material breakout that ultimately requires the banks leadership as testament of greater investment confidence in the economy. Similar to the last time yields scraped the trough of the long-term cycle in the mid 1940s, market participants do not appear ready to invest in the next secular growth cycle even if the economy could structurally support it. Unfortunately, you cant have one without the other, or as the great philosopher Yogi famously framed its ninety percent mental and the other half is physical. Well get there eventually, just not quite yet.

The content on this site is protected

by U.S. and international copyright laws and is the property of GoldSeek.com

and/or the providers of the content under license. By "content" we mean any

information, mode of expression, or other materials and services found on GoldSeek.com.

This includes editorials, news, our writings, graphics, and any and all other

features found on the site. Please contact

us for any further information.

Live GoldSeek Visitor Map | Disclaimer

The views contained here may not represent the views of GoldSeek.com, Gold Seek LLC, its affiliates or advertisers. GoldSeek.com, Gold Seek LLC makes no representation, warranty or guarantee as to the accuracy

or completeness of the information (including news, editorials, prices, statistics,

analyses and the like) provided through its service. Any copying, reproduction

and/or redistribution of any of the documents, data, content or materials contained

on or within this website, without the express written consent of GoldSeek.com, Gold Seek LLC,

is strictly prohibited. In no event shall GoldSeek.com, Gold Seek LLC or its affiliates be

liable to any person for any decision made or action taken in reliance upon

the information provided herein.