-- Published: Thursday, 9 February 2017 | Print | Disqus

By John Mauldin

Longtime readers of Outside the Box know that I am a fan of Dr. Lacy Hunt of Hoisington Investment Management. Lacy and his partner, Van Hoisington, produce a quarterly letter that is a must-read for me, as it reliably informs my thinking in a world drowning in conventional economics economics that seem to continually miss the mark.

It almost goes without saying that Lacy will be speaking at our Strategic Investment Conference again this year, and hes just one of a long (and still-lengthening) list of top-flight speakers. Learn more and reserve your chair, right here.

Todays OTB is one of the most important pieces Van and Lacy have written in a long time. They establish that the proposed tax reforms will face enormous headwinds that were not there during previous tax-reform eras, which means that the benefits that Republicans think will accrue are likely to take longer to appear and be less than expected, which will mean that it is going to take more than what is presently proposed to jump-start the economy.

A few readers have asked me whether I am still a deficit hawk. The answer is, Yes, more than ever, because total debt has now rendered both monetary and fiscal policy much less effective. Debt, as Lacy and Van clearly show, is an impediment to growth.

There are other issues impeding growth, such as the ten million men between ages 24-64 who are not in the work force, a condition that has been steadily worsening for 40 years. Its not just a recent phenomenon, but it must be addressed. These are men who have chosen to not participate for one reason or another and are perforce a drain on overall GDP growth.

And lets not forget that for the last nine years we have seen more businesses close than be created, which has certainly affected GDP.

Tax reform is fine, but far more structural change is necessary if growth is to return. I will be writing on that topic over the next few weeks. But today we appreciate the work of Lacy and Van.

I find myself writing this introduction on yet another plane on my way to speak at the Orlando MoneyShow. If things work out, I will have dinner with Larry Kudlow, and I hope Art Laffer makes it as well. Ill test out some of my recent ideas on them.

This week in Thoughts from the Frontline Ill be looking at the good things (and there are a lot of them) in the proposed tax reforms, before we deal with the problems the following week.

Your not trying to miss the forest for the trees analyst,

John Mauldin, Editor

Outside the Box

JohnMauldin@2000wave.com

Hoisington Quarterly Review and Outlook 4Q2016

CHANGE?

The 2016 presidential election has brought about widely anticipated changes in fiscal policy actions. First, tax reductions for both the household and corporate sectors along with a major reform of the tax code have been proposed. In conjunction, a novel program of tax credits to the private sector has been discussed to finance increased outlays for infrastructure. Second, provisions have been suggested to incentivize domestic corporations to repatriate $2.6 trillion of liquid assets held overseas. Third, there is talk of regulatory reform along with measures to increase domestic production of energy. Finally, various measures related to international trade have been discussed in an effort to reduce the current account deficit.

Judging by sharp reactions of U.S. capital and currency markets, success of these proposals has been quickly accepted. Such was the case with the fiscal stimulus package of 2009, as well as with Quantitative Easings 1 and 2; initially there were highly favorable market reactions. In these cases the rush to judgment was misplaced as widespread economic gains did not occur, and the U.S. experienced the weakest expansion in seven decades along with lower inflation. It could be that the fundamental analytical mistake now, like then, is to assume that the economy is an understandable and controllable machine rather than a complex, adaptive system (William R. White, in his 2016 Adam Smith Lecture Ultra-Easy Money: Digging the Hole Deeper? at the annual meeting of the National Association of Business Economists). While many of the aforementioned proposals include pro-growth features, it appears that there is an underestimation of the nega tive impact of delayed implementation and other lags. Additionally, the risks of unintended adverse consequences and outright failure are high, especially if the enacted programs are heavily financed with borrowed funds and/or monetary conditions continue to work at cross purposes with the fiscal policy goals.

Tax Cuts and Credits

Considering the current public and private debt overhang, tax reductions are not likely to be as successful as the much larger tax cuts were for Presidents Ronald Reagan and George W. Bush. Gross federal debt now stands at 105.5% of GDP, compared with 31.7% and 57.0%, respectively, when the 1981 and 2002 tax laws were implemented. Additionally, tax reductions work slowly, with only 50% of the impact registering within a year and a half after the tax changes are enacted. Thus, while the economy is waiting for increased revenues from faster growth from the tax cuts, surging federal debt is likely to continue to drive U.S. aggregate indebtedness higher, further restraining economic growth.

The key variable to improve domestic economic conditions is to cut the marginal household (middle income) and corporate income tax rates. Due to the extremely high level of federal debt, if the deleterious impact of higher debt on growth is to be avoided, then these tax cuts must be expenditure-balanced to the fullest extent possible along with reductions in federal spending (which has a negative multiplier).

Providing tax credits to the private sector to build infrastructure should be more efficient than the current system, but this new system has to first be put into operation and firms with profits must decide to enter this business. Moreover, all the various rights of way, ownership and environmental requirements suggest that any economic growth impact from the infrastructure proposal is well into the future.

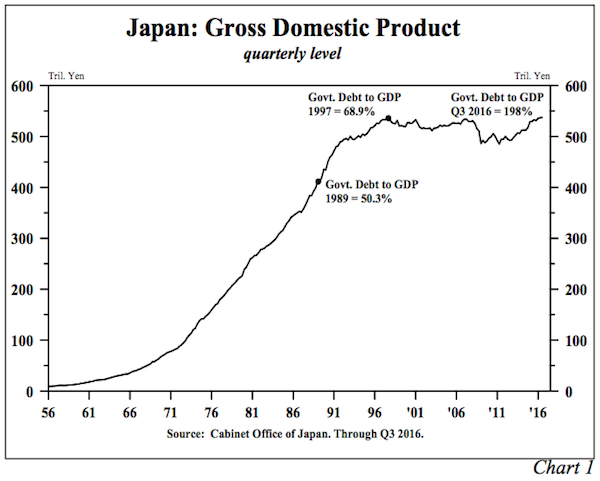

However, if the household and corporate tax reductions and infrastructure tax credits proposed are not financed by other budget offsets, history suggests they will be met with little or no success. The test case is Japan. In implementing tax cuts and massive infrastructure spending, Japanese government debt exploded from 68.9% of GDP in 1997 to 198.0% in the third quarter of 2016. Over that period nominal GDP in Japan has remained roughly unchanged (Chart 1). Additionally, when Japan began these debt experiments, the global economy was far stronger than it is currently, thus Japan was supported by external conditions to a far greater degree than the U.S. would be in present circumstances.

Tax Repatriation

One of the tax proposals with wide support gives U.S. corporations a window to repatriate approximately $2.6 trillion of foreign held profits under the favorable tax terms of 10% or 15%. There is a catch, however. To ensure that all funds are brought home, the tax is due on all of the un-repatriated funds even if only a portion is brought back to the United States.

Several considerations suggest there is no guarantee that these funds will actually be invested in plant and equipment in the United States. First, the fact that they are currently liquid suggests that physical investment opportunities are already lacking. Second, the bulk of the foreign assets are held by three already cash-rich sectors high tech, pharmaceutical and energy. The concentrated and liquid nature of these assets suggests that after an estimated $260 billion to $390 billion in taxes are paid, the repatriated funds will probably be shifted into share buybacks, mergers, dividends or debt repayments. Putting funds into financial engineering will improve earnings per share, further raising equity valuations for individual firms; however, such transactions will not grow the economy. Finally, the basic determinants of capital spending have been unfavorable, and they worsened in the fourth quarter. Capacity utilization was only 75% in November 2016, well below the peak of just under 79% reached exactly two years earlier. The U.S. Treasurys corporate income tax collections for the twelve months ended November 2016 were 13.1% less than a year earlier, suggesting corporate profits eroded considerably last year.

A possible additional negative result of the repatriation is that those assets denominated in foreign currency, estimated to be 10% to 30%, will need to be converted into U.S. dollars. This will place upward pressure on the dollar, reinforcing the loss of market share of U.S. firms in domestic and foreign markets. Tax repatriation was tried on a smaller scale during the Bush 43 administration in 2005-2006 with limited success. A much smaller amount of funds were repatriated, and the dollar showed strength.

Regulatory Reform

Regulatory reform could create increased energy production which would clearly boost real economic activity. This is accomplished by shifting the upward sloping aggregate supply curve outward and thereby lowering inflation. When the aggregate supply curve shifts, it will intersect with the downward sloping aggregate demand curve at a lower price level and a higher level of real GDP. The falling prices are equivalent to a tax cut that is not financed with more federal debt. Regulatory reform is a strong proposal and will benefit the economy greatly, in time, by making the U.S. more efficient and better able to compete in world markets. However, these benefits are likely to build slowly and accrue over time. Without question, the regulatory reform is the most unambiguously positive aspect of the contemplated fiscal policy changes since it will produce faster growth and lower inflation. Since bond yields are very sensitive to inflationary expectations, this program would actually contribute to lower interest costs as the disinflationary aspects of the program become apparent.

International Trade Actions

Proposals to cut the trade deficit by tariffs or import restrictions would have the exact opposite effect of the regulatory reforms and increased energy production. They would shift the aggregate supply curve inward, resulting in a higher price level and a lower level of real GDP. Any improvement in the trade account would reduce foreign saving, which is the inverse of the trade account. Since investment equals domestic and foreign saving, the drop in saving would force consumer spending and/or investment lower. Any improvement in the trade account would be limited since the dollar would rise, undermining the first round gains in trade. The more serious risk is that other countries retaliate. From the mid-1920s until the start of WWII this process resulted in what is known as a deflationary race to the bottom.

IMPEDIMENTS TO GROWTH

Over the past few months interest rates and the value of the dollar have risen sharply, and monetary policys quantitative indicators have contracted. These monetary restrictions have worsened the structural impediments to U.S. economic growth that existed before the election and continue today. These impediments include: (1) a record level of domestic nonfinancial sector debt relative to GDP and further increases in federal debt that are already built-in for years to come; (2) record global debt relative to GDP; (3) weak and fragile global economic growth resulting from the debt overhang; (4) adverse demographics; and (5) exhaustion of pent-up demand in the domestic economy.

Monetary Restrictions

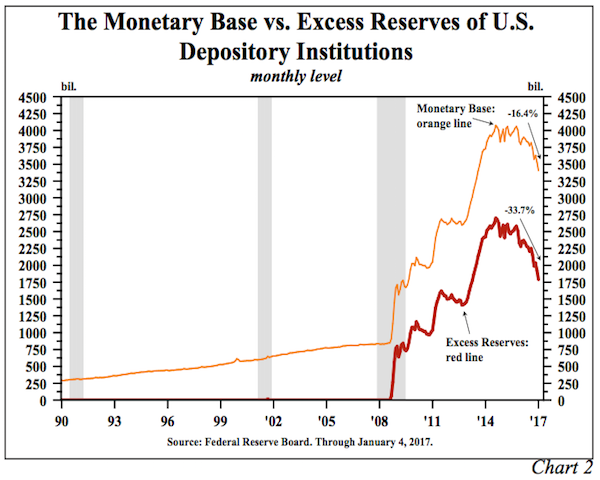

If monetary conditions are tightened and interest rates continue to rise, economic growth from tax reductions are likely to prove ephemeral. Monetary conditions have turned more restrictive in the broadest terms over the past year and a half. The monetary base and excess reserves of the depository institutions have been reduced by $668 billion (16.4%) and $910 billion (33.7%), respectively, from the peaks reached in 2014 or as the Fed was ending QE3 (Chart 2). This reduction in reserves is in fact an overt tightening of monetary policy, which will restrain economic activity in a meaningful way in the quarters ahead.

While maintaining the existing large portfolio of treasury and agency securities, the Federal Reserve has engineered contractions in the base and excess reserves by taking advantage of swings in other components of the base. The decrease in the reserve aggregates since 2014 reflects the following developments: (a) the substantial shift in Treasury deposits from depository institutions into the Federal Reserve Banks; (b) an increase in reverse repurchase agreements; (c) a shift from currency in the vaults of depository institutions to nonbanks (i.e. the households and businesses); and (d) a rise in required reserves as a result of higher bank deposits. These changes were necessitated by the Feds decision to raise the federal funds rate by 25 basis points in December of both 2015 and 2016. The Fed had the power to offset the reserve-draining effects of the shifting Treasury balances as well as the need for more currency and required reserves, but they chose not t o do so. The cause of the sharp drop in monetary and excess reserves is immaterial, but the effect is that monetary policy became increasingly more restrictive as 2016 ended.

Monetary policy has become asymmetric due to over-indebtedness. This means that an easing of policy produces little stimulus while a modest tightening is very powerful in restraining economic activity. The Nobel laureate Milton Friedman held that through liquidity, income and price effects, (1) monetary accelerations (easing) eventually lead to higher interest rates, and (2) monetary decelerations (tightening) eventually lead to lower rates. (In the near-term monetary accelerations will lower short-term rates and decelerations will raise short-term rates..."the liquidity effect".) Friedmans first proposition becomes invalid for extremely indebted economies. When reserves are created by the central bank, even if the amounts are massive, they remain largely unused, rendering monetary policy impotent. That is why M2 growth did not respond to the increase in the monetary base from about $800 billion to over $4 trillion. Plummeting velocity, which reflects too much counterproductive debt, further emasculated the central banks effectiveness. Thus, the efficacy of monetary policy has become asymmetric. Excessive debt, rather than rendering monetary deceleration impotent, actually strengthens central bank power because interest expense rises quickly. Therefore, what used to be considered modest changes in monetary restraint that resulted in higher interest rates now has a profound and immediate negative impact on the economy. This is yet another example of the adaptive nature of economies possibly unnoticed by federal officials.

Friedmans second proposition is clearly in motion. While monetary decelerations may initially lead to higher interest rates the ultimate trend is to lower yields. The Feds operations raised short- and intermediate-term yields in 2016. Although Treasury bond yields are mainly determined by inflationary expectations in the long run, the Fed contributed to the elevation of these yields in the second half of 2016 as well as a flattening of the yield curve. Working through both interest rate and quantitative effects, the Fed added to the strength in the dollar, which was further supported by international debt comparisons that favor the United States. The Fed stayed on the tightening course during the fourth quarter as the economy weakened. This suggests that the Fed contributed to both the rise in interest rates and the stronger dollar. More importantly, in view of policy lags, the 2016 measures by the central bank will serve to ultimately weaken M2 growth, reinforce the ongoing slump in money velocity, weaken economic growth in 2017 and accentuate the other constraints previously discussed.

(1) Impediments to Growth: Unproductive Debt

At the end of the third quarter, domestic nonfinancial debt and total debt reached $47.0 and $69.4 trillion, respectively. Neither of these figures include a sizeable volume of vehicle and other leases that will come due in the next few years nor unfunded pension liabilities that will eventually be due. The total figure is much larger as it includes debt of financial institutions as well as foreign debt owed. The broader series points to the complexity of the debt overhang. Netting out the financial institutions and foreign debt is certainly appropriate for closed economies, but it is not appropriate for the current economy. Much of the foreign debt resides in countries that are more indebted than the U.S. with even weaker economic fundamentals and financial institutions that remain thinly capitalized.

A surge in both of the debt aggregates in the latest four quarters indicates the drain on future economic growth. Domestic nonfinancial debt rose by $2.6 trillion in the past four quarters, or $5.00 for each $1.00 dollar of GDP generated. For comparison, from 1952 to 1999, $1.70 of domestic nonfinancial debt generated $1.00 of GDP, and from 2000 to 2015, the figure was $3.30. Total debt gained $3.1 trillion in the past four quarters, or $5.70 dollars for each $1.00 of GDP growth. From 1870 to 2015, $1.90 of total debt generated $1.00 dollar of GDP.

We estimate that approximately $20 trillion of debt in the U.S. will reset within the next two years. Interest rates across the curve are up approximately 100 basis points from the lows of last year. Unless rates reverse, the annual interest costs will jump $200 billion within two years and move steadily higher thereafter as more debt obligations mature. This sum is equivalent to almost two-fifths of the $533 billion in nominal GDP in the past four quarters. This situation is the same problem that has constantly dogged highly indebted economies like the U.S., Japan and the Eurozone. Numerous short-term growth spurts result in simultaneous increases in interest rates that boost interest costs for the heavily indebted economy that, in turn, serves to short circuit incipient gains in economic activity.

(2) Impediments to Growth: Record Global Debt

The IMF calculated that the gross debt in the global non-financial sector was $217 trillion, or 325% of GDP, at the end of the third quarter of 2016. Total debt at the end of the third quarter 2016 was more than triple its level at the end of 1999. In addition to the U.S., global debt surged dramatically in China, the United Kingdom, the Eurozone and Japan. Debt in China surged by $3 trillion in just the first three quarters of 2016. This is staggering considering that the largest rise in nonfinancial U.S. debt over any three quarters is $2.3 trillion, and China accounts for 12.3% of world GDP compared with 22.3% for the U.S. (2016 World Bank estimates). Thus, the $3 trillion jump in Chinese debt is equivalent to an increase of $5.4 trillion of debt in the U.S. economy. Extrapolating this calculation, Chinese debt at the end of the third quarter soared to 390% of GDP, an estimated 20% higher than U.S. debt-to-GDP. This debt surge explains the shortfall in the Chinese growth target for 2016, a major capital flight, a precipitous fall of the Yuan against the dollar and a large hike in their overnight lending rate.

William R. White (as previously cited) describes the debt risks causally, fully and yet succinctly. By pursuing the monetary and fiscal policies in which debts are accumulated worldwide, spending from the future is brought forward to today. As time passes, and the future becomes the present, the weight of these claims grows ever greater. Accordingly, such policies lose their effectiveness over time. He quotes Nobel laureate F. A. Hayek (1933): To combat the depression by a forced credit expansion is to attempt to cure the evil by the very means which brought it about. White reinforces this view later when he says, Credit booms are commonly followed by an economic bust and this has indeed been the case for a number of countries.

(3) Impediments to Growth: Weak Global Growth

Based on figures from the World Bank and the IMF through 2016, growth in a 60-country composite was just 1.1%, a fraction of the 7.2% average since 1961. Even with the small gain for 2016, the three-year average growth was -0.8%. As such, the last three years have provided more evidence that the benefits of a massive debt surge are elusive.

World trade volume also confirms the fragile state of economic conditions. Trade peaked at 115.4 in February 2016, with September 2016 1.7% below that peak, according to the Netherlands Bureau of Economic Policy Analysis. Over the last 12 months, world trade volume fell 0.7%, compared to the 5.1% average growth since 1992. When world trade and economic growth are stagnant, and one group of currencies loses value relative to another group, market share will shift to the depreciating currencies. However, this shift does not constitute a net gain in global economic activity, merely redistribution. Thus, gains in economic performance of those parts of the world provide little or no information about the status of global economic conditions.

(4) Impediments to Growth: Eroding Demographics

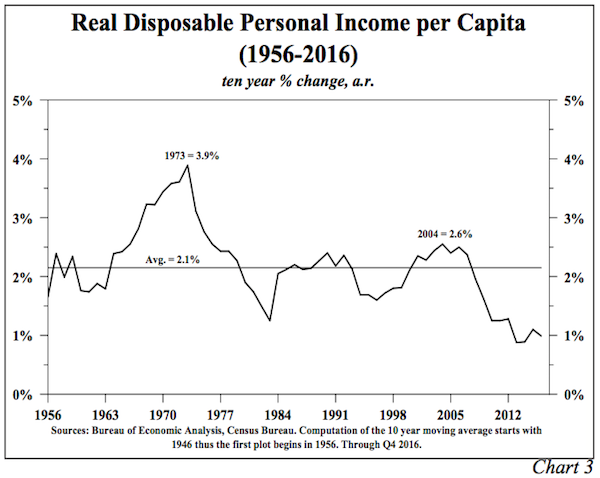

Weak population growth, a baby bust, an aging population and an unprecedented percentage of 18- to 34-year olds living with parents and/or other family members characterize current U.S. demographics, and all constrain economic growth. Moreover, real disposable income per capita is so weak that these trends are more likely to worsen rather than improve (Chart 3).

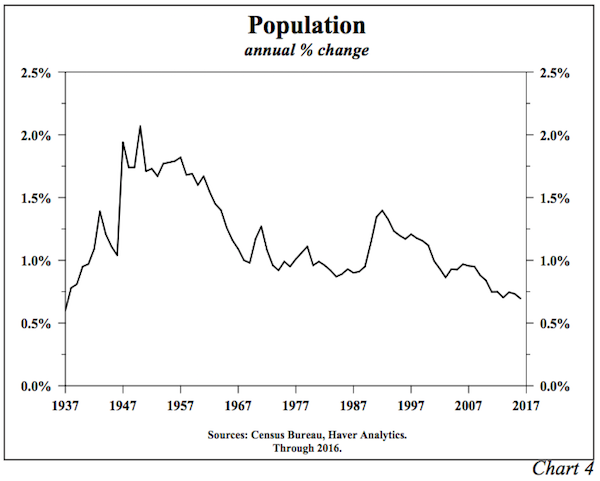

In the fiscal year ending July 1, 2016, U.S. population increased by 0.7%, the smallest increase on record since The Great Depression years of 1936-1937 (Census Bureau) (Chart 4). The fertility rate, defined as the number of live births per 1,000 for women ages 15-44, reached all time lows in 2013 and again in 2015 of 62.9 (National Center for Health Statistics). The average age of the U.S. reached an estimated 37.9 years, another record (The CIA World Fact Book). Population experts expect further increases for many years into the future. For the decade ending in 2015, 39.5% of 18-to 34-year olds lived with parents and/or other family members, the highest percentage for a decade since 1900, with the exception of the one when new housing could not be constructed because the materials were needed for World War II.

Over time, birth, immigration and household formation decisions have been heavily influenced by real per capita income growth. Demographics have, in turn, cycled back to influence economic growth. If they are both rising, a virtuous long-term cycle will emerge. Today, however, a negative spiral is in control. In the ten years ending in 2016, real per capita disposable income rose a mere 1%, less than half of the 50-year average and only one-quarter of the growth of the 3.9% peak reached in 1973. In view of the enlarging debt overhang, which is the cause of these mutually linked developments, economic growth should continue to disappoint. There will likely be intermittent spurts in economic activity, but they will not be sustainable.

(5) Impediments to Growth: Exhausted Pent-Up Demand

In late stage expansions, pent-up demand is exhausted as big-ticket items have already been purchased. At the start of 2017, the current expansion reached its 79th month, more than 20 months longer than the average since the end of World War II. At this stage of the cycle, setting new records is a reason for caution, not optimism. With regard to pent-up demand, the economy is in the opposite condition of a recession or an early stage expansion. The lack of such demand makes the economy susceptible to either slower growth or to the risk of an outright recession. Numerous signposts of this late cycle risk include low factory use, weakness in new and used car prices as well as most discretionary goods, a rising delinquency rate on the riskiest types of vehicle loans and a fall in office and apartment vacancy rates.

Bond Yields

Our economic view for 2017 suggests lower long-term Treasury yields. Considering the actions of the Federal Reserve to curtail the monetary base and excess reserves, M2 growth should moderate to 6% in 2017, down from 6.9% in 2016. In the fourth quarter, on a 3-month annualized basis, M2 growth already decelerated below the 6% pace anticipated for 2017. This is unsurprising given the fall in excess reserves and the monetary base. Velocity fell an estimated 4% in 2016 on a year ending basis. We assume there will be a similar decline for 2017, although in view of the huge debt increase and other considerations, velocity could be even weaker. On this basis, nominal GDP should rise 2% this year, which means inflation and real growth will both be very low. A 2% nominal GDP gain for 2017 points to a similar yield on the 30-year in time, meaning that the secular downward trend in Treasury bond yields is still intact.

Van R. Hoisington

Lacy H. Hunt, Ph.D.

| Digg This Article

-- Published: Thursday, 9 February 2017 | E-Mail | Print | Source: GoldSeek.com