-- Published: Sunday, 4 June 2017 | Print | Disqus

By John Mauldin

Centenarians Everywhere

The $400 Trillion Gap

A Wedding and the Virgin Islands

I often joke that 100 years from now I hope people are saying, Dang, she looks good for her age!

Dolly Parton

Just because you live 20 years or 100 years doesnt make it less meaningful. Theyre both short amounts of time. So all we can do is just live in that time, whatever time were given.

Ansel Elgort

If I had more time, I would have written a shorter letter.

Blaise Pascal, 1657 (and a few score other later attributions)

Welcome to the new, improved, faster-to-read, better yet still-free Thoughts from the Frontline. My team and I have been doing a lot of research on what my readers want. The reality is that my newsletter writing has experienced a sort of mission creep over the years. Bluntly, the letter is just a lot longer today than it was five or ten years ago. And when Im out talking to readers and friends, especially those who give me their honest opinions, they tell me its just too much. There are some of you who love the length and wish it were even longer, but you are not the majority. Not even close. We all have time constraints, and I wish to honor those. So I am going to cut my letter back to its former size, which was about 50% of the length of more recent letters. (Note: this paragraph is going to open the letter for the next month or so, since not everybody clicks on every letter. Sigh. Surveys showed us its not because you dont love me but because of demands on your time. I want you to understand that I get it.) Now to your letter

This week I have good news and bad news for you. The good news is that you and your children will probably have much longer lives than you currently imagine. The bad news is that youll have to pay the bill for them.

Ill explain what that means in a minute. First, let me thank everyone who helped produce this years Strategic Investment Conference, as well as all who attended. I know it sounds trite to say that this one was the best ever, but it really was. Every speaker brought a unique and valuable perspective, which the panels then mixed into new and even more interesting blends. Attendees asked probing and sometimes uncomfortable questions. I think everyone left Orlando bearing loads of new ideas.

If you missed SIC, you can still get our Virtual Pass. It gives you audio recordings of all sessions, all the slides that accompanied them, and written transcripts. Its the next best thing to being there. Click here for more information and to place your order. We will close this offer in early June, so dont wait too long.

Im also pleased to announce that next year were taking SIC back to our old home at San Diegos Manchester Hyatt. The dates are March 69, 2018. Thats just a little more than nine months away, so now is the time to start planning your trip. Well let you know when early bird registration opens in the fall.

Now, on to this weeks main course.

Centenarians Everywhere

One of my team members pointed me to a World Economic Forum white paper called Well Live to 100 How Can We Afford It? Regular readers know Ive been saying well live that long and asking how well pay for it for several years now. It is good to see Davos Man finally catching up with me.

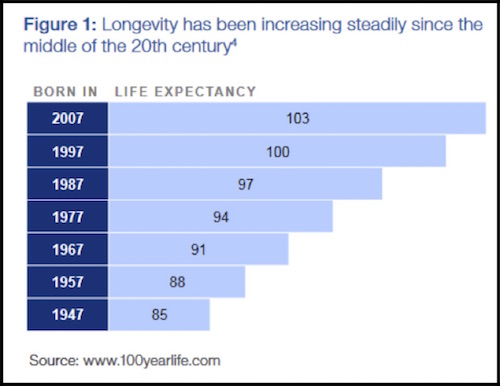

The WEF paper has some interesting data that I havent seen elsewhere. To begin, it breaks down life expectancy by birth year, showing a different picture than we see from simple averages. Here are the global numbers.

As far as I can tell, these estimates dont consider the kind of major life-extending breakthroughs that Patrick Cox writes about for us and that he and I both expect to be realized in the next few years. Rather, the methodology of the WEF paper seems to depend on extending current trends. So I believe the numbers above are conservative.

Note also, these are median life expectancies, not simple averages. Half the people in each group will live longer than the median. Most of todays young children will live to see the 2100s. Some (many?) of the younger Millennials will see their lives span three different centuries. Thats astonishing.

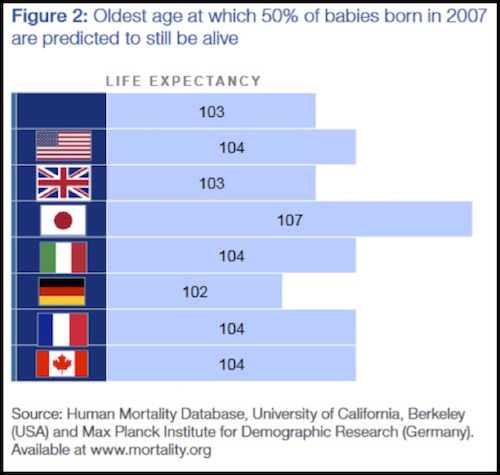

Heres another table showing the differences among major countries for those born in the year 2007.

Again, this is astounding if correct. A Japanese child born in 2007, who is 10 years old today, has a 50% chance of living to 107. That will be the year 2114. Those in other developed countries are not far behind.

Better yet, the coming medical technologies will let us live to those ages or more without the decades of physical and mental decline that are now common. Were not just increasing lifespans; were increasing health spans, too.

The good news is that many of those antiaging breakthroughs are going to be coming to a pharmacy near you in the near future as in five to ten years. It is likely that you will live much longer and healthier than you are currently planning to. Most of us will be happy with that outcome. The bad news is that you will have to make your money last those extra years.

We had a panel at SIC with Patrick Cox and leaders of three of the biotechnology companies he follows. What theyre working on, from different angles, is almost unbelievable. It is entirely possible that we will see cancer wiped out in the next five years. Scientists are making huge strides with heart disease, dementia, spinal cord injuries, and the other great enemies of life and health. One by one, the dominoes are falling. Other companies we know about are working on the Fountain of Middle Age, whereby they intend to either delay or semi-reverse the aging process. It wont take you back to your youth, but for many of us 50 years old sounds pretty good.

And there are groups like Mike Wests at BioTime, Inc., that are working on technologies like induced tissue regeneration (ITR), which will literally turn back your cellular clock. This was science fiction and a pipette dream 10 years ago. Today it is simply science, and its coming out of the theoretical stage and the petri dish and moving further up the experimental lab chain.

Some of you will object, What will we do if everybody lives so long? Frankly, thats a first-world problem. I see very few people who ask that question offering to die. If we live in a world that can figure out how to turn us young again, give us automated cars, and all sorts of abundant resources, you think well have trouble figuring out how to feed everyone and keep them occupied? Malthus was so wrong in so many ways.

The $400 Trillion Gap

While this is wonderful news for humanity, it will bring some challenges, too. The world is not financially prepared to support as many retirement-age people as it will have to sustain in coming decades. We have some huge adjustments in store.

Specifically, we already have a huge retirement savings shortfall, both public and private. I discussed that problem at length recently in Part 4 and Part 5 of my Angst in America series. Adding millions more person-years to the equation will make the problem much worse.

The World Economic Forums white paper tries to quantify how much worse the personal retirement shortfall will be if current practices continue. The amounts presently earmarked for retirement income via government-provided pension systems (i.e., Social Security), employer plans, and individual savings fall far short of the mark.

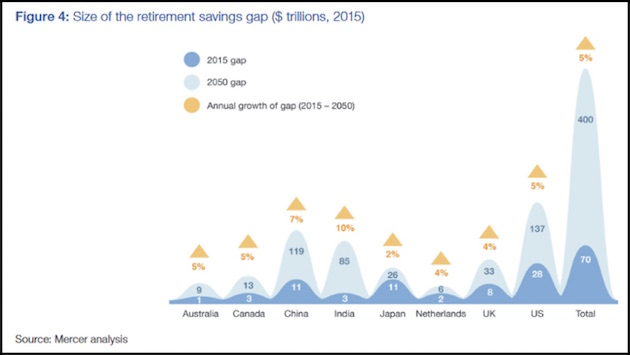

Here is the bad news in graphic form.

The bumps you see there are the difference between what is necessary to fulfill obligations (defined as 70% of pre-retirement income) and what has actually been saved or set aside to do so. The darker blue is the 2015 gap, and light blue is a 2050 estimate.

WEF shows these eight countries, which are obviously not the whole world, simply because the data was available. They also excluded assets held by the wealthiest 10% of the population, in order to show the situation of non-wealthy citizens. (Their full methodology is described on page 22 of this PDF file, for those of you who want to take a deeper dive.)

By 2050, the total shortfall in these eight countries alone will be $400 trillion. That number is so absurd that I feel very confident we will never have to face it. One way and another, some promises will be broken. The only questions are, whose and to what degree.

Remember, this is just the personal savings shortfall. This is not the government and unfunded liability shortfall. Globally, that runs into the multiple hundreds of trillions on top of the $400 trillion savings shortfall.

The present standard of retiring somewhere between ages 60 and 70 is not going to be sustainable when half the population lives to 80 or 90 which is already realistic today let alone 100 or more. Its just not possible. If youre like me, you dont intend to retire at 70 or maybe not at all, but its nice to know we have the option. Future generations wont.

According to WEF, the global dependency ratio under current policies will plummet from 8:1 today to 4:1 by 2050. That means just four active workers for each retiree. And thats including developing and frontier markets. Developed markets will see a global dependency ratio of about 2:1. I see no way that can work. WEF doesnt either. Here is their advice to political leaders.

Given the rise in longevity and the declining dependency ratio, policy-makers must immediately consider how to foster a functioning labour market for older workers to extend working careers as much as possible.

There you have it, straight from Davos. We must extend working careers as much as possible. Your dream of hanging up the work clothes at 65 and going on extended vacation will remain a dream until some later date. Early retirement will survive only for the kind of people who go to Davos.

Again, for me this is fine. Im 67 and I love my work. I plan to keep at it for many years to come. But I understand many people dont have that option. They have health problems, or their professions are being automated, or they spent their career doing physical work that is no longer possible. The medical advances I foresee will help, but theyll take time to become affordable to everyone. Some people are going to fall through the cracks.

Moreover, simply saving more money probably isnt an answer, either. Interest rates are a function of supply and demand. You cant invest your savings in a high-yield bond unless someone out there can borrow at that same yield. When so many of us want to lend and no new borrowers appear, supply and demand will keep yields low. We already see this in todays near-ZIRP conditions, and they may not improve much.

Part of the justification for ZIRP was that it would force capital into risk assets, thereby stimulating the economy. It now appears that the only thing stimulated was asset prices, and by and by the risk is going to catch up with those taking unwise amounts of it. That unhappy outcome will likely widen the retirement shortfall even further.

And so the expectation of longevity is going to motivate people to want to save more money, except theyll have to have jobs that pay enough to enable them to save money to flesh out the retirement plan. This headline appeared a few weeks ago:

Oops. The Council of Economic Advisers now estimates that artificial intelligence will replace 83% of low-wage jobs. Im not certain how they came up with that number it seems high but whatever is the figure turns out to be, its alarming. And the jobs we are creating today are not the high-paying manufacturing jobs that everybody wants to bring back. Theyre not there to be brought back. There is actually a quite large re-shoring movement going on, but the companies that are coming back are doing so with automated technology and far fewer workers than before. The advantage of using inexpensive offshore labor has fallen before the advantage of being close to your markets and employing robots and artificial intelligence.

The McKinsey Global Institute published a report last December that said: On a global scale, we calculated the adoption of currently demonstrated automation technologies could affect 50% of the world economys 1.2 billion employees and $14.6 trillion in wages. That is an astonishing statistic.

By the way, one of the subheads in that screenshot above points out that 61% of financial services positions are at high risk of being replaced. If you are in the financial services industry, maybe you should be thinking about how you can keep from being automated out of a job.

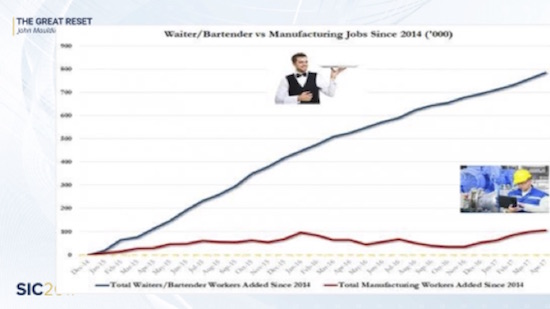

The jobs we are creating? Think 800,000 waiters and bartenders versus 100,000 manufacturing jobs. I have children who work in the food service industry, and I can tell you they are making barely enough to provide for themselves, let alone raise a family or save for retirement.

Officially, the US unemployment rate is 4.3%. There are 200,000+ manufacturing jobs that employers cant find suitable, highly skilled candidates to fill. Last year, the labor force participation rate declined by another 0.2% to 62.7%. The employment-to-population ratio fell to 60%. Fewer of us are working and making enough to actually be able to save for retirement.

In other words, I dont think we can invest our way out of this. The obvious answer extend the retirement age has the unwelcome side effect of reducing job opportunities for younger workers. At some point that might be okay if low birth rates create widespread worker shortages, but the adjustment will take time.

The solution may turn out to be something presently unimaginable. We dont know where technology will take us and what opportunities it will create. We also dont know what political alliances can create. What if the next time around we got not just President Bernie Sanders but a Bernie Sanders-compatible House and Senate? Could we see a wealth tax in addition to a whole slew of other taxes? Would our dear leaders be willing to tax your retirement plan so that people without adequate savings could enjoy a more pleasant retirement? Forget fairness to you as an individual, because they will be arguing about fairness to everyone in the country. Yet today the Republican majority refuses to consider instituting a value-added tax and lowering income taxes and corporate taxes to very low levels. They could do this, because they now have a majority. They are simply afraid of a VAT and are going to find themselves in far less sympathetic hands in a future crisis.

What we do know is this: An unsustainable situation will not be sustained. Retirement as we know it is unsustainable. It will give way to something else, and maybe soon. Frustration is building in America because of the problems I highlighted above, and we could well see an administration and Congress that will push through a much less friendly VAT plus income tax increases, not cuts.

Think it cant happen? When your back is against the wall and youre down to your last few bullets and the enemy just keeps coming, you start to very quickly consider all sorts of options. Within 10 years we are not only going to be thinking the unthinkable, we will be doing the unthinkable. And not just in the US but all over the world. The unthinkable will be coming to a country near you, along with unbelievable science-fiction-grade technology.

Count on it.

A Wedding and the Virgin Islands

Im not doing much traveling this month until Shane and I go to the Virgin Islands the last week of June. On Monday, June 26, she celebrates her birthday. Since I asked her to marry me on her birthday last year, we are going to get married on her birthday this year. Just the two of us on the beach, and the rest of the week relaxing and thinking of the future together. While this approach does allow me to only have to remember one important day rather than two, I am informed by many friends that it does not relieve me of the responsibility to buy two presents.

Shane and I have lived together for four years now, and she has pretty much figured out how I operate. She has amazing forbearance and patience she not only puts up with my peripatetic lifestyle; she even allows me to withdraw into my chair to read or to sit in front of my computer all day writing. Not exactly the most exciting of activities.

We will stay in the Virgin Islands for eight days and then come home to a full schedule. And Im fully committed to begin to bring together the various chapters of my book, The Age of Transformation. That project will hopefully benefit from my new commitment to write fewer words per letter. Maybe I can do that for a chapter or two of the book as well. The reality is that each chapter could almost be a book of its own. I have to make sure I dont get carried away. The book will not be a deep dive but rather a sweeping pass over the transformations that are coming to our world, not just technologically but also socially, demographically, politically, and especially geopolitically. The economic world will be turned upside down as we make decisions to do previously unthinkable things to get clear of the enormous debt burdens and bubbles we created.

And with that I must hit the send button. You have a great week.

Your determined to be more succinct analyst,

John Mauldin

subscribers@MauldinEconomics.com

Copyright 2017 John Mauldin. All Rights Reserved.

| Digg This Article

-- Published: Sunday, 4 June 2017 | E-Mail | Print | Source: GoldSeek.com