-- Published: Monday, 2 January 2017 | Print | Disqus

By John Mauldin

Trumping DC

Canadian Bubble

Crowded Exits in Europe

Asian Angst

DC, Florida, the Caymans, and a Few Final 2016 Thoughts

Experience is simply the name we give our mistakes.

Oscar Wilde

Mistakes are the usual bridge between inexperience and wisdom.

Phyllis Theroux

Economists are often asked to predict what the economy is going to do. But economic predictions require predicting what politicians are going to do and nothing is more unpredictable.

Thomas Sowell

Weve reached that wonderful time of year when financial pundits pull out their forecaster hats and take a crack at the future. This time the exercise is particularly interesting because were at several turning points. Any one of them could remake the entire year overnight. I should probably say up front that I am actually somewhat optimistic about 2017 optimistic, meaning I think we Muddle Through but thats a lot better outcome than I was expecting five months ago. And since my annual forecast has been Muddle Through for about six years now (which has been turned out to be the correct forecast), then, given all the speed bumps in front of us, this could be the year where Im spectacularly wrong. Midcourse corrections may be warranted.

Ill have my own specific predictions later this month, along with a review of others that I find instructive. Todays letter, though, will preface that discussion. Instead of trying to answer questions about the future, Ill try to list those we should be asking as 2017 opens. These are the things that I sit and meditate about when I consider the future of economics, markets, and investing. Todays economy is something like an old-fashioned Swiss watch. Its a thing of beauty when all those delicate little gears mesh just right. If you ever take the time to actually study the inner workings of the marvelous manifestations of human ingenuity that keep us all alive, it is difficult not to come away awestruck by the ability of the human mind to craft such complexity. But if any of the gears get just a little out of whack, the entire contraption can grind to a halt.

Now, if your watch stops working, it isnt the end of the world. You can know roughly what time it is just by looking out the window. The global economy is another matter we cant afford for any of its major components to break down; so its smart to ask, Where are the weak points. Thats what well do today: Well poke at the economic mechanism as it grinds along here on New Years Eve 2017; then Ill get more specific in my forecast issue.

Before we begin, let me briefly mention that our most exclusive service of all, the Mauldin Alpha Society, is currently open to new members.

I launched the Alpha Society last year as a way to connect more intimately with my most valued readers the idea chasers, as I call them. If you join this inner circle of the Mauldin Economics family, youll pay a one-time initiation fee (plus a small annual maintenance fee) and receive all our research for life.

How fast this investment pays for itself depends on which services youre already subscribed to, but I can guarantee you that you will completely recoup your investment in no more than two and a half years. After that time and potentially much sooner youll essentially get everything we publish for free, for as long as we publish.

Aside from saving copious amounts of money on subscriptions every year, as an Alpha Society member youll enjoy all sorts of useful perks among them a generous discount on the coveted tickets to my Strategic Investment Conference (to be held this year in Orlando, Florida) and the opportunity to attend a special SIC meet n greet, hosted by yours truly, where you can share drinks and thoughts with me, our blue-ribbon speakers, and the Mauldin Economics editors.

These events are always my favorite part of the SIC. Its where we get to pick each others brains about our mutual investing future. I learn so much every time we hold these get-togethers that by now Im convinced we have some of the most brilliant subscribers of any investment research service out there.

I hope youll join us this year as an Alpha Society member, so we can get to know each other. Enrollment is open until January 15 or until we have filled the 300 available member slots, whichever comes first. Get all the details here.

Now, lets look under the hood at 2017.

Trumping DC

The biggest change will happen in Washington when Donald Trump takes office. Aside from the changes he can make on his own authority, hell be in position to approve the many Republican initiatives that President Obama blocked. Here are some items Im watching.

Tax Reform: Our monstrosity of a tax system needs major reconstruction. Ive described what I think would be ideal: a reduction and simplification of corporate taxes, a significant reduction of the individual income tax, and replacement of the Social Security tax with a VAT-like consumption tax. What will come out of the House is still unknown. If you look at House Ways and Means Chairman Kevin Bradys bill, he uses the word tariffs, but his proposal looks suspiciously similar to the VAT that Im suggesting, except that Republicans arent allowed to say VAT saying Im against it in the same sentence. Or at least they couldnt until both Rand Paul and Ted Cruz basically suggested a VAT. I will admit to discussing the topic with both of them, but their versions are an amalgam of ideas.

My sources are telling me House members want to pass an initial tax cut quickly and defer the more complicated changes for later in the year. The easy initial tax cut is to remove the Obamacare tax when they repeal Obamacare (the Affordable Care Act), which it appears they will do early in the session. It wont be an immediate repeal but rather a slow, orderly retreat. But getting agreement on a replacement system is going to be contentious. The problem is the Medicare taxes dont kick in until about $250,000 of income.

While the tax outcome could be nice for some of us, Im afraid of the political perception problem if the first tax cuts go mainly to high-income taxpayers. Democrats will cry foul and try to force a split between the GOPs business wing and its new populist elements. More to the point, a tax cut for the wealthy wont stimulate the economy enough.

So I very much hope the first tax cuts either target middle- and low-income taxpayers or at least somehow encourage beneficiaries to reinvest their tax savings back into the economy. Lack of capital is not our problem; we need to stimulate demand and tax policy can help.

Final thoughts on taxes: What Kevin Brady is saying basically sounds good, as he acknowledges that some industries will suffer massive impacts if you slap tariffs on incoming goods. Further, putting a high tariff on products that are sold at Walmart and Costco and on Amazon is massively inflationary to those shoppers (and thats most of us). Look at the immediate and one-time negative effect on inflation in Japan when they increased their sales tax a few years ago. These policies can be tricky, and the consequences can have a big impact on consumer confidence.

You have to be very careful about applying tariffs to raw commodities that we need as inputs to our own manufacturing but that we cant produce in sufficient quantities here at home. We dont want our manufacturers to be hamstrung because we load them up with increased costs for their input materials, like iron ore, heavy crude, or rare earths. Those materials are in a different category than processed goods. Like I said, its tricky. Changes as massive as the ones being contemplated simply cannot be good for everybody. Somebodys ox is going to get gored.

If I have one suggestion, it would be to implement the large changes over three or four years and let businesses adjust.

Energy: The Obama administrations heavy-handed environmental regulations are a major impediment to US energy independence. Trump can change many of them quickly, because they came in the form of executive orders and rulemaking that doesnt require congressional approval. Ill be watching to see if the new administration approves more natural gas export terminals and pipelines, which will both create jobs and help reduce the trade deficit.

Trump can also approve some of the Arctic and offshore drilling projects that Obama would not consider. I am told that there are some $50 billion worth of oil-production projects that are ready to go, which would be a massive source of high-paying jobs.

If he wants to play hardball with OPEC, Trump could even impose a tariff on imported petroleum products that we can produce here (as opposed to the raw crude, especially heavy crudes, that we currently dont produce). That would give domestic producers and refiners a further boost. It would also aggravate the rest of the worlds oil glut.

Sidebar: I read this week from a reliable source that in 2017 it will be 20% cheaper than it was in 2016 to drill the same well in West Texas. I keep telling you that oil production is now a technology business. Im going to do a special letter on that subject at some point, because it is difficult to grasp just how much big data and new drilling technologies have impacted the business. It is not impossible to envision a future in which, not that many years from now, a $30 a barrel oil well will be considered profitable, especially if you can capture the attendant natural gas and ship it around the world.

With the continued improvement in vehicle gas mileage and the overall reduction in the use of oil in the US (which is an ongoing trend), energy independence is no longer a pipe dream.

Economic stimulus: The bond-financed infrastructure program Ive advocated doesnt seem to be on anyones radar, unfortunately. What I hear is mainly a tax-credit privatization program. I suppose that would help, but it wont accomplish the same goals. And it will necessarily be smaller in scope.

We have plenty of shovel-ready projects, or could create them in short order, that would create jobs and simplify trade and travel. Some will not be very profitable in the short run, so they may not happen under a tax-credit scheme. Investors will want to finance toll roads and the like projects that will generate predictable cash flows.

Trade: Import-dependent businesses are on pins and needles right now, hoping the Trump administration doesnt turn toward the kind of protectionism some of the new appointees have advocated in the past. Well see. The president has considerable latitude in this area, so almost anything is possible.

China is the main point of contention. We already see Trump trying to use Taiwan as a bargaining chip. Beijing isnt at all happy about that, but their options are limited. I feel sure we will see some kind of new US-China trade arrangement, but I really dont know what to expect. The stakes here are enormous, so the situation bears close watching.

The appointment of Peter Navarro to oversee American trade and industrial policy has made more than a few of us a little nervous. I simply do not agree with his analysis of the impact of imports on GDP. I think it would make a lot of us on the free/fair trade side of the fence a lot more comfortable if somebody like Larry Kudlow is appointed chairman of the Council of Economic Advisors. He has been rumored for the job for about three weeks, but Trump has not pulled the trigger. (I know, I know, Larry does not have a PhD. But he is more than qualified. But if not him then somebody who has the same views, as a balance to Navarro.)

For the record, I explicitly agree with Stephen Mnuchin, who says he prefers to do bilateral rather than regional trade agreements. Trump should appoint 25 trade specialists and assign them to different countries and put them on planes within a few weeks of his inauguration. Trying to get agreement from 14 to 20 countries that all have competing interests makes any trade document so unwieldy that it ends up looking more like managed trade than free trade or fair trade. Not every country will want to get involved, but Ill bet you a lot will.

Obama threatened the United Kingdom that if it left the EU it would fall to the back of the line as far as US is concerned in trade deals. Trump and Mnuchin say the UK will always be at the front of the line. Negotiations on a new trade agreement should start now so that it can be ready to sign as soon as possible.

Banking: One reason the stock market has gone bananas since the election is the prospect of banking deregulation. Wall Street has been chafing under the Dodd-Frank Acts requirements and restrictions. The Volcker Rule on proprietary trading has clearly worsened bond market liquidity and taken a major revenue center away from the banks. I am not so worried about the revenue source, but there will always be another crisis in the future. Right now, liquidity in the bond markets can dry up in a Wall Street second much faster than it would have done in the past. The banks really did provide liquidity, which is a useful item (as opposed to high-speed trading, which should be reined in as soon as possible).

Worse, the Dodd-Frank Act as presently constructed could actually aggravate matters if we find ourselves in another financial crisis. Dodd-Frank prevents the Federal Reserve from stepping in with liquidity and instead says that the FDIC should resolve any failing banks. I see the point, but the main reason we have a central bank is to provide a lender of last resort to the banking system. The FDIC simply cant act fast enough, nor does it have the ability or the cash to act effectively in a crisis. Congress needs to fix this soon.

Finally, Dodd-Frank puts our regional and small community banks at a massive disadvantage. They get all of the costs and are restricted from their normal activities. Hardly a week goes by that I dont see some fixed-income equivalent return in the high single digits or/low double digits from private businesses looking for cash. These are the types of deals that banks used to do to their considerable profit, and now regulators are restricting what they can do. The deals still get done, or now they are just done in the private sector. I am not complaining about that because I am part of the private sector and from time to time get to take advantage. But the greater good really does require small community banks to be able to function properly. Overhauling Dodd-Frank will be a big boon to entrepreneurs and small businesses and will create jobs.

I am all for serious restrictions on too-big-to-fail banks. I would prefer that they have to increase their capital reserves. But that doesnt describe 99% of the banks in this country, yet we have written rules to make sure the 1%, the largest banks, dont put taxpayers at risk (even while those rules make it more likely that they will be at risk in some future crisis).

Federal Reserve: We should also see at least two nominees to the Feds Board of Governors soon after Trump takes office. He may get a third one if Daniel Tarullo leaves, as some observers expect. He will get to nominate both the chair and vice chair next year, and it is likely that the remaining members will think about leaving as well when Yellen departs. But the early nominees will tell us a lot about Trumps priorities and long-term plans hopefully for the better. (I do hope that Richard Fisher is on the very short list for Fed chair and that Dr. Lacy Hunt is in line for one of those board seats.)

Meanwhile, the Fed is in the middle of a long-overdue policy turn. Theres still a risk that they will find they started tightening just in time for a recession, which is also long overdue. I was convinced last summer that they would push rates negative in that scenario. Negative rates could yet happen, but I think they will be less likely if the FOMC abides by their dot plots and raises rates three times this year. And I find it difficult to believe that a Trump-appointed Fed would take us into negative rates. We are going to have to find more creative ways to do things.

Wall Street is actually fine with higher rates, by the way. Yes, hiking at the short end raises their cost of funds a bit, but long-term rates have jumped even more. That results in a steeper yield curve and makes lending more profitable for banks.

Surprises: Black swans arent a risk limited to the world of finance; they happen in politics, too. George W. Bush had no idea that September 11 would hit less than eight months into his presidency. God forbid we get something like that again, but a similarly unforeseen crisis is possible and maybe even likely in 2017. Such an event could push aside all the best-laid plans and change everything.

Canadian Bubble

Our neighbors to the north are at their own turning point. The Canadian economy was riding high in the commodity boom but has run into problems after two years of sharply lower oil prices. Since then Canada has avoided recession but has not enjoyed much growth, much like the US. I should point out that Canada is by far our biggest trading partner.

Canada also has a housing bubble that looks increasingly ready to pop. (Then again, Ive been saying that for three or four years.) Home prices in Vancouver are unbelievable, and Toronto is not far behind. These prices have little to do with oil and everything to do with Hong Kong Chinese and other Chinese buying property. Wealthy Chinese, eager to evade their own countrys capital controls, are buying homes as offshore savings accounts. What look like astronomical prices to us are still attractive to Chinese buyers, especially if they believe (and I think with good reason) that their own currency is likely to drop relative to the US dollar over the coming years .

What happens in Canada will tell us something important about China and vice versa. Anything that keeps Chinese money from leaving the country will raise the odds of Canadas bubble popping.

US energy policy matters to Canada, too. The countrys huge oil sands deposits would help its export balance, but in some cases the best access requires pipelines through the US, like the Keystone that Obama has held up. Trump can help Canada by letting that project go forward. We should find out fairly soon if he will.

Crowded Exits in Europe

I thought there was a good chance the Italian bank crisis would come to a head in 2016. The Italians seem to have yet again delayed the inevitable. Reality hasnt fundamentally changed, though. Monte dei Paschi and the other troubled institutions are not going to get better on their own, nor is the new government going to miraculously gain public confidence.

Monte dei Paschi has at least 36% of its loan portfolio in the nonperforming category. The Italians have raised 20 billion for a bank bailout fund, but there is serious doubt that will be enough to cover Monte dei Paschi alone. My friend George Friedman says Goldman Sachs estimates that successful recapitalization would require 38 billion, while a senior market analyst at London Capital Group suggests the number might be closer to 52 billion. And that is just one bank.

Saving Italian banks will take multiple hundreds of billions of euros, which Italy does not have, nor do they technically even have the legal right to unilaterally bail these banks out. They would have to utilize an ECB facility that does not now exist to get that much money, and such a measure would require German approval. By the way, individual Italian investors and savers have invested at least $200 billion in junior, well-subordinated debt that paid a higher yield than bank savings accounts do; and they were told the investment was safe. Think about what would happen if $1 trillion disappeared from the savings of retirees in the US, and then double that number and youll be getting close to what the equivalent impact would be. Think thats politically possible?

I keep telling you that Italy is the most dangerous economic issue on the world front. Attention must be paid.

That said, Europe is quite capable of staving off disaster. They are professionals at that. They can do it again this time if nothing else goes wrong. Thats a big if.

In the something else category, start with political pressures. France and Germany will both hold elections in 2017, with populist parties itching to take charge. I dont think they will succeed in either country, but the price of holding them off could be high. Merkel may have to surrender her wish to accept more Middle East refugees. The refugee flow will not stop, though. People will instead pile up in Italy, Greece, and Turkey, all of which have their own serious problems. And Merkel is not going to want to acquiesce to Italian demands for relief on its banking issues prior to the German election in September.

Further north, it looks like the UK will formally begin the Brexit process in 2017. Implementation will consume energy and resources that the EU really needs to devote elsewhere. Also, the closer the UK gets to actual withdrawal, the more pressure other countries will face from their own anti-EU parties. The arguments against EU withdrawal will weaken considerably once the UK pulls the trigger without world-ending consequences.

Then theres NATO. The defense alliance partially overlaps with the EU but also includes Turkey. Trump wants the other member states to increase their defense spending. He says, correctly, that they arent paying their fair share and has openly questioned whether the US would come to their aid in an attack. The Baltic countries and Poland are very concerned, as they are the most exposed to potential Russian aggression.

Does Putin intend to attack and try to occupy one of those countries? Think Afghanistan. I really rather doubt he will, but he can cause all kinds of problems without attacking. Fear alone is sufficiently troublesome. Meanwhile we have President Obama, despite his being on the way out the door, imposing new sanctions on Russia for alleged hacking activity. And we see Russia and Turkey actually growing closer after the assassination of the Russian ambassador in Ankara last month.

As with Italy, though, fear has consequences. Leaders can juggle only so much. When too many things happen at once, the risk rises that someone will drop a ball.

Asian Angst

Relationships within Asia are in flux, to say the least. Trumps phone call with the Taiwanese president and subsequent comments show hes willing to roll back prior commitments in order to get better ones. Beijing was not pleased, to put it mildly, but I dont see this as a crisis. I suspect Trump intermediaries are already working quietly on new deals with China. We could see some major changes in 2017.

China has other problems, too. They are holding the domestic economy together with astonishing amounts of debt. New liquidity cant leave the country due to capital controls, but it has to go somewhere. The result is rolling asset bubbles that make even Vancouver housing prices look flat.

The transition from an economy driven by exports to one led by domestic demand is probably going as well as it can, but thats not saying much. The process may accelerate if Trump has his way. This is one area where I fully expect him to follow through on the rhetoric. It will look crazy, but crazy with a purpose. The hard part will be giving the Chinese leaders a face-saving way to accept the demands without causing domestic instability. I am not sure Trump fully appreciates that side of it. Either side could miscalculate and set off a bad reaction.

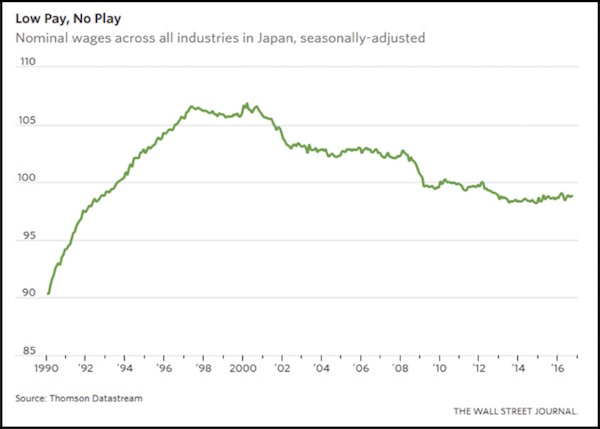

Over in Japan, something interesting is happening. The job market is unbelievably tight. I saw in a Wall Street Journal report last week that each available worker has two job offers on average. The unemployment rate is historically low. In a normal market, you would expect employers to compete for workers by raising wages, right? But it isnt happening. Wages are flat or even falling.

Japans culture and some unique labor policies partly explain this, but I think the situation really shows how hard it is to escape a deflationary spiral. Deflation has changed the psychology for two generations of workers and managers. Employees are afraid to demand more, and companies are afraid to pay more.

Its also a potentially ominous sign for the US. The Fed and many others are watching labor markets closely for signs of wage inflation. Rising wages are one of the factors that would justify tighter interest-rate policies. Yet Japan shows that unemployment can stay low for years without necessarily causing wage inflation. The BOJ would probably love to see some, but they arent getting it.

Japan is another potential target of Trumps trade policy. Unlike China, Japan really is devaluing its currency. The policy is working, too, in terms of promoting exports. But those exports dont all go to the United States. Japan sells China much of its industrial equipment and technology, demand for which will presumably drop if Trump succeeds in reducing Chinese exports.

(And while we are talking about currencies that are devaluing against the dollar, lets note that the British pound is down 40% and the euro is down about 35%, and I dont think it will be much longer before the euro is at parity with the USD. Are we going to declare those countries currency manipulators? Chinas small currency drop is meaningless by comparison. And if China were to float its currency? My bet is the renminbi would drop by another 25 to 30% almost immediately. So much for free markets

)

While were talking about Asia, I have to mention Indias paper-money crackdown. Prime Minister Narendra Modi has been trying hard to control the countrys very large underground economy. In November they did an overnight cancellation of the two largest-denomination paper bills, giving people until Dec. 30 to deposit them in a bank account before the paper became worthless.

The problem, of course, is that hundreds of millions of Indian workers dont have bank accounts. The result, at least according to news reports, has been nothing short of chaos in some places. Normal commerce simply ground to a halt. People have been existing on barter and IOUs. The debacle may cost India a point or two or more of GDP growth, according to some estimates.

Worse, it may not have even accomplished the original goal. The theory was that people hoarding large amounts of cash would be afraid to turn it in, and it would simply become worthless. That would teach them, Modi must have thought. But now it appears that almost all of the cash returned to the banking system. That means the black market was not as large as the government thought, or people found other ways to launder their cash.

I explain all that to make an important point. Government mistakes are a top risk factor now. I think Modi had good intent. Im sure the government planned the operation as well as it could. They were attacking what they thought was a real problem with what seemed like a reasonable plan (at least to them). But it still didnt work and might even have caused additional damage.

Imagine the damage a similar-scale policy error could cause in the US. We have an incoming government that will likely try things no one has ever tried before. We have a Federal Reserve that needs both to raise interest rates and to reduce its bloated balance sheet. We have all kinds of international challenges. I havent even mentioned Africa, the Middle East, Australia or Latin America. They all hold potential problems for the global economy, too.

We enter 2017 with more question marks than I can count. Even if all the policymakers are competent and have good intentions, stuff happens. Things go wrong. People dont react the way you think they will. You end up causing more problems for the people and businesses you wanted to help.

I have full confidence in the ability of US business to produce quality products and services at fair prices. Ditto for many other countries. Their decisions are not what we need to worry about. Now more than ever, economic risk around the world emanates from our governments and central banks.

I was with Steve Forbes the other night in New York. He asked me how I was feeling and gave me a list of about seven adjectives. I told him that I was skeptically optimistic. He laughed and said thats probably the right position. I have not been happy with the bulk of what has come out of Washington DC for the last 16 years.

Trump has the traditional 100 days to deliver something to keep the optimism going. Hopefully, a Congress that is nominally Republican controlled can agree on important measures and move more quickly than we have seen it move in quite a while. But then New Years Day is a moment for optimism and hope. Thats how well end this letter; and next year that is, next week Ill have my own economic and market forecast for 2017 for you.

DC, Florida, the Caymans, and a Few Final 2016 Thoughts

Tonight I will celebrate New Years Eve with close friend David Tice of Prudent Bear fame, who is getting married to his new wife Sophia in a few hours. It should be quite the New Years Eve party. Then Shane and I will be in Washington, DC, for the inauguration. I am on the board of a public company called Ashford Inc., which manages hotel REITS, among other things. We own several hotels in DC, including the Capital Hilton, and our chairman and my good friend, Monty Bennett, decided we would move our board meeting up a few weeks and hold it in Washington during the inauguration. I will get to see a lot of friends and of course will be at the huge Texas inaugural ball, called Black Tie and Boots, on Thursday night (if you are there or in DC, lets meet) and am still looking for tickets for an inaugural ball on Friday night.

We will go straight from DC to the Inside ETFs Conference in Hollywood, Florida, January 2225. If you are in the industry and coming to that conference, make a point to meet with me. Mauldin Solutions (my investment advisor firm) will have a booth at the conference, where I will try to hang out some. If you are an independent broker advisor in the area, make a point to come by and see me. I will be making some big announcements at the conference. Then I'll be at the Orlando Money Show February 811 at the Omni in Orlando. Registration is free. I am also scheduled to speak at a large hedge fund conference in the Cayman Islands February 14 to 18.

During the last week of the year, I always end up thinking about what my next five years will look like. Ive been doing that since I was 22 and leaving Rice University with a freshly printed sheepskin. I have had 45 opportunities since to analyze how effective and accurate my five-year planning is. So far Im 0 for 45. Thats right. A guy who makes his living as an analyst and forecaster has never been able to accurately predict his own life, the one thing that he theoretically has under control. Not even once! I actually get the general direction right about half the time, which I suppose is not too bad. Well, and thats with a pretty broad definition of direction. That said, while I would have preferred to avoid a few bumps, I am pretty happy with where I am. Not too bad for a poor country boy from Bridgeport, Texas.

There have been only a few times when I was not optimistic about the coming year, and thankfully this is again one of the optimistic times. Im actually as pumped as I have been in a long time. I have been hinting that I will have a new portfolio construction concept ready to share with readers for some time always at some vague time in the future but now I can begin to narrow the date when everything should be ready for prime time to sometime in the middle of March. I have quietly been assembling an all-star cast of partners and team members.

I have lost some good friends this year. Age and disease can be a bitch. These people were all planning to keep working for a long time; then things changed. That has made me a little more reflective, but it is not changing my attitude. At 67 I am launching a business that will require at least a 10-year commitment to my partners and future clients. It will require even more travel time than I put in now. I was in the gym this morning with The Beast, trying to keep this body together and working. I say this every year at this time, but this year I mean it: I am honest to God going to get in real shape this year. I am already starting to change my lifestyle a little bit, acknowledging that perhaps I cant do some of the things that I did when I was 30 and 40. But that doesnt mean I cant do everything I can do today and more tomorrow with what I have. I know that more than a few of my readers share that attitude. We are just having too #$%$ much fun to want to go sit on the porch and watch the world go by.

A little tease: I think core portfolios, the way they are designed today, are going to be in for very difficult 5710 years, so my partners and I have been rethinking a better and smarter way to do core portfolios. Cheaper, better, faster-acting and reacting. Something that can work not only for accredited investors but for average investors and for those who are overseas as well. The problem, from my standpoint, is that I have to be ready to handle all the responses to our program, and do so efficiently and capably, from day one. The user experience must work seamlessly. That doesnt happen without a lot of planning and a very experienced team.

What we are doing with portfolios today was not even possible five years ago, and what we are planning to do in five years is not yet possible today. This will not be your fathers portfolio construction model. Going to the sidelines is not an option, because you cant grow your portfolio if youre not involved in the markets. But nobody says you have to endure massive bear markets and huge changes in asset classes passively.

2016 has been a year of major surprises. Frankly, I think 2017 has the potential to offer even more challenges than 2016 did. When I sit with my friend George Friedman and talk about the geopolitical changes that are brewing, I realize that politicians are getting ready to be bigger players in the market than they should be. But we dont get to choose the times in which we live. Our choice is how we live them.

One thing I can predict: Barring some physical challenge, I will still be writing this letter for free for a long time to come. It is my passion and joy. I feel a connection with each and every reader every time I hit the send button or when I meet you and we talk and share our lives. I try to read every comment that comes back and answer some of them directly, and some questions and comments become topics for letters. My partners tell me we have some 70,000 new email addresses this year, so welcome to the family. And feel free to tell others to join us. The next 20 years are going to be the most hellaciously fun time of any period in history. And we are all going to have a front-center-row seat. To paraphrase another media outlet: I write. You decide.

Thanks for being with me and making 2016 such a great year. I will be traveling a lot more this next year, hopefully to a city near you where we can share a few thoughts. Let me give you my sincere and heartfelt wish for a wonderful and happy new year!

Your raring to start the new year analyst,

John Mauldin

subscribers@MauldinEconomics.com

| Digg This Article

-- Published: Monday, 2 January 2017 | E-Mail | Print | Source: GoldSeek.com