-- Published: Monday, 21 November 2016 | Print | Disqus

By John Mauldin

Setting the Stage

Will There Be a Recession in 2017?

What Should Trump Do?

A Few Final Thoughts

RIP Jack Rivkin

The problems of victory are more agreeable than those of defeat, but they are no less difficult.

Winston Churchill

Crying is all right in its way while it lasts. But you have to stop sooner or later, and then you still have to decide what to do.

C.S. Lewis, The Silver Chair

I must have a prodigious amount of mind; it takes me as much as a week, sometimes, to make it up!

Mark Twain

No matter who won the presidency, the economic way forward was not going to be easy. The Republican team understands they must stand and deliver. But as we will see in todays letter, that is not going to be easy. Im going to depart from the normal format of my letters, where I talk about the economic realities we face and how we should invest, and instead offer my view of what I think the Trump administration and the GOP-led Congress should do.

Please note, this is not necessarily what they will do. In complete candor, what Im proposing will be remarkably difficult for certain members of the Republican and Democratic Congress to countenance. It requires accepting some significant philosophical heresies that are anathema to all politicians (different heresies/anathemas for different politicians, according to their philosophical bent), but I see it as the only way forward if we want to dodge a deep recession and/or a greater crisis in the future.

I know for a fact that many of the people you have seen listed on the Trump economic transition team will be reading this. That is one reason Ive been taking so long to put these thoughts to paper. And some of the ideas Ill share are quite frankly things I have come around to in just the last week. I will readily admit to having already mentally written my post-election letter based on the assumption that Hillary Clinton was going to win; and on Wednesday morning I had to throw out everything I had thought about and start all over. And its not just you and I who had to shift gears quickly: I know that quite a few people on the transition team had speaking engagements and other projects arranged for later that week, and they had to scramble to redo their schedules.

Ive done a lot of talking with a lot of people and listening and reading in the last 10 days. This letter is where I currently come out. What Im going to propose is something that I think is politically possible (in terms of gaining bipartisan support, which will be necessary for certain portions of what Im suggesting). I also think it has the potential to solve the deficit/debt problem and provide the funding needed for healthcare, Social Security, and the other necessary categories of government spending. It would also be a massive stimulus to the economy boosting jobs, new business creation, and entrepreneurial activity.

Up front we must face the fact that the American people want several incompatible things at once: They want lots of expensive healthcare provisions for everyone; they want tax cuts; and they want a balanced budget. As we will see below, we can have relatively universal healthcare (no matter how its funded and delivered), tax cuts, or a balanced budget; but we can have only two of the three. Most Americans want all three and dont see why they shouldnt have them. There are some exceptions there are, for example, some economists who dont care about tax cuts or a balanced budget. They are working from an economic theory that says deficits and debt dont matter; but in practice, in the observable, empirical world, they do matter. Greatly. Maybe not this year, but sooner or later the piper has to be paid.

Setting the Stage

Lets look briefly at where we are now at the constraining facts that any economic proposal must take into consideration.

The US federal government debt will be slightly north of $20 trillion before Obama leaves office in January. Add in local and state debt of another $3 trillion (plus), for a total of more than $23 trillion of government debt. The US economy will be a few hundred billion dollars under $19 trillion at the end of this year. That is a debt-to-GDP ratio of somewhat over 121%. For the record, when you are trying to determine the effects of total government debt on the economy, not to include state and local debt is disingenuous. The debt must all be paid by the same general taxpayers at one level or another. (Please note: I am rounding out the numbers in this letter because when youre talking about trillions and hundreds of billions, anything to the right of the decimal point is kind of meaningless.)

That debt has risen roughly $10 trillion under Obama, in just eight years. Last year the debt rose $1.3 trillion, even though we were told that the budget deficit was only around $600 billion. Lots of off-budget debt gets added every year. It greatly annoys me when spin doctors dont include total debt when they are talking about the deficit (and they do it on both sides of the aisle). I wish I could get my banker to adopt the same enlightened view.

I know that Krugman and others call me a debt scold (scornfully, as if I am some kind of troglodyte coming out of my cave to issue unnecessary warnings), but there are 160 historical instances of major countries having to renegotiate their bonds because they had too much debt, and in the recent century some countries that did so ended up in serious financial crises. I dont for a minute think that the US will not pay every dollar of its debt; but getting those dollars, whether through taxation or printing, will impact the economy significantly. And if we wait too long, the ensuing crisis could be ruinous to many.

I start with the premise that to get the deficit and debt under control is an a priori condition for avoiding a future crisis. Avoiding that crisis even if it is 10 years out is important. The solution doesnt have to be implemented all at once, but there has to be a clear trajectory along the lines of the Clinton/Gingrich budget compromises that gave us balanced budgets and even deficit reduction.

Standard Republican thought is that we have to engender enough growth to overcome the deficit. The Reagan tax cuts certainly increased the deficit, but when they were combined with the Clinton/Gingrich budget controls, we were soon paying down the debt and growing much faster. The debt became far less of a problem, at least in terms of GDP. It was when Bush II and the aggressively enabling Republican Congress basically abandoned budgetary controls (we could have used a deficit hawk like Gingrich as Speaker of the House to control the spending urges), combining tax cuts with large spending programs, that the deficit and debt once again began to get out of hand. Then along came the recession, triggered by the housing bubble brought on by interest rates held too low for too long by the Federal Reserve; and seemingly all of a sudden the deficit exploded $10 billion in just eight years.

Sidebar: Everyone focuses on the size of the federal budget as if that is the government. The US federal spending budget is $3.88 trillion as of this year. State and local outlays are $3.3 trillion, bringing us close to $7 trillion of total government spending. Very few people realize that state and local spending is almost the same size as total federal spending.

Total US debt, including private and business debt, is $67 trillion, or just under 400% of GDP. We have 95 million people not in the labor force, 15 million of whom are not employed (twice the number officially unemployed). We have almost 2 million prison inmates, 43 million living in poverty, 43 million receiving food stamps, 57 million Medicare enrollees, and 73 million Medicaid recipients. And 31 million still remain without health insurance. (Youll find a treasure trove of information like this at the US Debt Clock.

This US debt total does not even take into account the over $100 trillion of unfunded liabilities at local, state, and federal levels, which are going to have to be paid for out of current revenues at some point (see more below).

I bring up the size of the debt because unproductive debt is a limiting factor on growth. 10 years ago it wasnt that big a deal. Today it is. The more we increase our debt, the more difficult it is going to be to grow our way out of our problem with the debt. Thats just an empirical fact. Both Europe and Japan have much larger debt ratios than we do, and both have much slower growth rates. Note also that the velocity of money in both those regions is much lower than ours, and the velocity of money in every developing portion of the world continues to drop. (More about that below.)

Something like $5.5 trillion is intergovernmental debt. The theoretical Social Security trust fund is an example. We owe it to ourselves, and so many economists simply deduct that money when they talk about the size of the total debt. And technically it is true that we pay interest on that debt, which comes back to the government. But that doesnt mean those debts arent going have to be paid.

The Social Security trust fund assumes as part of its future budgeting process that the interest will be paid. So do most other intergovernmental debtors. Think of it like borrowing against the cash value of your life insurance. You technically owe the money to yourself, and you are (typically) paying interest on the amount you borrowed, but if you die your outstanding debt reduces the amount of your life insurance. If you want the life insurance, youre going have to pay that borrowed debt. For economists to talk about this portion of the debt as irrelevant is economic malpractice. It is smoke and mirrors economics of the worst kind. But even if we did dismiss $5.5 trillion dollars of internal debt, the governments debt-to-GDP ratio would still be almost 100% when you include state and local debt. And that is definitely in the range where all the data and economic analysis suggests that debt is a detriment and a drag on growth.

Vice President Dick Cheney once remarked that Deficits dont matter as he defended his spending on the Iraq and Afghanistan wars. And when he said it, he was more or less correct. Then, the deficit as a percentage of GDP was less than nominal GDP growth, which meant that the country was growing faster than the debt was. (Later, it turned out that deficits did matter, when the spending on everything else plus defense spun out of control.) And for those people who say that tax cuts create growth, I would suggest that 2% growth for 16 years is not exactly what we were expecting. And much of the growth we did get during the housing bubble years was clearly spurious.

Yes, the US economy has grown at something like an average 2% for the last 16 years. Inflation was higher in the early years, but now it is about 1.5%, which gives us nominal GDP growth of about 3.5%. Total debt this year rose by 6.8%, or almost double our growth rate. Not the right direction. After eight years of the slowest economic recovery in history, we are growing our debt dramatically faster than we are growing our country even when we include inflation.

Remember that seemingly innocuous velocity of money bit of detail that I threw in earlier? You need the velocity of money to begin to increase so that you can actually get inflation. Ask Japan about how much money you can print without getting inflation. That also suggests it is going to be harder to create inflation than many economists would like. I know that many establishment economists would like to see inflation closer to 4%, with GDP growth of 3%, so that we could begin to quote grow our way out of the debt. Thats not impossible, but its highly unlikely. Frankly, we will be lucky to get 2% growth and 1.5% total inflation for the next four years.

Republicans want to cut corporate and individual taxes to help stimulate growth. That is a necessary but not sufficient condition to stimulate growth. Significant regulatory rollback will help. It is also necessary but not sufficient. Fixing the Affordable Care Act and bringing costs and benefits into alignment is another necessary but not sufficient condition for growth.

There is a major lag time for any economic programs that are enacted. Even if they are enacted in the first 100 days of the Trump administration, it will be months if not years before we see actual results. A $19 trillion economy does not turn on a dime.

Will There Be a Recession in 2017?

My friend Raoul Pal, in his latest Global Macro Investor, talks about the potential for a recession in 2017:

I recently noted that since 1910, the US economy is either in recession or enters a recession within twelve months in every single instance at the end of a two-term presidency

effecting a 100% chance of recession for the new President.

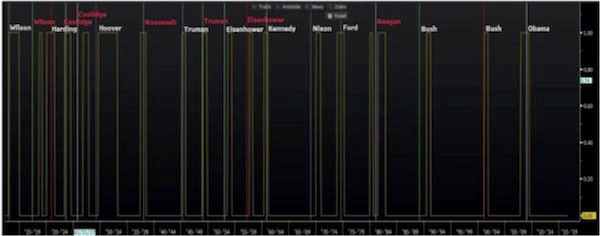

The following chart shows every NBER recession since 1910 (in yellow) with the new President after a two-term election marked in white and the new presidents after a single-term presidency in red. Wilson and Eisenhower appear as both. Only Coolidge saw more than a year (sixteen months) from his second-term election and the onset of the subsequent recession at the end of WWI...

Every single US recession bar one (with explainable circumstances) occurred around an election. Only two Presidents in history did not see a recession, and they were inaugurated after single-term Presidents.

You can see the whole piece here. There are a few caveats and some slight curve fitting, but his general observation of recessions after a two-term presidency pretty much holds as far as I can see.

A proper objection many will have to this finding is that there are not enough data points to make it a really accurate predictor. There is nothing that I can think of economically about a two-term presidency that requires a recession to follow it. And if the economy were now growing at 3% to 4%, if unemployment were truly under 4%, and if we had the deficit under control, I wouldnt be worried at all. But Raoul has pointed out a statistic that appears on my radar just as Im also watching the country grow rather slowly (at very close to stall speed) and seeing corporate profits come under pressure while the post-election US dollar rises seemingly relentlessly (doing damage to US corporation profits, not to mention emerging markets) and interest rates climb all over the world. And then theres Europe, which could potentially deliver a massive shock to the global economy in the not-too-distant future

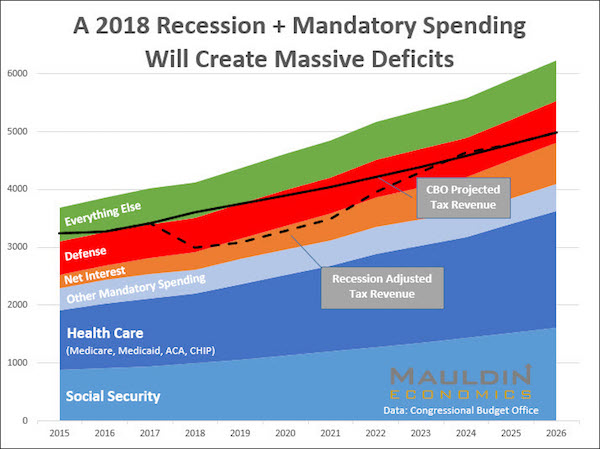

Patrick Watson had our team at Mauldin Economics create the following chart, which shows what would happen to the federal budget if there were a recession in 2018. (If the recession were to move up to 2017 or if it were to hold off till 2019, the result would be much the same.) Revenues go down, and expenses go up. Note that taxes actually received under the current system would pay only for mandatory spending like healthcare and welfare and Social Security plus interest costs. Money for defense spending and everything else would have to be borrowed. The on-budget deficit would rise to over $1 trillion closer to $1.3 trillion. Add in the off-budget debt that always seems to increase and you could quickly grow total US debt to $30 trillion before the end of Trumps first term.

Obviously, that doesnt take into account any of the measures the new administration will put in place to try to hold off the effects of a recession or to resolve any of the problems Ive described. This is just using CBO data for our current trends. By the way, the chart also shows that we can expect trillion-dollar budget deficits as far as the eye can see.

I should point out that federal income tax revenues are basically flat, even though the jobs numbers are up. That means a lot of people are getting lower-paying jobs. The underlying economy is weaker than it appears.

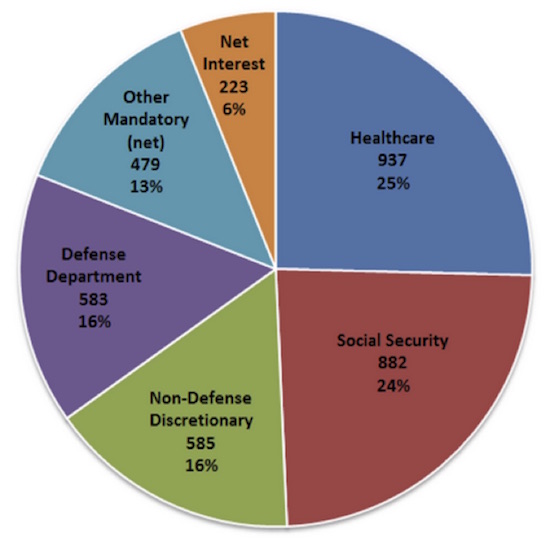

Just to demonstrate that we cant balance the budget by cutting out waste and fraud (which of course we should do), let me offer the following pie chart. Even if you cut out every single non-defense discretionary item, the budget still would not have been balanced last year, at the tail end of a recovery.

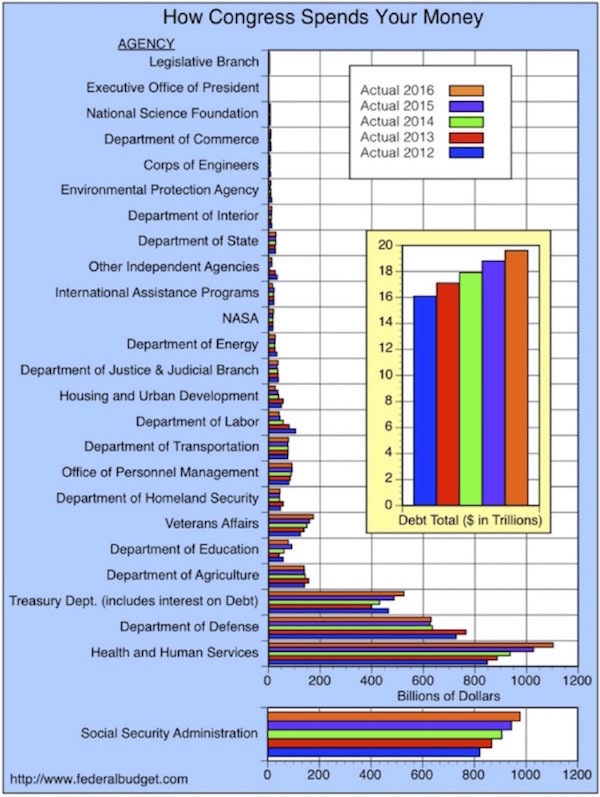

For some detail, take a look at this bar graph, which shows the growth of spending in the various branches and departments of government. Which areas are you going to cut to make any meaningful difference?

For the purposes of my argument, I am going to assume that the Republican Congress and administration somehow wrestle with the Affordable Care Act and bring actual individual healthcare costs down. But the demographic reality of the Baby Boomer Bulge is that no matter what we do, overall costs are still going to rise again within a few years unless we ration healthcare, which is not a viable political option. As Baby Boomers retire in droves, not only will they need more healthcare, they will also need more Social Security. There are things we can do to get the whole healthcare process under control and to improve the general health of the country, but thats not going to have a significant effect in the next two or three years.

So bluntly, if you cut income and corporate taxes (which is something I think we should do) without any offsetting revenue increases, youre going to make the deficit and debt problems worse. As one of my readers wrote me last week:

Hi John,

Very briefly: If Trump does a Reagan and makes his voter base happy with unfunded tax cuts that triple the national debt by the time he ends his second term, wont that just put off tough choices and make everything worse in the long term?

Regards,

Douglas

Douglas, while I dont think the debt will triple, it is easy to imagine that it rises by 50%, which would, in and of itself, be problematical. It does put off the hard choices and make them a lot harder still when we hit the wall.

So let me offer a program that I think might actually solve the deficit and debt problems, jumpstart the economy, pay for healthcare and other costs, and do so with the least damage to the body politic and economy.

Let me again restate for the record that any one of these suggestions taken apart from the rest of the body of actions might be useful but would not be sufficient to ensure recovery and a balanced economy. It is with a somewhat heavy heart that I offer these proposals, knowing that there will probably not be one person who doesnt find some of them extremely distasteful. And that includes me. But the simple reality is that this is where we find ourselves today: we are left with distasteful choices. When youre left with nothing but difficult choices and bad choices, and you avoid the difficult ones, then you end up with only bad choices (cf. Greece).

What Should Trump Do?

1. Cut the corporate tax rate to 15% on all income over $100,000. No deductions for anything. Period. A 10% tax rate on all net foreign income (with allowances for taxes paid against total income.) That will make us the most tax-friendly business nation in the world, competitive with Ireland, and stops all the financial shenanigans that try to avoid taxes. International companies will not only move their headquarters here, they will bring their manufacturing and jobs with them. Ask Ireland how that worked out for them. I can imagine a horde of global companies moving from Europe and elsewhere to take advantage of the competitive taxes. Frankly, it will put them at a disadvantage if they dont.

The simple fact is we will collect more total corporate taxes under this plan than we do under the current system with all its deductions and loopholes. This tax plan will have the side benefit of putting out of work an army of lobbyists whose sole role is to try to get tax benefits for their clients.

2. Cut the individual tax rate to 20% (and later Im going to demonstrate how it could even be 15%) for all income over $100,000. No deductions for anything. Period. No mortgage deduction, no charitable deductions. No nothing. Anybody who makes less than $100,000 will not pay income taxes and will not file. This will dramatically promote entrepreneurial activity and help small businesses.

So far, the above is standard Republican doctrine. Now were going to venture into left field.

3. Im working under the assumption that we must make a serious effort to have a balanced budget and to fund healthcare and Social Security. That requires money, which is another way of saying that we will need to find taxes from another source. I would propose some form of a value-added tax (VAT) that would specifically pay for Social Security and healthcare. All the other parts of government are paid for from income and corporate taxes. Given the monster size of the healthcare budget, we would need somewhere close to a 15% VAT. That could change somewhat depending on various workarounds. For instance, if you drop the income tax to 15% but keep the 3.9% Medicare tax, that would leave the total tax rate under 20% but would offer a portion of payment for healthcare, which might mean a lower VAT.

I personally presented this plan to Senators Rand Paul and Ted Cruz, who later adopted a version of it that they characterize as a business tax; but I dont care what you call it. There are multiple variations on the theme, and I only mention Paul and Cruz to point out that you can actually get serious conservatives to consider such a tax. Now, to be fair, they were against increasing the total amount of taxes taken. And that is not what I am advocating here. To pay for healthcare and balance the budget, we are going to need to generate more revenue. Not a whole lot in terms of percentage of GDP, but some.

Let me reiterate that whatever you call the VAT-like tax, it would be specifically targeted at paying for healthcare and Social Security. If you want to hold down the amount of the VAT, then Congress needs to aggressively figure out how to hold down the cost of Social Security and healthcare. This does not eliminate the need for aggressive restructuring of both of them. In fact, it would require it.

4. Policy wonks are going to note that you would not need a 15% VAT just for healthcare. I would propose that we eliminate Social Security funding from both the individual and business side of the equation and take those costs from the VAT.

Progressive and liberals will complain that a VAT is a regressive tax it falls more heavily on lower-income people since they spend much of their income on items subject to such taxes. For the truly lower-income, you could offer a rebate to even out the load, but if you get rid of Social Security taxes you give everybody a 6.2% raise and a 6.2% reduction of employment costs to businesses.

Getting rid of individual and business Social Security payments is the opposite of regressive and so balances out the cost to the working poor rather well. Those with incomes between $40,000-100,000, who had been making Social Security payments, would not be paying income taxes, so a VAT would still be a cost reduction for them.

This would be a huge stimulus to the economy. Plus, VAT taxes can be deducted by businesses at the border when they export products. This would make us competitive with every other country in the world whose companies also deduct VATs at the border.

As a general rule, most economists (even guys from Harvard and Princeton) will tell you that a consumption tax such as a VAT is better than an income tax in terms of its overall impact on the economy.

5. We need to jumpstart the economy, and both sides of the partisan divide are talking about some kind of infrastructure program. The problem with infrastructure spending is that it still adds to the national debt, which is already outsized. I do think we need infrastructure spending, as infrastructure is typically productive as opposed to nonproductive, and the program would help to jumpstart growth. But I would do infrastructure a little bit differently. I would create an Infrastructure Commission that would authorize federally guaranteed bonds for cities, counties, and states. Thats not significantly different from the guarantee we extend to the $1.7 trillion in Ginnie Mae bond funds.

The guarantee would let these entities borrow at 30-year Treasury rates, which right now is around 3%. The program would allow the authorization of up to, say, $1 trillion in infrastructure bonds for projects initiated within the succeeding three years. The various political entities that issued the bonds would have to legally agree to cover the payments to retire the bonds over 30 years. I would prefer that they couch this agreement in the form of a public vote so that the citizens can see what theyre agreeing to.

Further, we could subsidize the bonds at 2% for the first 5 years and 1% for the next five years, which would mean a $20 billion per year expenditure for those first five years. But also recognize that it would be highly unlikely that $1 trillion would be put to work by the end of the next four years. In the meantime, millions of jobs would be created by the process, which would generate GDP growth and tax revenue and would be very likely to produce more in terms of revenue than the program costs. Plus, our kids get something for the future water systems, new ports and airports, roads, bridges, etc.

There could be some exceptions to the focus on state or local funding for projects that are truly national in scope. A Smart Grid (that would also hopefully be EMP-hardened to counter a potentially civilization-ending threat that few people are talking about) is a good candidate; and frankly, we could save enough in electrical costs that we could probably work the payments for the bonds into power bills as a very small-percentage add-on that comes out of the savings.

The commission itself should be composed of savvy businessmen and women who are hopefully not politicians (or who have been retired from politics for at least six years). Members from a particular state or polity would have to recuse themselves on any vote that affected that jurisdiction. The commission would be responsible not only for determining that there is local buy-in to the process, but also that the political entity issuing the bonds is capable of making the payments.

6. Roll back as many rules and regulations as possible. I would instruct every cabinet member to find, every year for four years, 5% of the rules and regulations within their purview and eliminate them. If they want to write a new rule, they have to find an old one to eliminate. Bureaucrats are like your crazy old aunt who still has every magazine she has gotten for the last 30 years just in case she might need to go back to some article and read it again. Time to clean out the attic.

In particular, I dont want to reform the FDA; I want to replace it lock, stock, and barrel with a 21st-century drug regulatory authority that promotes innovation and allows individuals, in consultation with their doctors, to opt for potential life-changing and even death-preventing treatments if they so choose. Im tired of having friends die of diseases for which there are cures in the pipeline, but the companies with the treatments are prevented from even making medications available to dying citizens. To withhold such aid is, to my mind, a criminal act.

That would not be a bad approach for every regulatory authority to take: Forget about the legacy rules and think about the world as it is today and how it will change, and design a regulatory system that not only enables and encourages change but that makes sure everyone benefits.

7. Trump will have two immediate appointments to the Board of Governors of the Federal Reserve. He will have another two in another year, giving him four out of the seven governors. I would also imagine that, given the ambitions of some of the other current governors, they will opt for the much higher income available in private practice. Having a Federal Reserve that is more neutral in its policy making and that realizes that the role of the Fed should be to provide liquidity in times of major crisis and not to fine tune the economy, will do much to balance out the future. I have several names in mind that I would like to submit, but one in particular is Dr. Lacy Hunt, a former Federal Reserve economist and one of the finest economic minds in the world. Kevin Warsh or Richard Fisher might come back to the Fed if either were nominated as chairman (although it would be a large pay cut for them). Janet Yellens term as chairman expires in January of 2018, though s he could remain on the board if she opted to. I cant imagine anybody would want to hang around on the board after theyve been chair.

8. Getting trade right will be tricky. It is one thing to talk about unfair trade agreements and we have certainly signed a few. But we also need to recognize that some 11.5 million jobs in the US are dependent upon exports (about 40% of which are services). Frankly, if we drop our corporate tax to 15% and work on reducing the regulatory burden, I think we will be pleasantly surprised by how many jobs are created just by those steps alone.

9. In connection with trade, as I look around the world I see other countries experiencing or getting ready to experience economic stress that is going to force them to allow their currencies to weaken against the dollar. The euro is already down by over 30%. The potential crisis in Italy (not out of the question and a topic for a future letter) could easily push the euro below parity. The value of the dollar relative to the currencies of other countries comes under the purview of the Treasury Dept., not the Fed. And I can imagine a time when we will see some strange new policies being suggested because of the competitive pressures exerted by a strengthening dollar.

A Few Final Thoughts

The central advantage of the entirety of my proposals is that they offer a path to a finance the needs of the country and at the same time allow a balanced budget. The actual increase in the total tax revenue needed will be a function of the degree to which Congress can get the various budgetary items under control, especially healthcare and Social Security. I know a lot of conservatives would like to see no increase in total tax revenue to the federal government, and if we can do that and balance the budget, I am all for it. I am decidedly in the camp that government is too large and would be more than happy to eliminate a few departments here and there.

But voters clearly want healthcare and Social Security benefits to be paid for, along with other government services that are actually necessary (especially defense). Therefore, we must figure out how to pay for those services. Simply holding government expenditures flat for four years would go a long way to solving the problem, but it wont get us all the way there.

Boosting growth is going to be difficult. This is not the 1980s and the environment that Reagan encountered. Stock markets are at highs, not lows, as they were in his term. Today, the market capitalization is 196% of GDP, versus 40% when Reagan took office (hat tip Stephanie Pomboy). Reagan also had a falling-interest-rate environment. Plus he had a huge demographic shift to work with, from Baby Boomers coming of age. Reagan also had his recession at the beginning of his term, so the economy was coming off its lows. There was a great deal of pent-up demand, which is not presently the case. All of these factors were a great help in spurring the economy when combined with tax cuts. Those conditions all tended to boost growth, yet they dont exist today.

We can have growth and create good jobs, but its not going to look like the 80s and 90s. Our rebuilding of the economy will have to take a different path, and a more challenging one in many respects.

Let me be very clear. If we dont get the debt and deficit under control and by that I mean that at a minimum we bring the annual increase in the national debt to below the level of nominal GDP growth we will simply postpone an inevitable crisis. We have $100 trillion of unfunded liabilities that are going to come due in the next few decades. We have to get the entitlement problem figured out. And we have to do it without blowing out the debt. If we dont, we will have a financial crisis that will rival the Great Depression. Not this year or next year, and probably not in Trumps first term, but within 10 years? Very possibly, if we stay on our present trajectory.

For investors, navigating the next few years is going to be tricky. We already have multiple markets with valuations at the upper end of their historical trading ranges. Interest rates are likely to rise, although by less than most people now assume.

OK, Im going to close now, and perhaps in the future letter I can answer questions and criticisms Ive provoked here. As always, I look forward to your comments.

RIP Jack Rivkin

It is with a heavy heart that I pen a few thoughts about the passing of a man known to many of my readers and one came to be one of my best friends, Jack Rivkin. He was a Wall Street legend who ran one major investment group after another, ending up as head of investment for Neuberger Berman. He was lured out of retirement by friends of his who had made a major investment in a firm that I work with, Altegris Investments. Jack came in and eventually became CEO, with the intention of doing what he did so well: creating new investment practices and themes that end up becoming industry standards.

I first met Jack in a plane coming back from somewhere overseas (I really cant remember where) and then again at various conferences. We both had an abiding interest in the future and technology and their implications for investments. I could spend, and often did, hours talking with him on an extraordinarily wide range of topics. His investment analysis was brilliant, and it was always delivered with good grace and a lot of humor. He was involved in dozens of technology startups with no seeming connections among them other than that they were fun and interesting projects. I cant remember many occasions when he wasnt smiling. He was just generally happy and a fun friend to be around.

With his involvement at Altegris, we became much closer, as we both believed that the future of the investment business is going to be much different than its past, and we were trying to figure out not only what it would look like but how to be part of it. He began to participate in the annual Camp Kotok fishing trips in Maine. In the summer of 2015 I remember visiting him at his home in the Hamptons, where we talked earnesting about working together for the next 10 years and how to make that happen.

And then, it seems suddenly, he was diagnosed with pancreatic cancer; and after a typically optimistic struggle, he succumbed to one of the nastiest diseases known to humanity. Honestly, the outcome is still shocking. We had talked about how he had great inherited genes and had more energy and was in better shape than I am.

Our mutual friend Barry Ritholtz wrote a very good tribute to Jack in his Bloomberg column, calling him a Wall Street research giant. And he was. But to those of us who knew him well, he was much more. He was a giant of a friend. He will be missed.

And with that, let me wish you a great week. I look forward to reading your comments on this letter. Last week my staff sent me a Word document that was 23 pages long with your emailed comments. Plus, there were many online comments. There is a great deal of passion on every side about the outcome of this election. This election was not my first rodeo; but that being said, I dont recall there ever being this amount of emotional upheaval and national drama. The next four years are going to be interesting, and I plan to be right here with you, trying to figure out and create the way forward.

Your wondering how the transition will come about analyst,

John Mauldin

subscribers@MauldinEconomics.com

| Digg This Article

-- Published: Monday, 21 November 2016 | E-Mail | Print | Source: GoldSeek.com