-- Published: Monday, 15 August 2016 | Print | Disqus

By John Mauldin

Summer in Bretton Woods

IMF Love Affairs

PIIGS in Bankruptcy

We Need an Event

European Bias

An Inheritance of Incompetence

Denver, Dallas, and Writing

Always remember that the future comes one day at a time.

Dean Acheson

Practical men who believe themselves to be quite exempt from any intellectual influence, are usually the slaves of some defunct economist.

John Maynard Keynes

I dont often agree with Keynes, but he is the most quotable of all major economists. The above sentence was one of his best. He was right about defunct economists. Of course, he was talking about all those other defunct economists who no longer kept up with his new and improved way of thinking about all things economic. Now his quip comes back to haunt his legacy and his followers.

Theories and practices often outlive their usefulness in our fast-changing world. So do institutions, including those chartered at the 1944 Bretton Woods Conference. In todays letter we are going to look closely at the International Monetary Fund and a scathing report from its own internal auditors. For those of us who have been following the IMF for decades, the report is not all that surprising.

My real purpose here is not to point the finger at the IMF but to point out where its problems are part and parcel of a greater problem in global institutions. During the next global recession we are going to see a continuation of the same approaches to crisis solving that weve seen in the past, based on the theories of defunct economists mixed with personal and institutional biases. Their prescription is a witches brew that we will be told is good for us but that will in fact ensure that those of us least able to cope will bear the brunt of its impact.

Lets be generous to the World War II generation. In a war-torn world that had yet to recover from a depression that began 15 years earlier, revamping the existing economic order probably seemed a good idea. And the results did look positive for the first few decades. With US help, Europe and Japan launched huge rebuilding projects. Here in the States we enjoyed rapid growth and a Baby Boom that produced me and perhaps you.

Yet that era also bequeathed to us some new problems. What we now call the European Union grew out of a postwar Franco-German coal and steel trading pact. The euro currency is a branch in the same family tree as the World Bank, the International Monetary Fund, and others. Its a big, bushy tree desperately in need of trimming.

Today well look at a report that suggests the IMF is indeed long overdue for a good pruning. This sordid story is just one thread in a much bigger one, but it helps explain a lot of global imbalances. Lets go back to the very beginning.

Summer in Bretton Woods

The Second World War was still raging in July 1944, but the Allies thought victory was at hand. Representatives from 44 nations met at a Bretton Woods, New Hampshire, resort (pictured above) to design a new global monetary system. You might think this would be a long, involved task. Not so. They finished in three weeks. (Imagine trying to get a major trade agreement done in three weeks.)

Two things were already decided before the conference even started. They werent going to have a gold standard, nor would they allow free-floating exchange rates. John Maynard Keynes was a great influence at the conference, and his thoughts on gold relegated it to the past it was he who first called it a barbarous relic. The basic concept agreed to at the conference was a hybrid system of fixed rates tied to the US dollar, which in turn was tied to gold.

The Bretton Woods conferees determined that an ounce of gold would fetch $35. Other currencies were given fixed rates in dollars with a 1% leeway. This was how the dollar became the worlds reserve currency.

There was little choice in the matter because the US owned most of the worlds gold bullion. To have tied every country to a gold standard would have been massively deflationary and would have seriously hindered the potential for global trade and growth at a time when both were desperately needed.

Whatever you think about the appropriateness of what was done, fixing rates in this way made payment and debt crises all but inevitable. The delegates agreed at Bretton Woods to set up two transnational institutions to manage problems: The International Monetary Fund (IMF) and the International Bank for Reconstruction and Development (IBRD). The IBRD later became part of the World Bank.

The IMFs job was essentially to lubricate the system when trade flows made currencies drift away from their dollar pegs. It worked for a while, but the Bretton Woods regime collapsed in 1971 when President Nixon closed the gold window, severing the dollars convertibility to gold.

With currencies now effectively free-floating, the IMF found itself with little reason to exist. Did it go off quietly into the night? Of course not. When has any bureaucracy ever volunteered to shut itself down? IMF officials simply redefined their mission. The IMF would now provide financing to nations with balance of payments issues, makes loans to nations in distress, and publish lots of economic research.

In the course of fulfilling this noble mission, the IMF has managed to get itself involved with dictators, human rights abusers, corrupt officials, and assorted other global shady characters. Sometimes the corruption has touched top IMF officials. The current managing director, Christine Lagarde, is currently on trial in France on corruption charges dating back to her time as that countrys finance minister.

The IMFs structure almost guarantees that it will always be dysfunctional. Votes on the board are weighted by each countrys capital contribution, so a few big countries call the shots. In theory the smaller members could band together and usurp power with an 85% supermajority vote. Unfortunately for them, the US alone has 16% of the votes, giving Washington an effective veto on any serious change.

Theres also a huge divide between the creditor nations, who contribute capital and borrow little, and the debtors who contribute little and borrow much. Creditors want stronger lending standards and higher interest rates. Debtors want the opposite. But they are all represented on the board and are expected to somehow agree on IMF policies. They seldom do.

So what happens? The European members, well aware that the small fry can only squawk, make policy decisions that favor themselves. Every now and then a few sordid details leak out.

IMF Love Affairs

This UK Telegraph headline caught my eye a couple of weeks ago, alerting me to a new development in the ongoing saga of IMF incompetence.

That such a love affair existed was no surprise, nor that the IMF had participated in the immolation of Greece. No, the surprise was that IMF would publicly disclose the extent of incompetence and massive rule breaking that had taken place.

The Ambrose Evans-Pritchard byline told me this was a story worth reading. Heres his lead:

The International Monetary Funds top staff misled their own board, made a series of calamitous misjudgments in Greece, became euphoric cheerleaders for the euro project, ignored warning signs of impending crisis, and collectively failed to grasp an elemental concept of currency theory.

This is the lacerating verdict of the IMFs top watchdog on the funds tangled political role in the eurozone debt crisis, the most damaging episode in the history of the Bretton Woods institutions.

Ambrose knows how to turn a phrase. Calamitous misjudgments is a good way to describe the way the IMF, along with the EU and ECB, has handled the continents sovereign debt crisis, which remains unresolved even now, six years later.

What aroused Ambroses ire? A report from the IMFs internal audit department describes an organization for which dysfunctional would be a compliment. The massive bailouts of Greece, Portugal, and Ireland broke the agencys own rules and arguably enriched the perpetrators of those countries ills while further punishing the victims. And as we will discuss later in this letter, the IMF carried on with its disastrous policies while fully recognizing what it was doing, because there was huge internal debate about the bailout process. Clearly, many in the IMF knew that what they were doing was wrong and would result in crisis. An analysis of why the leadership decided to do inappropriate things tells us a lot about the way international institutions go about making decisions.

Among other lapses, IMF officials had no plans for handling a eurozone debt crisis, because they presumed such a crisis was impossible. And it wasnt that the IMF hadnt been warned. Long before the deluge, people within the agency had argued that the euro system was fundamentally flawed and would eventually fall apart. Those who said so found themselves overruled and even punished.

The bias developed because, as Ambrose says, the European elites in the IMF have waged a massive love affair with the euro. And like many in love, they simply could not see the flaws in the object of their affection, the common currency of the eurozone. It was at the very foundation of the whole European project in their eyes.

The IMF-EMU love affair led the agency to accept reports and reassurances from eurozone officials at face value, without the same kind of verification they routinely demand from less-developed countries.

I dont know for sure, but I suspect those less-developed nations, perceiving favoritism toward Europe, asked the IMF Independent Evaluation Office to start probing. The IEO bypasses the bureaucrats and reports directly to the executive board. Once unleashed, the IEO had no trouble finding all manner of bias, incompetence, and underhanded dealing.

These tendencies led the IMF to cooperate in imposing harsh austerity measures on Greece while protecting Greek creditors from haircuts. The IMF was far more concerned about protecting the sanctity of the euro system and the stability of European banks than it was about making the citizens of Greece suffer. We cant know for sure, but it seems likely an orderly debt write-down process would have put Greece back on its feet, with the pain spread equitably among the parties. The IMF instead pushed a plan that it knew would never work or at least many inside the IMF were saying so.

The sad fact is that if Greece had simply walked away from its debt, left the euro, and reintroduced the drachma, it would have gone through a very severe depression but now be on its way to recovery. Instead, Greece is trapped in a five-, going on six-year-long depression that is worse than the Great Depression of the 30s in the US. Further, there appears to be no way out of their crisis if they continue to adhere to IMF-imposed mandates in order to keep bailout money coming.

The irony is that at some point Greece may simply be forced to leave, which will create an even deeper depression, making a terrible situation even more desperate. I truly feel sorry for the Greeks.

The full IEO report with appendices is hundreds of pages long. You can explore it here if you enjoy such things.

But this report isnt all. It is only the latest chapter in a long, sordid tale. To understand it in context, we need to back up a few years.

PIIGS in Bankruptcy

We think of Greece as the epicenter of the eurozone debt crisis, but it had company. The acronym PIIGS refers to five overstretched members: Portugal, Italy, Ireland, Greece, and Spain.

In late 2009, as the Feds initial QE program pushed US stocks higher, Greeces growing budget deficit led credit agencies to downgrade its sovereign debt rating. The government cut spending but not by enough. Prime Minister George Papandreou formally asked for, and received, a bailout from a Troika consisting of the EU, ECB, and IMF.

As the crisis unfolded, it became clear to most everyone that Greeces heavy debt load would require harsh measures. The question then became how to distribute the pain.

A normal bankruptcy proceeding would have resulted in some kind of balanced plan. Creditors would take a haircut while the debtor gave up assets and/or income. In this case, the creditors were large European banks that were not at all predisposed to writing down their asset values. Through the EU and ECB, they pushed for Greece to cut spending and sell state-owned assets to raise cash. On the Greek side, a population accustomed to generous government benefits and widespread tax avoidance was not enthusiastic about austerity. Further, the Greeks had created a bureaucratic system that was unbelievably bloated and a labor program that reinforced noncompetitive businesses and stalled startup activity. The population wanted its benefits, and the oligarchs didnt want to reform. Europe didnt want a banking crisis but also didnt want to pony up enough money to really rescue Greece. A long standoff ensued.

IMF rules say the organization is not supposed to make a loan unless the borrower has a reasonable prospect of repaying it. It has routinely demanded harsh conditions in exchange for aiding smaller African, Asian, and Latin American countries. These conditions for getting the money all but guaranteed continued crisis in the countries that were subjected to them. Yet the IMF seemed reluctant to apply similar measures to Greece.

Thanks to the IEO report, we now know that IMF officials sneaked a major rule change into the plan they presented to the IMF board. It allowed an exemption from normal credit standards in cases where there was risk of systemic contagion.

I dont doubt they were worried about contagion. Their action came on the heels of the Lehman Brothers bankruptcy and 20082009 financial crisis. Greece wasnt the only problem, either. There was great concern that anything done for Greece would set a precedent for far larger Spain and Italy. The markets knew that and were watching closely. The fear that contagion would result if the IMF played by its usual rules was not irrational.

On the other hand, rules exist for a reason. Propping up banks that make unwise loans is not part of the IMFs remit. Nor is it the IMFs mission to prop up governments that will not undertake reasonable economic reform measures. Arguably, the whole Greek affair was not the IMFs business. Greece was, after all, a member of the European Union, and the EU should have taken responsibility. I mean seriously, is the State of Illinois going to run to the IMF for aid when it topples into bankruptcy in a few years?

The IMF should have offered nothing but advice and best wishes. Thats not what happened. What were they thinking?

Well, it was around this time that Christine Lagardes predecessor, Dominique Strauss-Kahn, was arrested in New York for alleged sexual assault of a hotel maid. He admitted to inappropriate conduct but denied he had coerced her. Prosecutors dropped charges after the accusers story came into question. Whatever happened, it seems the IMF managing director had more than Greece on his mind. He stepped down in May 2011, and Lagarde took his place a few weeks later.

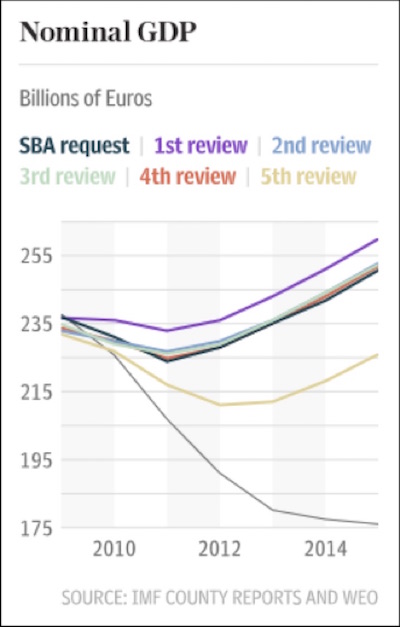

So in addition to being involved where it shouldnt and breaking its own rules, the IMF was also embroiled in internal turmoil while entire nations teetered on the edge. The stress showed up in disastrously wrong growth forecasts used to justify the eurozone bailouts. The thin black line that scrapes the bottom of the following chart is actual Greek GDP. The other lines are forecasts the IMF made in the course of its periodic reviews. By the fifth review they were getting closer to reality but were still tracking far above actual GDP. (Does this put you in mind of the forecasts the Federal Reserve makes?)

It gets worse. It seems that as late as this year, IMF technocrats were actively plotting how to create another European crisis to further their own goals.

We Need an Event

You would think, amid all the hacking incidents and email leaks, we all would have learned that nothing we say is private anymore. Apparently that reality hadnt dawned in IMF circles, because in April Wikileaks released the transcript of an IMF teleconference. The conversation occurred on March 19, 2016, and included the two IMF officials responsible for Greece, Paul Thomsen and Delia Velkouleskou.

Who exactly recorded the conversation and how Wikileaks obtained it is unclear. Here is the interesting part.

THOMSEN: What is going to bring it all to a decision point? In the past there has been only one time when the decision has been made and then that was when they were about to run out of money seriously and to default. Right?

VELCULESCU: Right!

THOMSEN: And possibly this is what is going to happen again. In that case, it drags on until July, and clearly the Europeans are not going to have any discussions for a month before the Brexit, and so,at some stage they will want to take a break and then they want to start again after the European referendum.

THOMSEN: But that is not an event. That is not going to cause them to

That discussion can go on for a long time. And they are just leading them down the road

why are they leading them down the road? Because they are not close to the event, whatever it is.

VELCULESCU: I agree that we need an event, but I dont know what that will be.

The event they are wishing for is something that will put Greece in default and force Europe, particularly Germany, to agree to IMF demands. They see the upcoming Brexit vote as an opportunity, since Britain and others will be looking away from Greece. They also think the event will jar the Greek parliament into agreement.

We dont know if the hoped-for event would have done the trick, since the leak happened weeks before the Brexit vote. At least, the IMF may have demonstrated that it understood the situation. Their goal was to force recalcitrant Greek and EU negotiators into a compromise that had eluded everyone for years. On the other hand, to do so they were apparently willing to set off a whole new crisis, in which case they might have cured the disease but killed the patient.

European Bias

In June 2012, an executive in the IMFs European division named Peter Doyle resigned via a scathing letter to IMF management. His letter made the rounds on the internet at the time but is even more interesting in the wake of the IEO report. It makes very clear the turmoil that was going on inside the IMF. He is describing the status quo within the IMF, and we can assume that he has been its victim (bolding is mine).

Heres what Doyle said:

After twenty years of service, I am ashamed to have had any association with the Fund at all.

This is not solely because of the incompetence that was partly chronicled by the OIA report into the global crisis and the TSR report on surveillance ahead of the Euro Area crisis. More so, it is because the substantive difficulties in these crises, as with others, were identified well in advance but were suppressed here.

Given long gestation periods and protracted international decision-making processes to head off both these global challenges, timely sustained warnings were of the essence. So the failure of the Fund to issue them is a failing of the first order, even if such warnings may not have been heeded. The consequences include suffering (and risk of worse to come) for many including Greece, that the second global reserve currency is on the brink, and that the Fund for the past two years has been playing catch-up and reactive roles in the last-ditch efforts to save it. [It being the euro, which is not an IMF responsibility.]

Further, the proximate factors which produced these failings of IMF surveillance analytical risk aversion, bilateral priority, and European bias are, if anything, becoming more deeply entrenched, notwithstanding initiatives which purport to address them. This fact is most clear in regard to appointments for Managing Director which, over the past decade, have all-too-evidently been disastrous. Even the current incumbent is tainted, as neither her gender, integrity, or élan can make up for the fundamental illegitimacy of the selection process.

In a hierarchical place like this, the implications of those choices filter directly to others in senior management, and via the appointments, fixed term contracts, and succession planning of senior staff, they go on to infuse the organization as a whole, overwhelming everything else. A handicapped Fund, subject to those proximate roots of surveillance failure, is what the Executive Board prefers. Would that I had understood twenty years ago that this would be the choice.

The managing director selection process he mentions is indeed strange. By custom the job always goes to a European. Likewise, an American always leads the World Bank. These unwritten rules serve neither organization well. Both institutions should have the best possible leaders and not rule out highly qualified candidates who happen to come from the wrong continent.

Doyles letter should have warned people that something was badly amiss within the IMF. Instead it was dismissed as sour grapes on the part of a disgruntled employee and the problems got worse. But the real smoking gun was still to come in the form of the IEO report some four years later, which bears out the warnings and confirms the very events that Doyle wrote about.

An Inheritance of Incompetence

The IMF was created to solve the problems of a war-torn world. When those problems no longer needed solving, it reinvented a purpose for itself and morphed into an entrenched bureaucracy, increasingly in the thrall of defunct economists and their hoary economic theories, forcing countries to self-immolate, attacking one crisis after another by creating even more problems. The IMF doubles down on failed strategies by prescribing more of the same, always blaming client states for not following through sufficiently and never acknowledging its own flawed strategies.

Reviewing the internal auditors report in the light of other revelations reveals hidebound bureaucrats creating their own internal fiefdoms and jealously guarding their turf, rewarding those who agree with them and banishing those who disagree to Outer Mongolia (or the bureaucratic equivalent). New directors and managers take their places in the hierarchy and inherit the incompetence and corruption endemic within the system.

Ive been rather harsh on the IMF, but it is just one of many institutions that have created their own bureaucratic nightmares. While there are many people within these institutions who are personally competent, the institutions have come to be driven by their own particular biases and agendas, which they are collectively going to take into the next global crisis. For us to expect that global institutions, including central banks and national bureaucracies, will do anything other than apply more of the same failed fixes to whatever crisis we face in the future is simply to kid ourselves.

The sad thing is that, for most people in most places in the world, the IMF is just the tip of the bureaucratic iceberg. Most countries will not be able to blame the IMF for the problems that pile up in the next crisis. They will have to look hard at their own bureaucratic sclerosis. Until we can change the fundamental orientation the controlling philosophies of these organizations and excise institutionalized incompetence, we are going to continue to get the same dismal results from them.

Denver, Dallas, and Writing

I remember writing that I was going to stay home most of the summer. I look back at my calendar and see that somehow the empty days got filled in, but as I look forward I see only one trip planned in the next few months. Sadly, I had to cancel the trip to Iceland next week. Another time. I know things will happen to change my near-future schedule, but I am going to try to hold travel to a minimum to concentrate on the massive amount of writing I need to do. That being said

I will be in Denver on September 14 for the S&P Dow Jones Indices Denver Forum. If you are an advisor/broker and are looking for ideas on portfolio construction, I will be there along with some friends to offer a few suggestions. And sometime in the fourth quarter I will go public with what I think is an innovative way to approach portfolio construction and asset class diversification.

This new Mauldin Solutions approach makes more sense in terms of what I see coming in our macroeconomic future than the traditional 60/40 investment model that most people and funds tend to follow. I think 60/40 model-based portfolios are going to be

lets just say, very challenged.

Ive been thinking about this portfolio model for a very long time, and now we are putting the final touches on the project. While the investment model itself is relatively straightforward, all of the details involved with making sure that the regulatory is and business ts are crossed the stuff that has to happen behind the scenes are far more complex. Plus, as you might guess, there are white papers to write and web pages to construct.

Tonight finds me on Flathead Lake looking at the mountains as the sun sets behind me on the other side of the lake. Its 107° back in Dallas, but its perfect here right now. And later in the evening, as we watch the stars and shooting stars, Ill have to wear a sweater. Shane and I are at my partner Darrell Cains home, along with nine uber-geek rocket scientists.

You may remember my writing some four years ago about an MIT/Stanford graduate student who developed a brain cancer. He had partnered with a rocket scientist and was developing a very complex new trajectory concept that would increase the life of communication satellites by 30% with no extra cost for fuel. The two had patented the concept and were in the early stages of marketing it when he developed the cancer. The young man, Darrell David, was Darrell Cains son. Darrell had approached me looking for a biotech company that might help his son. I called Patrick Cox, and he pointed me to a private company in Cincinnati that was developing a new therapy for all types of cancer that get past the blood-brain barrier. We all flew to Cincinnati and met the founding partners. Long story short, we put in some money, hoping to speed up their process. Tragically, young Darrell David died before it was possible to attempt an intervention in humans.

As part of his sons legacy, Darrell Cain helped the young rocket scientists launch their company; and now it is up and running, with contracts and revenue coming in. The nine young gentlemen are all part of this venture and are here on a company outing. It is really fun to listen to them talk about new ventures and the future of space. I should mention that three or four of them are full professors at the University of Colorado, which, they tell me, is the number one pure space program in the country. Unsurprisingly, some of these guys are involved in a sophisticated drone company, and Im getting a real lesson in the state of drone technology.

In the evenings I walk away from the computer and geek out with them. No surprise, they are nearly all sci-fi fans. So is Darrell, who has a collection of 2000 autographed first-edition sci-fi books. We all compare notes on favorites. It is possibly the only area we have been discussing where I can hold my own. No matter the advances we are making, I find that we are still a long way from the moon colonies of Heinleins The Moon Is a Harsh Mistress. Of course, Heinlein did set his novel in the year 2075. But moon exploration and maybe even some mining in the next 20 years? Very possible. Wait for my new book before you say no way.

I am working most days, enjoying conversations, and watching for the international space station and Perseid meteors at night, then drifting back in to watch the Olympics, which I probably would have missed if left to my own devices (which would have been a shame).

I will leave here more optimistic than I came. Its hard to be around guys who are totally into creating the future and not be very positive. And, oh yes, that cancer therapy company I mentioned earlier? Phase I safety trials begin next month. Finally. Maybe by this time next year well have some more good news about the potential to improve life back here on earth. Stay tuned. And have a great week!

Your overwhelmed by the complexity of the future analyst,

John Mauldin

subscribers@MauldinEconomics.com

| Digg This Article

-- Published: Monday, 15 August 2016 | E-Mail | Print | Source: GoldSeek.com