-- Published: Friday, 16 December 2016 | Print | Disqus

By Market Anthropology

Rattling an already skittish government bond market, Chair Yellen delivered another seasonal interest rate hike with seemingly greater resolution that the New Year will be tighter than the last

The Fed's holiday wishes had all the usual hawkish trappings we've seen from time to time when the data aligns, with greater confidences in the economy that not one but three, separate rate hikes could be delivered next year. Not surprisingly, the expedited path sent the dollar and shorter-term yields screaming, the net effect of which hit hardest at emerging market debt and equities as well as gold that had already lost its luster since the US presidential election last month.

Of course cynics and trends be damned, as many ourselves included, have tasted a respective macro victory over the past few years only to find it to be more ephemeral than satisfying. Generally speaking, trending markets became increasingly range bound with the transitional illusion that a more lasting pivot was closer than it actually was or perhaps is. Essentially, markets became more or less a fractal expression of the Feds own collective range of confidence with enacting policy. The question today is has that calculus changed and will the Fed or Trump be able to maintain a breakout or even an illusion of one, as whos to say where reflexive expectations become reality.

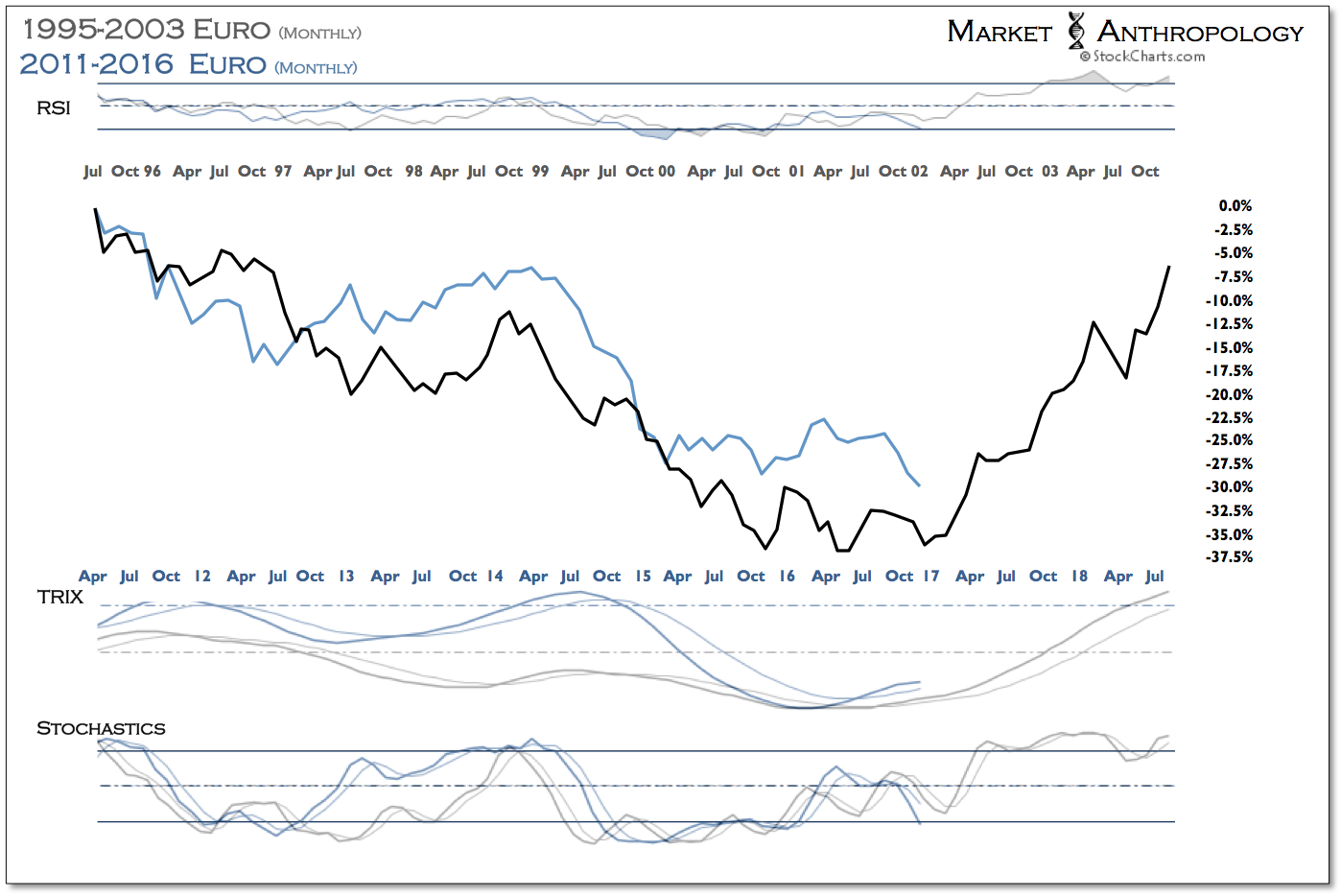

While the strength in the dollar this quarter has certainly given pause to our own expectations of a cyclical move south, we continue to look through the wide-angle lens of a more long-term prism on the dollar and yields that we have argued points towards another reversion to the mean of both the Feds own confidence in enacting policy as well as the respective long-term downtrends in the dollar and yields. Overall, although it certainly has not been a crisp pivot lower for the dollar, we are again reminded it is the trough of the very long-term cycle, which as history depicts pivots with less volatility than the sharp reversals witnessed at secular highs e.g. yields 1981, dollar 1985.

_______________________________

"It's like deja vu all over again," said Yogi.

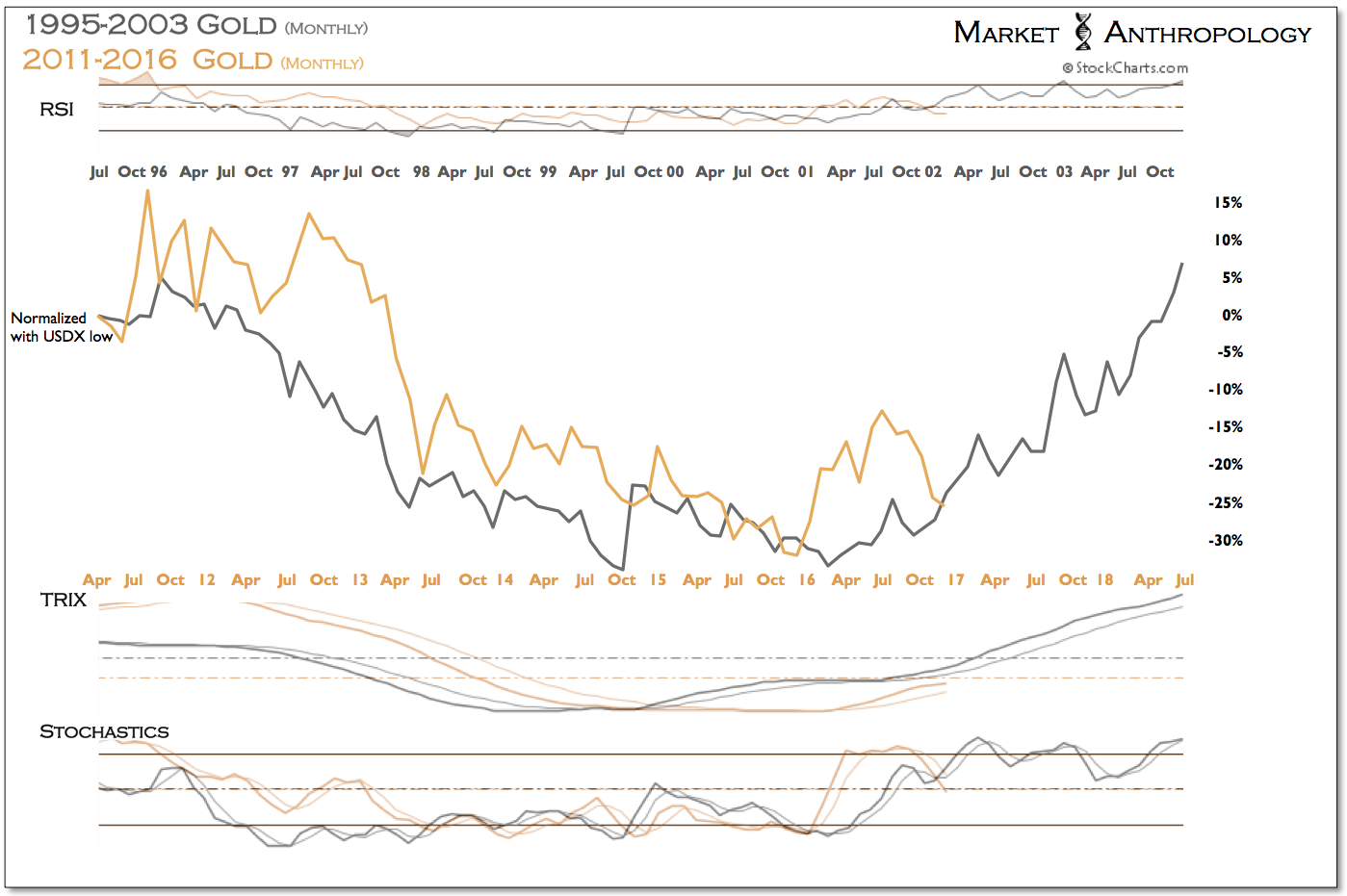

The day after the December Fed meeting where a major policy shift was enacted has presented a tradable low in gold over the past few years. The chart below was one we had followed from the 2015 rate hike, with strikingly similar conditions in sentiment to last December. Note the strengthening inverse correlation with the dollar.

US equities have made the outlier breakout move with the dollar. We don't have confidence in either and suspect they follow gold's lead lower as emerging markets have begun to breakdown this week.

The move lower in long-term Treasuries has been relentless, now eclipsing the bloodbath of the 1987 breakdown. Although our long-term chart of the 30-year bond impressions a prospective move to ~140, we would speculate the risk/reward shifts long for investors today around these levels.

Granted, looking back at previous cyclical highs in the dollar index has been as useful to-date as the Fed's own dot plot projections, we still firmly believe that lower-for-longer will ultimately prevail in both yields and the dollar and that the relative and absolute performance of both previous major cyclical bull markets in the dollar augurs that there's much greater room on the downside for opportunity in investors longer-term investment theses. And although gold and silver have taken it on the chin in recent weeks, we still approach them as volatile proxies for commodities that should have another day in the sun as the dollar weakens on a more lasting trajectory.

http://www.marketanthropology.com/

| Digg This Article

-- Published: Friday, 16 December 2016 | E-Mail | Print | Source: GoldSeek.com