-- Published: Sunday, 1 October 2017 | Print | Disqus

By John Mauldin

Global Shortfall

UK Time Bomb

Swiss Cheese Retirement

Pay-As-You-Go Woes

Lisbon, Denver, Lugano, and Hong Kong

Today well continue to size up the bull market in governmental promises. As we do so, keep an old traders slogan in mind: That which cannot go on forever, wont. Or we could say it differently: An unsustainable trend must eventually stop.

Lately I have focused on the trend in US public pension funds, many of which are woefully underfunded and will never be able to pay workers the promised benefits, at least without dumping a huge and unwelcome bill on taxpayers. And since taxpayers are generally voters, its not at all clear they will pay that bill.

Readers outside the US might have felt smug and safe reading those stories. There go those Americans again, spending wildly beyond their means. You are correct that, generally speaking, we are not exactly the thriftiest people on Earth. However, if you live outside the US, your country may be more like ours than you think. Today well look at some data that will show you what I mean. This week the spotlight will be on Europe.

First, let me suggest that you read my last letter, Build Your Economic Storm Shelter Now, if you missed it. It has some important background for todays discussiion, as well as a special invitation to attend my Strategic Investment Conference next March 69 in San Diego. With so much change occurring so quickly now, next years conference is an event you shouldnt miss.

Global Shortfall

I wrote a letter last June titled Can You Afford to Reach 100? Your answer may well be Yes; but, if so, you are one of the few. The World Economic Forum study I cited in that letter looked at six developed countries (the US, UK, Netherlands, Japan, Australia, and Canada) and two emerging markets (China and India) and found that by 2050 these countries will face a total savings shortfall of $400 trillion. Thats how much more is needed to ensure that future retirees will receive 70% of their working income. This staggering figure doesnt even include most of Europe.

This problem exists in large part because of the projected enormous increase in median life expectancies. Reaching age 100 is already less remarkable than it used to be. That trend will continue. Better yet, I think we will also be healthier at advanced ages than people are now. Could 80 be the new 50? Wed better hope so, because the math is pretty bleak if we assume people will stop working at age 6570 and then live another quarter-century or more.

That said, I think well see a great deal of national variation in these trends. The $400 trillion gap is the shortfall in government, employer, and individual savings. The proportions among the three vary a great deal. Some countries have robust government-provided retirement plans; others depend more on employer and individual contributions. In the aggregate, though, the money just isnt there. Nor will it magically appear just when its needed.

WEF reaches the same conclusion I did long ago: The idea that well enjoy decades of leisure before our final decline simply cant work. Our attempt to live out long and leisurely retirements is quickly reaching its limits. Most of us will work well past 65 whether we want to or not, and many of us will not have our promised retirement benefits to help us through our final decades.

What about the millions who are already retired or close to retirement? Thats a big problem, particularly for the US public-sector workers I wrote about in my last two letters. We should also note that were all public-sector workers in a way, since we must pay into Social Security and can only hope Washington gives us something back someday.

Lets look at a few other countries that are not much better off.

UK Time Bomb

The WEF study shows that the United Kingdom presently has a $4 trillion retirement savings shortfall, which is projected to rise 4% a year and reach $33 trillion by 2050. This in a country whose total GDP is $3 trillion. That means the shortfall is already bigger than the entire economy, and even if inflation is modest, the situation is going to get worse. Further, these figures are based mostly on calculations made before the UK decided to leave the European Union. Brexit is a major economic realignment that could certainly change the retirement outlook. Whether it would change it for better or worse, we dont yet know.

A 2015 OECD study (mentioned here) found that across the developed world, workers could, on average, expect governmental programs to replace 63% of their working-age incomes. Not so bad. But in the UK that figure is only 38%, the lowest in all OECD countries. This means UK workers must either build larger personal savings or severely tighten their belts when they retire. Working past retirement age is another choice, but it has broader economic effects freezing younger workers out of the job market, for instance.

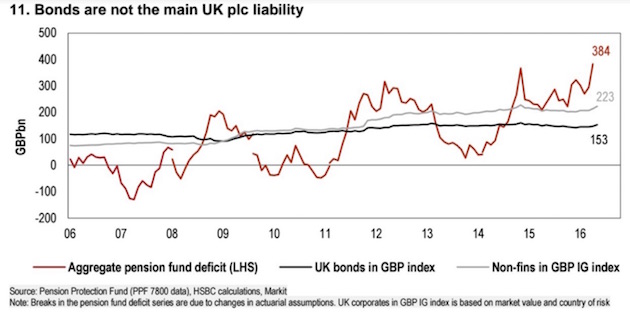

UK employer-based savings plans arent on particularly sound footing, either. According to the governments Pension Protection Fund, some 72.2% of the countrys private-sector defined-benefit plans are in deficit, and the shortfalls total £257.9 billion. Government liabilities for pensions went from being well-funded in 2007 to having a shortfall 10 years later of £384 billion (~$500 billion). Of course, that figure is now out of date because, just a few months later, its now £408 billion thats how fast these unfunded liabilities are growing. Again, thats a rather tidy sum for a $3 trillion economy to handle.

UK retirees have had a kind of safety valve: the ability to retire in EU countries with lower living costs. Depending how Brexit negotiations go, that option could disappear.

Turning next to the Green Isle, 80% of the Irish who have pensions dont think they will have sufficient income in retirement, and 47% dont even have pensions. I think you would find similar statistics throughout much of Europe.

A report this summer from the International Longevity Centre suggested that younger workers in the UK need to save 18% of their annual earnings in order to have an adequate retirement income which it defines as less than todays retirees enjoy. But no such thing will happen, so the UK is heading toward a retirement implosion that could be at least as damaging as the USs.

Swiss Cheese Retirement

Americans often have romanticized views of Switzerland. They think its the land of fiscal discipline, among other things. To some extent thats true, but Switzerland has its share of problems, too. The national pension plan there has been running deficits as the population grows older.

Earlier this month, Swiss voters rejected a pension reform plan that would have strengthened the system by raising womens retirement age from 64 to 65 and raising taxes and required worker contributions. From what I can see, these were fairly minor changes, but the plan still went down in flames as 52.7% of voters said no.

Voters around the globe generally want to have their cake and eat it, too. We demand generous benefits but dont like the price tags that come with them. The Swiss, despite their fiscally prudent reputation, appear to be not so different from the rest of us. Consider this from the Financial Times:

Alain Berset, interior minister, said the No vote was not easy to interpret but was not so far from a majority and work would begin soon on revised reform proposals.

Bern had sought to spread the burden of changes to the pension system, said Daniel Kalt, chief economist for UBS in Switzerland. But its difficult to find a compromise to which everyone can say Yes. The pressure for reform was not yet high enough, he argued. Awareness that something has to be done will now increase.

That description captures the attitude of the entire developed world. Compromise is always difficult. Both politicians and voters ignore the long-term problems they know are coming and think no further ahead than the next election. The remark that Awareness that something has to be done will now increase may be true, but theres a big gap between awareness and motivation in Switzerland and everywhere else.

Switzerland and the UK have mandatory retirement pre-funding with private management and modest public safety nets, as do Denmark, the Netherlands, Sweden, Poland, and Hungary. Not that all of these countries dont have problems, but even with their problems, these European nations are far better off than some others.

(Sidebar: low or negative rates in those countries make it almost impossible for their private pension funds to come anywhere close to meeting their mandates. And many of the funds are by law are required to invest in government bonds, which pay either negligible or negative returns.)

Pay-As-You-Go Woes

The European nations noted above have nowhere near the crisis potential that the next group does: France, Belgium, Germany, Austria, and Spain are all pay-as-you-go countries (PAYG). That means they have nothing saved in the public coffers for future pension obligations, and the money has to come out of the general budget each year. The crisis for these countries is quite predictable, because the number of retirees is growing even as the number of workers paying into the national coffers is falling. There is a sad shortfall of babies being born in these countries, making the demographic reality even more difficult. Lets look at some details.

Spain was hit hard in the financial crisis but has bounced back more vigorously than some of its Mediterranean peers did, such as Greece. Thats also true of its national pension plan, which actually had a surplus until recently. Unfortunately, the government chose to borrow some of that surplus for other purposes, and it will soon turn into a sizable deficit.

Just as in the US, Spains program is called Social Security, but in fact it is neither social nor secure. Both the US and Spanish governments have raided supposedly sacrosanct retirement schemes, and both allow their governments to use those savings for whatever the political winds favor.

The Spanish reserve fund at one time had 66 billion and is now estimated to be completely depleted by the end of this year or early in 2018. The cause? There are 1.1 million more pensioners than there were just 10 years ago. And as the Baby Boom generation retires, there will be even more pensioners and fewer workers to support them. A 25% unemployment rate among younger workers doesnt help contributions to the system, either.

A similar dynamic may actually work for the US, because we control our own currency and can debase it as necessary to keep the government afloat. Social Security checks will always clear, but they may not buy as much. Spains version of Social Security doesnt have that advantage as long as the country stays tied to the euro. Thats one reason we must recognize the potential for the Eurozone to eventually spin apart. (More on that below.)

On the whole, public pension plans in the pay-as-you-go countries would now replace about 60% of retirees salaries. Further, several of these countries let people retire at less than 60 years old. In most countries, fewer than 25% of workers contribute to pension plans. That rate would have to double in the next 30 years to make programs sustainable. Sell that to younger workers.

The Wall Street Journal recently did a rather bleak report on public pension funds in Europe. Quoting:

Europes population of pensioners, already the largest in the world, continues to grow. Looking at Europeans 65 or older who arent working, there are 42 for every 100 workers, and this will rise to 65 per 100 by 2060, the European Unions data agency says. By comparison, the U.S. has 24 nonworking people 65 or over per 100 workers, says the Bureau of Labor Statistics, which doesnt have a projection for 2060. (WSJ)

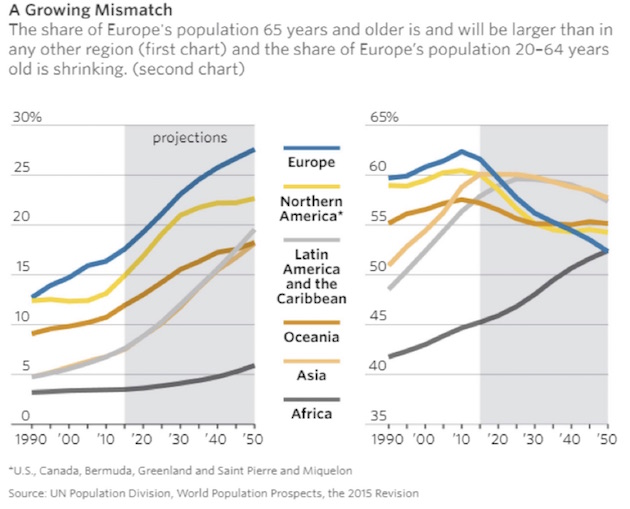

While the WSJ story focuses on Poland and the difficulties facing retirees there, the graphs and data in the story make clear the increasingly tenuous situation across much of Europe. And unlike most European financial problems, this isnt a north-south issue. Austria and Slovenia face the most difficult demographic challenges, right along with Greece. Greece, like Poland, has seen a lot of its young people leave for other parts of the world. This next chart compares the share of Europes population that 65 years and older to the rest of the regions of the world and then to the share of population of workers between 20 and 64. These are ugly numbers.

Source: WSJ

The WSJ continues:

Across Europe, the birthrate has fallen 40% since the 1960s to around 1.5 children per woman, according to the United Nations. In that time, life expectancies have risen to roughly 80 from 69.

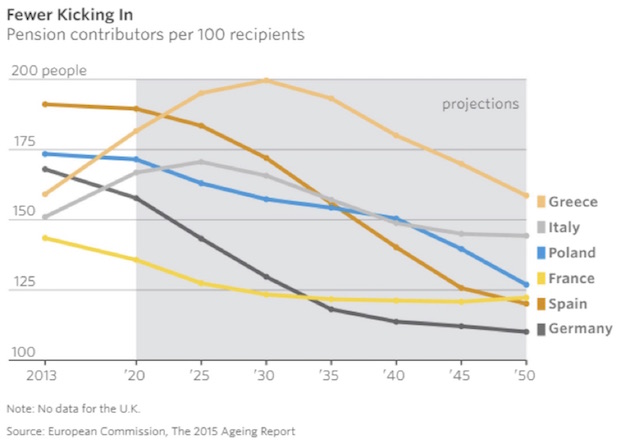

In Poland birthrates are even lower, and here the demographic disconnect is compounded by emigration. Taking advantage of the EUs freedom of movement, many Polish youth of working age flock to the West, especially London, in search of higher pay. A paper published by the countrys central bank forecasts that by 2030, a quarter of Polish women and a fifth of Polish men will be 70 or older.

Source: WSJ

Next week we will look at the unfunded liabilities of the US government. It will not surprise anyone to learn that the situation is ugly, and there is no way zero chance, zippo that the US government will be able to fund those liabilities without massive debt and monetization.

Now, what I am telling you is that every bit of analysis about the pay-as-you-go countries in Europe suggests that they are in a far worse position than the United States is. Plus, the economies of those countries are more or less stagnant, and they are already taxing their citizens at close to 50% of GDP.

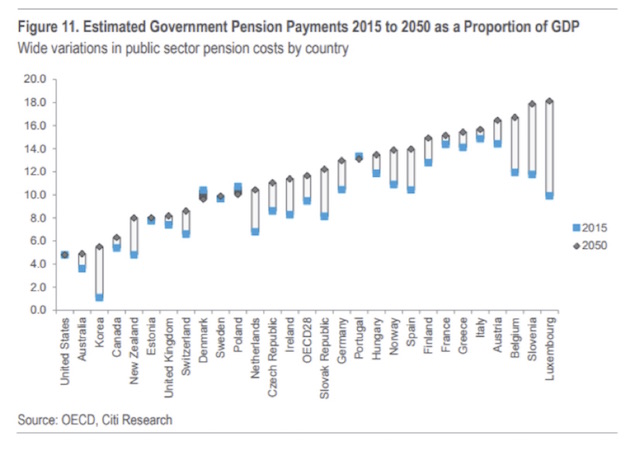

The chart below shows the percentage of GDP needed to cover government pension payments in 2015 and 2050. But consider that the percentage of tax revenues required will be much higher. For instance, in Belgium the percentage of GDP going to pensions will be 18% in about 30 years, but thats 4050% of total tax revenues. That hunk doesnt leave much for other budgetary items. Greece, Italy, Spain? Not far behind.

And there is other research that makes the above numbers seem optimistic by comparison. The problem that the European economies have is that for the most part they are already massively in debt and have high tax rates. And they cant print their own currencies.

Many of Europes private pension companies and corporations are also in seriously deep kimchee. Low and negative interest rates have devastated the ability of pension funds to grow their assets. Combined with public pension liabilities, the total cost of meeting the income and healthcare needs of retirees is going to increase dramatically all across Europe.

Macron, the new French president, really is trying to shake up the old order, to his credit; and this week he came out and began to lay the foundation for the mutualization of all European debt, which I assume would end up on the balance sheet of the ECB. However, that plan still doesnt deal with the unfunded liabilities. Do countries just run up more debt? It seems like the plan is to kick the can down the road just a little further, something Europe is becoming really good at.

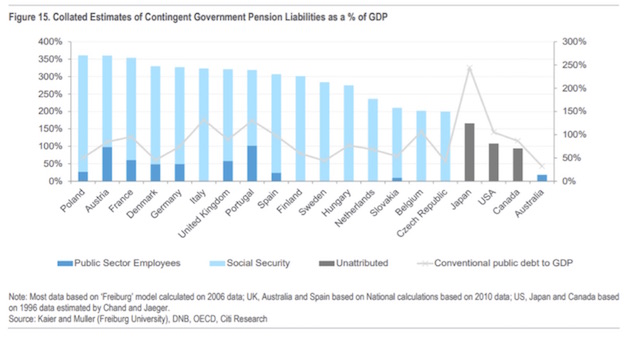

In this next chart, note the line running through each of the countries, showing their debt as a percentage of GDP. Italys is already over 150%. And this is a chart based mostly on 2006 and earlier data. A newer chart would be much uglier.

I could go on reviewing the retirement problems in other countries, but I hope you begin to see the big picture. This crisis isnt purely a result of faulty politics though thats a big contributor its a problem that is far bigger than even the most disciplined, future-focused governments and businesses can easily handle.

Look what were trying to do. We think people can spend 3540 years working and saving, then stop working and go on for another 203040 years at the same comfort level but with a growing percentage of retirees and a shrinking number of workers paying into the system. Im sorry, but thats magical thinking. And its not what the original retirement schemes envisioned at all. Their goal was to provide for a relatively small number of elderly people who were unable to work. Life expectancies were such that most workers would not reach that point, or would at least live just a few years beyond retirement.

As I have pointed out in past letters, when Franklin Roosevelt created Social Security for people over 65 years old, US life expectancy was about 56 years. If the retirement age had kept up with the increase in life expectancy, the retirement age in the US would now be 82. Try and sell that to voters.

Worse, generations of politicians have convinced the public that not only is a magical outcome possible, it is guaranteed. Many politicians actually believe it themselves. They arent lying so much as just ignoring reality. Theyve made promises they arent able to keep and are letting others arrange their lives based on the assumption that the impossible will happen. It wont.

How do we get out of this jam? Were all going to make big adjustments. If the longevity breakthroughs I expect happen soon (as in the next 1015 years), we may be able to adjust with minimal pain. Well work longer years, and retirement will be shorter, but it will be better because well be healthier.

Thats the best-case outcome, and I think we have a fair chance of seeing it, but not without a lot of social and political travail. How we get through that process may be the most important question we face.

I havent even thrown in the complications that are going to arise because of changes in the nature of employment and the future of work that will be caused by technological change in the next 1020 years. That will mean even fewer workers for each retiree. Facebooks Zuckerberg talks about a basic minimum income. I think that is the wrong thing to do. It is the nature of human beings to need to do things that contribute meaningfully to the lives of their family and society. But the reality is that increasing numbers of people are already having trouble finding that sort of work.

Maybe we should think about basic minimum employment. FDR put a generation of people to work building public projects that helped get us through the Great Depression. Our world is going to change in ways that we dont yet understand and that we are not prepared for, psychologically, socially, politically, or economically.

In the US and much of Europe we have developed social echo chambers in which we talk just to ourselves and those who are like-minded, ignoring or demonizing the other side. We have lost the ability to disagree rationally and productively. When the childrens books written by Dr. Seuss are considered by some to have been written by a white racist and are therefore deemed unacceptable to be in a public library, you know the quality of civil discourse has spiraled downward.

I do not like that, Sam I am.

Lisbon, Denver, Lugano, and Hong Kong

In a few hours, Shane and I will leave for the airport to catch a late-night flight to London and then on to Lisbon. My hosts, the event coordinators of the large food retailing group of Jerónimo Martins, have been particularly gracious with their arrangements and in giving us plenty of time to explore Lisbon. And the rest of the speaking lineup is quite impressive, so I imagine that I will be attending a lot of the conference. They are focused on how the world is changing, which is right up my alley.

Then we are back to Dallas on October 4 my 68th (!) birthday and I speak the next day at the Dallas Money Show. I am told that my 20-minute talk at 9:15 AM Central Time will be available on live stream. Go here and then click on the LIVE STREAM tab. I will be in Denver on November 6 and 7, speaking for the CFA Society and holding meetings. After a lot of small back-and-forth flights in November, Ill end up in Lugano, Switzerland, right before Thanksgiving. Then there will be a (currently) lightly scheduled December, followed by an early trip to Hong Kong in January. It looks like Lacy Hunt and his wife, JK, will join Shane and me there. Lacy and I will come back home exhausted from trying to keep up with our indefatigable better halves.

I am really looking forward to both Lisbon and Hong Kong, and I have never been to Lugano. Some of the back-and-forth trips do wear me out, but I enjoy it when I get to play tourist with Shane. I am sure I will have to go on an even more serious diet when I get back from Lisbon, because everybody tells me the food is fabulous.

Its time to hit the send button and get ready to run to the airport. You have a great week. I see a little port sampling in my near future. Just for appearances

Your ready to explore Lisbon and Portugal analyst,

John Mauldin

subscribers@MauldinEconomics.com

Copyright 2017 John Mauldin. All Rights Reserved.

| Digg This Article

-- Published: Sunday, 1 October 2017 | E-Mail | Print | Source: GoldSeek.com