-- Published: Monday, 5 June 2017 | Print | Disqus

By David Haggith

These updates to my list of Seven Troubles Assailing the US Economy are far too important to remain buried at the end of that article since many readers may not return to the article to check for updates. The summer economic crisis Ive been predicting is building even more rapidly than when I reported a week ago. Its almost here:

Total household debt now exceeds the peek it hit just before the economic collapse into the Great Recession. While the number of households is also up, wages are correspondingly down, so households have maxed out

again:

Total U.S. household debt was $12.73 trillion at the end of the first quarter of 2017, up $473 billion from a year ago, according to a Federal Reserve Bank of New York survey. Total indebtedness is now 14 percent above the 2013 trough of household deleveraging brought on by the 2007-2009 financial crisis and Great Recession. The previous peak, in the third quarter of 2008, was $12.68 trillion

. Auto loan and credit card delinquency flows are now trending upwards, and those for student loans remain stubbornly high. The survey showed lenders tightened borrowing standards for home and auto loans, a sign of their increased caution. (Newsmax)

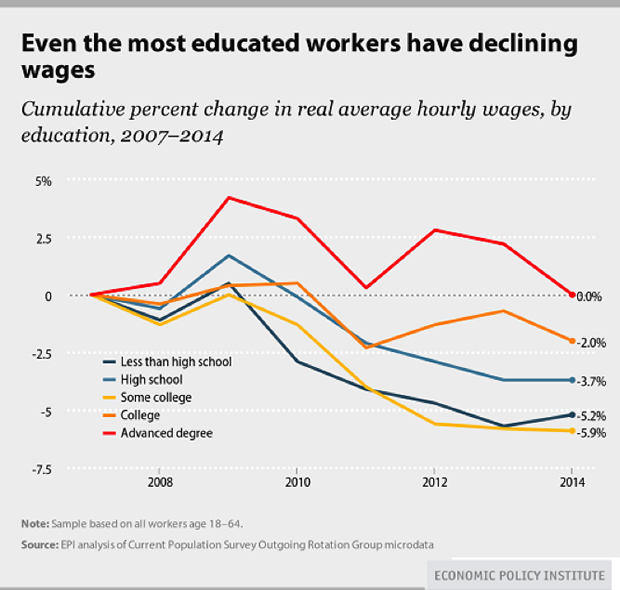

While population rose about 7% between 2007 and 2014, wages for most people have dropped about 5% during that time. (The time frame of the graph above.) Those two changes roughly cancel each other out. With lenders now tightening borrowing standards for mortgages and auto loans out of caution, they are draining liquidity out of those markets. That may be contributing to the decline in those markets as listed above. Lowered liquidity at at time when we are hitting peak debt again are combined factors that will likely keep those markets down.

Housing and all other construction take another big drop as we move into June, following Marchs rise:

U.S. construction spending recorded its biggest drop in a year in April as investment in both private and public projects fell

. The Commerce Department said on Thursday that construction spending tumbled 1.4 percent

. Economists polled by Reuters had forecast construction spending increasing 0.5 percent in April

. In April, private construction spending fell 0.7 percent, also the biggest decline in a year

. Investment in private residential construction fell 0.7 percent after six straight monthly increases

. Investment in residential and nonresidential structures such as oil and gas wells was one of the economys few bright spots in the first quarter. (Newsmax)

So, now, even one of the few bright spots is gone.

Financial stocks have collapsed. Financials, which shot up more than other classes of stocks during the Trump Rally, have already completely collapsed in terms of their rally gains:

Share prices of the biggest U.S. banks reportedly are flirting with bear-market territory amid fears of weak trading revenues and fading hopes for President Donald Trumps ambitious economic agenda.

Goldman Sachs and Bank of America were among the biggest beneficiaries of the stock rally in the weeks after Donald Trumps election victory in November, as investors looked forward to a profit-boosting mix of higher interest rates, lower taxes and lighter regulation, the Financial Timesreported.

But some of those underpinnings have fallen away since then, as Trumps early setback over healthcare policy cast doubt over his ability to implement other promised reforms, the FT explained

.

Bank analysts have been switching blue-sky earnings scenarios of late last year with more cloudy outlooks

. Hopes of corporate tax reform happening any time this year have almost evaporated.

Tax reform was difficult enough in 1986, when you had bipartisan support and an extremely popular president

. Without either, it always looked like a bit of a long shot.

To be sure, in an even more disturbing sign, CNBC reported that the financial sector just gave up all of this years gains, and some strategists say thats sending the broader market a message about the health of the economy. (Newsmax)

Pending home sales also just tanked, taking their biggest drop since August, 2014. Signed contracts fell 5.4% from a year ago.

Auto inventory is back up to its highest point since just before the auto crash in 2007:

With 935,758 unsold GM units collecting dust in dealer lots, this was the highest inventory number in 9.5 years, the highest since Nov. 2007, and, as Bunkley reminds us, one month before the recession officially began. (Zero Hedge)

That was April inventory. Mays inventory, just in, rose by another 30,000 vehicles. When sales stall and inventory backs up, prices collapse under force. Values of used cars collapse, and that means the value of collateral also collapses, making people less likely to maintain their auto loans as the balance on a new loan exceeds the value of the car. The pressure is on for an auto collapse that has been predicted here for some time.

The state of Illinois was just downgraded to the lowest credit rating ever given to a U.S. state (one mark above junk) by Moodys and S&P. The downgrade is due to unrelenting political brinkmanship [that] now poses a threat to the timely payment of the states core priority payments.

That brinkmanship is a just a microcosm of what is going on in the US congress. It is also due to intensifying pressure from pension liabilities, something congress hasnt even begun to address with both government pension funds and Social Security and Medicare. Wait until that battle hits! If Illinois credit gets downgraded to junk, its financial problems instantly rise exponentially.

The retail apocalypse grows: Not even halfway through 2017, closures of retail stores have doubled last years closures as of this time and already exceed the last peak in closures during the crash of 2008.

The bottom line is simple here. Commercial real-estate investment trusts (REITs), malls, mortgage-backed securities (remember those?), and their bankers are in a lot of trouble. The anchor stores are closing up the worst. Because they are vital to a malls success, they will pull others down in the wake by reducing traffic to malls.

Thousands of new doors opened and rents soared. This created a bubble, and like housing, that bubble has now burst. According to Credit Suisse, 20-25% of US shopping malls will shut down within the next five years. While this is due to a paradigm shift in how people do their shopping, not an overall reduction in retail sales, it will send shudders and close shutters throughout real-estate-based retail economy, having a huge impact on construction, land sales, banking, jobs, etc.

Things look even more perilous in the stock market in terms of the CAPE ratio, which measures how pricy stocks are in comparison to their ten-year average. The CAPE just hit thirty, matching the rarified atmosphere of stock prices when the 1929 crash happened! The only time stocks have ever been more overpriced was just before the dot-com crash.

Albert Edwards, global strategist at French bank Societe Generale, said earnings reports for U.S. companies show that their overseas profits have grown but are still falling domestically. The decline may even point toward recession. Domestic non-financial economic profits are really struggling badly and are still down 6 percent year-over-year, Edwards said

. (Newsmax)

The US jobs market finally tanked, coming in at 138,000 new jobs in May, which is near the generally considered recessionary level of 100,000 new jobs. Thats a 32% drop from last month and is much lower than any economists expected (the average expectation being 185,000 new jobs). Previous months were also revised downward. Typical of these massaged job reports, May saw the biggest drop in full-time jobs since June of 2014, and the jobs that came in to replace them were largely part-time, but are counted with the same weight as if a job is a job is a job, regardless of how much less it pays, how much less permanent it is likely to be, how many fewer hours it provides and how reduced or eliminated its benefits.

Even the insanely optimistic Ron Insana said the jobs report could be a worrisome sign of a pronounced economic slowdown, according to Newsmax. Wage data, an area where even the Fed has acknowledged growth is mandatory in order for the economic benefits of recovery to be sustainable, was also softer than expected.

Insana offered a litany of economic omens: looming interest rate hikes, banks pulling back on extending auto credit, soaring housing affordability and softening inflation rates after briefly, and only briefly, touching the Feds 2 percent target

. And, most important, consumer confidence has begun to dip

.

With the Federal Reserve poised to raise interest rates again in June, todays data notwithstanding, and scant fiscal stimulus loaded in the Washington pipeline, this could be the beginning of a worrying trend, he wrote. (Newsmax)

I rarely look to Ron Insana for anything because his permasmile on the economy is always several shades too rosy for my reality glasses. However, when even Insana is starting to read bad news in the tee leaves, you know its getting hard to keep putting lipstick on this pig of an economy.

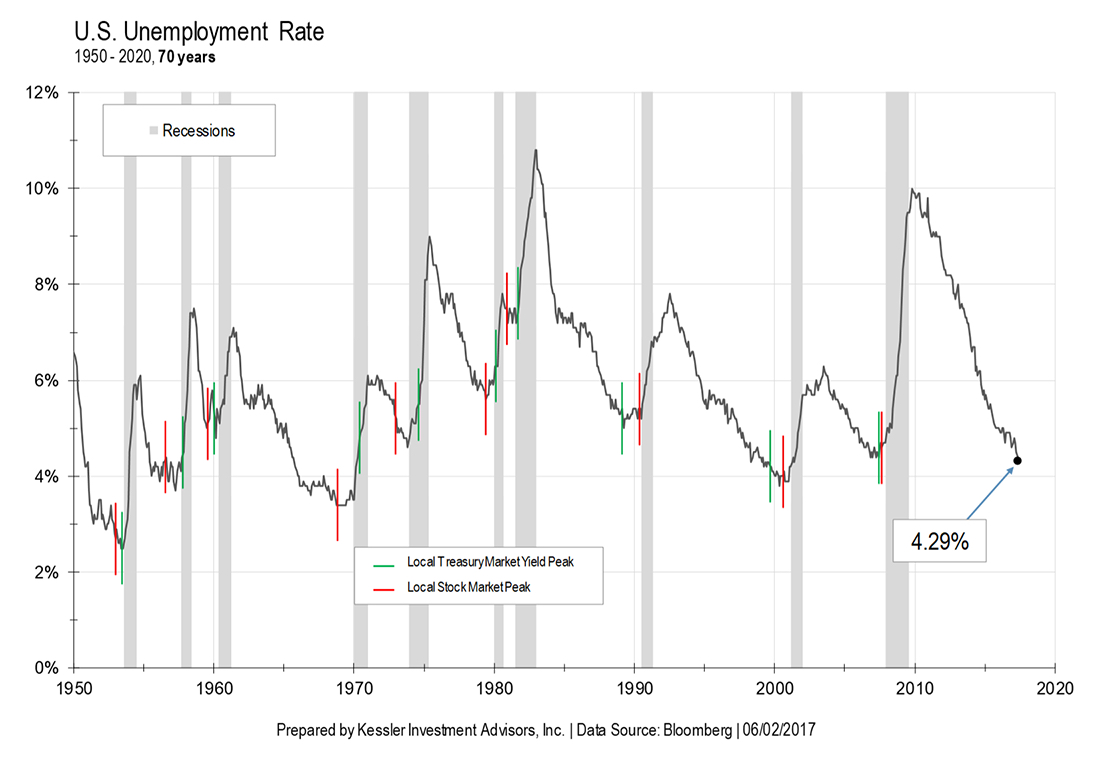

Speaking of the pig, the official US unemployment rate is now exactly at the nadir it has reached right before almost every recession the US has ever experienced:

And those are just the problems inside the US! They dont even begin to include pressures that may arrive from outside, such as Europes rapidly failing banks in Spain, Italy, Greece, and even Germany! Nor the potential capsizing of China over the months ahead as its shadow banking system roles over just as even shadier collateral is called upon in a system that has been rank with corrupt bookkeeping and fake government statistics since Genghis Khan founded the Mongol empire. It doesnt include an implosion of the Canadian housing explosion. It doesnt take into account the possibilities of the land down under turning upside down (as even one of its own famous hedge fund managers has said the Australian stock market and housing market are so insane hes returning all of his investors money as there are no safe bets.)

Conclusion: Fundamentals are falling out RAPIDLY from under the stock market, but the robotraders keep trying to do their relentless programmed job of ratcheting the market up with a million incremental squeezes. Eventually, the falling fundamentals will overwhelm the machines. They will click their last ratchet upward. When they do, I highly suspect these bots that have been designed by programmers who never knew anything but a bull market during their short careers will outbid each other all the way to the bottom unless some human wisely yanks the IT cord on New York Stock Exchange to stop the slaughter.

Even in that case, restarting the stock market the next day will be problematic with all the bots on line and ready to charge downhill in mutual electronic bewilderment. If the bots have failsafes or circuit breakers built into their algos, Im willing to bet those stops perform poorly. So, expect more jolts and plug pullings.

My observation of human-designed failsafes is that the word, itself, should trigger alarms. Failsafes can can be summed up in single words or short names like like Three-Mile Island, China Syndrome, Chernobyl, Fukushima. All things that were human engineered to be beyond failure with all their safety mechanisms. Nature (reality) always finds a way. The slow, crushing collapse of the now-churning economy will overwhelm the algorithms, and I doubt those human replacements will have a clue as to what to do in a bear market. Well be at the mercy of the machines.

Stay in for the ride only if youre good at making money on the ugly because summer is stacking up perfectly for my predictions. (But also note that I have no credentials or license as a financial advisor, so you are responsible to make your own calls. This is just one average Joes opinion who has a habit of seeing which way the wind is blowing when others dont want to see it.)

Once the Feds fake recovery fails, even as it is now crumbling all around us, the true depth of the Great Recession will become known and felt by all

except the 1%. The Fed is knocking the props out from under their own recovery, which was intended to bridge the Great Recession, just as their bridge to nowhere is starting to fall of its own dead weight. They are fitting their old pattern of raising interest rates into a failing economy, something Ive also predicted they would do because they are so good at that. Thus, their next interest raise will also assist the collapse.

http://thegreatrecession.info/blog/summer-storm-keeps-building-second-dip-great-recession-approaches/

| Digg This Article

-- Published: Monday, 5 June 2017 | E-Mail | Print | Source: GoldSeek.com