-- Published: Tuesday, 2 August 2016 | Print | Disqus

By Frank Holmes

Fixed-income isnt what it used to be. As the Wall Street Journal reports, the total amount of global government bonds that bear negative yieldsmeaning it costs you to have the government hold your moneyhas now climbed to a massive $13 trillion.

This figure is likely to grow as yields continue to plumb the depths of negative territory, giving global investors little choice but to seek income elsewhere.

For some, its corporate debt. But even these securities have fallen significantly since the start of the year, many below zero. Bloomberg reports that roughly $512 billion worth of European, investment-grade corporate bonds now offer a negative yield.

Its not much better in the U.S. Blue chip Walt Disney just issued a 10-year bond with the low, low yield of 1.85 percent.

For other investors, its American municipal bonds, which still offer attractive, tax-free income, not to mention low volatility and low default rates. Back in May, I shared with you how yield-starved foreign investors were piling into munis at an impressive clip, even though theyre ineligible to take advantage of the tax benefit. But no matterat least its not costing them to participate, unlike a growing percentage of negative-yielding government debt.

Negative bond yields have also boosted demand for gold, which has had two of the most spectacular quarters in modern history. Although it doesnt provide any income, the yellow metal has been treasured as an exceptional store of value, especially in times of political and macroeconomic uncertainty. Gold stocks are up more than 115 percent year-to-date, as measured by the NYSE Arca Gold Miners Index and Swiss financial services firm UBS puts gold prices near $1,400 by years end.

(Gold prices are also being supported right now by the likelihood that weve reached peak gold. According to my friend Pierre Lassonde, cofounder of Franco-Nevada, new discoveries have fallen steadily since the 1980s, while current mine production has not kept up with demand.)

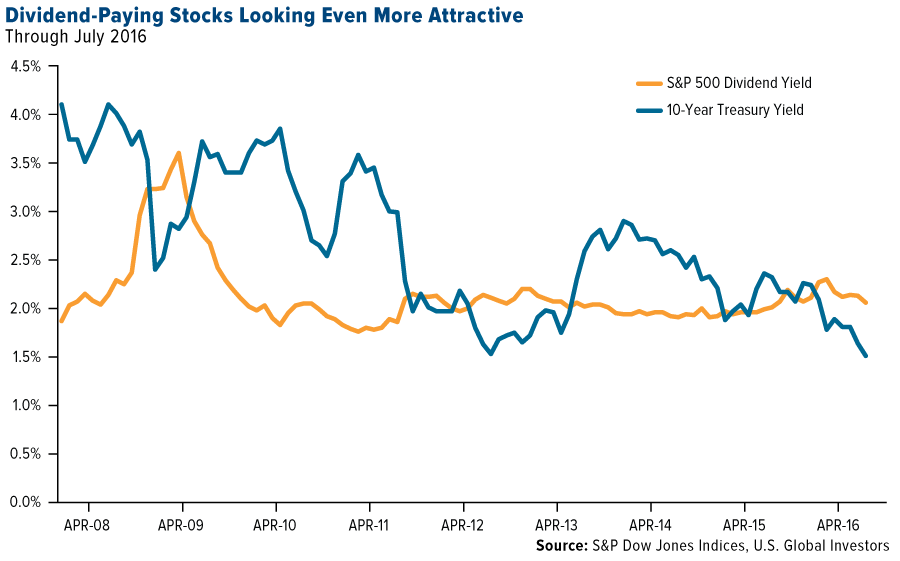

Are Stocks the New Bonds?

The hunt for yield has also inevitably landed many income investors in dividend-paying stocks. According to Reuters, about 60 percent of S&P 500 Index stocks now offer dividend yields that exceed the 10-year Treasury yield, which hit an all-time low of 1.36 percent earlier this month.

This is one of the main reasons why recent cash flows into U.S.-based stock funds have been so strong. Money goes where its most respected. In the week ended July 13, ETF and mutual fund equity funds took in a whopping $33.5 billion in net new money, the largest positive weekly net inflow of the year.

Meanwhile, Treasury bond funds have been witness to some huge outflows this year. For the week ended July 25, the iShares 7-10 Year Treasury Bond ETF lost $90.5 million. Back in April, foreign investors unloaded nearly $75 billion in U.S. Treasuries, the single largest monthly amount since transactional recordkeeping began in 1978.

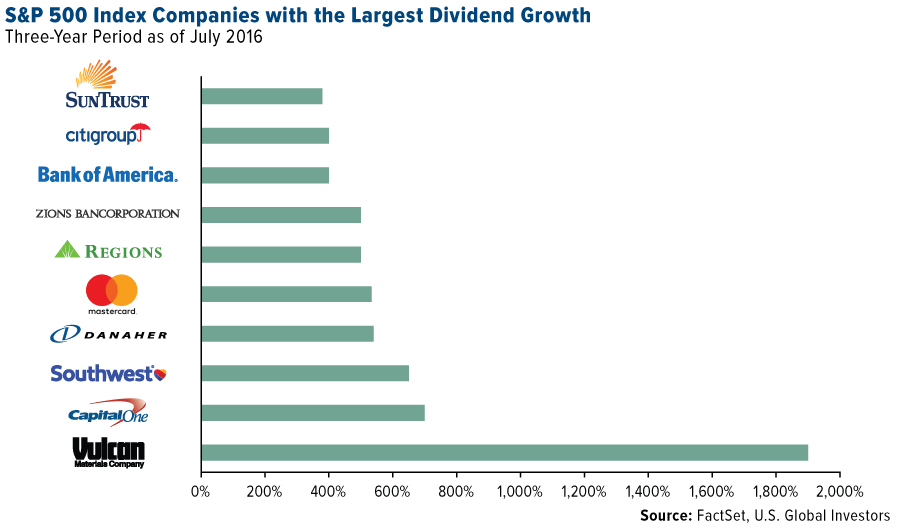

Increasing Dividends over the Past Three Years

In selecting the best dividend-paying stocks, we like to identify those that have grown their payments the most over the past three years. Using that metric, the leader by far right now is Alabama-based Vulcan Materials, which has increased its dividend a jaw-dropping 1,900 percent, according to FactSet data. Many financial groups, including Regions Financial and Zions Bancorporation, have also been very generous in rewarding shareholders.

The challenge going forward has to do with corporate earnings. Dividend growth is largely driven by earnings, which are expected to be down 3.7 percent in the second quarter once all companies have reported. This will mark the sixth consecutive quarter of declines.

Energy stocks lead the way down, with crude oil prices at nearly three-month lows after falling over 20 percent since early June.

Apple is perhaps the largest contributor to declines this quarter. The iPhone-maker posted net income of $7.8 billion, a massive 27 percent drop from the $10.7 billion it recorded during the same period last year.

But lets give the tech giant a breakit just sold its one billionth iPhone last week, despite a decrease in sales for the second straight quarter. I must also add here that Apple is the undisputed dividend king, having paid out $2.9 billion in the first quarter alone.

Standouts this earnings season included Facebook, Amazon and Alphabet (Google)three quarters of the FANG tech stocksall of which crushed expectations. Mark Zuckerbergs social media giant handily beat analysts estimates on the top and bottom lines as well as ad revenue, which totaled $6.2 billion during the quarter. This helped add $5 billion to Facebooks market capitalization, pushing it ahead of Warren Buffetts Berkshire Hathaway.

Buffett was also surpassed last week by Amazon CEO Jeff Bezos, whose wealth leaped $2.6 billion after an extraordinary earnings report. Hes now the worlds third-richest man, ahead of the Oracle of Omaha.

Netflix, on the other hand, reported a disappointing 59 percent loss in profits, from $40.5 million in the first quarter to $16.7 million. The popular streaming service added only 1.7 million subscribers during the quarter, far below its guidance of 2.5 million.

Banks on the Chopping Block?

Well, theres no questioning it now: Donald Trump and Hillary Clinton have both been anointed as our presidential candidates. Many wondered if Bernie Sanders would try to disrupt the nomination process and insist on a brokered convention, similar to what Franklin Roosevelt did in 1932. Sanders supporters certainly put up a fight, but in the end, Clinton prevailed.

This week before last, I suggested that the only thing Trump and Clinton have in common with each other is theyre both in favor of increasing infrastructure spending. Its now come to my attention that no matter who wins, there could be an effort to break up the big banks, as both parties platforms include an interest in reviving the Glass-Steagall Act of 1933. The goal, of course, would be to prevent another financial crisis, but whether the banking act would actually work is up for debate.

Another solution might be to break up the regulatory bodies into two separate branchesone overseeing banks, the other overseeing all other financial and investment institutions, from brokers to insurance companies to mutual fund companies. Each side would have its own unique set of rules and regulations. Whats good for banks isnt necessarily good for investment firms, and vice versa, because theyre often playing very different games.

Think of it this way: We expect referees to be experts in their particular sport. That only makes sense. But imagine if all competitive sports, from basketball to hockey to softball, suddenly drew from the same pool of referees. Games would be conducted a lot less efficiently. Officials would constantly be putting on and taking off different hats. One games set of rules might mistakenly (and awkwardly) be applied to a completely different game.

This is whats happening in the financials industry as a whole.

As I always say, regulations are often well-intentioned. Theres a reason why they exist. We need them to maintain a level and fair playing field.

At the same time, its important that they be commonsense and not hinder or prohibit everyday, lawful business activity.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time. Past performance does not guarantee future results.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The index benchmark value was 500.0 at the close of trading on December 20, 2002. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of 6/30/2016: Franco-Nevada Corp., FactSet Research Systems Inc., MasterCard Inc., Southwest Airlines Co.

The content on this site is protected

by U.S. and international copyright laws and is the property of GoldSeek.com

and/or the providers of the content under license. By "content" we mean any

information, mode of expression, or other materials and services found on GoldSeek.com.

This includes editorials, news, our writings, graphics, and any and all other

features found on the site. Please contact

us for any further information.

Live GoldSeek Visitor Map | Disclaimer

The views contained here may not represent the views of GoldSeek.com, Gold Seek LLC, its affiliates or advertisers. GoldSeek.com, Gold Seek LLC makes no representation, warranty or guarantee as to the accuracy

or completeness of the information (including news, editorials, prices, statistics,

analyses and the like) provided through its service. Any copying, reproduction

and/or redistribution of any of the documents, data, content or materials contained

on or within this website, without the express written consent of GoldSeek.com, Gold Seek LLC,

is strictly prohibited. In no event shall GoldSeek.com, Gold Seek LLC or its affiliates be

liable to any person for any decision made or action taken in reliance upon

the information provided herein.