-- Published: Sunday, 8 October 2017 | Print | Disqus

By John Mauldin

Doubled Debt

Yes, Trillions

The $210 Trillion Gap

A Tax, Not a Promise

How Will We Fund the Deficit?

San Francisco, Denver, Lugano, Hong Kong

Prime Rib: The Recipe

Heres a surprisingly profound question: What is a promise? Dictionaries offer various definitions. I like this one: An express assurance on which expectation is to be based.

Image: Simon James via Flickr

That definition captures the two-sided nature of a promise. One party offers an assurance, which the other converts into an expectation. You deposit money in your checking account, and the bank assures you that you can have it back on demand. You expect that the bank will fulfill its promise when you visit an ATM.

Governments likewise make promises, but those are different. Government is the ultimate enforcer of promises, but we have no recourse if it chooses to break them except at the ballot box. As weve seen in recent weeks regarding public pensions, thats ineffective when the promises were made long ago by officials who are no longer in office.

The federal governments keeping its promises is important for everyone in the US, because almost all of us are part of the largest public pension system: Social Security. We pay taxes our whole working lives and expect the government to give us retirement benefits. But what happens if it cant?

Three weeks ago we visited the problems with local and state pensions. Last week we looked at European pensions. This week we are going to take a hard look at the unfunded liabilities and debt of the US government. And even though the federal unfunded pension liabilities dwarf those of state and local pensions, I want to make it clear that I believe the state and local problems will be far more intractable.

I have to warn you: You may be hopping mad when you finish reading this.

Doubled Debt

In the United States we have two national programs to care for the elderly. Social Security provides a small pension, and Medicare covers medical expenses. All workers pay taxes that supposedly fund the benefits we may someday receive. Thats actually not true, as we will see in a little bit.

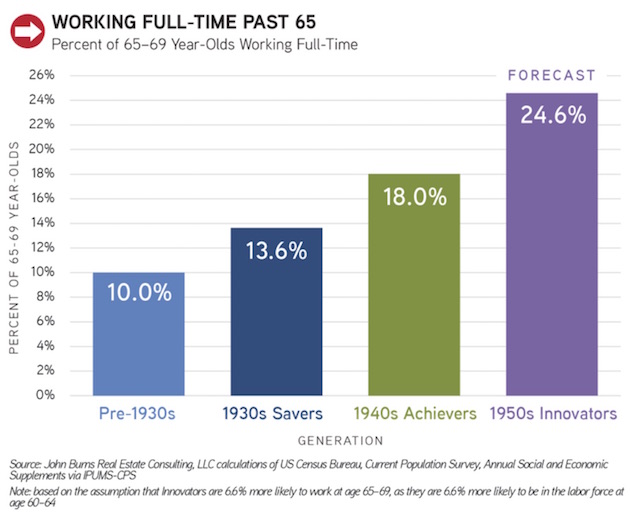

Neither of these programs is comprehensive. Living on Social Security benefits alone is a pretty meager existence. Medicare has deductibles and copayments that can add up quickly. Both programs assume people have their own savings and other resources. Nevertheless, the programs are crucial to millions of retirees, many of whom work well past 65 just to keep up with their routine expenses. This chart from my friend John Burns shows the growing trend among generations to work past age 65. Having turned 68 a few days ago, I guess Im contributing a bit to the trend:

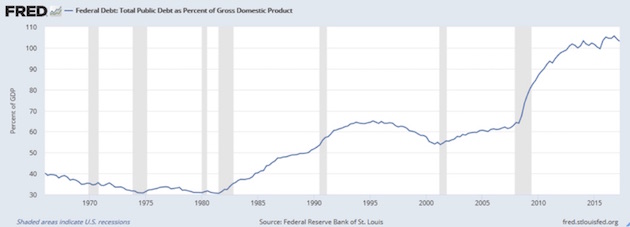

Limited though Social Security and Medicare are, we attribute one huge benefit to them: Theyre guaranteed. Uncle Sam will always pay them he promised. And to his credit, Uncle Sam is trying hard to keep his end of the deal. In fact, hes running up debt to do so. Actually, a massive amount of debt:

Federal debt as a percentage of GDP has almost doubled since the turn of the century. The big jump occurred during the 20072009 recession, but the debt has kept growing since then. Thats a consequence of both higher spending and lower GDP growth.

In theory, Social Security and Medicare dont count here. Their funding goes into separate trust funds. But in reality, the Treasury borrows from the trust funds, so they simply hold more government debt.

The Treasury Department tracks all this, and you can read about it on their website, updated daily. Presently it looks like this:

Debt held by the public: $14.4 trillion

Intragovernmental holdings (the trust funds): $5.4 trillion

Total public debt: $19.8 trillion

Total GDP is roughly $19.3 trillion, so the federal debt is about equal to one full year of the entire nations collective economic output. In fact, its even more when you consider that GDP counts government spending as production, even when Uncle Sam spends borrowed money. Of course, that total does not count the $3 trillion-plus of state and local debt, which in almost every other country of the world is included in their national debt numbers. Including state and local debt in US figures would take our debt-to-GDP above 115%. And rising.

You can quibble over the calculations, but theres no doubt the numbers are astronomically huge and growing. And we havent even mentioned the huge and growing private debt.

Just wait. Were only getting started.

Yes, Trillions

We in the business world put a lot of faith in accountants. We trust them to count the beans honestly and give us accurate reports. We may not like the numbers (I was certainly distraught with my final tax numbers this year!), but we mostly believe them. Nothing will make a companys stock drop faster than accounting irregularities will.

Government accounting is, well, different. The government doesnt need to make a profit, but we expect it to spend our tax money wisely and to deliver services efficiently. Thats not possible unless there is reliable accounting. But reliable accounting is the last thing most politicians want it constrains them from promising things they cant deliver. So we have to take all government numbers with many grains of salt.

However, there is one chink in the politicians armor. An old statute requires the Treasury to issue an annual financial statement, similar to a corporations annual report. The FY 2016 edition is 274 enlightening pages that the government hopes none of us will read.

Among the many tidbits, it contains a table on page 63 that reveals the net present value of the US governments 75-year future liability for Social Security and Medicare. That amount exceeds the net present value of the tax revenue designated to pay those benefits by $46.7 trillion. Yes, trillions.

Where will this $46.7 trillion come from? We dont know. Future Congresses will have to find it somewhere. This is the fabled unfunded liability you hear about from deficit hawks. Similar promises exist to military and civil service retirees and assorted smaller groups, too. Trying to add them up quickly becomes an exercise in absurdity. They are so huge that its hard to believe the government will pay them, promises or not.

Now, I know this is going to come as a shock, but that $46.7 trillion of unfunded liabilities is pretty much a lie. My friend Professor Larry Kotlikoff estimates the unfunded liabilities to be closer to $210 trillion. When presidential candidate Ben Carson last year quoted Kotlikoffs numbers, the Washington Post, New York Times, and other mainstream media immediately attacked him. Of course, the journalists doing the attacking had agendas, and none of them were economists or accountants. None. Zero. Zip.

Larry responded in an article in Forbes, since Carson was using his data:

The fiscal gap is the present value of all projected future expenditures less the present value of all projected future taxes. The fiscal gap is calculated over the infinite horizon. But since future expenditures and taxes far off in the future are being discounted, their contribution to the fiscal gap is smaller the farther out one goes. The $210 trillion figure is based on the Congressional Budget Offices July 2014 Alternative Fiscal Scenario projections, which I extended beyond their 75-year horizon.

The journalists used a very poorly researched analysis, which fit their political bias (shocking, I know). Apparently they take that fabricated analysis more seriously than they do the views of 17 Nobel Laureates in economics and over 1200 PhD economists from MIT, Harvard, Stanford, Chicago, Berkeley, Yale, Columbia, Penn, and lesser known universities and colleges around the country. Each of these economists has endorsed The Inform Act, a bi-partisan bill that requires the CBO, GAO, and OMB to do infinite horizon fiscal gap accounting on a routine and ongoing basis.

Now why would 17 Nobel Laureates and over 1200 US economists, all listed by name at www.theinformact.org, including many, like Jeff Sachs, who lean to the left, and others, like Glenn Hubbard, who lean to the right, endorse infinite horizon accounting. Because they understand something that I told Michelle repeatedly and have also told Bruce Barlett repeatedly. The fiscal gap is the only measure of our fiscal position that is mathematically well-defined.

Every other fiscal measure, including fiscal gaps calculated over any finite horizon, such as the CBOs 25-year fiscal gap Michelle references, are not mathematically well defined. The infinite horizon is mathematically well defined because it is the same number no matter what choice of internally consistent fiscal words we use to label government receipts and payments. Moreover, the infinite horizon fiscal gap is the only measure of our fiscal policys sustainability that puts everything on the books. It is also the only measure of our fiscal policys sustainability that is invariant to the choice of words.

Congresss choice of fiscal labels determines what gets put on and what gets kept off the books. I told Michelle that her grandparents Social Security benefits, for which she is now paying taxes, are not on the books because the government chose to call those payments transfers paid in exchange for FICA contributions not return of principal plus interest paid in exchange for purchase of government bonds.

Every mathematical model of the economys dynamic transition path incorporates the infinite horizon fiscal gap, which is called the governments infinite horizon intertemporal budget constraint. This constraint has to hold, which means the infinite horizon fiscal gap must be zero. Our countrys infinite horizon fiscal gap is far from zero. It would take an immediate and permanent 59 percent increase in all federal taxes or an immediate and permanent 33 cut in all federal expenditures (including official debt service) to eliminate our fiscal gap. The longer we wait to fix our fiscal system, the larger the adjustment needs to be. This means that (the journalist), and others her age, will need to pay even more for all the assets, including my own Medicare and Social Security benefits that have been left off the books.

Yes, something will have to give.

The $210 Trillion Gap

I will admit that Im not worried about the $210 trillion in unfunded liabilities. Long before we ever get to having to fund those liabilities, the country will be in a massive crisis.

Using the CBOs own numbers, the projected total US debt will be $30 trillion within 10 years, but the CBO also makes the rosy assumptions that there will be no recessions and that GDP will grow at a 4% nominal rate. Now, thats possible; but Im inclined to haircut it a bit.

If you asked me to bet the over/under on the debt in 2027, I would bet the over at $35 trillion. After the next recession the deficit will be $30 trillion within 45 years and then grow from there at a rate of anywhere from $1.5 to $2 trillion per year. Note: That is not the CBOs projected debt. It does not count the off-budget deficit that still ends up having to be borrowed. Last year the deficit was well over $1 trillion but we were told it was in the neighborhood of $600 billion. If any normal company tried to use accounting like the US Congress does, the SEC would rightly declare it fraudulent and shut it down immediately. .

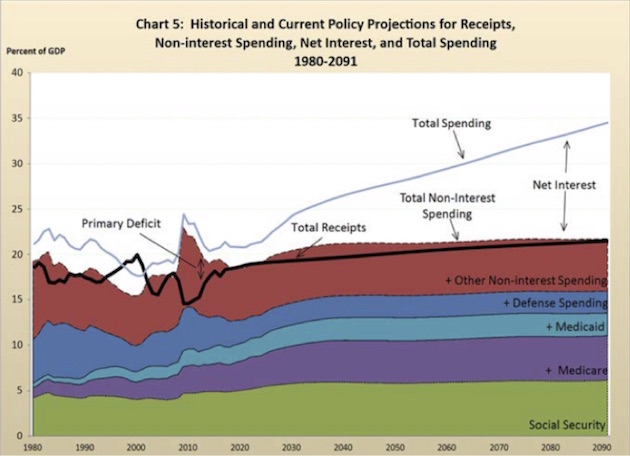

Heres another chart from the Treasurys annual financial report, projecting government receipts and spending:

Note that this chart expresses the various items as percentages of GDP, not dollars. So the relatively flat spending categories simply mean they are forecasted to grow in line with the economy, or just a little faster. But the space representing net interest grows much faster than GDP does fast enough to make total federal spending add up to one-third of GDP by 2090.

Obviously, this chart is based on all kinds of assumptions, and reality will be far different. I doubt we will make it to 2090 (or even 2050) without at least one global depression or other calamity that radically resets all the assumptions. Beneficial changes are also possible biotech breakthroughs that reduce healthcare expenditures, for instance.

Still, looking at the demographic reality of longer lifespans and lower birthrates, its hard to believe Social Security can survive over the long run in anything like its present form. But any major change will mean that the government is breaking its promise to workers and retirees.

Well, guess what: They backtracked on that promise decades ago. Few people noticed it at the time, and even fewer remember it now.

A Tax, Not a Promise

Theres a big difference between that federal government financial statement and similar ones from private companies. Liabilities for a business represent contracts it has signed the long-term lease on a building, for instance. The company agrees to pay so many dollars a month for the next 20 years. That obligation is enforceable in court. Even if the company enters bankruptcy, the court will award creditors damages from whatever assets it can recover.

The federal government doesnt work that way. It signs contracts all the time but often with escape clauses that private businesses could never get away with. Social Security is a good example.

Many Americans think of their Social Security like a contract, similar to insurance benefits or personal property. The money that comes out of our paychecks is labeled FICA, which stands for Federal Insurance Contributions Act. We paid in all those years, so its just our own money coming back to us.

Thats a perfectly understandable viewpoint. Its also wrong.

A 1960 Supreme Court case, Flemming vs. Nestor, ruled that Social Security is not insurance or any other kind of property. The law obligates you to make FICA contributions. It does not obligate the government to give you anything back. FICA is simply a tax, like income tax or any other. The amount you pay in does figure into your benefit amount, but Congress can change that benefit any time it wishes.

Again, to make this clear: Your Social Security benefits are guaranteed under current law, but Congress reserves the right to change the law. They can give you more, or less, or nothing at all, and your only recourse is the ballot box. Medicare didnt yet exist in 1960, but I think Flemming vs. Nestor would apply to it, too. None of us have a right to healthcare benefits just because we have paid Medicare taxes all our lives. We are at Washingtons mercy.

Im not suggesting Congress is about to change anything. My point is about promises. As a moral or political matter, its true that Washington promised us all these things. As a legal matter, however, no such promise exists. You cant sue the government to get what youre owed because it doesnt owe you anything.

This distinction doesnt matter right now, but I bet it will someday. If we Baby Boomers figure out ways to stay alive longer, and younger generations dont accelerate the production of new taxpayers, something will have to give.

If you are depending on Social Security to fund your retirement, recognize that your future is an unfunded liability a promise thats not really a promise because it can change at any time.

How Will We Fund the Deficit?

And now we come to the really uncomfortable part. Notice that Larry Kotlikoff said we would need an immediate approximately 50% increase in taxes to fund our future deficits. Thats what we would need to create a true entitlements lockbox with the funds actually in it. But surely everybody knows by now that there is no lockbox with Social Security funds in it. That money was spent on other government programs and debts. And so when the CBO doesnt count the trust funds as part of the national debt, they are not only being disingenuous, I think they are committing financial fraud. The money that will actually pay for Social Security and Medicare down the road is going to have to come out of future taxes, just as for any other debt of the US.

So at some point even though Republicans are jawboning hard about cutting taxes now we are going to have to raise taxes in order to fund Social Security and Medicare. I personally think it will have to be done with a value-added tax (VAT), because the necessary increase in income taxes would totally destroy the economy and potential growth.

(And yes, I know some of you will write back and say we had much higher tax rates in the 50s and we had good growth then, but our demographics and productivity levels were completely different in that era. Plus, nobody actually paid the highest tax levels. I remember that in the 80s, before Reagan cut the tax rate, I had so many deductions that my effective tax rate was about 15%. The irony is that after the Reagan tax cuts, my total tax payments went up, not down I lost all of my cool deductions! Aaah, the good old days

)

But the simple fact of the matter is that no Congress is going to fund Social Security and Medicare through tax hikes. Before they ever go there, they will means-test Social Security and increase the retirement age which they should.

Of course, Congress could always authorize the Treasury Department to authorize the Federal Reserve to monetize a certain amount of the Social Security and Medicare debt, which is essentially what Japan is doing (and seemingly getting away with it). I think we should all be grateful to the Japanese for being willing to undertake such a fascinating experiment in monetary and fiscal policy.

Let me close with a quick sidebar note. I think the Feds mad rush to raise rates and reduce its balance sheet at the same time is unwise. I mean, seriously, is the Federal Reserve balance sheet making that much of a difference to the US economy? Perhaps when that extraordinary balance was created, it did but not today. This is one of those times when I think our policy makers should go slowly and tread carefully. Just saying

San Francisco, Denver, Lugano, and Hong Kong

My few days in Portugal were not long enough. My hosts, the Soares dos Santos family, showed me a marvelous time. The conference I participated in was truly mentally exhilarating, but I came back exhausted and have picked up some bug that has given me a low-grade fever and stomach issues. Im sure Ill kick it soon. The good news is, it has also killed my appetite, so I am working off some of the calories that I picked up in Portugal.

I will be going to San Francisco (technically, to Marin County) to visit the Buck Institute, which is the premier antiaging research center in the world. I have been invited join their Buck Advisory Council, which will afford me the privilege of receiving once or twice yearly updates on where antiaging research is going. I will give you a report when I return. Then on November 7 I will be speaking to the Denver CFA Society. A week later I will fly to Lugano, Switzerland, for a presentation to a conference and Ill try not to push myself quite so hard on this next trip across the Pond. I will also be in Hong Kong for the Bank of America Merrill Lynch conference in early January.

I come back from Lugano the day before Thanksgiving, when in theory I will be cooking for 4050 friends and family. And I will again be making my special prime rib. Recently Ive been cooking it regularly when I host dinners for brokers and advisers who are interested in my new Mauldin Smart Core Program. I also make chili. And while people often say its the best chili theyve ever had, trying to claim you make the best chili in Texas will get you into trouble. There is really only very good chili; there is never the best. Chili is a very personal, very subjective taste experience.

Prime Rib: The Recipe

On the other hand, there is universal acclaim that my prime rib is the best ever. Over the years, Ive had hundreds of people ask me for the recipe; and so today, well in advance of Thanksgiving, Im going to share it with you. Those of you who are not interested should just stop right here, because this is about 20% of the letter; and while Ive been told I need to write shorter letters, you cannot abbreviate a great recipe. The details are critical.

First, the most crucial ingredient is a great piece of meat. You simply cannot skimp on the quality. And this is going to surprise people, but I have found that the best-quality prime rib comes from Costco. You can get a delicious 12- to 13-pound, already boned prime for about $120$130. Which is about 40% of what it costs at Whole Foods or Central Market. And frankly, the quality is better and more consistent. I was on a plane with the national food buyer for Walmart and asked him about that, and he claimed that Walmart has stepped up its game in order to compete with Costco. I have never put that claim to the test, but if any of you do, let me know how it turns out.

About four hours before youre going to cook the prime, take it out of the refrigerator and bring it up to room temperature. And then make the hand rub. Finely chop up two onions and place in a fairly large bowl. Then grab some fresh rosemary. Its best if you can actually pick it off a plant somewhere near you, but most good Whole Foods or other organic grocers have relatively fresh rosemary. Take off the leaves and discard the stems. Chop the rosemary finely. I probably use six to eight long stems of rosemary. Honestly, dont worry about using too much rosemary just make sure to chop it finely.

Add some form of coarse salt. At least one cup. More if you like your meat a little salty. Remember, this rub is going to go mostly on the outside. Then add 68 ounces of coarse-ground pepper. Lately, I have found smoked coarse-ground pepper at Whole Foods. It really does seem to add a little extra kick. Then throw in a generous amount of Cavenders Greek Seasoning. I might use 1/3 of one of their larger containers. Now slowly add a decent-quality olive oil to the bowl and stir until you get a consistent paste. (Over the course of time, you will develop your own sense of how you want your ingredients combined, and how much of what.)

And now we have to prepare the prime itself for seasoning. Take a sharp knife and essentially butterfly the prime, leaving maybe a 1-½ inch connection at the back. Then score the meat on both the inside and the outside every inch and and a half or so with a ½-inch-deep cut. Then take the rub and apply it on first the inside of the prime, working the rub into those scores you have made, so that more of the flavor can seep into the meat. Then fold the prime back together, and repeat the process on both the top and bottom of the meat. Place the prime in a roasting pan that has a grill that stands at least about ½ inch off the base of the pan. You want to convection cook the roast, not the metal of the pan.

Now, this is important. Get a good meat thermometer, preferably one that is electronic and that will alert you when the meat is at the proper temperature. (You can get a really good electric cordless meat thermometer at Bed, Bath & Beyond for under $40.) Have your oven preheated to 200° yes, we are going to slow-cook it. Cooking a prime too fast will end up making it not as tender.

When the prime is not bone-in, it will generally take about two to three hours to cook, depending on size. When the meat gets to 120°, take it out of the oven. That should mean it is about medium rare on the inside. If it will be more than 30 minutes before you eat, put it in an oven that is at about 100°, just to keep it warm (but not to cook it further). Fifteen minutes before you are ready to serve it, put the prime back into the oven, which has now been preheated to 500°. We are going to sear the outside of the meat to hold in the flavor and to have it at the perfect temperature for eating. Leave it in there for 10 minutes, then take it out of the oven, put it on your large wooden chopping board, cut it into the sizes you want to serve, and take it immediately to the table. And be prepared for people to tell you that youre a culinary genius. You dont even have to tell them you got the recipe from a financial newsletter.

If I get a sufficient response from this, next week I will even lay out my mushroom recipes. (Yes, there are two of them, and I generally make about 10 pounds of mushrooms to accompany the prime.)

And with that, I will hit the send button. Have a great week and start planning your Thanksgiving dinner early. And yes, ours does include several different types of turkeys, not to mention cakes and pies (I make the cakes if I have the time) and all the usual trimmings. Remember, there are no calories on Thanksgiving Day.

Your thinking he is going to see Blade Runner 2045 tonight analyst,

John Mauldin

subscribers@MauldinEconomics.com

Copyright 2017 John Mauldin. All Rights Reserved.