-- Published: Thursday, 6 April 2017 | Print | Disqus

Source: Michael J. Ballanger for The Gold Report 04/05/2017

Precious metals expert Michael Ballanger explains why he believes base metals are overbought and precious metals, especially silver, are set to appreciate.

As the debate rages on and on and on concerning the global economic expansion (U.S.)/recovery (Eurozone)/Ponzi (China/U.K.), I am beginning to feel like a tennis ball in the heated heart of the 1981 McEnroe/Borg Wimbledon final being batted back and forth over the proverbial "Net" of Indecision, Confusion and Fear.

The greatest phrase ever concocted that is applicable to the world of trading and investing is NOT one lifted from the Edwin Lefevre book about the legendary Jessie Livermore ("Reminiscences of a Stock Operator," 1940) nor is it found in the hallows of Gerald M. Loeb's "Battle for Investment Survival"; it is a quote by the masterful writer Samuel L. Clemens, otherwise known by the nom de guerre Mark Twain, and it is as follows:

"It ain't what you don't know that gets you into trouble; it's what you know for sure that ain't just so. . ."

This brings me to the top of the metalsALL metalswhich includes two basic investment sub-groups known as "precious" and "base" metals, with the former being "monetary" metals and the latter being "industrial" metals. The two most notable monetary metals are gold and silver, with platinum and palladium being the lesser weights in the group, while the two most notable industrial metals are aluminum and copper, with zinc, lead and nickel being lesser weights in that group.

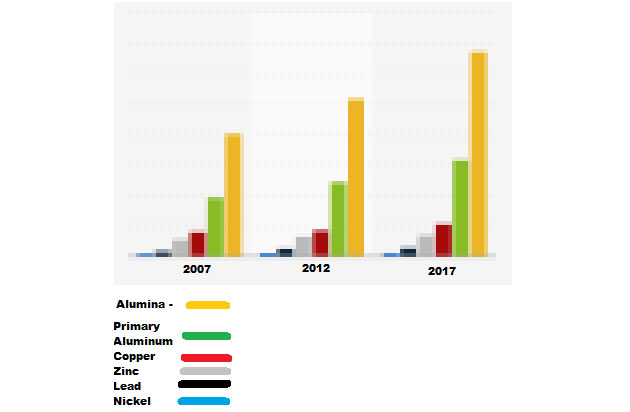

From the chart shown below, it is obvious that the greatest growth in consumption looking out is found in alumina and primary aluminum, with copper a distant third. Zinc, lead and nickel are all lumped together as also-rans, thus confirming what is, at least for me, an flagrant illustration of Mark Twain's insightful quote shown above: That the investment world of portfolio managers and analysts are all charging into zinc and copper because they know "for sure" that demand/supply fundamentals are undeniably sound. This is pure folly and as Twain says "it's what you know for sure that ain't just so. . ." that has in the past gotten me into a world of hurt.

In the world of investment academics, the term they use (to sound "smart") is "anchoring," which is the human tendency to rely on the first piece of (investment) information offered when making (investment) decisions, such as "zinc will be in shortage in 2018." That is exactly where we are today and why everyone now has their favorite zinc name to trot out be it Trevali or Canada Zinc or Teck or Tinka. That is one of the classic earmarks of a top in any sector, just as in 2011 at $1,900 per ounce, every PM and Internet blogger had a gold stock and how in 2006 after uranium prices had tripled, everyone owned a uranium stock. That "but it's different this time!" is the siren song for every bull market, that is exactly what I have been hearing for the last three months since zinc penetrated the $1.30 level.

With every blogger from the hiding places in Peru to the cubicles of Seeking Alpha, blogger "analysts" are all anchored in "knowing for sure" that zinc is going to $5 per pound due to what the world all knows is a "tight supply scenario," but as the self-proclaimed smartest man in the junior mining world, Rick Rule has said "The best cure for high and rising prices is high and rising prices." (A brilliant comment and one that I would like to pretend was mine.)

I first identified the zinc story back in 2012 while I was working as a broker with a small junior resource boutique where during a luncheon with an investment banker from Raymond James, he made the remark that he was far more bullish on zinc than on any other metal. Now, this was WAY before anyone was even talking about zinc because, as you recall, gold and silver were still well elevated despite having topped out in 2011. Zinc was clipping along at the totally unremarkable level of $0.80/lb. and if you even mentioned it in an investment meeting, it usually evoked exaggerated yawns and obviated watch-staring.

At the time, I was raising money for current market darling Tinka Resources (TK.V) at the $0.35 level and the company had not yet made the now-popular Ayawilca discovery. The RJ banker was dismissing Tinka's Colquipucro Silver asset (which I was highlighting) and accentuating the November 2011 Ayawilca discovery hole on the basis that silver was "old news" and that zinc was about to assume the role of the metals leader shortly. Needless to say, we were both wrong in that the next four years were as if we were getting root canal surgery without the benefit of Novocaine, as metal prices continued to sag and the juniors associated with either precious or base metals suffered.

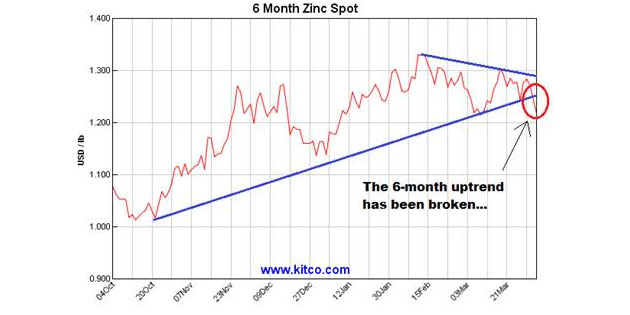

However, since around fifteen months ago, zinc prices mounted that very move that I was hoping for in 2013 through 2015 but which never materialized until early 2016. It then got amplified by the Trump election victory and all of the hype associated with the "Reflation Trade" where a country with $19 trillion (with a "T") debt monster goes out and doubles its debt in order to rebuild infrastructure and a wall on its southern border. The net effect is that in Q1/2017 the funds have all piled into the infrastructure trade with zinc a major beneficiary, but as can be seen from the chart below, the six-month uptrend for zinc has now been vanquished while most other components of the Trump Rally (including the U.S. dollar) have begun to roll over. Accordingly, I am moving away from zinc and copper and lead and into precious metals with silver at the forefront.

To be clear, the purpose of this missive is not to be critical of the base metal juniors but rather to highlight "that which is loved" versus "that which is hated" in the metals world. As I wrote about a few weeks ago, I try to own "that which is hated," although the risk is that I tend to be early in certain sectors leaving the invested capital as "dead money" as I await the turn, and by avoiding "that which is loved," I tend to miss the final speculative spikes in sectors that have attracted the momentum-chasers that reside throughout the blogosphere in chatrooms and investment forums.

In those forums today, silver is seen as "yesterday's trade" and interest in new silver deals is now confined to the silver bulls while the generalists are still focused on the base metals. Although silver is not by and large a "hated" sector, it is not nearly as over-owned as the infrastructure names are right now. Since I see the Trump Rally as very long in the tooth, all of the infrastructure names are going to get hurt when the big consensus trades start to get reversed, which they are with the Financials already having corrected 10% since January.

The rotation out of the base metal "infrastructure" sector into the precious metals is going to be coincident with the continued retracement in the U.S. dollar, which I firmly believe will come under continued pressure as the Trump administration continues to flounder in its attempts to implement the promises made during the pre-election campaigning period. The repeal of Obamacare has already failed as Republican congressional solidarity has disappeared, giving rise to doubts about the rest of the items on the Trump agenda. Since the gargantuan dollar advance that began before the election from the low 90s on the $USD has now given back over half of those gains, it is apparent that a goodly portion of the excuse for the stock market and concomitant $USD explosion has disappeared.

I am of the belief that when the investing public wakes up and realizes that the lights have been turned out on the Reflation Trade and that the infrastructure stock rally is toast, the sector that got thrown overboard on election night last November, the precious metals, will have an opposite reaction and one that turns out to be even more violent than the sell-off in the wee hours of the morning after.

The strategy I am attempting to describe is one that essentially debunks all of the bullishness for U.S. stocks and the economy and all of the bearishness for gold and silver brought about by the Trump victory. The only part of the Reflation Trade that I see as relevant is the part that deals with higher inflation rates, but the key takeaway here is that it will be the mountain of debt out there and not Trump fiscal policies that trigger the resurgence in inflation. Since silver is always the largest beneficiary of accelerated inflation, I am focusing all of my investment dollars for the second half of 2017 on the premise that infrastructure and economically sensitive stocks get battered as does fixed income, while precious metals enjoy a return to popularity with silver stocks from the junior explorers to the senior producers all firmly in the limelight.

So shut off the TV sets and avoid the KoolAid-distribution chatrooms and email blasts telling you that there is a cement "play" on the Mexican Wall being built or a Pennsylvania "coal trade" based upon Trump deregulation or a copper/zinc "opportunity" based upon new cars and trucks being built for bridge and highway replacementno one is talking about the $20 trillion debt bomb that was masterfully discarded in favor of the Reflation Trade by the Wall Street spin doctors but when they do, the monetary metals gold and silver will be back in vogue and from much higher levels.

We would all be well served to remember the immortal words of Mr. Twain as we reflect on those investment themes of which we "know for sure" (like the base metals) that are "no-brainers" when in fact it "just ain't so" and wind up in the trash bin. Being anchored in a mind-set where 90% of the market resides spells certain doom.

Buy precious, sell base. . .

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger's adherence to the concept of "Hard Assets" allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Want to read more Gold Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Disclosure:

1) Michael Ballanger: I, or members of my immediate household or family, own puts on the following companies mentioned in this article: Tinka Resources. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: None. I determined which companies would be included in this article based on my research and understanding of the sector.

2) The following companies mentioned in this article are sponsors of Streetwise Reports: None. Streetwise Reports does not accept stock in exchange for its services. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.

All charts courtesy of Michael Ballanger.

| Digg This Article

-- Published: Thursday, 6 April 2017 | E-Mail | Print | Source: GoldSeek.com