-- Published: Tuesday, 3 January 2017 | Print | Disqus

By Michael J. Kosares

Reversal, resurgence and renewal on the road to the new year

Quietly, while all attention was riveted on the U.S. election, gold made a notable comeback in 2016. The gain was not spectacular at 8.7%, but it was respectable, and it came after three straight down years. (Silver had an even better year with a 15.2% gain.) In addition and perhaps even more importantly, global investment demand registered its fourth largest increase since the 2011 post-crisis peak. That resurgence suggests that down years for gold did not temper the global inclination to own it. To be sure, these numbers in tandem represent an important turnaround for gold and a break from the near-term past. It is also perhaps the first hint that we may have turned the page from the corrective phase of cycle to resumption of the long-term secular bull market for both gold and silver.

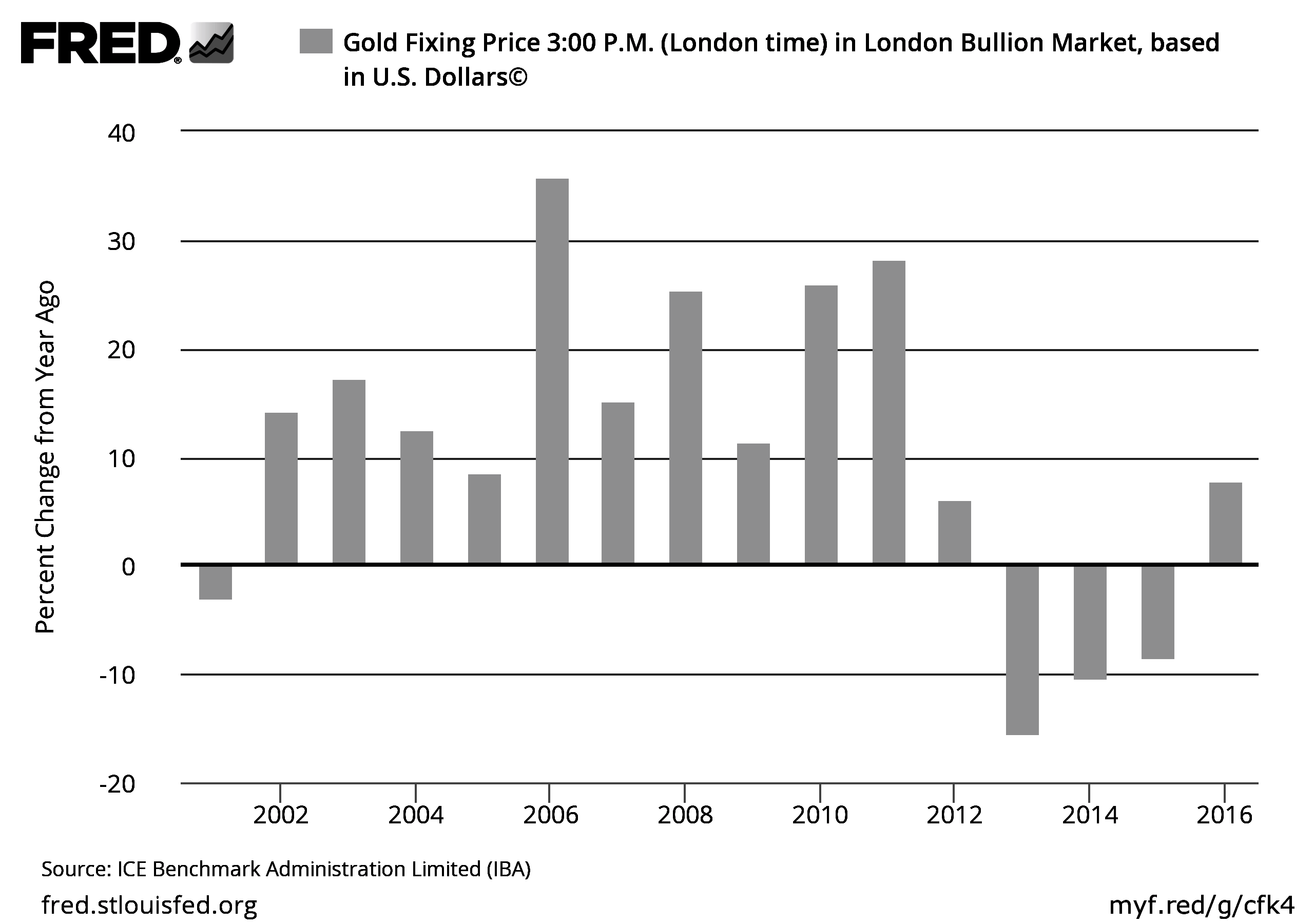

Gold has averaged a 12% annual gain since 2002

Gold has posted gains twelve of the last fifteen years under decidedly disinflationary circumstances. Since the turn of the century, gold has averaged a 12% gain annually, even after the negative returns in 2013 through 2015 are blended into the calculation. That, by any measure, is an impressive track record and one that should be taken into account by anyone interested in prudent wealth management and effective portfolio design with the longer-term in mind.

In the years 2013-2015, gold experienced a healthy, some would say necessary, secular bull market correction. In 2016, the downtrend was broken with a fresh 8.7% gain, perhaps setting the stage for the next leg of the secular bull market. In future years, gold owners may look back at 2016 as an important turnaround year.

According to a Bloomberg survey of twenty-six analysts, gold will rally 13% in 2017. The gold big trading banks are generally optimistic about the price of gold for 2017. Here is a partial list of predictions:

UBS $1,350.00 HSBC $1,440.00 Bank of America/Merrill Lynch $1,200.00 Credit Suisse $1,338.00 ABN Amro $1,425.00 RBC Capital $1,500.00 Citibank $1,160.00

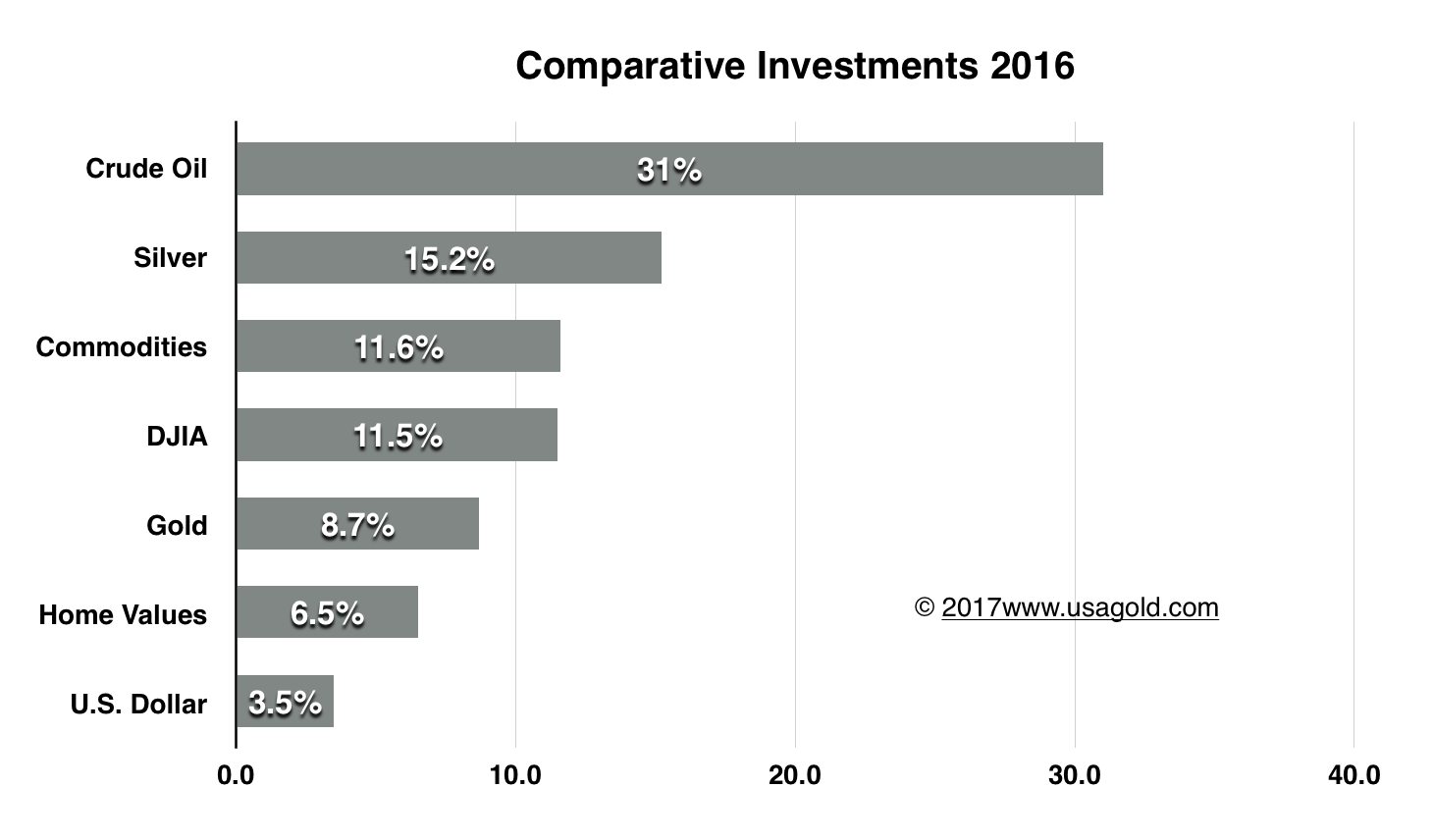

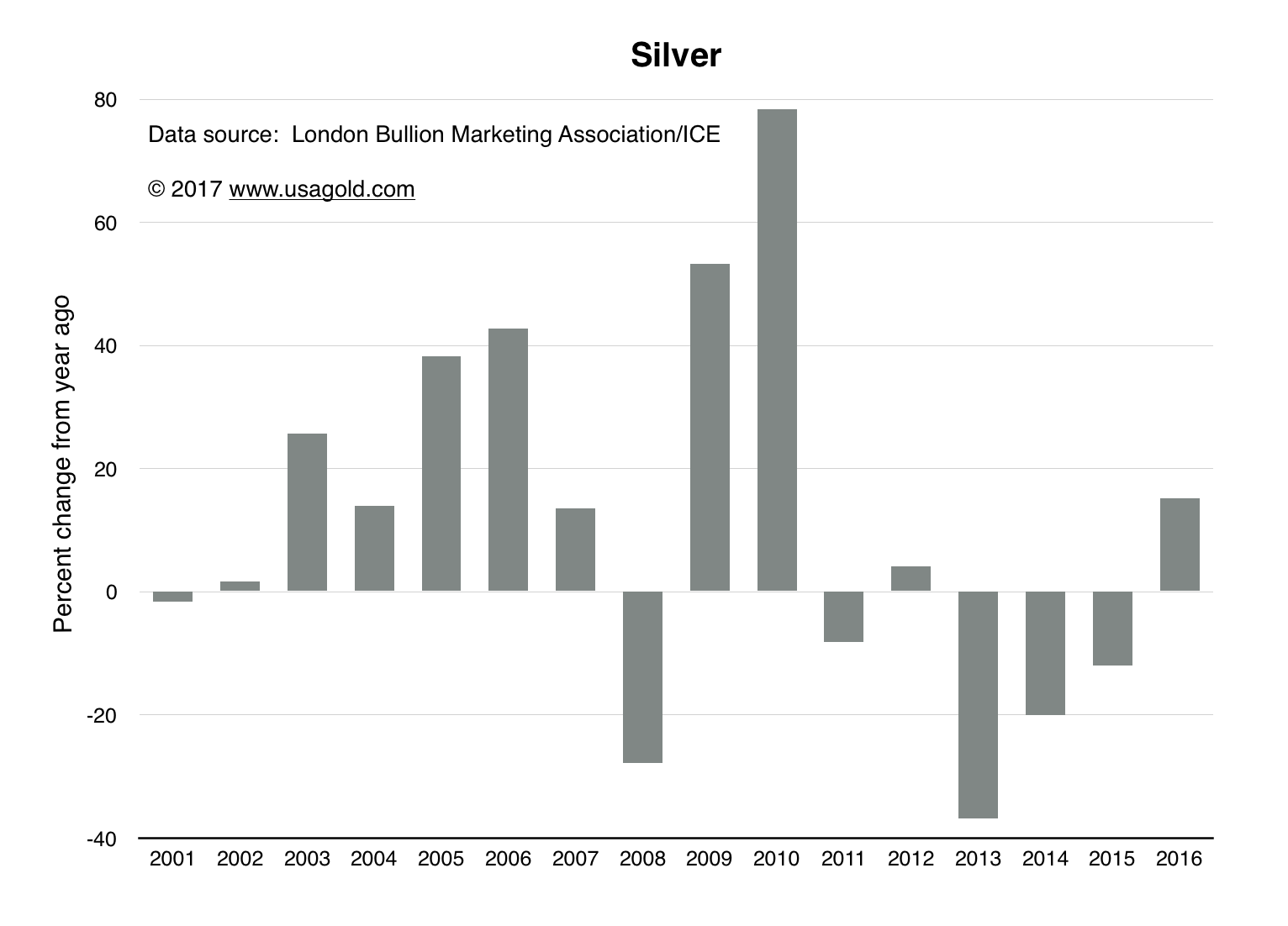

Silver a standout in comparative investment performance for 2016

After all was said and done. . . . .and after everything had been stacked and counted, the chart above shows the final tally on the primary investment markets for 2016. As you can see, silver finished second to runaway oil prices in the year's comparative investment sweepstakes up 15.2% in 2016 even after the sharp year-end correction. It outperformed gold which gained 8.7% and stocks which gained 11.5%.

Silver investors, we know from direct experience working with our clientele, view silver as a safe-haven alternative to gold with the added bonus of stronger upside potential (Experience also tells us it also has stronger downside potential. Please see chart below.) Silver sales at USAGOLD have steadily and markedly climbed year over year the past few years and we suspect that sales will be strong at the start of 2017 due to the currently low price level at around $16 per ounce. Last summer we experienced a strong increase in investor interest at the $16 to $18 price level. Then prices jumped to near $21 before correcting into the end of the year.

One of the more interesting developments to surface over the course of 2016 was the strong growth in silver demand from India. Indian investors are concerned that their government will impose import and capital controls on gold, perhaps even ban it. As a result, some investors are switching to silver as a hedge against currency debasement. Silver, as a result, has become to a certain extent, as India's Economic Times suggested recently, the new gold in that country.

Commodity experts and bullion traders," says Economic Times, "feel that silver can trump gold in coming months as demand for the metal is increasing for solar panels and electronics sector. Demand for silver is increasing in the home décor and fashionable jewelry categories in the country which may push the price of the metal by almost 15-20% in 2017, feel the traders and analysts.

If even a small amount of Indias massive gold interest were to migrate to silver, it could cause supply disruptions and premium increases here in the United States. We have seen before the hair trigger relationship between ramped up physical demand and premium increases. The physical silver market globally in terms of availability is not nearly as deep and liquid as gold, and a heavy source of new demand could become problematic.

(Data sources for 2016 gains: Bloomberg Commodities Index, Zillow Home Value Index, U.S. Dollar Index, Brent Crude Oil, Dow Jones Industrial Average, Gold Spot Forex, Silver Spot Forex)

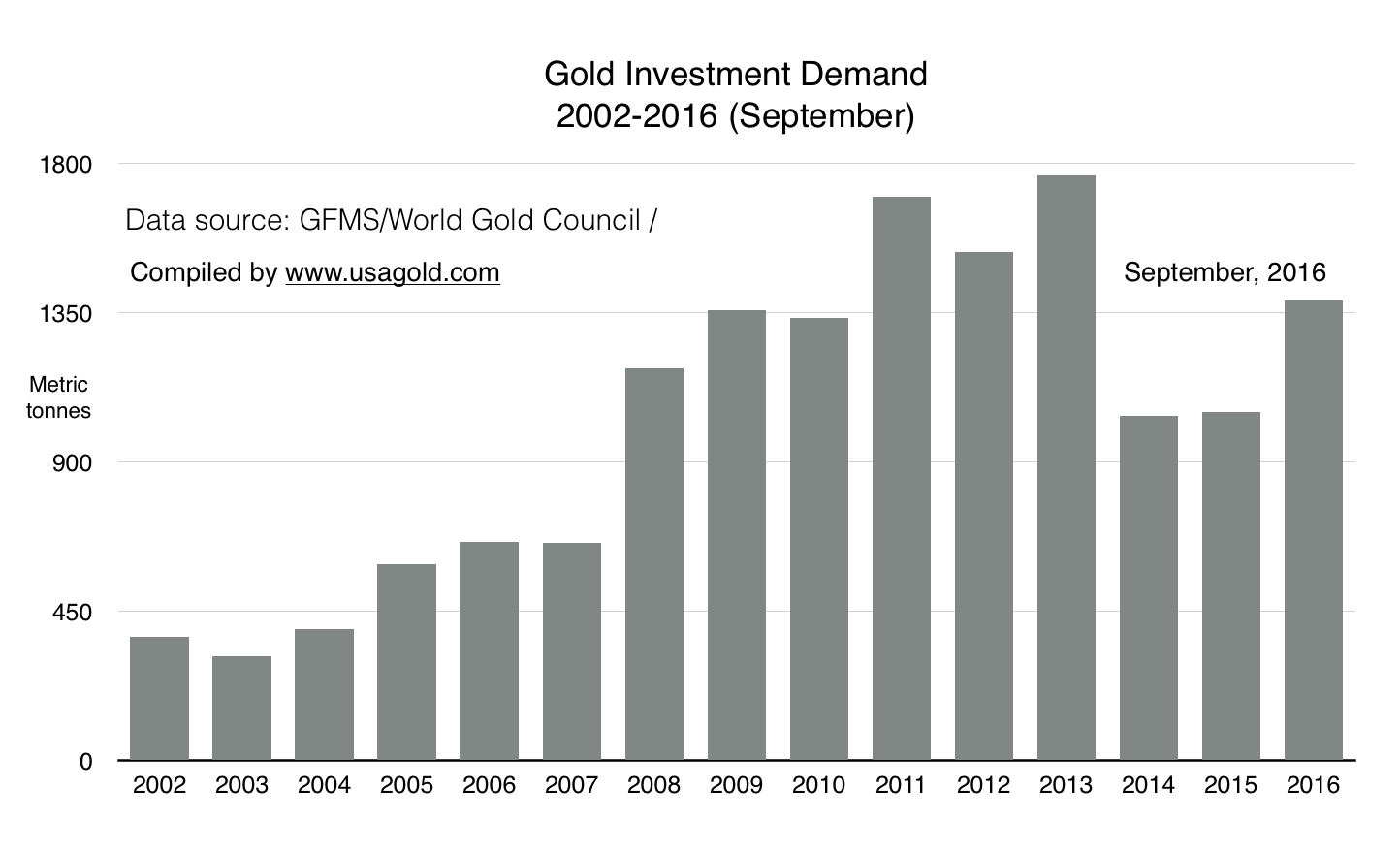

Gold investment demand's 2016 resurgence, what it means for 2017

One of the more important developments over the past year has been the quiet resurgence of gold investment demand on a global basis. At 1390 tonnes, investment demand now represents an impressive 58% of mine production and 42% of overall demand. Investment demand is driven by events and there is much with investors will be concerned as we move into 2017. "The only way to prepare for a world of uncertainty," says Financial Times' Gillian Tett, "is to stay as flexible and diversified as possible. Now is not the time for investors to put all their eggs in one basket, or bet on just one asset class. Nor is it a time for businesses to be locked into rigid business plans; political and geopolitical upheaval could strike almost anywhere." Tett finds herself among a vanguard of analysts voicing similar warnings for the new year.

With so much uncertainty on the table, the gold investment demand juggernaut is more likely to gather pace in 2017 than slow down. It is important to note that gold demand scaled new heights in the post 2007-2008 environment and stayed there. In that context, this year's resurgence in demand after two subdued years, and under comparatively benign economic circumstances, is worth noting. It signals the potential for surpassing past performances by a wide margin the next time an economic storm rolls over the horizon something investors yet to hedge their portfolios should keep in mind.

Algo trading creates buying opportunities for long-term gold investors

Algos cannot peer around the corner. There is no rationale for their function other than what its programmers have fed into the governing equation. Thus, if the algo says sell gold when the dollar rises, it sells gold when the dollar rises. It doesnt stop to think that the dollar is rising in a milieu of crashing currencies globally and the potential consequences. It doesnt stop to consider that it will take months for the Trump administration to get a tangible, workable economic program through the Congress, and then months more for the program to have an effect on the overall economy. Such critical thinking is left to the rest of us who are not tethered to computer trading programs.

Along those lines, we are reminded that the computerized polling prior to the election was also algo-based, and you see where that got those who believed the polls to be reliable. Surprise! We missed something! So it is that buying opportunities are created in the gold market (and betting opportunities for those who like to gamble on elections). Some consider such opportunities a gift. As you can see by the top chart, there is a cadence to the market action upsides are followed by downsides, downsides followed by upsides. When you zoom out and look at the dollar index chart over the long run, here is what it looks like:

As you can see in the chart below, even in a world of generally declining fiat money across the spectrum of currencies, the dollar is in a long-term downtrend and gold is in a long-term up trend. The dollar appears to be enjoying a secular bear market rally and gold appears to be suffering a bull market correction. What that tells the longer-term gold owner about the todays pricing in a nutshell is that gold might be a good buy at current prices. Its all a matter of perspective. . . .that and the courage to act on ones convictions even in the prototypical euphoric period just following a presidential election.

As our regular readers will attest, we tend to shy away from predicting short-term price movements for gold. At the same time, we cannot help but take note of one trading pattern worth passing along to our clientele. We caution from the outset that just because gold has displayed a pattern in the past, it does not mean that same pattern or tendency will repeat itself in the future, so exercise due caution with this information.

Since 2013, gold has fallen into a pattern of declines in the second half of the year followed by recoveries during the first half of the succeeding year. The second half lows range from $1050/oz to $1150/oz, and the first half highs range from $1300/oz to $1450/oz. In each instance, the lows were posted in December. In 2016, gold posted its low for the second half in mid-December at $1128/oz. It is also worth noting that the recovery tops fall in line with the price predictions for 2017 posted by many of the gold trading banks (see top of page).

There's an old saying in the business realm that if you watch the pennies the dollars will take care of themselves. Likewise, if you build your portfolio on solid principles for the long-run, you will be well-positioned should the short run provide benefits. The best analysis, it follows, concerns itself not with what is likely to occur in the coming 365-day period (although it can be somewhat helpful), but with societal issues that will have a lasting impact on the political economy.

Along these lines, it has become a custom in News & Views to annually post an update of Neil Howe's in our Gold Owners' Guide to the New Year. Howe is the co-author (along with William Strauss, now deceased), of The Fourth Turning the remarkable and prescient analysis of generational cycles that first hit the bookstores in 1997. These generational cycles play out over long periods of time though their effects register consistently and on an on-going basis in the financial markets.

Consider the following passage from The Fourth Turning and keep in mind that it was written at a time when the stock market was bumping along all-time highs driven by a technological revolution and the illusion of a perfectly balanced Goldilocks economy some analysts promised would last a lifetime:

"The next Fourth Turning is due to begin shortly after the new millennium, midway through the Oh-Oh decade. Around the year 2005, a sudden spark will catalyze a Crisis mood. Remnants of the old social order will disintegrate. Political and economic trust will implode. Real hardship will beset the land, with severe distress that could involve questions of class, race, nation, and empire."

Predictions like that one of the more remarkable in recent memory have a way of building credibility. In 2013, Neil Howe publicly proclaimed that the financial crisis which had its start in 2007, and in which we still find ourselves immersed today, was indeed the Fourth Turning he and Strauss had predicted.

At the end of this past December, Howe was asked where we stand now along the Crisis timeline and this was his response:

"[W]e're still not halfway through yet and I think there's a lot more history to come, a lot bigger history. Because history suggests that Fourth Turnings are creative destruction in the public sector and the institutional sector, in political and economic institutions. We're likely to see things get worse before they get better."

Since a Turning, according to Howe, lasts roughly twenty years, the end of this one would take us at least midway into the 2020s before we cross the line to a new societal and economic era. Howe puts it this way: "You are not just into it and out of it immediately. . .It is a season you have to move through before you are born again, so to speak, as a society, and regain institutional confidence. You have go through the crucible to get there."

In other words, a lot of water will run under the bridge between now and a return to the highs of the First Turning the last of which encompassed the Truman, Eisenhower and Kennedy administrations. It is no accident, I might add, that gold's secular bull market which began in 2002 has coincided with the great societal and economic upheavals described in The Fourth Turning.

Michael J. Kosares is the founder of USAGOLD and the author of "The ABCs of Gold Investing - How To Protect and Build Your Wealth With Gold." He has over forty years experience in the physical gold business. He is also the editor of News & Views, the firm's newsletter which is offered free of charge and specializes in issues and opinion of importance to owners of gold coins and bullion.

Disclaimer - Opinions expressed on the USAGOLD.com website do not constitute an offer to buy or sell, or the solicitation of an offer to buy or sell any precious metals product, nor should they be viewed in any way as investment advice or advice to buy, sell or hold. USAGOLD, Inc. recommends the purchase of physical precious metals for asset preservation purposes, not speculation. Utilization of these opinions for speculative purposes is neither suggested nor advised. Commentary is strictly for educational purposes, and as such USAGOLD does not warrant or guarantee the the accuracy, timeliness or completeness of the information found here.

The content on this site is protected

by U.S. and international copyright laws and is the property of GoldSeek.com

and/or the providers of the content under license. By "content" we mean any

information, mode of expression, or other materials and services found on GoldSeek.com.

This includes editorials, news, our writings, graphics, and any and all other

features found on the site. Please contact

us for any further information.

Live GoldSeek Visitor Map | Disclaimer

The views contained here may not represent the views of GoldSeek.com, Gold Seek LLC, its affiliates or advertisers. GoldSeek.com, Gold Seek LLC makes no representation, warranty or guarantee as to the accuracy

or completeness of the information (including news, editorials, prices, statistics,

analyses and the like) provided through its service. Any copying, reproduction

and/or redistribution of any of the documents, data, content or materials contained

on or within this website, without the express written consent of GoldSeek.com, Gold Seek LLC,

is strictly prohibited. In no event shall GoldSeek.com, Gold Seek LLC or its affiliates be

liable to any person for any decision made or action taken in reliance upon

the information provided herein.

There's an old saying in the business realm that if you watch the pennies the dollars will take care of themselves. Likewise, if you build your portfolio on solid principles for the long-run, you will be well-positioned should the short run provide benefits. The best analysis, it follows, concerns itself not with what is likely to occur in the coming 365-day period (although it can be somewhat helpful), but with societal issues that will have a lasting impact on the political economy.

There's an old saying in the business realm that if you watch the pennies the dollars will take care of themselves. Likewise, if you build your portfolio on solid principles for the long-run, you will be well-positioned should the short run provide benefits. The best analysis, it follows, concerns itself not with what is likely to occur in the coming 365-day period (although it can be somewhat helpful), but with societal issues that will have a lasting impact on the political economy.