-- Published: Thursday, 13 July 2017 | Print | Disqus

By David Haggith

One of the kookiest moments last month came when Fed Chairwoman Yellen spoke about seeing no financial collapse in sight during our lifetimes

Would I say there will never ever be another financial crisis? No. Probably that would be going a little too far, but I do think that were much safer, and I hope that it will not be in our lifetimes, and I dont believe it will be. (CNBC Play video for quote on next crisis.)

That certainly calls to mind the times when Chairman Ben Break-the-banky pontificated about there being no housing bubble and no recession in sight:

Yellens predecessor, Ben Bernanke, once famously called problems in the subprime mortgage market contained, a statement that would be proven wrong when the collapse of illiquid mortgage-backed securities cascaded through Wall Street and contributed to the worst economic downturn since the Great Depression.

Asked at a recent FOMC meeting about any possible problem with banks still being too big to fail, Yellen only said, Im not aware of anything concrete to react to.

Nice to know shes sound asleep while sugar plums dance in her head, bringing forth prophecies of good times for the rest of everyones foreseeable life

or, at least, the rest of hers.

When a Fed chair says something as audacious as there is no chance of another financial crisis in our lifetimes and when she sees no concrete situations of banks being too big to fail, even when the ones that were too big to fail last time are now twice as big, I think Titanic disaster. I think of all those nuclear experts who said, when three Fukushima reactors were blowing up and melting down, that they saw no chance of meltdown anywhere because these reactors were built too tough to melt down. As they spoke, you could hear the reactors exploding and see tops blowing off the buildings on videos playing behind them and watch people running around in protective suits, which made for quite a spectacular orchestration of expert feel-safe baloney.

Nothing to see here, folks. Just minor gas venting, typical of reactors in a non-meltdown stage of something. Move along.

I think minor gas venting is what we are hearing out of Yellen.

The inability of central bankers to see anything coming, even as it is bearing down on top of them, is classic. If recessions were trains, Yellen would be tied to the tracks right now, sipping tea. Her saucer would be rattling on the rails, but you wouldnt be able to hear the rattle because of the rumbling of a locomotive in the background. Yellen would look up from her tea cup and smile at you like the nice grandmother that she is as the train runs over her.

You can also comfort yourself with this bit of superior Fed protection: All of Yellens major underling banks just passed the Feds most stringent stress test of their reserves. Because they passed gloriously, Yellen & Co told them they can now reduce their reserves, just as she is talking about strapping the economy with quantitative tightening. This move is for the important reason of freeing up something like $100 billion so they can pay themselves fat bonuses and share the wealth with their stockholders.

Whew! Glad the risk of being too big to fail is over. Maybe she meant she has just removed the risk for banksters and major share holders because they all get their bonuses now before the banking collapse.

If you wonder how blind Grandma Yellen is, look at her following statement, which offers a penetrating glance into the obvious:

Valuation pressures across a range of assets and several indicators of investor risk appetite have increased further since mid-February

(Zero Hedge)

Really? Just since mid-February? That was the first time you noticed that maybe, just maybe, the stock and bond markets were starting to look a little bubbly? These high valuations are just now pressuring the Fed to back off on stimulus because the market started to look a tad inflated in February?

She made this statement in order to justify her other statement ab out the Feds following choice to reduce stimulus even though its inflation target has not yet been met:

The Committee currently expects to begin implementing the balance sheet normalization program this year provided that the economy evolves broadly as anticipated

So, the Fed has changed its metric from its mandate of manipulating inflation to setting policy based on curbing overly exuberant market valuations. Once again, we see evidence that the Fed is manipulating markets and setting a course correction on stimulus because of markets.

In other words, the Fed wants you to believe the bubblicious pricing of stocks was not something they rigged by trying to create a wealth effect in front-running the stock market as former Fed governor Richard Fisher said of the actions he was involved in, but that it is just a side-effect of their stimulus that now pressures them to back down. No, it was dangerous manipulation that is now pressuring the Fed to pursue a course of unwinding stimulus.

The Great Unwind is about to begin

The unwinding of the Federal Reserves balance sheet has been saved to the end because it is more problematic than either the end of quantitative wheezing or the end of low-interest policy, and it is being carried out be people who have never seen a recession coming in the past and who see no reason to believe we will ever again in our lifetimes see a financial crisis like the last one.

By the Great Unwind, I mean the reversal of QE (quantitative tightening). While investors are buoyed a little by Yellens dovish indication this week that the Fed will only raise interest one more time, the reversal of QE over time will be by far the Feds most difficult change toward normalization to navigate.

JPMorgan Chase & Co. Chairman Jamie Dimon said the unwinding of central bank bond-buying programs is an unprecedented challenge that may be more disruptive than people think.

Weve never have had QE like this before, weve never had unwinding like this before, Dimon said at a conference in Paris Tuesday. Obviously that should say something to you about the risk that might mean, because weve never lived with it before

. We act like we know exactly how its going to happen and we dont.

All the main buyers of sovereign debt over the last 10 years financial institutions, central banks, foreign exchange managers will become net sellers now, he said. (Newsmax)

A risk never experienced in the history of the world. Never is a long time. That risk, anticipated to begin at the end of summer, is far greater than the mere termination of QE that already took place or than the incremental rise in interest rates. This change actually sucks liquidity out of the market, versus slowing the expansion of liquidity.

Considering the Fed has pumped $4.5 trillion of liquidity into the economy to help recover from the Great Recession, there is potentially a lot of unwinding to now begin, and it starts in an economy that is limping along the ground, not in the kind of recovery the Fed anticipated rewinding from. Between the European Central Bank, the Bank of the Japan and the Fed, there is $14 trillion to unwind

or, at least, some large portion of that.

The Great Unwind happens in a period where global debt has reached $217 trillion, which presents a major problem for the Fed in selling off so many bonds. They will almost certainly have to offer them at better yields more interest in order to attract buyers. That sifts throughout debt markets to raise the interest on carrying or refinancing all of this debt. Nations will have to compete with central bank yields in order to issue new debt or refi old. The European Central Bank and Bank of Japan are also looking like they may start unwinding soon, so compound all of that in your mind.

As I believe the main factor in driving market multiples to historically high levels was QE, ZIRP and NIRP, then yes, the reversal will have major implications for markets and volatility. Peter Boockvar, chief market analyst at The Lindsey Group, told MarketWatch.

The Feds Great Unwind is scheduled to start (if the Feds hints bear out) during the stock markets unwind from Trumphoria, too, and during the retail apocalypse and auto market crash:

Crispin Odey, who made money for a second straight month by sticking to bearish equity bets, said the chance of a market crash is rising as growth slows and the Federal Reserve normalizes interest rates.

The credit cycle boosted by loose monetary policy has peaked and theres a widespread slowdown in the auto, commodity, industrial and retail sectors, Odey wrote in a letter to investors. Unlike previous dips since the financial crisis, central banks arent responding by printing more money.

This time they are doing the reverse, which is likely to exacerbate the negative trend, the London-based hedge fund manager wrote. All this sits very uncomfortably with the fun being felt in the stock markets. When I look at the move up since Trumps election as president, I detect the walk of a drunken man.

The chances of car crashes everywhere are rising, according to Odey. Enjoy the hot summer, (Newsmax)

The timing for the Feds Great Unwind does not look fortuitous. Key to understanding why the Federal Reserve always has such bad timing so that it routinely crashes its own recoveries can be found in recognizing that the Feds dual mandate setting monetary guidance based on maximizing jobs and maintaining inflation at a set level means the Fed is always aiming to create goals that may take a year to develop from the time they make any change.

Inflation is largely dependent on the wage/labor market, and a change in hiring decisions is dependent first on a change in economic conditions; so the movement of these lagging indicators that the Fed monitors the most can easily be a year or more away. Thus, the Fed will continue to move every quarter more and more toward their new bias of stimulus reduction until they see the results in their job and inflation metrics. But they are doing that when the economy is already receding. By the time they see the results in their two sacred metrics, theyve moved further than they need to and downhill momentum has already built up.

So, they will do it again.

The death of Trumphoria

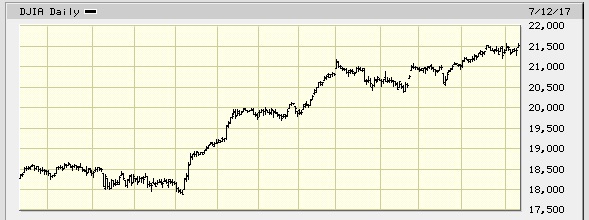

The irrational exuberance that superheated the stock market after Trumps election is dead right where I said months ago it died. A quick look at any chart of its biometrics proves that:

The patient has been pretty-well flatlining for half a year with a couple of attempted jolts with the paddles that yielded no lasting results. The market has scratched its way sideways in daily tremors up and down ever since, but has gone almost nowhere for more than four months.

While the NASDAQ just looks like a heart attack:

Chris Whalen, a long-time bank analyst, expects [bank] earnings to come in soft enough that the stocks will trade off. Theres no real growth on the top line, he told MarketWatch. After several lean years, banks have run out of expenses to cut to boost the bottom line.

And most investors are finally starting to acknowledge that the hoped-for reflation trade isnt coming, Whalen said. The Trump Bump is dead.

Hopes that the economy would be boosted by structural reforms, including tax reform, have faded as the administration of President Donald Trump has made little leeway on its plans. (Marketwatch)

The stock market gained a little more headroom in the first half of last month, but has, again, petered out. The market is in its summer doldrums that hot, sultry period of dead winds before the summer storms where any gains look like a mirage, typically passing away as soon as they are reached. Relentless stories about Trumps supposed Russian electioneering collaboration whether true or fake also have diminished investor hopes that a fiscal stimulus plan will come about this year, an outcome Ive suggested is likely all year.

And FAANG stocks those high-tech draft horses of the stock market are now weighing down on the market with dead weight, rather than dragging it up. This is a major reversal of the pattern that has supported the market for years when many stocks were in a bear market, but the FAANGs relentlessly pulled the averages ever skyward.

Bank of Americas chief strategist Michael Harnett sees the top forming in the market and predicts the stock market will crash this fall:

We dont think this is big top in stocks; greed harder to kill than fear; dont think this big top in stocks

. summer 2017 = significant inflection point in central bank liquidity trade

will likely lead to Humpty-Dumpty big fall in market in autumn, in our view. But Big Top likely occurs when Peak Liquidity meets Peak Profits. We think thats an autumn not summer story. (Zero Hedge)

In BofAs view, the stagnant humidity we feel in the market now the doldrums after Trumphoria is building toward an autumn storm more likely than a summer storm because it will required the Feds move into the Great Unwind to really kick things off. Ive said summer because Id rather err on the side of safety, miss a part of the ride and be out ahead of the stampede. (And Im not a trader, just someone who has moved his retirement funds out of stocks. I do not even try to give trading advice. My interest on this blog is macro-economics where the economy is headed and the stock markets of this world are only a part of that (a part we now know is rigged by central banks direct stock purchases).

Carmageddon on cruise control

Theres been a consistent reduction in plant output in the last six months, and what is ahead in the next six months could be pretty startling, said Ron Harbour, a noted manufacturing analyst

.

The industry has dramatically expanded employment in the United States in the last several years, but the growth is just not there anymore, said Harley Shaiken, a labor professor at the University of California, Berkeley.

And companies are increasingly looking to build their less profitable car models outside the United States. Ford Motor, for example, said in June that it would move production of its Focus sedan to China from Michigan

.

Scaling back jobs in car plants is part of a newfound discipline among automakers to avoid bloated payrolls and inventories when sales start slipping

.

Moreover, the Detroit companies have also hired large numbers of lower-wage, entry-level employees with less costly unemployment benefits

.

G.M., for example, has reduced the number of shifts at several of its domestic plants

.

We are beginning to enter a period we call the post-peak, said Jonathan Smoke, chief economist for Cox Automotive, which operates the auto-research sites Kelley Blue Book and Autotrader. (New York Times)

And auto parts are not doing any better than autos. OReilly Automotive Inc.s disappointing sales slammed a sector already seen as Amazons next source of fodder, taking a record plunge as it missed its second-quarter projections. Advanced Auto Parts and AutoZone are also continued declining. OReilly shares plunged as much as 21%. It is another area where demand is shifting away from brick-and-mortar stores and toward online purchases. Some say that auto manufacturers, seeing that customers are hanging on to their old cars longer, are stiffening up competition from OEM parts, too.

Attempts to ward off the retail apocalypse

Mitigating forces are at work, trying to turn the massive number of closures of mall anchor stores and smaller stores into opportunity for new life, but no one knows yet if these extravagant and creative efforts will work.

Costs are escalating as mall owners work to keep their real estate up to date and fill the void left by failing stores. The companies are turning to everything from restaurants and bars to mini-golf courses and rock-climbing gyms to draw in customers who appear more interested in being entertained during a trip to the mall than they are in buying clothes and electronics. The new tenants will pay higher rents than struggling chains such as Macys and Sears, and hopefully attract more traffic for retailers at the property, according to Haendel St. Juste, an analyst at Mizuho Securities USA LLC.

The math is pretty obvious, pretty compelling, but there are risks, St. Juste said in an interview. This hasnt been done before on a broad scale.

So far, jettisoning and replacing undesirable tenants has been a successful formula for many landlords, but there is still a lot of work to be done, according to Jeffrey Langbaum, an analyst with Bloomberg Intelligence. Some companies wont have the cash to keep up amid the relentless pace of store closures, he said.

For the most part, these companies have been able to redevelop and backfill space, Langbaum said. Thats great, but the big wave is still coming.

For Ziff of Time Equities, which buys outdated malls and renovates them, it doesnt matter how you categorize the expenses of making over a center for the modern era, or if there is a linear path to a return on a particular project. Whether its installing a fireplace in a new food hall, or buying artwork for the common area, the aim is to drive higher traffic and tenant sales, he said. Ultimately, its all cash going out the door. (Newsmax)

The response teams to the retail crisis are already at work on makeovers, but the costs are high, and no one knows yet if it will work beyond a few well-positioned success stories. The fact that they are taking such major risks shows how significance this retail paradigm shift is.

Government bankruptcies continue to grow

I recently reported on the near-default situation of several states, showing how deeply to the core of the state the residual problems of the financial crisis cuts. You can add to that list of serious funding problems, the capital city of Connecticut:

Like many other local governments across the country, Hartford city of Mark Twain and the young John Pierpont Morgan has been grappling with budget problems for years. On the same day that Illinois lawmakers finally scrapped together a long-overdue budget, Hartford hired the law firm Greenberg Traurig LLP to evaluate its options, which include bankruptcy. It would be the first prominent U.S. municipality to seek protection from its creditors since Detroit did so in 2013. (Newsmax)

The rise in both corporate and national defaults right now is showing up in other areas of the world, too:

Sovereign government and corporate defaults in both developed and developing economies are beginning to emerge. For example, China has registered in 2017 its highest level of corporate defaults in the first quarter of a calendar year on record. Delinquencies and charge-offs in the United States soared to $US1.4 billion in the first quarter of 2017, the highest recorded level since the first quarter of 2011

.

In May 2017, six major Canadian banks were downgraded by Moodys Investor Service (Moodys) as concerns rise over soaring Canadian household debt and house prices leave lenders more vulnerable to losses. Moodys also downgraded Chinas sovereign debt in May 2017 for the first time since 1989 and has warned of further downgrades if further reforms are not enacted

.

In May 2017, S&P has downgraded 23 small-to-medium Australian financial institutions as the risk of falling property prices increases and potential financial losses start to increase. In June 2017, Moodys downgraded 12 Australian banks, including Australias four major banks.

Standard and Poors and Moodys downgraded bonds for the US State of Illinois down to one notch above junk bond status as the state has over $US 14.5b in unpaid bills. (Zero Hedge)

These pressures are spreading at a rate that could be considered endemic around the world by next year.

More storm clouds keep gathering

Credit demand for both credit cards and auto loans has gone deeply negative for the first time in years. Credit cards briefly touched into the negative in 2012 with a 4% decline; but this years decline of 11% far exceeds that. Auto loans havent gone negative since 2011, but are now seeing a 14% decline.

US tax receipts have matched this negative move, also down about 14% this year with an uptick last month. They havent gone negative since the Great Recession, other than a brief downtick of about -4% in 2011. Other than that brief downtick, a negative turn of this indicator has exactly matched with every recession in the post WWII era.

Factory orders took their second monthly drop and fell by more than economists expected. Durable goods orders declined in April and May, following a year of steady albeit slight growth.

Even the formerly blind Fed Chair Alan Greenspan sees that we are now entering what he says will be a long, very tough period of stagflation. He anticipates GDP will bump up to growth of 3% for the second quarter, but says that is misleading number, a false dawn, that is merely born of problematic adjustments happening this quarter. The presumption that were going to come bouncing back is utterly unrealistic. (Newsmax) Thats quite a change for Greenspan who, like most central-bank chiefs, never saw trouble coming in the past.

Bank of America Merrill Lynchs Sellside Indicator hit its highest level since the official end of the Great Recession in June 2011. The indicator measures how bullish strategists are on US equities, now showing a strong move toward the jump out and sell side.

The Chicago Fed National Economic Activity Index took its biggest drop since August, 2016.

US mortgage applications and home purchases have seen steep declines recently. The week ending the month of June, usually a hot time for buying, dropped week-on-week by the most in half a year, even as interest rates had returned to nearly their lowest levels. Correspondingly, pending home sales fell each month from March through May. A majority of economists polled by Reuters, naturally, forecasted that May sales would increase. Heres dirt in your eye, Economists.

In summary, nothing happening this summer threatens my forecast from the beginning of the year, which said that a major economic breakdown would become evident by summer and that the stock market would crash sometime between early summer and the start of 2018, with it likely to be earlier than later. Ive bet my blog on it, and Ill comfortably stay with that bet. I dont think the above confluence of forces proves that bet right, by any means; but clearly forces are continuing to build strongly in that direction. There is, in fact, almost nothing on our horizon in the US that looks like a playful summer on the beach. (I hope YOU have such a summer, but I am speaking in terms of the economy.)

http://thegreatrecession.info/blog/us-summer-economic-storm/

| Digg This Article

-- Published: Thursday, 13 July 2017 | E-Mail | Print | Source: GoldSeek.com