-- Published: Tuesday, 23 May 2017 | Print | Disqus

By John Mauldin

The Great Reset

What Happened to Deleveraging?

Unfunded Liabilities

The Unthinkable Recession

How Should We Then Invest?

Introducing Mauldin Solutions Smart Core

Orlando and SIC

A speculator is one who runs risks of which he is aware, and an investor is one who runs risks of which he is unaware.

John Maynard Keynes

The biggest mistake investors make is to believe that what happened in the recent past is likely to persist. They assume that something that was a good investment in the recent past is still a good investment. Typically, high past returns simply imply that an asset has become more expensive and is a poorer, not better, investment.

Ray Dalio, founder, Bridgewater Associates, LP

This letter and next weeks will be two of the most important Ive ever written. They will set out my philosophy about how we have to invest in the coming days and years. They are the result of my years of actually working with clients and money managers and thinking about the economic and particularly the macroeconomic world. Because of some of the developments I will be discussing, I think the future is likely to be extremely challenging for traditional portfolio allocation models. The letters also discuss my thinking on new developments in markets that allow us to more quickly adapt to our ever-shifting environment, even when we dont know in advance what that environment will be. I hope you find the letters helpful.

Longtime readers know that this letter tends to talk more about our global economys problems than about its positive opportunities. Thats not to say that I ignore the opportunities. In fact, about half of my next book will focus on the tremendous potential I see developing over the next 20 years.

I am extraordinarily optimistic about the human experiment as we move deeper into this century. I foresee more of the world lifted out of poverty and afforded more of the necessities and even the luxuries of life, a much cleaner environment, steadily decreasing warfare, and healthcare radically altered in a positive manner. I truly believe most of us will live much longer than we currently imagine. In the not-too-distant future we will conquer many of the diseases that cut life so tragically short. Given this view, how is it possible to not be optimistic?

But other less benevolent trends cast deep shadows on that positive outlook. I think we are rapidly coming to the point where there is no simple way to avoid them. Much of our comfortable society is going to be radically altered, bringing new expectations and frustrations. Unfortunately, these trends will have an enormous impact on our investments. As I travel around the country, I am often asked after my speeches or at dinner, John, I have the same concerns. But what do I do about my investments, my family, especially my children and my business?

I will admit my answers have often been personally unsatisfactory, at least with regard to investing, which is my day job. Many potential solutions are not available to the average person or dont address the total problem.

I have spent the better part of four years and in some ways the last 35+ years of my financial industry career looking for those answers and trying to come up with an approach that not only makes sense but that also has a broader reach an answer not designed just for a few high-end investors in one particular country but something that could eventually be available and useful to everyone, everywhere.

Finding the answer hasnt been easy, because all the apparent best solutions seem to have market and regulatory issues. Some are only available to certain sets of investors or bring other problems along with them. Some of the things I wanted to do werent even technologically possible four or five years ago. But the markets and technology have evolved (rapidly!) to make it possible to now approach our portfolios in a systematic way that allows us to counter negative trends.

This letter will cover the philosophical underpinnings of my thinking. Ill also introduce some investment tools (which I will give you access to through a link later on in the letter) that express that philosophy, but you could also design a different answer that fits your own (or your clients) portfolio construction.

First, let me quickly review the investing challenges as I see them. First, there is the massive imbalance between the debts governments owe and the promises governments have made, sure to cause enormous market turmoil, the timing of which will be somewhat unpredictable.

Second, there has been a common misperception of critical points that Harry Markowitz made in his 1952 graduate student paper that eventually became his 1990-Nobel prize-winning work that we now call Modern Portfolio Theory (MPT). We have followed an interpretation of MPT that in my opinion could cause great damage to the returns and retirement lives of investors. We need to update our thinking to incorporate what I think of as MPT 2.0. Premature optimization is a major portfolio problem.

Third, we must understand that the underlying core investments in most portfolios are undergoing radical changes, which makes any backward-looking portfolio model essentially worthless. I can truly assert that the standard investment line that Past performance is not indicative of future results has never been more true than it is today.

Further, the way we determine relative value within an asset class (especially equities) is being short-circuited in a way that could seriously impair traditional active asset management.

And yet we cant retreat from the market. The only way we can grow our portfolios and income, other than by being involved in our own businesses, is by saving and investing our earnings. But as Ill describe below, markets will be volatile at best and destructive at worst. So how do we stay in the market yet avoid negative outcomes? How do we use MPT 2.0 to diversify among asset classes and smooth out long-term returns in our portfolios when, if I am right, all that diversification may simply diversify our losses?

That is what I have been deeply wrestling with for the last four years. I can see this train coming, and I want to get on it, not be run over by it. I am afraid most people will be run over it before they eventually climb on board, but with their assets much reduced. They will suffer this fate because they believe the future will play out like the past.

We need, instead, to restructure our portfolios to make sure we get as much of our wealth as we possibly can to the other side of the coming crisis, because afterward, I believe, we will see the greatest bull market of our lives. We just have to get there with our assets intact.

Let me offer the usual caveat/warning: This is my personal opinion based on my own analysis. There is no guarantee that Im right. We are talking about an unknowable future. Many knowledgeable investment professionals will strongly disagree with me.

That said, you and I have to decide how we will approach that future. These are my thoughts, so lets dive in.

The Great Reset

We are coming to a period I call the Great Reset. As it hits, we will have to deal, one way or another, with the largest twin bubbles in the history of the world: global debt, especially government debt, and the even larger bubble of government promises. We are talking about debt and unfunded promises to the tune of multiple hundreds of trillions of dollars vastly larger than global GDP. We are also going to have to restructure our economies and in particular how we approach employment because of the massive technological transformation that is taking place. But lets keep the focus for now on global debt and government promises.

All that debt cannot be repaid under current arrangements, nor can those promises ultimately be kept. There is simply not enough money and not enough growth, and these bubbles are continuing to grow. At some point, were going to have to deal with these issues and restructure everything.

Now, people have been saying that for years. Remember Ross Perot and his charts in the early 1990s? Weve all heard the doom and gloom predictions of the demise of civilization that will be brought on by our Social Security and/or healthcare and/or pension problems.

And yet, these are real problems we must face. Facing them wont be the end of the world, but it will mean we must forge a different social contract and make changes to taxes and the economy. That said, the day of reckoning is not here yet. We have time to adjust and prepare. But I believe that within the next 510 years we have to confront the ending of the debt and government promises supercycle that has been developing since the late 1930s. This is a global problem, but it will be felt most acutely in the developed world and China. The developing and frontier markets will be radically affected as well, but mostly by fallout from the impacts on the developed world.

There has been no instance in history when too much debt didnt eventually have to be dealt with. The even more massive bubble of government promises will have to be dealt with, too. We need some realistic way to decide how to meet those promises, or at least the portion of them that can be met.

For the record, what I mean by government promises are pensions and healthcare benefits in all their myriad varieties. Governments everywhere guaranteed these benefits assuming that taxes would cover their immediate costs and future politicians would figure out the rest. Now the time is rapidly approaching when those future politicians are the ones we elect in the here and now.

What Happened to Deleveraging?

Typically, after a significant recession there is a deleveraging of society. Thats certainly what many expected in 2009. Individuals in some countries did in fact reduce their debts, but not governments and corporations, or most individuals outside the US.

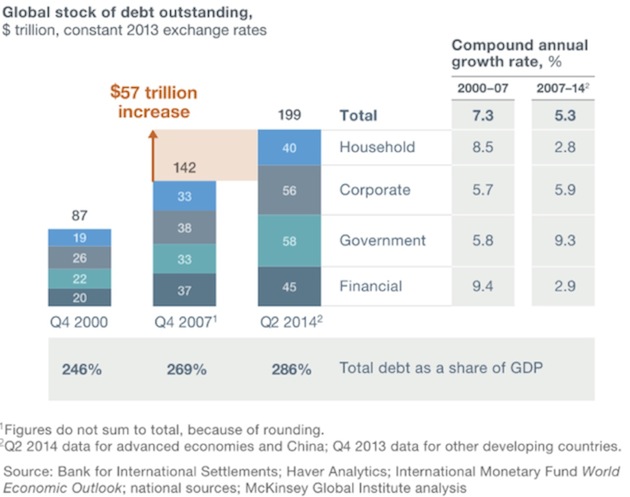

That the world is awash in debt is not exactly news. As of 2014, total global debt had risen to $199 trillion, growing some $57 trillion in just the previous seven years, about $8 trillion a year. The McKinsey Institute chart below shows 22 advanced and 25 developing countries that make up the bulk of the world economy. The chart illustrates how the debt is split among household, corporate, government, and financial sectors:

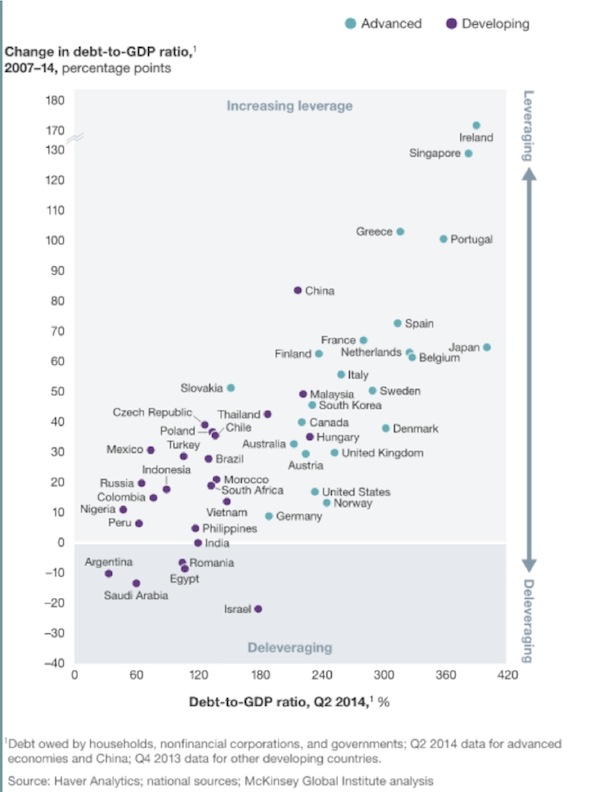

The debt-to-GDP ratio increased in all advanced economies from 2007 through 2014, and the trend is continuing. Heres a chart for the advanced and developing economies:

Since that 2014 report was published, global debt rose by $17 trillion through 3Q 2016. In fact, in the first nine months of 2016 global debt rose $11 trillion! After averaging a little over $8 trillion from 2007 through 2014, global debt growth is now accelerating. Global debt-to-GDP is now 325%, though it varies sharply by region and country.

More worrisome is that interest rates are slowly rising pretty much everywhere, so debt-servicing costs are rising, too. In the US, according to a note sent to me recently by my friend Terry Savage,

Interest on the national debt is the third largest component of our annual Federal budget after social programs and military spending. In the most recent fiscal year, we paid $240 billion in interest on the national debt. That was a relatively low cost, because the Fed has kept interest rates artificially low for years as savers can attest.

Now, with the Fed hiking rates, interest costs are set to soar. The Congressional Budget Office estimates that every percentage point hike in rates will cost $1.6 trillion over the next ten years! And thats without adding to the debt itself every year, by running budget deficits.

That 1% rate hike will take roughly an additional 3% of our current tax revenues every year. Governments must cover higher interest costs with additional taxes, lower spending, or an increase in the deficit (which means more total debt and even more interest rate cost). Of course, higher interest rates affect more than just government interest rates. Many of us have adjustable-rate mortgages and other loans with floating interest rates.

It is not just the US that faces a serious debt problem. Global GDP is roughly $80 trillion. If interest rates were to rise just 1% on our global debt, an additional $2 trillion of that GDP would go to pay that debt increase, or about 1.5% of global GDP. As we have discussed many times, debt is a limiting factor on future growth. Debt is future consumption brought forward. Repaying that debt requires either reduced future consumption or some kind of debt liquidation those are the only choices.

Debt has additional consequences. I have highlighted research from my friends Lacy Hunt and Van Hoisington that correlates increased total debt with slower overall growth. The graph below from Hoisington Investment Management shows total debt as a percentage of GDP for the major developed countries.

Note that Japan, with by far the highest debt-to-GDP ratio, is growing slower than Europe, which is growing slower than the US. Chinas debt is rapidly overtaking the USs debt, and at its current growth rate it will soon overtake Europes. The grand Chinese debt experiment will eventually reveal the true linkage between the size of debt and growth.

Unfunded Liabilities

A Citibank report shows that the OECD countries face $78 trillion in unfunded pension liabilities. That is at least 50% more than their total GDP. Pension obligations are growing faster than GDP in most of those countries, if not all. Those are obligations on top of their total debt.

By the way, most of those pension obligations are theoretically funded from future returns, which are going to be sparse to nonexistent. That means obligations are compounding significantly faster than the ability to pay them. Without serious adjustments to either benefits or funding, there is literally no hope of catching up.

Thought exercise: In European countries where taxes are already more than 50% of GDP, where will they find an extra 510% to meet those future pension obligations? How long will younger generations tolerate carrying older generations when the government is taking two thirds of their paychecks? You can begin to see the scope of the problem.

Sometime this year, world public and private debt plus unfunded pensions will surpass $300 trillion not counting the $100 trillion in US government unfunded liabilities. Oops.

These obligations simply cannot be paid. A time is coming when the market and voters will realize that these obligations cannot be met. Will voters decide to tax the rich more? Will they increase their VAT rates and further slow growth? Will they reduce benefits? No matter what they decide, hard choices will bring political turmoil, which will mean market turmoil.

The Unthinkable Recession

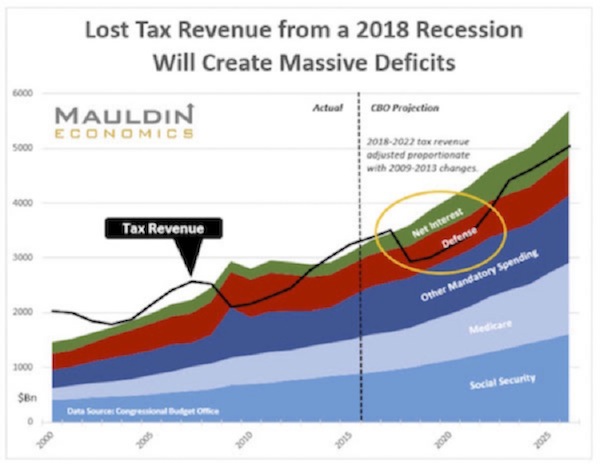

History shows it is more than likely that the US will have a recession in the next few years, although one doesnt appear to be on the near horizon. But when it does come, it will likely blow the US government deficit up to $2 trillion a year. Obama took eight years to run up a $10 trillion debt after the 2008 recession. It might take just five years after the next recession to run up the next $10 trillion. Here is a chart my staff created in late 2016 using Congressional Budget Office data, showing what will happen in the next recession if revenues drop by the same percentage as they did in the last recession (without even counting likely higher expenditures this time). And you can add the $1.3 trillion deficit in this chart to the more than $500 billion in off-budget debt, plus higher interest rate expense as interest rates rise.

Whether the catalyst is a European recession that spills over into the US, or one triggered by US monetary and fiscal mistakes, or a funding crisis in China, or an emerging-market meltdown, the next recession will be just as global as the last one. And there will be more build-up of debt and more political and economic chaos.

President Trump is a fairly controversial figure, but I think most of us can agree that Trump is going to make volatility great again. The Great Reset will bring an increase in volatility, and the correlation among asset classes will once again approach 1.0, as it did during 20082009.

If Im right about the growing debt burden, the recovery from the next recession may be even slower than the last recovery has been unless the recession is so deep that we have a complete reset of all asset valuations. I dont believe politicians and central banks will allow that. They will print and try to hold on as long as possible, thwarting any normal recovery, until markets force their hands.

But then, I can think of at least three or four ways that politicians and central bankers could react during the Great Reset, and each will bring a different type of volatility and effects on valuations. Flexibility will be critical to successful investing in the future.

(Next week, in part two, we will deal with two other major problems in putting portfolios together, but todays letter is long enough. I will wrap up with just a few comments and an offer.)

How Should We Then Invest?

So lets sum up. In my opinion, the entire world is entering what I call the Great Reset, a period of enormous and unpredictable volatility in all asset classes. I believe that diversifying among asset classes will simply diversify your losses during the next global recession. And yet, active management seemingly has not been the answer. So what do we do?

I think the answer lies in diversifying among noncorrelated trading strategies that can invest in any asset class. For a reasonably sophisticated investment professional with sufficiently high assets, there are any number of ways to diversify trading strategies.

Up to this point, Ive talked philosophy rather than action. Now I will tell you how I intend to diversify trading strategies and give you a link to the actual strategies and managers I will be using. Some will not agree with the philosophy outlined above, some will think they can do a better job themselves. However putting on my entrepreneurial business hat my hope is that some of you will join me.

Back in the day, I allocated money to asset managers who traded mutual funds and did so successfully. Unfortunately, the rules changed to make active trading of mutual funds difficult, which significantly reduced return streams. But the growth of money in exchange-traded funds (ETFs) changed things again. Globally, there is now about $4 trillion in ETFs. There are almost 2000 ETFs in the US alone, and according to ETFGI there are 4,874 ETFs globally, with assets skyrocketing from $807 billion in 2007 to $4 trillion today.

You know how somebody will talk about getting a time-consuming task done and then the next person says, Theres an app for that? No matter what asset you want, theres now an ETF for that. I am constantly amazed how narrowly focused ETFs can be. There is now an ETF that focuses its investments just on companies in the ETF industry. Its not all large-cap-index ETFs anymore. Some really small, niche-market ETFs have attracted significant capital.

Not surprisingly, a growing number of asset managers actively trade ETFs using their own proprietary systems. I began searching for the best of them some three years ago. I soon realized, for reasons I will explain in a white paper, that a combination of several managers is much better than just one. I have assembled a portfolio of four active ETF asset managers/traders with radically different styles. That approach theoretically gives me the potential for much less volatility than each managers system would face individually. The combination Ive put together has been less volatile historically than the markets, over a full cycle.

Part of my edge is that I have been in the manager of managers business for more than 25 years, looking at hundreds of investment managers and strategies. That has actually been my day job when Im not writing. So when a manager explains his system to me, I can see how it fits with those of other managers, understand whether it is truly different, and finally, determine whether it would add any benefit to my total mix. Ive also learned that having more than the optimal number of managers doesnt necessarily improve overall performance, but it does add complexity and increase trading costs.

Introducing Mauldin Solutions Smart Core

I believe passive investment strategies will come under severe pressure in the coming years. Many investors have their core portfolios in these passive strategies. If you are prepared to ride out another 200102 or 200809 and then go through what I think will be an even longer and weaker recovery (until the debt issue is resolved), then stick with your passive strategies. But if youre looking for another option, let me offer you one.

My investment advisory firm is called Mauldin Solutions, LLC. I am calling the ETF trading strategy I have developed the Mauldin Solutions Smart Core. I dont think of it as an alternative investment for a sliver of your total portfolio. Rather, I think it can become a significant part of your core portfolio.

Now, what the size of your core portfolio should be depends on many factors. That is something you should discuss with your investment advisor or counselors. (I think most investors should have an investment advisor and financial coach for tax strategies, retirement planning, estate planning, budgeting, and more. Im not looking to become your financial advisor. I want to provide you and your advisor with an easily accessible strategy.)

For regulatory reasons, I cant go into too much more detail in this letter. If you would like to know which managers Ive chosen and what they do, go to www.mauldinsolutions.com and read a summary and then a more detailed white paper.

Mauldin Smart Core is now available on a growing number of platforms where we trade directly for larger investors and brokers and advisers. We also have a mutual fund that I will tell you about in the free white paper that is available now on most of the popular platforms.

I have assembled a professional team to help you get your questions answered. We are especially looking for investment advisors and brokers. While we are just in the US at this moment, we will soon be available in most parts of the world. I am amazed at how technology allows us to do that today.

For those of you in Europe, creating a UCITS around this product is fairly simple, and we intend to do that. If you are in a country other than the US, then come to the website, give us your name and email address. If you are an investment firm that would like to partner with us, make sure that you put that in the note, and somebody from my Mauldin Solutions team will get back to you. If you are an institution, pension fund, insurance company, bank or family office, you have your own special place to register on the website. With the team and partner companies Ive assembled, I can structure almost anything you might want to satisfy your needs. The white papers will discuss fees and what you need to do to compare this strategy with those of other active managers. They will also show you how Mauldin Smart Core can fit into your own personal strategy.

When you go to the Mauldin Solutions website, the rules require me to gather your name and a little bit of information about you. If you would like, we can send you free regular updates from Mauldin Solutions so that you can follow our work as we continue to parse this remarkable economy. Mauldin Solutions will also issue regular portfolio strategy letters, along with the letters of my partners/strategists. And we can keep you updated on additional offerings and portfolio strategies that I think will enhance your portfolio opportunities if you sign up through the Mauldin Solutions website.

Click on this link to let me show you what Mauldin Solutions can do for you.

Orlando and SIC

I leave on Sunday for Orlando and the Strategic Investment Conference. There is so much last-minute preparation to do that I think I will just hit the send button without sharing much in the way of personal thoughts today. But do follow me on Twitter, as I will be posting ideas from the conference.

And you know you want to see what Im doing with Mauldin Solutions. So click on the link, and take your time reviewing the white paper created just for you.

Your pumped about the conference analyst,

John Mauldin

subscribers@MauldinEconomics.com

| Digg This Article

-- Published: Tuesday, 23 May 2017 | E-Mail | Print | Source: GoldSeek.com