-- Published: Thursday, 10 August 2017 | Print | Disqus

By: Market Anthropology

Economic medicine that was previously meted out by the cupful has recently been dispensed by the barrel. These once unthinkable dosages will almost certainly bring on unwelcomed after-effects. Their precise nature is anyones guess, though one likely consequence is an onslaught of inflation. Warren Buffett, February 2009

Looking back at the current decade in the shadow of the global financial crisis of the previous, one topic has overwhelmingly remained in focus by policy makers, pundits and participants alike.

Inflation: a general increase in prices and fall in the purchasing value of money.

An paradoxically, for all of the collective attention thats been paid to the prospects of inflation, by and large, the dire warnings cast by both the brightest and most prudent in finance have appeared misplaced, as inflation has remained subdued and still below the Federal Reserves 2 percent long-term target more than 8 years after the final throes of the global financial crisis.

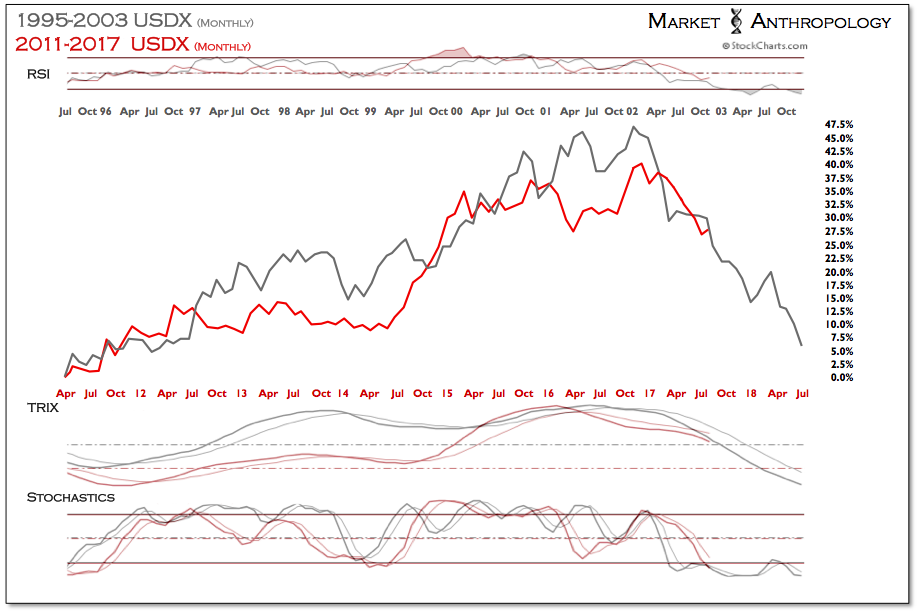

Last weeks release of the Feds preferred measure of inflation the Personal Consumption Expenditures Chain-type Price Index for June, indicated that core inflation sits at 1.5 percent, down from a high of 1.91 percent in October of last year. And although causality and correlation between inflation and the financial markets is as nuanced and complicated as any intractable problem, when it comes to the equity markets today we believe they broadly function along a binary highway where low to moderating inflation is welcomed and fundamentally expected, with higher realized inflation largely reserved for economic folklore. In essence, weve been driving down a seemingly one-way street for so long that participants have ignored the travel risks of oncoming traffic with higher prices. Should the dollar continued to breakdown from its cyclical high which we believe it will, thats precisely what will be coming our way. And like most things in life, nothing kills the mood quicker than the surprise realization that you now get less bang for your buck.

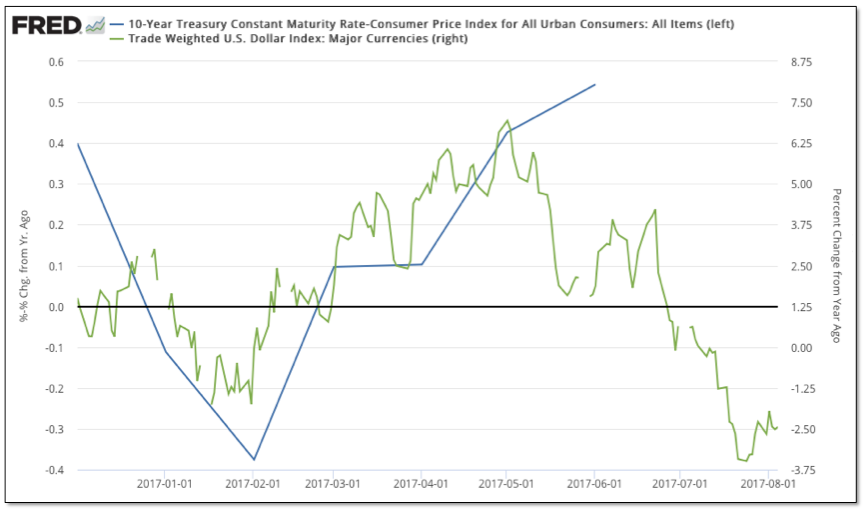

With tomorrow's PPI and Fridays CPI inflation reports on deck in the back half of the week, we wanted to quickly point out that the markets are now in the window where US dollar weakness on a year-over-year performance basis, could again begin to positively affect the inflation data.

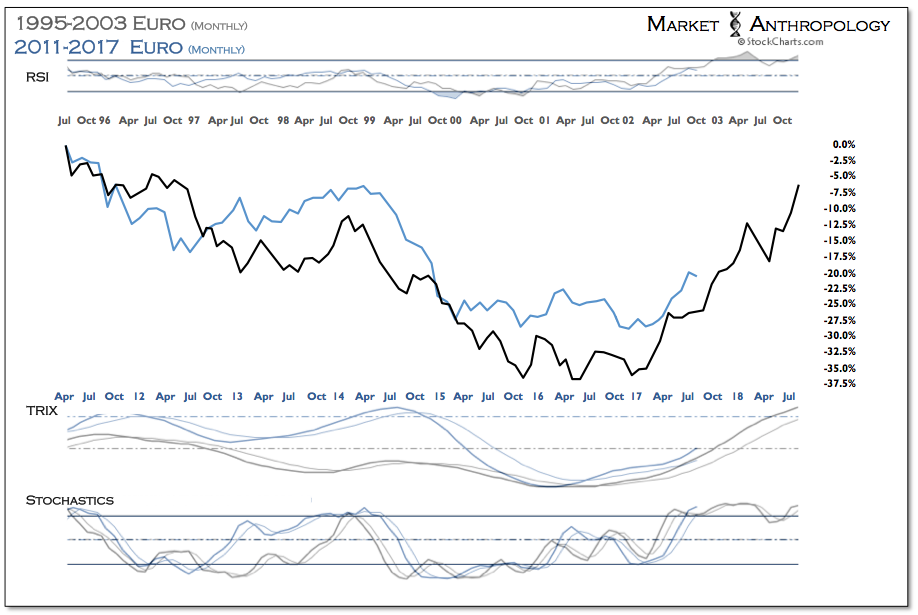

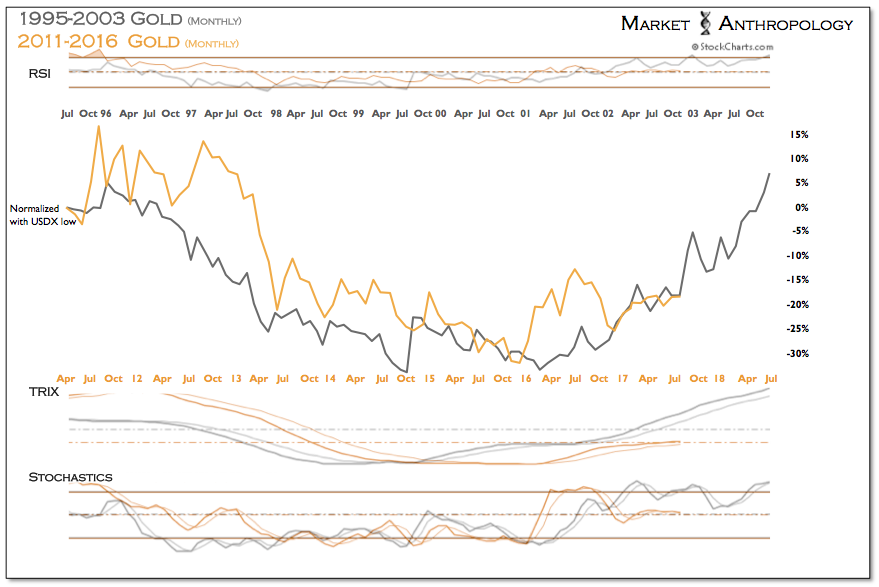

From our perspective, the attached two charts imply (we use real yields here as it positively trends with the dollar, albeit with a several week lag) that the YOY performance of the dollar has led the move in real yields, with underlying support of the dollar's broad 3-year top serving as the fulcrum for next major move in inflation (we believe higher) and real yields (lower).

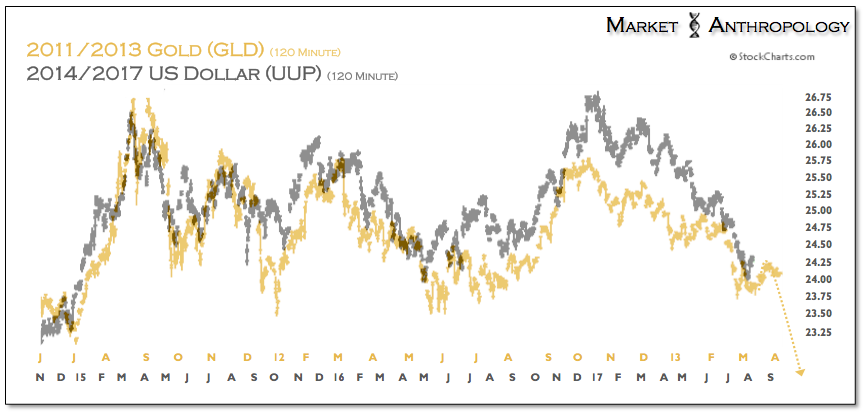

As we pointed out at the start of summer (see Here), despite breaking down since last December, US dollar weakness was largely obscured from the inflation reports this year, primarily because on a YOY performance basis the dollar had actually trended higher through May, essentially arresting the respective moves of higher inflation and lower real yields that began in the back half of 2015 which led the cyclical pivot higher in gold in late December of that year.

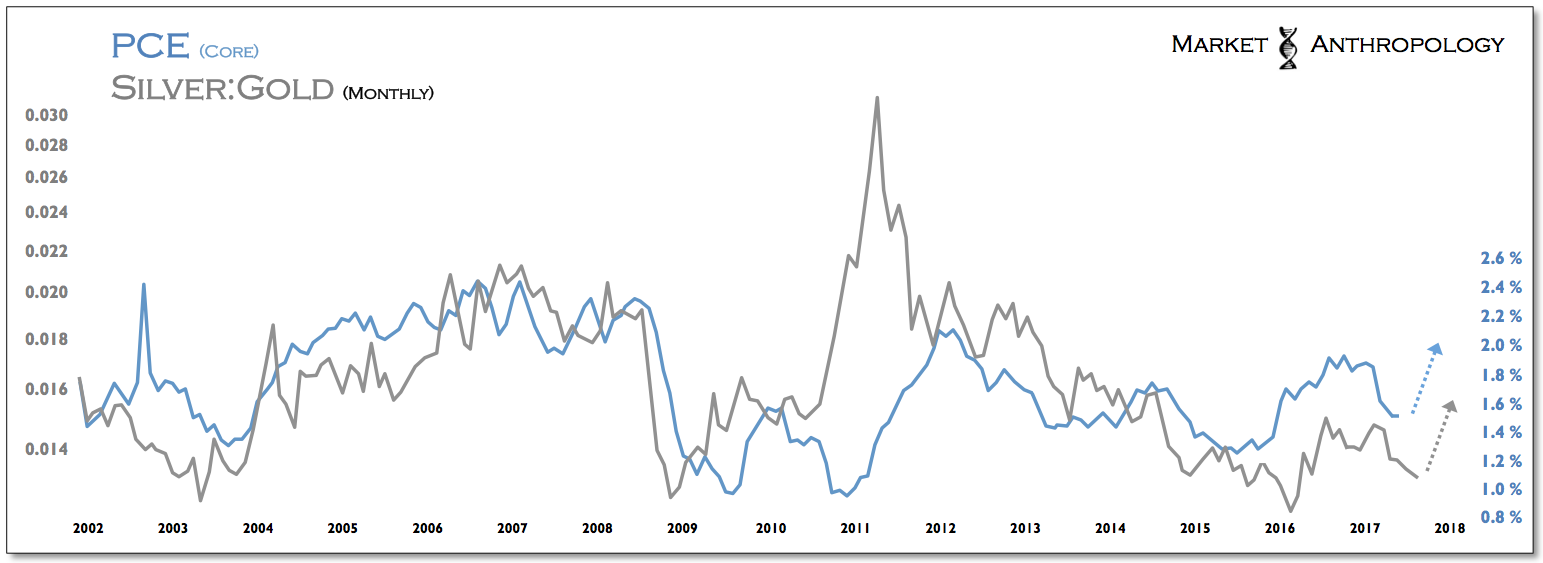

Wed speculate that if YOY weakness in the dollar fails to bump the July inflation data, it will more than likely show up next month. All things considered, its a good bet we see the downtrend in the data reverse course soon, which when it hits could see a more hawkish market reaction over the immediate-term with a stronger dollar, weaker precious metals and rising yields. While over the intermediate-term we firmly expect gold and silver to break out above their respective highs from last year (with silver once again leading the way), recent strength may give way to weakness as the market considers further Fed action.

| Digg This Article

-- Published: Thursday, 10 August 2017 | E-Mail | Print | Source: GoldSeek.com