-- Published: Wednesday, 8 March 2017 | Print | Disqus

By John Mauldin

The Super-Trend Puzzle

Washington DC: Debt Conduit

Growing Debt and Slowing GDP

How Much Government Do You Want?

You Cant Cut Spending to Get a Balanced Budget

Incoherent Contradictory Dysfunctional Voters

Changing and Incentivizing the Corporate Tax System

Moving to a Consumption Tax Revenue Source

What True Tax Reform Could Look Like

New Jersey and New Launches

A tax loophole is something that benefits the other guy. If it benefits you, it is tax reform

Russell B. Long

Corporate tax reform is nice in theory but tough in practice.

Andrew Ross Sorkin

I hold it that a little rebellion, now and then, is a good thing, and as necessary in the political world as storms in the physical. Unsuccessful rebellions, indeed, generally establish the encroachments on the rights of the people, which have produced them. An observation of this truth should render honest republican governors so mild in their punishment of rebellions, as not to discourage them too much. It is a medicine necessary for the sound health of government.

Thomas Jefferson, in a letter to James Madison. January 30, 1787 (230 years ago)

You say you want a revolution

Well, you know we all want to change the world

You tell me that it's evolution

Well, you know

We all want to change the world

You say you got a real solution

Well, you know we'd all love to see the plan

You ask me for a contribution

Well you know were doing what we can.

But its gonna be all right!

John Lennon/Paul McCartney, the Beatles, 1968

Today, patient reader, we hopefully reach the end of our tax reform saga, which has grown much longer than I expected. I seriously thought at the beginning that I could fit all this into one letter. Then it became a two-parter, then a trilogy, and then

well, here we are. The length notwithstanding, I have had more feedback on this series than on anything Ive written in a very long time. Opinions run strong. Todays letter is pretty much guaranteed to create even stronger reactions, as the realities I present are not pretty, and the options we have to fix the system without its completely imploding on us are simply not all that palatable. Candidly, I feel like the doctor having to tell the patient about a particularly difficult illness he or she has contracted. Its not going to be fatal, but there is no choice that wont require a great deal of discomfort and unpleasantness.

The time for us to make good choices about budgets, taxes, and our economy in general was 17 years ago. We are now dealing with the consequences of both the Bush and Obama administrations compounding poor budget, spending, and tax decisions including, in many cases, crucial decisions they declined to make. But some of these problems go back 40 years or more.

The research and writing for this series has underscored for me the extent to which all our challenges hang together. We tend to talk as though growth, taxes, currencies, central banks, politics, debt, jobs, and technology are independent topics; but drawing hard lines between them is impossible. The more comprehensive and systemic our analysis can be, the better.

I am reminded of something I wrote almost 13 years ago when I was describing macroeconomic trends. It speaks to the issues surrounding tax reform equally well.

The Super-Trend Puzzle

I am a big fan of puzzles of all kinds, especially picture puzzles. I love to figure out how the pieces fit together and watch the picture emerge, and have spent many an enjoyable hour at the table struggling to find the missing piece that helps connect the patterns.

Perhaps that explains my fascination with economics and investing, as there is no greater puzzle (except possibly the great theological puzzles or the mind of a woman, for which I have only a few clues).

The great problem with the economic puzzle is that the shape of the pieces can and will change as they come into contact with each other. You often find that fitting two pieces together will change the way they meld with the other pieces you thought were already nailed down, which may of course change the pieces with which they are adjoined, and suddenly your neat economic picture no longer looks like anything close to the real world.

There are two types of major economic puzzle pieces. The first are those pieces which represent trends which are inexorable: They will not themselves change, or if they do it will be slowly, but they will force every puzzle piece that touches them to shift to the force of their power. Demographic shifts

would be an example of this type of trend.

The second is what I think of as the balancing trends or trends that affect each other.

Last week I talked about job creation being the ultimate goal of the current congressional leadership in proposing tax reform. But to accomplish that laudable goal requires real tax restructuring, which is always controversial. To their credit, they are looking for new sources of revenue in proposing a consumption tax in the form of a border adjustment tax. However you want to go about reforming taxes, it has to be done in the context of the current budget, todays economic reality, and voter desires/wants/needs. Today well consider how government spending and debt affect the tax reform challenge. Unravelling cause and effect wont be easy, but the attempt will show us something important.

Before we jump in, I want to announce a special event were holding this month. On March 16, Jared Dillian and I will host an online virtual summit that weve dubbed Investing in the Age of Trump. Jared and I, along with some special guests, will talk about what weve learned in these first weeks of a new era and what we think is coming. Financial professionals especially need to tune in, because I know youre getting many question from your clients. Click here to learn more.

Now, on to the dramatic conclusion of our tax reform saga.

Washington DC: Debt Conduit

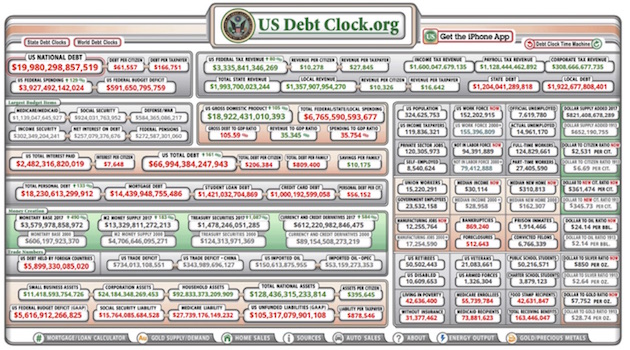

If you have never seen it before, stop right now and visit the US Debt Clock website. Youll see something like this, except that the numbers will be bigger:

The entire debt clock updates in real time, right before your eyes. Watching it is strangely mesmerizing and more than a little depressing. It exposes the human brains inability to comprehend large numbers. We can look right at them and still not truly understand their magnitude. Regardless, we have to try.

Direct your attention to the top left area of the Debt Clock. Youll that see the national debt has surged to almost $20 trillion (and will cross that line in the next few months). (State and local debt is another $3.2 trillion.) The $20 trillion is the face amount of all outstanding Treasury securities. It doesnt include unfunded liabilities like Social Security and Medicare. Those are down at the very bottom of the page, but set them aside for now.

Break down that national and state and local debt by the number of US citizens, and we find that we each every man, woman, and child owe over $70,000. Worse yet, the total debt per taxpayer is over $190,000 and rising fast. If you include unfunded liabilities, the total debt per taxpayer rises to around $1.2 million, give or take. (There are some analysts who would make it somewhat less than a million and others who would make it more than $2 million. Whatever, its a huge number.) By the way, that number does not include the unfunded liabilities at the state and local level, including the pensions that are theoretically guaranteed by the states. Add another few hundred thousand or so per taxpayer, depending on the state you live in. Trigger warning: If you live in Illinois or California, do not attempt to estimate this number without alcohol or heart medication nearby.

That is the amount of debt and future obligations weve allowed our elected representatives at every level of government to accumulate in our names. The amount is growing, too. Federal spending is near $4 trillion a year now, which is something like $591 billion more than the tax revenues received. But of course thats the budgeted deficit. The unbudgeted deficit is something else altogether. Yes, our government representatives structure things in such a way that they can actually increase the national debt without having to take the blame for doing so. For instance, in rough and round figures, the budgeted deficit was around $1 trillion in the last two years, but the actual increase in the national debt was $2 trillion. There are all sorts of expenses that are not technically considered budgeted items, including student loans, some Social Security spending, and so forth. But the government still has to borrow the money for those things from the pub lic.

You might be surprised how tax revenue breaks down. For all the talk about corporate taxes, the individual income tax is still by far the biggest revenue source. Total federal tax revenue of about $3.4 trillion comprises roughly of $1.6 trillion in income tax, $1.1 trillion in payroll taxes, and $308 billion in corporate taxes. (The rest is excise tax applied to things like liquor and cigarettes, along with other smaller tax levees. Odd factoid: receipts from the Federal Reserve, because the Fed ran up their balance sheet, now contribute about 3% of total US government revenue.)

What is wrong with this picture? The answer is clearer if you take off a few zeros. If your income is $335,000 a year and youre spending $390,000 a year, on top of the $2.3 million in debt you owe from previous years, plus the $10 million you are committed to pay in the future, are you overleveraged? And if youre adding another $50,000 a year to your total debt in addition to your budgeted spending, Id say youre overleveraged. But thats roughly the federal governments condition.

(Would you loan still more money to someone in that condition? Probably not. But people do so every time they buy a T-bill.)

This is just the federal government. State and local governments spend roughly $2.8 trillion a year. Their debt is smaller, relatively speaking, than Washingtons, at only $3.2 trillion; but they are trying hard to catch up. The debt load will get worse at all levels when (not if) the economy goes into recession again. Spending will rise, and revenue will fall.

Now, it is easy for us to criticize the government, but we need to look in the mirror, too. We elected these people and let them run up this debt. Why did we do that? I think in part because were so indebted ourselves that we are numbed to the reality.

US Debt Clock tracks personal debts, too. Add up our mortgage, auto, credit card, and student loan balances, and we collectively owe lenders over $18 trillion, in addition to the $20 trillion federal debt and $2.8 trillion state and local government debts.

Here is an important point. The debt Congress has run up on our behalf, $62,000 per citizen, is only slightly more than the $56,000 per citizen in debt weve taken on ourselves. In fairness, 80% of that amount is for home mortgages, which in theory have an asset behind them that is worth more than the mortgage.

But wait, theres more. Corporate and nonfinancial businesses have also run up debt roughly another $20 trillion. Total indebtedness in the US is around $65 trillion today, or roughly a 340% debt-to-GDP ratio. Total federal, state, and local government debt is 121% of GDP. Remember when just a few years ago I was talking about what a big problem Italys 120% debt-to-GDP ratio was? Thats where we are today.

(I am not sure why the St. Louis Feds Fred database discontinued this series in 2015, and I couldnt find it anywhere else in the database.)

Now, before we get into how we should reform our taxes, we need to create a list of all the factors that have a bearing on our decision. These are the key pieces to the super-trend puzzle I mentioned at the beginning of the letter.

1. Growing Debt and Slowing GDP

In a peer-reviewed study, Reinhart, Reinhart, and Rogoff demonstrated that when government debt rises above 90% it begins to have an effect on the growth of GDP. That conclusion is somewhat controversial in economic circles, as some say the critical level is higher or lower. Whatever weve gone well past 90%.

Understand, RR&R are not examining some theoretical proposition; they are looking at actual debt levels and actual growth levels in scores of countries and situations over a long period of history and seeing that excess debt inhibits growth. We can argue about why that is true, but the fact is that debt at the level that has already been reached here in the US makes it far more difficult to even talk about 3% or 4% growth. So when politicians talk about growing the economy by 3% a year, they are facing very strong headwinds. That sort of growth is not impossible in our circumstances, but it would be abnormal given what we know of the history of debt and growth. To grow the economy at 3% today will require tax reform beyond anything thats being suggested. It will require real tax reform, not just tinkering around the edges.

In the past Ive been critical of the Congressional Budget Office because it has been overly optimistic with its projections of GDP growth. So I must step in now and say that I am very impressed that the CBO has become far more real-world with its numbers this year. For the next 10 years they are projecting slightly under 2% growth per year, with 2017 being the outlier year at 2.3%. They also project an unemployment rate below 5% for the next 10 years and inflation in the low 2% range. That gives us nominal GDP growth of around 4%. (You can see this data and scores of other spreadsheets here.

That growth rate means a deficit topping $700 billion, and it means our debt will be growing faster than our economy can. In addition, as we learned above, there is the off-budget debt, which means that the debt will grow at about $1 trillion per year or more as long as we dont have a recession.

The CBO basically projects total deficits to add up to more than $10 trillion over the next 10 years. (See the New York Times story here.) That is roughly in line with nominal growth projections, so theoretically our debt-to-GDP ratio wouldnt rise all that much. Except

State and local debt will also rise, and then there are those pesky little off-budget numbers, which will add another $6$10 trillion to the national debt. Again, give or take. It is really hard to get a definitive handle, but Im pretty sure Im in the neighborhood. Now we are beginning to talk debt-to-GDP in the 150% range (give or take 10%) if everything is roughly left in place the way it is today.

Debt is consumption brought forward. If you borrow money and spend it on something today, thats money you cant spend in the future. In theory you have to pay the money back, too. Debt can be a good thing if it is used to purchase a productive asset that contributes to growth or adds to your net worth over time. But the debt that the government incurs is used almost 100% for current consumption and not for productive assets like infrastructure.

There are several theories as to why the debt has an inhibitory effect on growth. Clearly, debt can also fuel growth; but there is a limit to how much debt you can productively take on, and when you stop taking on that debt because youve reached your limit, the growth that has been created through the use of that debt ceases, too. Further, the money used to pay back the debt is money that cant be used to grow the economy.

Europe in general has more debt than the US does, and Japan has more debt than Europe and both of those regions grow more slowly than the US. Their citizens dont have bad lifestyles, and there is much to admire about their cultures; but if your goal is 3% growth and more jobs, then adding debt at the level we have already reached much less at European or Japanese levels is not something that should be seen as positive.

So one of the imperatives in this tax reform must be to reduce the deficit enough that the growth of nominal GDP will begin to reduce the negative effect of debt on growth. More on that in a moment.

2. How Much Government Do You Want?

When you add up government expenditures at all levels, you find that government spending is just under 40% (my calculators says 38.9%) of total US GDP. At the current rate of growth of budgets at all levels, the figure will be over 40% by the end of the year. (Some spending may be double-counted, so perhaps it will be only 39%. It is really difficult to come up with a definitive number. Theres a PhD thesis in here somewhere for someone who gets the numbers down in a workable spreadsheet that updates.)

You can see what percentage of GDP government expenditures are in other developed countries here. Not surprisingly, European levels tend to be high, and Korea and Switzerland have the lowest levels. But in general, as you ratchet up the level of government involvement in the economy, you start seeing countries with slower growth. (The research on the effects on growth of the size of government relative to the private sector is not as definitive as research regarding total debt.)

US gross domestic product will be over $19 trillion this year. The private economy will total $11.4 trillion, give or take. For total GDP to be $19 trillion, the private economy has to contribute the additional $7.6 trillion in the form of taxes. (Note: I am including debt that has to be financed by the private markets in my numbers.) Budgeted federal spending is only about 21% of GDP. The off-budget spending runs it up an average of 23 percentage points, depending on the year. (The number can actually vary quite widely.).

Most Republicans would prefer to see a smaller government footprint on the economy, so that means they want to hold tax revenues roughly where they are today but just collect them from different sources. Democrats, in general, would not mind seeing a larger government footprint and higher revenues.

3. You Cant Cut Spending to Get a Balanced Budget

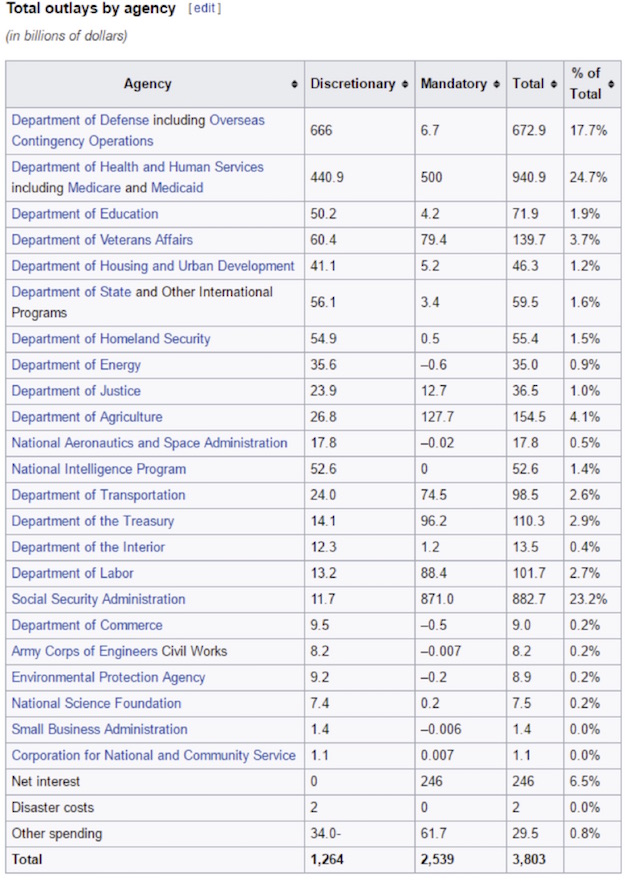

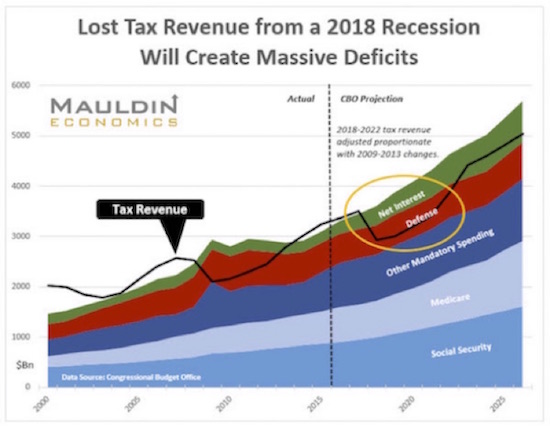

Every politician in every campaign (in pretty much every country in the world) talks about getting rid of government fraud and waste. If we could only cut out all of that wasted spending, we would have money either to lower taxes or to spend on something more useful. Except there is nothing to cut that is of any meaningful consequence. Here is a list from Wikipedia of the total outlays by agency and the percentages of the budget they represent. I am then going to share a few more charts that show how difficult it is to effectively reduce the deficit. Take a bit of time to go down through the list. See what small percentages most of the discretionary spending represents. Then remember that we already have a 15% budget deficit. You could cut a dozen whole departments and still not get a balanced budget. Try to find a dozen departments you would like to eliminate. Not one or two or three, but a dozen. Cutting their budgets by 20% gets you only about one-quarter of the way there. And do you really want to cut veterans benefits by 20%? Or slash space and technology R&D by 20%? If we are going to put more immigration officers into the field, that means a budget increase oops. And Trump wants to increase defense spending.

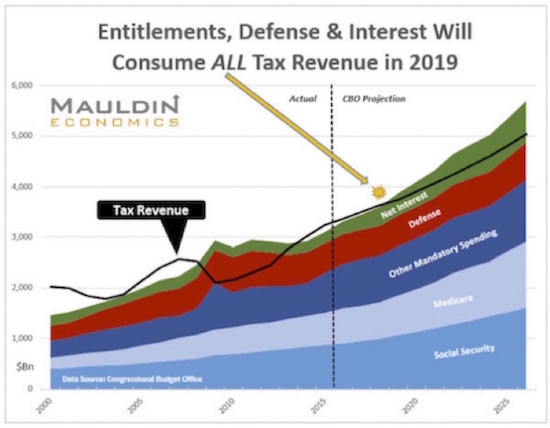

The following is a chart my team made for me last year. Basically, under current assumptions, entitlements, defense, and interest will take 100% of tax revenues in 2019. which means that every penny we spend above that level on any government expense, no matter how important, will either have to be borrowed, or taxes will have to be increased. And those current assumptions? Theyre optimistic.

I then asked my staff to basically replicate the 200809 Great Recessions drop in tax revenues and assume a recession in 2018. First, the resulting figures have the budgeted deficit approaching $2 trillion. The off-budget deficit would be at least $500 billion and probably much more. After a recession we could absolutely see $6 trillion added to the national debt in three years under an optimistic scenario.

We are deep into the third-longest recovery since World War II, and we are averaging over a full point of GDP growth less than we have seen in previous recoveries in part because of the size of our debt.

We can conclude one primary thing from this section: It is imperative to avoid a recession not just for the usual political reasons but because it would truly blow out the budget, deficits, and debt, and suck us into a downward spiral that would leave us with no good choices. But how realistic is it to expect no recession in the next several years?

I think pretty much everyone recognizes that the market is expecting nothing less than a miracle from the coming tax and regulatory reforms. Some regulatory reforms can be done quickly, and others are going to take quite some time. It will take years for the overall effects to have an impact.

If the tax reforms end up falling short of expectations, the market will turn on a dime; and the Trump bull market will suddenly become the Trump bear market. The Republicans simply have to deliver if they want to stay in power in two years not to mention see Trump returned to the White House in four years. His margin of victory was thin.

4. Incoherent Contradictory Dysfunctional Voters

Health care costs well over $1.1 trillion. Social Security is almost $1 trillion. Defense spending is $620 billion. Entitlement programs for our nations seniors and low-income individuals and families run $550 billion. (Thats food stamps, disability, affordable housing, earned-income tax credits, childcare tax credits, and so on.)

Where do you find $500 billion that you can take from the above items to balance the budget?

The American electorate wants two incompatible things: They want their taxes reduced, and they want more benefits. Or at least, they dont want their benefits cut nor those of their parents or friends.

And of course they want more GDP growth which is inconsistent with the growing debt.

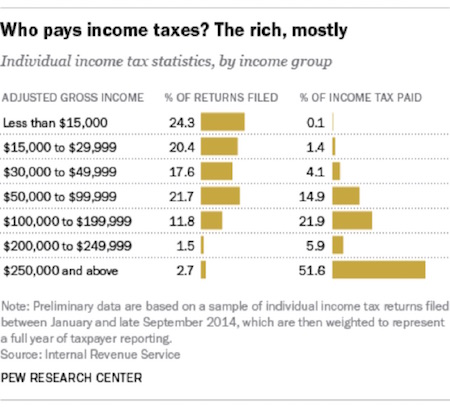

Who actually pays the income taxes the federal government collects? Lets look at this next chart from Pew Research. What we find is that almost 80% of taxes are paid by people making $100,000 or more. Just 2.7% of the taxpayers paid 51% of the taxes. Some 62% of individual filers paid a mere 5.7% of the taxes, and their average tax rate was 4.3% (not including Social Security taxes).

The top 1% of taxpayers accounted for more income taxes paid than the bottom 90% did. If youre going to cut income taxes, youre going to end up cutting taxes for the rich.

Here is the incoherent dissonance that Republicans are afraid to address: If theyre going to balance the budget, theyre going to have to either increase revenues or cut benefits. Since cutting benefits is a political nonstarter, theyre going to have to increase revenues. I will give Ways and Means Committee Chairman Brady kudos for trying to do that with his border adjustment tax. Lets look past the fact that I think a BAT will engender a global recession: Bradys motive is good. He certainly recognizes that in order to cut income taxes hes going to have to go to a consumption tax of some form. Seriously, that is an extraordinarily brave position for Republican in the house leadership to take. That Ryan has signed on to it says that he too realizes they have to do something radical.

Yes, repealing Obamacare and really restructuring health care might save a few hundred billion here and there. Maybe. Over time. Great, now were down to needing only another $800 billion to balance the budget. And we havent cut personal taxes or done anything with corporate taxes. Or come up with measures to create jobs.

I would like to think that the American voter would someday wake up and become less dysfunctional. I would also like the Jobs Fairy to create another 5 million high-paying middle-class jobs. I think both events fall in about the same range of probabilities. As in not going to happen.

Clowns to the left of me, jokers to the right, and here I am, stuck in the middle with the American electorate.

Conclusion? Unless we want to blow out the debt and we could do that (later I will even talk about how we should do that if we decide to do it) we are going to have to raise revenues. But raising income taxes is precisely the opposite of what we need to do if we want to create more jobs and investments.

5. Changing and Incentivizing the Corporate Tax System

Everybody knows that the US has the highest corporate income tax in the world. That heavy corporate tax burden puts us at a serious disadvantage, and we are watching one corporation after another leave the US for lower-tax countries. That exodus needs to stop and there is pretty good bipartisan agreement that it needs to stop. The House leaderships A Better Way plan calls for a 20% corporate income tax. Is not clear what deductions would be left, but I hope there would be damn few of the normal loopholes.

The irony is that the corporate tax is only 11% of the total revenue of the United States. If you got rid of loopholes and dropped the corporate tax to 15%, you really wouldnt lose all that much revenue. Corporate profits are roughly $1.5 trillion (before tax). A 15% flat tax would still produce well over $200 billion, or about two thirds of what we collect today. That would make us hypercompetitive internationally. It would also attract companies to come here because they would see us as the tax haven. (Sorry, France. And Europe and everyone else. This is the hometown boy talking.)

And if you taxed foreign income at some de minimis marginal rate like 57%, you could make up that remaining third. Since we are going to have to find some kind of consumption tax revenue source hopefully not the BAT lets get radical on corporate taxes.

6. Moving to a Consumption Tax Revenue Source

Right off the top, let me offer the proposition that economists of pretty much every stripe will agree that a consumption tax has fewer negative effects than an income tax does. Perhaps the one thing that 98% of economists can agree on is that incentives matter. If you want more of something, then tax it less; and if you want less of something, tax it more. Its about that simple.

If you want more income and jobs, tax them less. So if you can substitute a consumption tax for an income tax, even if the two generate the same revenue, the incentive structure you create is superior under the consumption tax regime. I am going to be walking into territory that is considered heretical for Republicans, but Im going to argue that we need to radically reform taxes by going to much higher consumption taxes and much lower income taxes. If we want to avoid a recession and really boost the economy and jobs, then we need to get medieval on income taxes. Dont take a scalpel to them. Bring out the axes and chainsaws.

The House GOPs A Better Way proposal creates a border adjustment tax in order to reduce income taxes. The problem is that the reductions, while significant, still just amount to tinkering around the edges. The top rate is still 33%, although the pass-through business tax rate is reduced to 25%, which starts to become a significant tax cut for small businesses. And while that will help, I dont think it is the jumpstart to the economy that they think it will be.

Ways and Means Chairman Brady was bold enough to introduce the concept of a consumption tax. So, with consumption taxes on the table, lets look at alternatives (since we really dont want the BAT causing a global recession, as I argued in part one and part three of this series).

There are a group of people who have proposed what they call a Fair Tax, which is basically a sales tax in the range of about 30%, which could replace all personal and corporate income taxes, payroll taxes, etc. Adding state sales taxes on top of that would bring actual taxes paid closer to 37% pretty much everywhere. That is enough to send a significant chunk of the economy deep underground, which is why I oppose the Fair Tax. I like the idea theoretically and would be for it in a minute if I didnt think that the black market economy, which is already probably 10 to 15% of the US economy, would double or triple. Maybe I dont have a high-enough opinion of my fellow citizen taxpayers.

There are two more significant options for creating a consumption tax. One is a value-added tax, or VAT, which is a great deal more difficult to avoid paying by going to the black market. Not impossible of course (see Italy or Greece for your tax-avoidance guidelines), but more difficult. Most of the world uses a VAT as a main tax system, including our large, industrialized peers. A VAT is not a great deal more complicated than the sales tax many states now impose. The difference is that it applies at every level of production, not just to final consumers. It is a well-tested option and generates abundant revenue with minimal side effects.

The VAT is a system that the rest of the world developed at its own risk. They worked out the bugs, in other words, yielding a proven, well-defined methodology the US can easily adapt with very predictable results. It doesnt offend my patriotism to admit that other countries do some things better than we do. I think we should embrace good ideas wherever they may originate.

The other thing about a VAT is that you can take it off at the border for exports. That gives it the same positive feature that the BAT has, just without picking winners and losers. Every business is treated the same in terms of the corporate tax they pay. It just makes us far more competitive as an exporting powerhouse, which translates into jobs.

You want real tax heresy? A significant majority of Democrats would like to see a carbon tax. Basically, that would be a tax on the use of petrochemicals to produce energy. They see it as a way to combat global climate change by reducing the incentives to use petroleum products. If I were House Speaker Paul Ryan or Majority Leader Mitch McConnell, I would go to Nancy Pelosi and Charles Schumer and ask them whether they are serious about this global warming thing. Would you really like a carbon tax? Id say. Well, well give you one, which we can use to offset the income taxes we want to reduce. In fact, well let you increase the carbon tax every year for the next 10 years. Fixing the budget deficit and stuff like that is important, you know.

Double dog dare them to not take you up on the offer of a carbon tax. Go public with it. Let their base see them back off of it.

Why would I propose such a radical thing? Let me hasten to assure you that I think the carbon tax would have absolutely no effect on climate change. But it would be an excellent form of consumption tax. And would it reduce the use of petroleum products over time? Sure. Would it result in a somewhat cleaner environment? Absolutely, and Im all for that.

I am as much an environmentalist as anybody else. I dont want to see the air I breathe, and I dont want anything in my water other than scotch or coffee. (And organic scotch and coffee at that.) But a carbon tax is just another form of a consumption tax. A $15 per ton of CO2 tax should generate about $80 billion per year of revenue. Raise it by $10$12 per year and after 10 years youre generating roughly $400 billion in revenue. The first level adds about $0.13 to a gallon of gas. In my SUV thats not inconsiderable on an annual basis, but the Europeans have shown us that they can live with 15 times the taxes on gas that we live with. In Germany they pay about five dollars per gallon just in taxes (give or take).

The point is, as we will see below, that a combination of consumption taxes could allow a radical reduction in or even the elimination of income taxes and a far lower corporate income tax. That would give a real boost overall to the economy. Of course, every combination requires trade-offs, but thats what makes the approach possible and workable.

What True Tax Reform Could Look Like

Lets sum up the constraints and desires mentioned above as we set out on our quest for tax reform. Admittedly, these are my constraints and desires, but sharing them will help you understand what my ultimate goal is.

1. Since too much debt at the level we currently have creates a drag on growth, we have to control the growth of debt. Thats pretty much like the admonition that when you find yourself in a hole, stop digging. At some point, maybe we could repeat the Clinton/Gingrich experience of actually paying down the debt. (Let me have my dreams!)

2. My fellow Americans want two inconsistent things: They want their entitlements and benefits to continue, and they would like their taxes to be lower. Cutting benefits will quickly result in a return to a Democratic Party-led government, and no politician on either side of the aisle has any stomach for doing more than tinkering with Social Security or really cutting healthcare.

I think Republicans will seek to find efficiencies in the way health care is delivered and thereby maybe reduce total healthcare expenses somewhat, but benefits are going to stay roughly the same. Yet somehow we need to get a handle on how to reduce the constant cost increases. So we have to figure out how to fund those benefits. And while you could probably cut $50 billion from the discretionary parts of the budget if you include defense spending as discretionary (which would elicit anguished screams and derogatory name-calling from everyone) we must sadly acknowledge that cutting $50 billion gets you only about 10% of the way to balancing the budget.

3. What is the appropriate size of government in the US economy? Here I am conflicted. I am truly a small-government advocate. But I also want to balance the budget and actually reduce the debt, which means (and I cant believe Im using these words) that were going to have to find additional revenues unless we are willing to take a hatchet to entitlements, which we are not.

4. We really do have to create jobs, or the future is going to get pretty bleak pretty quick. Job creation means allowing small businesses and entrepreneurs to keep more of what they make and to increase their savings. It also means radical regulatory reform. It comes down to the most basic of identity equations in economics. GDP is the sum of Consumption (C), Investment (I), Government Spending (G), and Net Exports (X M): GDP = C + I + G + (X M), which reduces down to Savings = Investments.

Its more complicated than that of course, but if you want investments that will create new jobs, the best thing you can do is to stop taxing savings and income and start taxing consumption. This country doesnt need more consumption; it needs more income. That in turn will lead to increased consumption and more jobs. This is a basic Hayek versus Keynes argument, and I come down on the side of Hayek. Which means that the vast majority of academic economists believe I am wrong.

5. We have to change the corporate tax structure to put our businesses on an equal footing with their competitors around the globe. And while were at it, why not make them hypercompetitive? Why not take the corporate tax rate down to 15% of everything over $100,000, with no deductions other than to comply with normal GAAP accounting principles? Really want to jumpstart things? Then allow 100% write-offs of all business investments such as research and development, equipment, and buildings (but normal depreciation on the actual land).

6. There are several types of consumption-based taxes.

a. A sales tax (which would be too high thats why I dismissed the concept above)

b. A border adjustment tax, which would be challenged by Europe at the WTO, and we would lose because the vote is a political vote. Further, the BAT (Im tempted to add Out of Hell) would set off immediate reactions by all of our trading partners, precipitating a round of tit-for-tat changes that would quickly deteriorate into something that looks like Smoot-Hawley. A BAT would cause a global recession. Further, it would pick winners and losers here in the US. Why is an export business better than an import business? They are equally valuable to the country. And they both create jobs.

c. A value-added tax (VAT) would easily withstand a challenge at the WTO, since nearly every other country in the world has a VAT.

d. We could introduce a carbon tax on petroleum products that would gradually increase, generating significant revenues over time. As noted above, a carbon tax is just another form of consumption tax, and it has the value of making progressive Democrats giddy about doing something for the environment and climate change, which makes them more likely to go along with the real Republican goals of job creation, income tax reform, and deficit reduction.

So what could we do to get real tax reform that would make a real difference? Some combination of a VAT and a carbon tax could essentially replace most income and corporate taxes. It would take a VAT of approximately 25% to completely eliminate all taxes (including Social Security taxes), and I think that would be too high. You would probably have to rebate the VAT to the lower two income quintiles (40% of wage earners) to mitigate the admittedly regressive nature of the VAT, so the VAT would probably have to be closer to 27% or 28%. Thats just too high.

In a conversation I had with Lacy Hunt, he reminded me of a paper in which he proposed a VAT (he calls it a consumption tax) of 16% (excluding food and medical care) and lowering the income tax to 7% on incomes over $250,000. He would also rebate the VAT to the lower two quintiles. In his paper he did not mention corporate taxes.

Since his study was done a few years ago, my guess is that the income tax rate he proposes would have to be about 10%, as government is now bigger. But its a simple flat-tax postcard filing. You pay 10% of everything over $250,000, with no deductions for anything. Then I would use the carbon tax to begin to reduce the corporate tax, dropping it to 20% immediately and to 15% eventually. As the carbon tax would slowly rise it would allow for some growth in entitlement spending that is already cooked into the books without having to go into further deficit spending.

Ultimately, you could use the increases in the carbon tax to begin to reduce the Social Security deficit. This approach, along with true Social Security reform, including raising the retirement age, means testing, and other measures, you could bring the Social Security system into balance relatively quickly. By relatively quickly I mean over 510 years

The VAT might need to be 17% if we want to get to a balanced budget more quickly. To help this process, I would absolutely hold the line on all government discretionary spending for five years. By that I mean that if a department is spending $1 billion today, it will be spending $1 billion in five years. Federal departments have to figure out how to make do, just as individuals must do when their incomes dont rise. Nondiscretionary spending could rise in step with inflation but no more than that. And of course there will be spending exceptions, but you make them as few and far between as possible. Or better yet, actually cut spending somewhere to allow the increase elsewhere. That is essentially what the Clinton/Gingrich tax reform did.

Now, Republicans will counter that opening up the door to a VAT will allow the Democrats to raise that tax later. Theres really no way around that. Democrats can always raise taxes when they come to power. We saw that in the first two years of the Obama administration.

The key would be to cut income taxes so much that it becomes difficult to raise them in any meaningful way if and when the Democrats are back in control. (That said, a BAT has the same disadvantage that a VAT does. Democrats can raise the BAT just as easily.)

These types of radical changes will jumpstart the economy and constitute true tax reform. They will level the playing field with our trade partners.

My assumption is that at some point we are going to have a recession, and that recession is going to blow the deficit and the debt out of control, as I outlined above. It is also likely to bring the Democrats back to power on promises to balance the budget and fix other problems they will say the Republicans caused. And then we will see tax reform on their terms, which will mean higher taxes of all types and a much larger government in terms of its impact on the country.

The Republican Party today has the possibility of introducing a consumption tax on their terms and accompanying it with serious corporate and income tax reductions. Do you really think that when the Democrats introduce such legislation in the future we will get anywhere close to the income tax reduction that we would see with a Republican offering?

The simple fact is that Medicare and Social Security expenses are going to rise inexorably over the next 20 years as the Baby Boomer generation grows older and requires more services. That $100 trillion of unfunded liabilities will come due, and the only way it will be even remotely possible to meet those obligations over the next 20 years is with a booming economy made possible through a combination of consumption taxes.

Tinkering around the edges of tax reform is not going to delay or overcome the potential for a global recession coming from outside our borders. Europe is on the edge. China has issues. Russia is on the brink of an economic disaster. If we can jumpstart the US economy, we can muddle through a European recession without actually having to endure a US recession.

I asked the following question of several well-placed political leaders who have long dealt with such things: If we are ready to go through the pain and hassle of a major tax overhaul, why not go all the way? They all said basically the same thing. Its really quite simple: Conservative Republicans are allergic to the three letters V-A-T. The VAT is unknown to them and their constituents, and therefore they fear it.

I understand the feeling. I also understand how much these same people dislike the IRS. Yet they choose to keep the awful current tax system despite having much better alternatives. I find this mind-boggling.

Heres the reality. Any tax reform will be difficult, because so many people and businesses have a stake in the status quo. They will resist any change, either stopping it completely or diluting it into a slightly different version of the same broken system we have now. That might be change, but its not progress. It is certainly not the kind of bold reform politicians talk about at re-election time.

So here is my question for Paul Ryan, Kevin Brady, Mitch McConnell, and President Trump. Like the Beatles of your youth, you say you want a revolution. They actually delivered one, musically and culturally. You can do the same economically by tossing out the entire broken tax system and replacing it with a proven alternative. Youll face opposition, yes, but that will happen no matter what you do. Just go all the way. And it will be much more palatable than the opposition that will grow in the wake of tax reform lite, which wont help solve our problems in any case. That is opposition you will meet in the polls and the voting booth, and you wont like it.

Real change requires political leaders to show real leadership. Do we have such leaders now? There is reason to be skeptical, but I think our leaders can rise to the occasion. Trump and the team around him are actually ready to do something big and bold. History is full of unlikely people who, thrust into seemingly impossible situations, somehow found the strength to accomplish great tasks. It happens. It can happen again.

But it wont happen if we do what weve so often done and accept incremental change because we think its the best we can do. Its not. We can do more. We have a chance to do it now. If we dont seize the opportunity to make these changes today, then in four years or eight years we may no longer be able to turn our economy around. We will have dug a bigger, deeper hole for ourselves. In less than 10 years, total US government debt could be in the $35$40 trillion range. That debt estimate is not much more than CBO estimates, and they dont include off-budget and state and local debt. Plus, they assume no recessions and low interest rates forever.

Seriously, what kind of choices will we have to make if we find ourselves up against that wall in four or eight years? And could we make them?

For the country and for our children, we have to make meaningful tax reform happen this year.

New Jersey and New Launches

I will be in New Jersey March 14 and 15. I will be speaking at Summit, Red Bank, and Hackensack, New Jersey, in the two evenings and at a lunch. The events are free and are sponsored by my friend Josh Jalinski, who is known as the Financial Quarterback on weekend morning radio, which he dominates in the New York/New Jersey area. My good friend Steve Blumenthal will also be doing part of the presentations. The events are already close to capacity; but if you would like to come, drop an email to Tina@jalinski.com, and she will get the specifics back to you. This is for individual investors I look forward to seeing you.

As part of the launch of my new portfolio-management company, I will be hosting regular dinners at my home for independent brokers and advisers, where we will share the specifics of how we are going about changing the way you manage the core of your portfolio. As I keep saying, the key is to diversify trading strategies, not just asset classes. Technology has allowed us to do some marvelous new things, and portfolio diversification in order to smooth out the ride is one of them. One of my goals is to be able to help brokers and advisers get their clients through the storms we all know are coming as the world struggles to deal with the massive amounts of debt and government obligations that are piling up. Maybe not this year, but at some point there has to be a great reset, and you need to be able to get your clients through it. If youre interested in attending to learn more about what were doing, drop a note to me at business@mauldinsolutions.com. Give me your name and tell me what firm youre with. Well get back to you ASAP. We will hold the first of my chili dinners in late March and then on a regular basis here in Dallas.

My friend and business partner George Friedman of Geopolitical Futures is hosting his own Geopolitical Futures conference on April 5 in Washington DC. With a few exceptions, I can almost guarantee youve never heard of his speakers which is precisely the point. People who are involved in geopolitical intelligence are generally not public figures. George and Meredith have invited the people they want to listen to and interact with, and they are limiting the audience to 80 people. There are fewer than two dozen spots left, so if geopolitical thinking is your bag, you really should consider coming. This is one of the few conferences I attend where I not speaking but will be in the audience all day taking notes. Join me.

Sadly, they are building a 22-story office building that will partially block the views from my bedroom. But the good thing is, I am getting to look down on a construction site and watch the process unfold. This weekend they put up a crane, which will be centered in the building as it goes up. Ive always wondered how those things just seemingly appear overnight, and its because the guys that do it really know what the heck they are doing. This is clearly a well-oiled team. Climbing up a 24-story tower by ladder several times a day, walking out onto that boom to grab the next piece, guiding a multi-ton section attached to cable it actually took an amazingly intricate effort to build that crane, and the process afforded me a rather inspiring view of American business at work. As I look out my windows, I can literally see a dozen cranes all over Dallas. Local builders are not thinking recession, thats for sure. I hope theyre rig ht.

Its time to hit the send button. You have a great week. This weekend well be sending a special Outside the Box your way, and then the following weekend Ill be talking about how we design portfolios and invest in the midst all the problems we face here and there in the world. You can take control of your own life and portfolio.

Your hoping we get real tax reform analyst,

John Mauldin

subscribers@MauldinEconomics.com

| Digg This Article

-- Published: Wednesday, 8 March 2017 | E-Mail | Print | Source: GoldSeek.com