-- Published: Monday, 12 June 2017 | Print | Disqus

By John Mauldin

Sell to Whom? (Almost) Everything Is Awesome Bending the Yield Curve The Dangers of Passive Investing Getting Married on St. Thomas, Omaha, San Francisco, and Freedom Fest in Las Vegas

Forget the past. The future will give you plenty to worry about.

George Allen, Sr.

I try not to worry about the future, so I take each day just one anxiety attack at a time.

Tom Wilson

Welcome to the new, improved, faster-to-read, better yet still-freeThoughts from the Frontline.My team and I have been doing a lot of research on what my readers want. The reality is that my newsletter writing has experienced a sort of mission creep over the years. Bluntly, the letter is just a lot longer today than it was five or ten years ago. And when Im out talking to readers and friends, especially those who give me their honest opinions, many tell me its just too much. There are some of you who love the length and wish it were even longer, but you are not the majority. Not even close. We all have time constraints, and I wish to honor those. So I am going to cut my letter back to its former size, which was about 50% of the length of more recent letters. (Note: this paragraph is going to open the letter for the next month or so, since not everybody clicks on every letter. Sigh. Surveys showed us its not because you dont love me but because of demands on your time. I want you to understand that I get it.) Now to your letter

The middle ground can be uncomfortable. As someone now widely known as the muddle-through guy, I have learned this the hard way. My bullish friends call me a worrywart, and the bearish ones think I am Pollyanna incarnate.

The irony here is that Ive never claimed to be a great trader or a short-term forecaster. I think I have a pretty good record of calling major turning points. Next week or next month is another matter. Anything can happen, and it probably will.

That said, the fact that my forecast may be wrong doesnt prevent me from making one. So, with all the usual disclaimers, today I will review some recent analysis from my reliable sources and let you take a peek into my worry closet.

One point we all agree on: We live in unusual times.

Sell to Whom?

Last week Doug Kass sent around an e-mail comparing todays markets to Queens classic Bohemian Rhapsody. I know that seems odd, but it was actually a good fit. I shared Dougs full message with myOver My Shouldersubscribers. For everyone else, the point is that, like the song says, Nothing really matters to whoever is buying stocks these days. They just keep buying and pushing prices higher. As Jared Dillian says, Its a bull market, dude! Stock prices do go higher in a bull market; and sometimes, as the end approaches, they make value investors very uncomfortable.

Neither Doug nor I quite understand the Nothing really matters attitude, though we have some theories. Doug is probably more bearish than I am. He has a long list of open questions. I zeroed in on the last one, which is critical: When ETFs sell, who will buy?

The stratospheric ascent of passive indexing is having side effects that I suspect will make markets sick at some point. Passive investing is perverting the financial markets core economic function, i.e., efficient capital allocation. In terms of stimulating buying interest, a companys fundamental business prospects are now much less important than its presence in (or absence from) popular indexes.

Weve created this environment in which badly managed companies can still see their stock prices rise along with those of well-managed companies. The actual facts about a company dont mean all that much in a passive-investing world. Capitalization-weighted indexes aggravate this already problematic phenomenon. Money is pouring into stocks like Apple (AAPL) and Amazon (AMZN) simply because they are big. The resulting higher prices make them bigger still, and they pull in yet more capital. Heres a look at the five largest stocks in the S&P 500.

What about the QQQ or the NDX? The five stocks above represent 42% of the NDX and 13% of the S&P 500. That means every time you buy an index based on the NASDAQ, 42% of your money goes into just five stocks, leaving 58% for the remaining 95. By the time you get past the largest 25, you are under 1% per stock. Apple alone is 12% of the NASDAQ 100 Index and 4% of the S&P 500. That explains, in part, why the NASDAQ has outperformed the S&P 500.

For the record, Goldman Sachs researchers recently released a paper with a strong fundamental forecast for those stocks. That is, they expect them to continue to go up, absent a recession or something else that triggers a bear market. I keep scanning the horizons in every direction, and I just cant see anything that would trigger more than a minor correctiontoday.Of course, a minor correction could deliver outsized impacts, given the heavy weighting of a few stocks and passive index investing. Be careful out there.

Doug asks,When ETFs sell, who will buy? The ETFs of the world may quickly begin trading below their actual net asset values (NAV). This is called price discovery, and the arbitrageurs will not be slow to take advantage of that difference. This means the indexes will drop much faster than they have gone up. I am neither a fortuneteller nor the son of a fortuneteller, but there are a few things Ive picked up along the way. One of them is that, next time, stocks are going to go down breathtakingly fast once they begin to roll over.

This bull cant end well, but it will end. At that point, Dougs question becomes critical: Who will buy? I dont know, but someone will. Prices for goodandbad stocks will drop to whatever levels attract buyers. The indexes will eventually fall lower than any of us think likely right now. Whether that will happen next month, next year, or next decade is anyones guess.

Sidebar: You should think of cash as an option on your ability to buy the stocks that will lose 50% of their value and suddenly become the value stocks of the future. The option value on your cash today is not that much. You dont make much on it, but you dont lose much holding it. The time is going to come when you will be glad you have a little cash to put to work. Think March 2009.

(Almost) Everything Is Awesome

While Doug was musing about Queen, Louis Gave was thinking about rugby. Should one go where the ball is now, or try to figure out where the ball will be?

Louis asks that question while noting that it has been extremely difficult to lose money this year. Almost every tradable asset class has been climbing. You are probably making good returns this yearunlessyou have been:

Overweight energy and materials, and/or

Overweight financials.

Those have been the primary weak spots. Investors in everything from technology to emerging markets, to Europe and even utilities have done well. All you had to do was avoid energy, materials, and financials.

The reasons for this are pretty simple. Inflation remains low to nonexistent in most places, which hurts commodity prices along with companies in the energy and materials sectors. The widespread belief that inflation will stay low is keeping long-term bond yields low, which reduces the net interest margin for lenders, particularly banks. Hence, we see underperformance in financial services stocks, too. Further complicating the energy story is the continued expansion of unconventional shale oil production in the United States. Eventually the technology will spread to the rest of the world. Countries that depend on high oil prices are hurting. (And not just Saudi Arabia and Russia but a whole host of Middle Eastern countries).

The conditions that will change this pattern arent complicated: higher inflation expectations and rising long-term bond yields. That combination would push energy and metals prices up and steepen the yield curve. But the problem there is that the Federal Reserve remains intent on raising short-term rates. If they tighten another notch next week, as everyone expects, the current trends seem likely to continue. Heres Louiss conclusion:

In sum, it is hard to foresee what will disturb the current Goldilocks scenario. So, investors who liken themselves to Rugby forwards (aka piggies) [an actual rugby term that is a double-play pun on investors getting greedy and hungry JM] will want to continue dining at the trough of the current bull market. Meanwhile, investors who like to get their hair blow-dried before games (backs, or princesses), and prefer to run where the ball is going to be rather than where it is, may want to look at reducing their underweights in financials. After all, at current global fixed income valuations, it wouldnt take much central bank hawkishness, upside surprises to core CPI to trigger a mild fixed income sell-off. And any steepening of the yield curve would lead to a very different investment environment.

The shape of the yield curve is clearly critical in assessing markets right now. I agree with Louis that any steepening would lead to big changes. I wonder if we might get a steepening theotherway: An inverted yield curve when short-term rates are higher than long-term rates is a classic recession indicator. Its something the US hasnt seen lately but cant avoid forever.

How can we get an inverted yield curve with short-term rates so low? The Federal Reserve just slowly and surely raises rates; the weight of debt begins to slow economic growth even more; and long-term rates drop. Voilà, inverted yield curve. That is at least classically what is supposed to happen. So lets think about that for a few paragraphs.

Bending the Yield Curve

The other much-anticipated news from next weeks FOMC meeting is how/when the Fed intends to start reducing the massive bond portfolio it accumulated during the QE years. The initial move may be simply to stop reinvesting the proceeds when bonds mature. That is still billions of dollars each month enough for even the very deep Treasury bond market to notice. (Then again, maybe they just let their mortgage bonds roll off and keep buying the Treasuries. They have so many options, and they havent bothered to tell us which ones they are seriously considering.)

A little-discussed aspect of this situation is, who will buy the Treasury bonds once the Fed backs out? That part is beyond the Feds control. The federal government wont stop borrowing just because the Fed stops lending. The Treasury will have to find other buyers for its paper and will likely pay higher rates to attract them. Maybe. That is what is supposed to happen. In a world where the unthinkable keeps happening, well just have to wait and see.

Brevan Howards chief US economist, my friend Jason Cummins (a past SIC speaker, I should note) wrote a fascinatingguest columnin theFinancial Timeson this topic. He points out something quite obvious that hasnt occurred to many. The Treasury Department must borrow enough cash to pay the governments bills, but it has huge discretion as to how it structures federal debt.

That means Treasury Secretary Steve Mnuchin can choose to replace the Feds purchases by issuing new debt at any point on the yield curve. It doesnt have to be of the same term as the maturing paper it replaces. He can issue thirty-year bonds, three-month bills, or anything in between, in whatever combinations he thinks best.

The implication, as Jason gently explains, is that Steve Mnuchin can essentially rebuild the yield curve into whatever shape he wishes presuming he can find buyers. He always will, of course, at some price.

The Treasury is such a massive borrower that its entry at any given maturity level can crowd out other borrowers and force rates higher. I am sure the Treasury people who manage this process try to reduce interest expense as much as possible, but they can only do so much. The government has bills to pay.

If Mnuchin decides to concentrate new borrowing at the long end, it will drive up those yields and steepen the yield curve. Thats exactly what banks would like to see. That would enhance their profit margins but with the possible outcome of raising mortgage and other long-term rates. Not good for the housing sector.

Or, Mnuchin could do more borrowing at the short-term end. That would be a bit of a gamble because theres no way to know what rates will be when the debt matures in the relatively near future. The strategy would also flatten and possibly even invert the yield curve.

Just to make all this more suspenseful, the government is also bumping up against its statutory debt ceiling. Congress might have to approve an increase as soon as August, and some in the House want to use the opportunity to exact spending cuts. The odds are low, but we cant rule out the possibility of another government shutdown scenario, as we saw in 2011 and 2013.

As Cummins noted, As the clock ticks down and investors get increasingly skittish, the last thing the Treasury needs is to have to find more private sector buyers of its debt. Agreed. That is why I expect the Fed to delay implementing its balance sheet reductions until after the debt ceiling is raised or maybe longer, if employment growth and/or inflation weaken over the summer and fall.

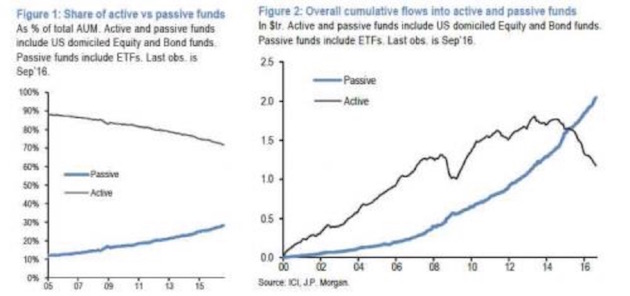

Before we end, I want to come back to a few charts that illustrate some of the problems that are building up in the passive index world. It is not just ETFs, but also index mutual funds and the enormous amount of pension and insurance funds, along with many trust funds, that are passively invested directly in stocks. They simply duplicate indexes.

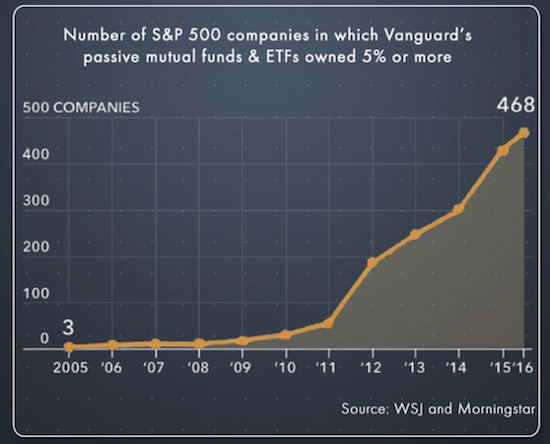

First, lets note that Vanguard now owns more than 5% of 468 stocks in the S&P 500. Thats one fund company.

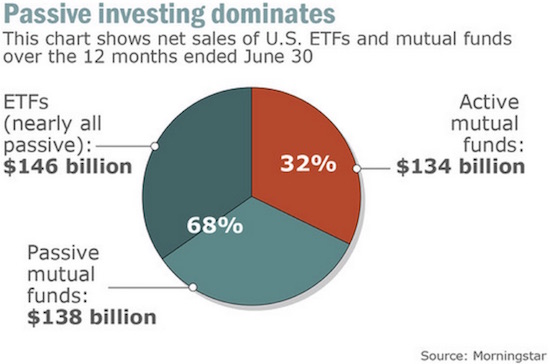

Heres the picture for fund flows last year:

The number of hedge funds is at its lowest level since 2000. Passive funds are eating away at the assets under management by active funds:

This trend goes back to a point I made a few weeks ago but that needs to be repeated again and again. When the market obscures distinctions between good stocks and bad stocks because it buys all of them at the same time, there is no way for an active manager to take advantage of his skill in determining value. That ability to look at a companys balance sheet and determine something close to true value is what gives active managers their edge. If you dont have the chance to do this, you cannot add any alpha, and you are going to underperform the simple passive indexes even though you charge higher fees. Money will leave you for the seemingly more plentiful pastures of passive indexing. One day you will be vindicated, and the money will come back (think Jeremy Grantham); but because investors will lose a great deal of their money in a bear market, you wont get as much back in the short term as left you over the past few years. If you are an active manager, this just sucks.

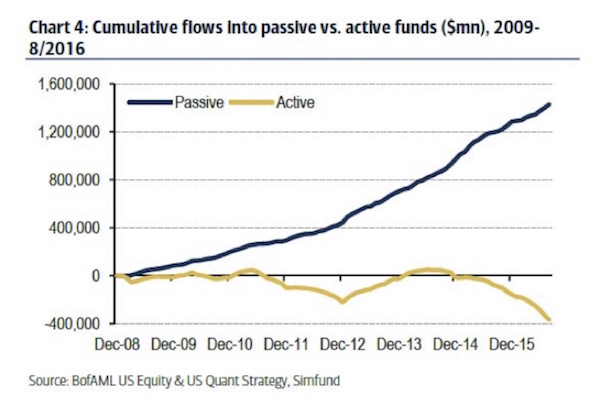

The next two charts show the difference between active and passive investing in the retail fund space. Its a huge contrast:

The chart below traces the widening imbalance since 2008.

As I stated above, this imbalance will eventually be corrected. But the correction will not be pretty, though it may be swift.

If Im going to keep my pledge to be shorter, more thoughtful, and faster, then Id better close on that note.

Getting Married on St. Thomas, Omaha, San Francisco, and Freedom Fest in Las Vegas

Shane and I will be leaving for St. Thomas on 24 June, and we will be married on some beautiful beach on June 26, her birthday. Then I actually intend to relax for a week, enjoying time with my new bride and reading books with no redeeming social value (also known as science fiction/fantasy). I will begin final writing on my new book when I come back. I am finally really ready to attack the topic of what the world will look like in 20 years.

I have a quick trip to Omaha in the middle of June, then Ill head directly on to San Francisco and Palo Alto for speaking engagements, come home to Dallas, recover for a few days, and then leave with Shane to go to Las Vegas for the Freedom Fest. It has become one of the largest libertarian gatherings, and I have so many good friends who go that its really a lot of fun for me. And while I am not much of a gambler (as in I suck at it and hate losing money to people who are much richer that I am), I really do like the shows. And dinners with friends.

That covers July, and August is, of course, the annual Maine fishing trip, but right now the rest of August looks to be pretty wide open. If I can figure it out, I may go somewhere that has a much cooler climate than Texas does in August and relax and write.

I will be cooking a chili dinner along with some prime this week for a dozen or so investment advisors who will be coming to Dallas to learn about my new Mauldin Solutions Smart Core investment program. For those of you have not yet gone towww.mauldinsolutions.comand given me a little bit of information about you, we have a white paper we would like to send to you, and there is other information on the website that will give you an idea as to how I think core portfolios should be structured in todays world. Whether you are an individual or a professional or an institution, the principles are the same.

And with that I will hit the send button. You have a great week.

Your not going passively into the next bear market analyst,

The content on this site is protected

by U.S. and international copyright laws and is the property of GoldSeek.com

and/or the providers of the content under license. By "content" we mean any

information, mode of expression, or other materials and services found on GoldSeek.com.

This includes editorials, news, our writings, graphics, and any and all other

features found on the site. Please contact

us for any further information.

Live GoldSeek Visitor Map | Disclaimer

The views contained here may not represent the views of GoldSeek.com, Gold Seek LLC, its affiliates or advertisers. GoldSeek.com, Gold Seek LLC makes no representation, warranty or guarantee as to the accuracy

or completeness of the information (including news, editorials, prices, statistics,

analyses and the like) provided through its service. Any copying, reproduction

and/or redistribution of any of the documents, data, content or materials contained

on or within this website, without the express written consent of GoldSeek.com, Gold Seek LLC,

is strictly prohibited. In no event shall GoldSeek.com, Gold Seek LLC or its affiliates be

liable to any person for any decision made or action taken in reliance upon

the information provided herein.