Understanding The Results of Financialization - Part II - "Mationalization"

-- Published: Sunday, 8 October 2017 | Print | Disqus

By Gordon Long

WHY A NEW FORM OF 'NATIONALIZATION' WILL OCCUR

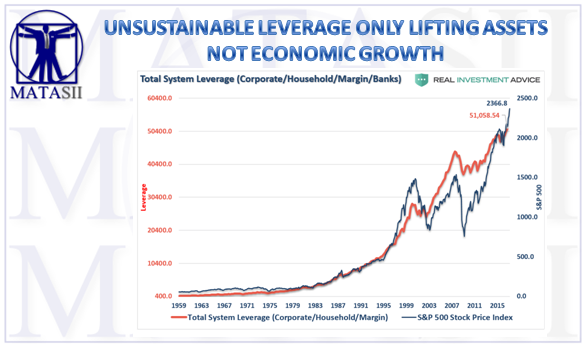

The extended period of Quantitative Easing (QE) and ZIRP have now left the major global central bankers in an untenable position because of the Era of Unlimited Leverage which it has fostered. According to the Bank for International Settlements, central banks combined asset holdings in the major advanced economies (the US, the eurozone, and Japan) expanded by $8.3 trillion over the past nine years, from $4.6 trillion in 2008 to $12.9 trillion in early 2017. Yet this massive balance-sheet expansion has had little to show for it. Over the same nine-year period, nominal GDP in these economies increased by only $2.1 trillion.

This implies a $6.2 trillion injection of excess liquidity the difference between the growth in central bank assets and nominal GDP that was not absorbed by the real economy and has instead, according to Stephen Roach of Yale University & Former Morgan Stanley Chairman, been 'sloshing around' in global financial markets, distorting asset prices across the entire risk spectrum.

As an Unintentional Consequence it has facilitated an explosion in financial leverage globally. This occurred BECAUSE of low interest rates (forcing a push for financial gearing) and additionally DUE to low rates (ready availability of credit). This shift can temporarily work if the collateral underpinning the leverage maintains being sound. If however the collateral becomes impaired or asset values fall, the whole foundation of this 'house of cards' expansion potentially collapses.

When you consider a problematic $400T global pension system is dependent upon bond and equity asset values, you can quickly imagine why policy planners know that the financial markets cannot be allowed to fall significantly or the financial, economic, social and political fabric of our entire system may be irreparably damaged!

THE NEW FORM OF "NATIONALIZATION"

The massive global debt problem and even greater financial leverage exposure is quickly and inevitably now reached the point of instability. The policy planners must find a way out of this quagmire. It is highly likely they already see this to be in the form of a new type of "Nationalization".

The word "Nationalization" is strongly repugnant to most Americans and is highly likely to never be used to describe the inevitable actions required to manage the situation central bankers and governments now find themselves in. Historically, this term has meant the government "Taking Over" with 100% ownership. This is not what is likely to occur!

What is more likely to evolve is a progression of what we have already been witnessing. Governments are more likely to "Take Control" through financial "Guarantees" in a more sophisticated and stealth fashion.

EXAMPLE 1 - GOVERNMENT 'CONSERVATORSHIPS'

An example of the new emerging form of "nationalization" was witnessed during the 2008 Financial Crisis when Fannie Mae and Freddie Mac were taken control by the US government and placed in "Conservatorship". As a consequence today the US government controls 95% of all US mortgages. How is this not Nationalization?

We can expect forms like this, which received little public discord, to be a model for future government policy approaches.

EXAMPLE 2 - CENTRAL BANK 'FACILITY GUARANTEES'

During the last crisis the Federal Reserve also abruptly implemented 12 Facility Guarantees to arrest a rapidly deteriorating systemic breakdown in the financial markets. It was fundamentally aimed at creating assurances and confidence through Federal Reserve backed Guarantees. It proved to be highly successful.

We can additionally expect this form of "nationalization", which also received little public objection, to be a core structural approach for future Federal Reserve & Central Bank policy approaches.

TRIAL BALLOONS WARN OF WHAT IS TO COME

Charles Hugh Smith and myself lay out examples (in the video below) of trial balloons which we are already seeing from the ECB, Fed and JPM to prepare us for the next crisis when the Equity markets will potentially need to come under stronger "central policy control".

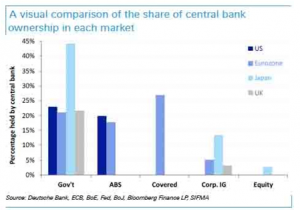

Without any recession or crisis, major central banks are purchasing more than $200 billion a month in government and private debt, led by the ECB and the Bank of Japan.

The Federal Reserve owns more than 14% of the US total public debt.

The European Central Bank (ECB) and Bank of Japan (BOJ) balance sheets exceed 35% and 70% of their GDP.

The ECB owns 9.2% of the European corporate bond market and more than 10% of the main European countries total sovereign debt.

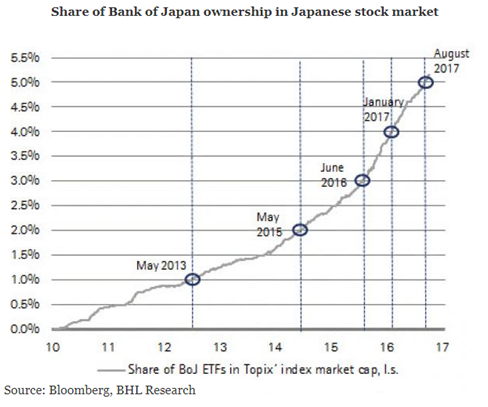

Now the global equity markets are witnessing the Bank of Japan recently increase its direct ownership of stocks. The BoJ conducts purchases of equities as part of its QQE (Quantitative & Qualitative Easing) and Deutsche Bank estimates that the BOJ effectively holds nearly 5% of the Japanese stock market.

The Bank of Japan is now a top 10 shareholder in 90% of the Nikkei.

The BOJ is on course to become the largest shareholder of the Nikkei 225s largest companies. In fact, the Japanese central bank already accounts for 60% of the ETFs market (Exchange traded funds) in Japan.

Over time the BoJ has become increasingly important. Its share of the Japanese stock market has risen from 0% in late 2010 to now 5% (see chart below). This has been funded from thin air, i.e.by simply printing money. The interesting point is that the incremental gains of one percentage point in ownership are realized in an increasingly shorter time period. It took 4 1/2 years to reach 2%, but only 2 1/4 years to add another 3 percentage points (to the current 5%). This reflects two patterns: the declining positive impact of BoJ buying on stock prices and the increase in buying volumes by the central bank.

We discuss examples in more detail (in the video below) regarding the expanding role Central Banks like Switzerland and others; Sovereign Wealth Funds like the Norwegian Wealth Fund; and Government Agencies like Japan Post are increasingly taking in the global equity markets. Financial markets are increasingly becoming more controlled and dependent on direct government and central bank actions. In reality we no longer have "Free Markets"!

THE ROAD AHEAD

It is clear to anyone following the financial markets closely, what is steadily occurring as central bankers and governments are becoming more involved and taking more control.

During the next crisis expect the rules to change and the new form of "Nationalization" to occur. It should not come as a surprise to anyone.

In the following 36 minute video myself and Charles Hugh Smith further explore what is occurring with the aid of 36 supporting slides.

The content on this site is protected

by U.S. and international copyright laws and is the property of GoldSeek.com

and/or the providers of the content under license. By "content" we mean any

information, mode of expression, or other materials and services found on GoldSeek.com.

This includes editorials, news, our writings, graphics, and any and all other

features found on the site. Please contact

us for any further information.

Live GoldSeek Visitor Map | Disclaimer

The views contained here may not represent the views of GoldSeek.com, Gold Seek LLC, its affiliates or advertisers. GoldSeek.com, Gold Seek LLC makes no representation, warranty or guarantee as to the accuracy

or completeness of the information (including news, editorials, prices, statistics,

analyses and the like) provided through its service. Any copying, reproduction

and/or redistribution of any of the documents, data, content or materials contained

on or within this website, without the express written consent of GoldSeek.com, Gold Seek LLC,

is strictly prohibited. In no event shall GoldSeek.com, Gold Seek LLC or its affiliates be

liable to any person for any decision made or action taken in reliance upon

the information provided herein.