-- Published: Monday, 24 April 2017 | Print | Disqus

No Magic Rainbows

Squeezing Too Hard

Nonexistent Dollars Dont Grow

Zemblanity

The Merciless Math of Loss

An Ugly Picture

Sonoma, Orlando, and Washington DC

The ship of democracy, which has weathered all storms, may sink through the mutiny of those on board.

Grover Cleveland, the 22nd and 24th president of the United States

It is your concern when your neighbors wall is on fire.

Horace

The biggest mistake investors make is to believe that what happened in the recent past is likely to persist. They assume that something that was a good investment in the recent past is still a good investment. Typically, high past returns simply imply that an asset has become more expensive and is a poorer, not better, investment.

Ray Dalio, Founder, Bridgewater Associates

When you spend a couple of decades writing weekly letters to hundreds of thousands of people you think of as friends, your readers naturally come to associate you with a few key ideas. I have certainly become known for at least one. My longtime regular readers think of me as the Muddle Through guy. Thats not an image I have tried to cultivate, but I have it anyway.

I have to confess that its usually accurate. In a typical letter I will describe some sort of potentially scary problem, explain what might happen, then conclude that well probably avoid the worst and muddle through. That has almost always been the right call. The worst doesnt happen, and we all survive. Muddle Through can mean widely varying outcomes for individuals, but for the world at large, things generally work out OK.

As a statistical matter, this stance makes sense. The extreme tails of any distribution curve comprise outcomes that almost certainly wont occur. The most probable outcomes cluster around the fat middle.

Yet there is one problem that is very definitely coming our way that I really dont think we can Muddle Through and where even the middle-of-the-road scenarios are terrible, and thats the public pension crisis. I really see no way it can end well. Its going to hurt just about everyone.

But wait, my Canadian and German friends will say, thats an American problem. Leave us out of it.

I wish I could. The sad fact is that the US is the big fish in the global economic pond. One way or another, our problems affect everyone. You catch cold when we sneeze. The Disappearing Pensions crisis I described last week will hurt you, too. The only question is which transmission mechanism will bring it to you. Further, most developed countries have their own version of the pension crisis in the form of government promises that cant be kept. Same song, different verse.

Today I want to delve a little deeper and explain why pension angst is completely reasonable and not at all overblown. If anything, it has been understated.

But first, its getting close to the last call if you want to attend my Strategic Investment Conference, May 2225 in Orlando, Florida. I am told we are down to 35 spots still available. When those are taken, we will create a waiting list, as we have done the past two years. There are always a few last-minute cancellations, but there are not enough to allow everyone on the waiting list to attend.

If you havent yet secured your spot, you seriously need to take a look at whos going to be speaking. Some of the best geopolitical, economic, and social commentators from around the world will be joining us to focus on how the world is going to evolve over the next 1510 years. The theme of the conference is Paradigm Shift: A Destabilizing World.

And this is not just a series of lectures: We have designed the program to be interactive between the speakers and the audience. There is no other conference that I am aware of that so aggressively encourages such interaction with the speakers. So stop procrastinating and arrange to join us.

No Magic Rainbows

Most pension fund analysis focuses on funding levels, i.e., the assets a plan actually has versus how much it should have at a given point, based on actuarial analysis of future liabilities and assumptions about future contributions and investment returns.

Funding levels are important. They are a useful canary in the coal mine but only to the extent that the responsible parties pay attention to them and respond correctly. No such thing is happening. Worse, the assumptions that are being made mean that funding levels probably understate the coming disaster.

Yes, disaster. I use that word because I dont have a stronger one that I can use in a family-friendly letter.

Lets make this simple. The defined benefits that any DB plan will eventually pay its beneficiaries come from two sources:

1. Cash contributions, mostly from the employers but often from workers, too

2. Interest, dividends, and capital gains earned on the investments into which those cash contributions are placed.

Thats it. There is no pot of gold at the end of the rainbow. Theres not even a rainbow. Every penny that every retiree receives from every DB plan comes from those two sources. Unlike the federal government, cities and states cant mint currency by fiat. No magical ponies will come pulling carts full of cash to bail out the pension plans. (We do that only for banks.)

The problem is that, with few exceptions, neither source is producing at the level necessary to deliver the promised benefits. In many cases there is a vanishingly small chance they ever will produce enough. And the longer we go without fixing the problem, the smaller the chance becomes.

In each municipality and state, a few hardy souls are jumping up and down and screaming about the coming crisis in their locales. But when politicians do pay attention, the required actions are so painful that they conclude there is very little chance of anything substantive being done. And so they do nothing. The sad fact is that even actions that would fix part of the problem are often pushed away.

There is a perverse logic to this failure to act, and it has to do with the Merciless Math of Loss.

Squeezing Too Hard

Well start with contributions. The amount a city or state agency must donate to its pension plan(s) is a function of the promises made to its workers, typically in union-negotiated contracts.

The unions naturally want as much as possible. The employer wants to contribute as little as possible. Fair negotiations should produce a number acceptable to both sides but that assumes negotiations are fair. Often, they arent.

Here we must recognize a practical distinction between public and private. In theory, a city council is responsible to its voters just as a corporate board is responsible to shareholders. Yet the relationships are quite different.

Corporate board members are generally themselves shareholders, who share in the gains or losses their choices cause the company, and there is actually quite a bit of legal liability attached to being on a corporate board. The more happy and productive the board can keep the workers, the more valuable their shares will be. City council members, while residents in the communities they represent, dont gain or lose monetarily from the contracts they approve. Their incentive is to garner political support that leads to re-election or advancement to higher office.

So public worker contract negotiations are a competition between highly organized and motivated workers on one side and diffuse and often disinterested voters on the other. Elected officials may nominally answer to the voters, but the unions have more immediate influence, so the elected officials may not negotiate as zealously as they should, especially when the city, police, fire, and school workers tend to vote en masse for the candidate that is the most favorable to the unions. And in most municipal elections such workers may represent a high percentage of voters: Turnout for elections is generally less than 20%, and in many cities it is less than 10%. In the last mayoral election in my hometown of Dallas, only 6.1% of eligible voters actually participated.

On the other side of the equation, workers have every incentive to demand higher retirement benefits. To them, a pension is substitute compensation for cash the agency doesnt have to put in their paychecks today. They accept the promise of future retirement benefits in lieu of higher pay. And the elected officials have every incentive to promise those benefits, because the immediate cost of doing so is much smaller than the perceived value they give to workers, and they get the votes and cooperation of the workers. The problems that come down the road will be dealt with by other politicians.

The immediate cost, though smaller, is not zero. Government agencies have to make annual pension contributions, and the amounts of those contributions are a function both of the benefits politicians promised and other factors, like market returns, life expectancies, etc.

The fatal flaw here is that required annual pension contributions are an easily gamed number. A city council can shop around for a consultant who gives them whatever number they desire, and they frequently do just that. But the game gets harder to play as time passes and the bogus numbers get bigger and bigger.

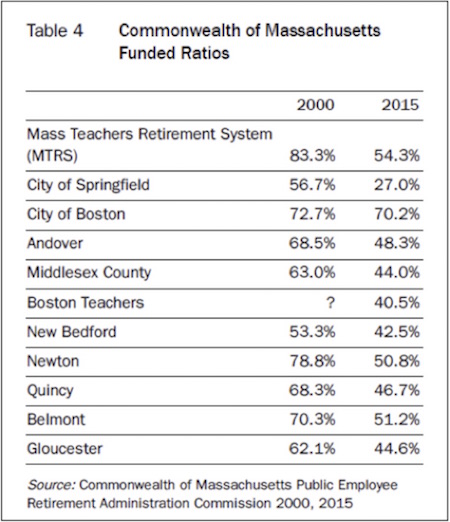

Repeated rounds of this process lead to funding ratios like these in Massachusetts:

As I said, these funding ratios depend on assumptions that are often far too optimistic. Yet most pension experts will tell you that there is no bouncing back, no restoring the ratio to a healthy level once it has dropped below 50%. Almost all the entities in the table above are in or near that zone. City of Springfield retirees are in deep trouble, and the rest not far behind.

What, realistically, can retirees expect from government agencies like these? Very little, frankly. I repeat: Benefits come from plan contributions and investment gains. I dont know the situation in these specific communities, but its highly unlikely that elected officials can raise taxes or cut other spending enough to make the kind of contributions required to make up these shortfalls. It cant happen, which means it wont happen.

Ive said this before, but it bears repeating: City limits are static, but the tax base is not. People can move away. Companies can relocate. Both will happen if local officials push too hard. That is what ultimately forced Detroit into bankruptcy. The city was depopulating, but its expenses didnt fall accordingly.

Nonexistent Dollars Dont Grow

The table above came to me via Marc Faber, who in turn got it from pension expert Frederick Sheehan. The title of Sheehans report is good advice:

Public Pension Recipients: Start Saving. You Are on Your Own.

That falls into the category of advice no one wants to hear, but it is nonetheless correct. Many, perhaps most, current city and state workers simply arent going to get anything like the pension benefits they have been led to expect. Sheehan puts it this way.

We are promised... is the haphazard refrain often encountered when the reduction of pension claims is mentioned. Promised or not, one distinguishing feature of non-federal government spending commitments stands out: only the United States has a printing press. States cannot print money. They can earn returns on their pensions invested assets, they can sell city hall, lay off the public works department, and tax, but an underfunded pension plan can only pay claims with dollars that exist.

This list of options is actually too generous. Sell city hall? That presumes someone will buy it. Lay off the public works department? Not good for property values. Raise taxes? Right, on all the people in those houses without sewage service.

Repeat Sheehans last line and burn it into your brain: An underfunded pension plan can only pay claims with dollars that exist. No one gets anything if the money isnt there, and in a disturbing number of places it isnt.

Keep in mind, those horrifyingly low funding levels would be far lower still if they didnt assume investment returns that are, in fact, unrealistically rosy. Between 7½% and 8% is typical now. Exactly how is that going to happen?

We know that pension plans typically have only 4050% of their assets in equities, something like 40% in bonds, and the rest in real estate and alternative asset classes. How do you get 8% from that mix? Keeping 40% in bonds at 3% (if youre lucky) means everything else has to make 15%.

Do you really want to bet that stock returns will average 15% over the next decade? If you actually think that is your future reality, then all I can say is that the 60s were probably pretty good for you, and you may still be living in a drug-induced hallucination. If you are a public pension beneficiary, that may be your best shot: just pretend. Good luck with that.

Marc Faber, who is even better at scaring people than I am, points out something that should be obvious but apparently is not: Pension plan funding ratios have been declining even as financial markets have posted impressive gains:

I find the deteriorating funding levels of pension funds remarkable because post-March 2009 (S&P 500 at 666) stocks around the world rebounded strongly and many markets (including the US stock market) made new highs. Furthermore, government bonds were rallying strongly after 2006 as interest rates continued to decline sharply.

In fact, if I look at the total return of both equities and bonds (including interest for bonds and dividends for equities) over the last ten years (ending August 31, 2016), I note that the return levels exceeded the expected asset return of almost 8% a year.

My point is this: If, despite these truly mouth-watering returns of financial assets over the last ten years, the unfunded liabilities have increased, what will happen once these returns diminish or completely disappear? After all, it is almost certain that the returns of pension funds (as well as other financial institutions) will diminish. Consider pension funds that have increased their allocation to bonds, and now (in the case of S&P 500 companies) exceed the equity allocation.

Now consider the following. Ten-year US Treasuries yield 1.74% and 30-year US Treasuries 2.48%. In Europe and Japan, government bond yields are frequently negative. How will it be possible with these low yields to achieve, in the long term, returns that even come close to the expected return of 8%?

Marc wrote that in October 2016, so those yields are a bit higher now; but you get his point. Yields are nowhere near high enough to deliver the kind of returns pension trustees are assuming. It just wont happen.

Worse, even if return assumptions are fulfilled for a while, as unlikely as that may be, those good years will not be enough if a bear market strikes at the wrong time. Sheehan quotes a study by Steven Malanga in City Journal last year. The State of Utahs pension plan lost 22.3% of its assets in 2008. It gained back 13% in 2009. A good start to recovery, right?

No, not right. Utah determined that its investment returns would have to compound at over 10% annually for the next 20 years just to recoup that 2008 loss. Why is that? Because while the portfolio was down, workers were continuing to earn new retirement credits. You have one set of people trying to fill the hole while another group digs it deeper. So just making back what you lost is not enough. You also have to make back the additional obligations you took on while you were trying to recover.

Zemblanity

The word serendipity was introduced to the English lexicon in 1754 by Horace Walpole as luck that takes the form of finding valuable or pleasant things that are not looked for. Let me introduce you to a new word. In 1998 William Boyd coined the term zemblanity to mean basically the opposite of serendipity. The Urban Dictionary defines zemblanity as the inevitable discovery of what we would rather not know. If you are or have been the parent of teenage kids, you have had some of those zemblanity moments.

America is going to be experiencing its own zemblanity moment during the next financial crisis when it discovers that many of its municipal and state pensions have crossed the threshold from merely difficult situations to almost impossible-to-fix ones. We are going to do a little math here, but I promise you it will be rather elementary. No calculus required. Seriously, this is so simple that even a politician could understand it. If you could get one to sit down and really think about it, much less do anything.

The Merciless Math of Loss

My friend Steve Blumenthal wrote a little essay called The Merciless Math of Loss. He opens by quoting Ned Davis:

Its a little-known but startling fact: The average buy-and-hold stock market investor spends 74% of his or her time recovering from cyclical downturns in the market (from 1900May 2015). (Ned Davis Research)

Thats according to well-respected Ned Davis Research, Inc., in Venice, Florida. It raises a big question: How is it possible that investors spend three quarters of their time just getting back to the starting line?

The answer is explained by the unforgiving mathematics of loss: When investments lose ground, they must make up more ground, percentage-wise, just to get back to even.

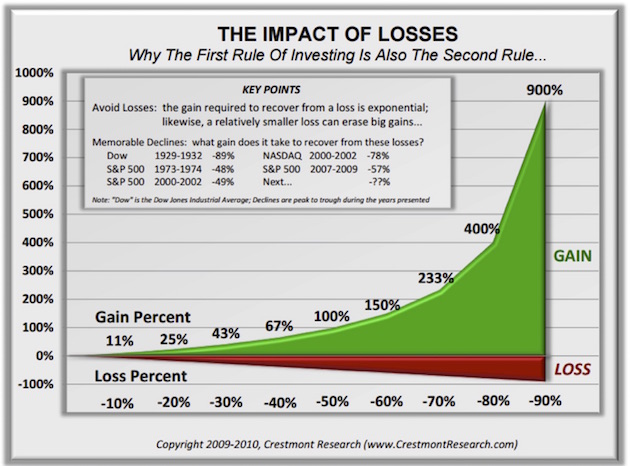

Say you invest $10,000 and your account takes a 10% loss over six months. Youre down to a $9,000 balance. Because of your reduced capital base, you will have to earn 11% to recoup your losses. The steeper the losses, the higher the hurdle becomes for breaking even. For example: Recovering a loss of 30% requires a 42.9% gain; a 50% loss requires a 100% gain. To recover from a loss of 75%, a 300% gain is required.

Getting back to even can eat up precious time. Take that 10% loss over six months. Earning a steady 4% annually after that, you will still need two and three-quarter years just to get back to where you started. That time would be much better spent accumulating new money. Remember, the idea is to grow your money, not just regain lost capital.

You can see the required recovery levels more graphically in this chart from my friend Ed Easterling at Crestmont Research:

A 50% loss requires a 100% return to get back to breakeven. Add just another 10% loss for a total loss of 60%, and it takes 150% to get back to breakeven. The mathematics get uglier the bigger the loss.

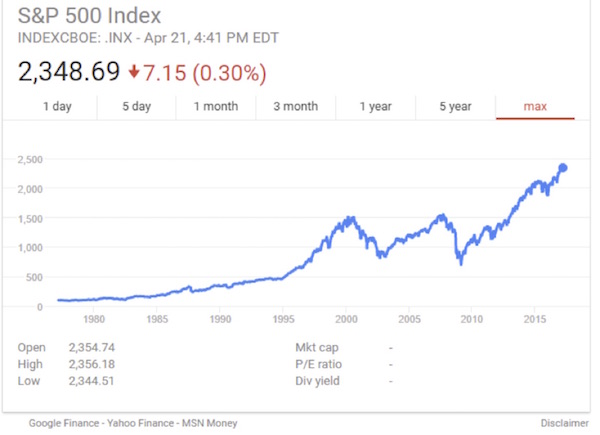

Lets look at two charts of the S&P 500. The first shows straightforward index levels since 1977. If you click on the link above or the chart below, you can bring up an interactive version of the chart. Click on max and then run your cursor back and forth to see where the index was on various dates. Note that it took 13 years to recover from the peak of 2000 (not including the very temporary peak of 2007). Since 2000, the market has risen roughly 50%. A 50% return over 17 years is not exactly what people thought they were going to get back in 2000 its a little less than 3% a year on a compounded basis.

But thats not really a fair way to look at it. While the NASDAQ and other indexes have small dividend payouts relative to the size of their indexes, the S&P 500 actually has reasonable dividends compounding over time. So this next chart shows the level of the S&P 500, including dividends, since 1988. And yes, while it did take almost 13 years for the market, including dividend returns, to fully recover from the top in 2000, since that time it has actually more than doubled with the help of dividends. That slightly-larger-than-2% dividend has compounded nicely over time.

That pleasant result has lulled pension plan managers and other investors into believing that this period is somehow normal. And it has convinced them that their pensions must be recovering lost ground. The problem is, thats an illusion.

I read recently that the average pension fund in the United States expects its investment prowess to bring home returns of 7.69% in the future. A number of funds still use 8% as their target. Seriously.

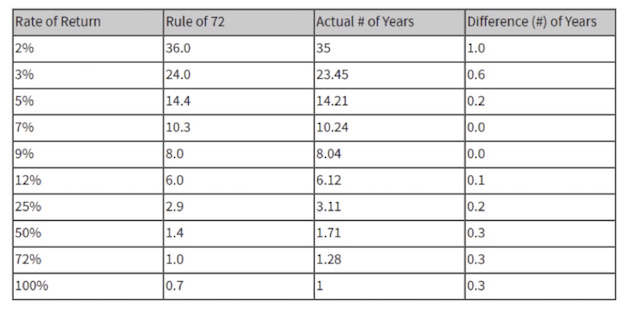

Now lets do some math based on the rule of 72. The rule of 72 is basically (according to Investopedia) a simplified way to determine how long an investment will take to double, given a fixed annual rate of interest. By dividing 72 by the annual rate of return, investors can get a rough estimate of how many years it will take for the initial investment to duplicate itself. Investopedia even provides this handy table:

Let me reiterate that the biggest portion of the money that will be used to pay retirees from a pension fund comes from actual returns on investments and not from the original contributions. That means that if there is a portion of the pension fund that is currently unfunded, those (nonexistent) dollars cant grow so that they can be redeemed 30 years later by the retirees.

Further, the amount by which a pension plan is underfunded is determined by the assumptions on returns that the fund makes. These next few paragraphs will drive the actuaries and math nerds among my readers crazy, but I am going to simplify here to make a point.

If you project returns of 8%, then you expect your assets to double every nine years. Thus in 27 years, $1 that is sitting in the fund today will have become $8.

But what if your returns grow at only 5%? Looking at the handy chart above, we see that it takes 14.2 years to double your assets, so that in 28 years $1 will have grown to only $4. That is only about half of the dollars that your actuaries and consultants have assumed would be there.

If you project 5% returns for the next 30 years, then you have to almost double the current level of contributions to have the necessary assets in 30 years. So basically, any pension fund that is assuming 8% compound returns and is falling significantly short of that level now, will turn out to be massively underfunded, far more so than funds are telling their retirees or the public.

I understand that the actuaries actually calculate the underfunding for each year, not just 30 years out. That makes the math far more complex, but the principle is the same. The lower you make your return assumptions, the more you are required to fund current pension balance sheets. And that funding comes from only two sources, taxpayers and current workers. Of course, you could go to your current retirees and tell them they are going to get less money, starting right away, but how popular will you be then? (And how illegal would that be?)

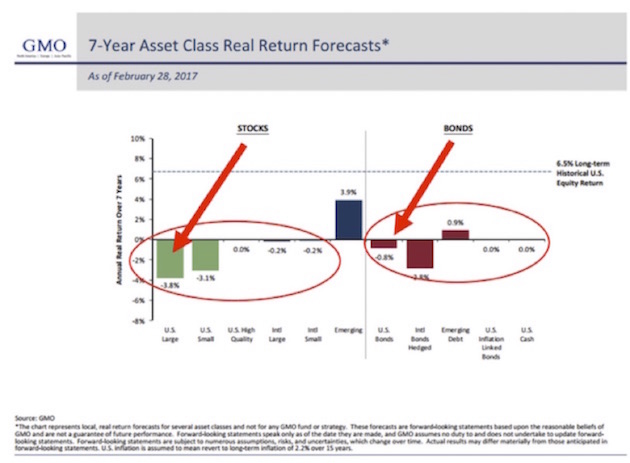

What happens if Jeremy Grantham is right (and he has been right 97% of the time with his seven-year projections), and total market returns are less than 1% over the next seven years?

Then not only will pension funds have to grow returns much faster in subsequent years to catch up, they will also have to go to their respective states, cities, or schools and say, You need to give us more money, because were becoming more underfunded each year.

Lets just make this pension data analysis even more fun. During the Great Recession, the market fell 58%. A 50% drop in the stock market during a recession is not unusual. What is the probability that we will not have a recession in the next four years? Pensions are making a huge wager on that proposition, so it is not a trivial question.

An Ugly Picture

The more I look at the situation with pensions, the more clearly I see that there is no practical way out. We know three things with near certainty:

1. Public pension plans are nowhere near able to meet their obligations.

2. Most cities and states cant possibly contribute enough to cover the gaps without serious budget upheaval or increased taxes.

3. Plan investments wont achieve projected returns, let alone earn enough to cover the contribution gaps.

I suppose in a different flavor of quantum universe where math works differently, it might be possible to make these pension plans work. Here in our universe, not so much. Not going to happen.

What does that mean?

It means several million more people are not going to have the kind of retirement they envisioned. If youre one of them, you need to aggressively start saving every penny you can, right now.

Further complicating the situation is that in many places, state and local workers dont participate in the Social Security system. They wont even have that minimal amount to cushion the blow.

All these unexpectedly uncomfortable retirees will affect the economy. Their added savings will serve to keep interest rates low for everyone. Their consumer spending will be lower, reducing demand for many goods and services. They may have to sell their homes and move to more economical locations, thereby depressing property values.

None of this is built into anyones economic projections, which are often not so good in the first place. Id like to point out a silver lining, but I just dont see one. All I see are clouds: dark, ugly clouds threatening to rain on us all.

Will we Muddle Through? Most of us will. But I am 100% confident that this pension debacle is going to end very badly for many millions of state and local public workers. And we havent even talked about the social impacts.

You think the 2016 presidential campaign was ugly and divisive? Wait until your local elections turn on whether or not to cut your neighbors pension in half. The arguments are going to be up close and personal. What kind of person will run for local office in those conditions? Probably people who shouldnt. Which will only make it all worse.

Like state and local pension obligations, US federal government pension obligations are also basically unfunded. They are expected to come from future tax revenues. Those obligations are the bulk of the over $100 trillion in unfunded liabilities that show up in the estimates of how much the United States is really in debt. That money is going to have to come from somewhere. But just as the United States will never default on its actual debt, I truly dont believe we will default on US government pension obligations.

Future politicians are going to be faced with some very uncomfortable choices, one of which will be how much money to ask the Federal Reserve print in order to honor those obligations. Or should they cut future pension payouts, or maybe even current ones?

When Illinois or any other state finds itself unable to pay its pensioners, I think it is unlikely that the federal government will ride to the rescue. And the other states will look at each other and say, Not my monkey, not my circus.

But what happens when a majority of the states and citizens in those states begin to demand that something be done to help the poor public service workers whose lives are being seriously impaired? We can say that in todays political environment it is unlikely that the federal government would rescue states and cities. But in a future political environment? Hard to say. The pressure to do something is going to be huge. And its going to be coming from seemingly everywhere.

If you arent already angst-ridden, consider this letter your ticket to the club. Its going to hurt to belong; but were all in this together, one way and another.

Sonoma, Orlando, and Washington DC

Last week we had a bit of an oops moment. I mentally knew that I had committed myself to an investment speaking engagement in Sonoma sometime in April or May, but for whatever reason that event did not make it onto my calendar. I have actually had conversations about the event with the host organizers, Brian Lockhart and Geoff Eliason of Peak Capital Management, but somehow the event never got firmed up here on my end, which of course meant that no one had actually booked airline tickets. I got an email on Wednesday asking me to confirm a time for a conference call about next weeks event. I immediately got on the phone to confirm the details and then asked my new executive assistant, Tammi Cole, to look into last-minute airline reservations and so on. Turns out there were seats available, and Shane and I will be in Sonoma on time Monday afternoon. Then, if I havent missed putting anything else on my calendar, my next trip wi ll be to the Strategic Investment Conference May 2225 in Orlando. On the 26th Shane and I fly up to Washington DC to be with Neil Howe and bride Gisela at their wedding. Im particularly honored that he would be willing to speak at SIC on Thursday morning and then fly back to get married! But then, what are friends for?

This past week has was filled with an endless array of meetings, conference calls, and research and writing, with my number one goal of working on next weeks letter somehow slipping until today, so I now find myself writing Sunday afternoon in an effort to get ahead of next week so that I can actually spend some time with my friends in Sonoma, rather than stay in my room writing. I dont want to say that Im running fast, but my shadow has started to complain about having to keep up.

Who knows, in Northern California I might even have to borrow some golf clubs and play a few holes to see if my back is up to it. I have been feeling a bit looser lately. I think the best idea might be to buy six balls and play until I lose them. Surely I can last a few holes.

You have a great week.

Your hearing the gym call my name because it misses me analyst,

John Mauldin

subscribers@MauldinEconomics.com

Copyright 2017 John Mauldin. All Rights Reserved.

| Digg This Article

-- Published: Monday, 24 April 2017 | E-Mail | Print | Source: GoldSeek.com