-- Published: Friday, 17 November 2017 | Print | Disqus

By John Mauldin

Vanity of Vanities

Those Crazy Swiss

The Absurdities in the Bond Markets

Lugano, Atlanta, and Hong Kong

Vanity of vanities, saith the Preacher, vanity of vanities; all is vanity.

Ecclesiastes 1:2, King James Version (attributed to King Solomon in his old age)

This weeks letter will take a look at the growing number of ridiculous, inane, and otherwise nonsensical absurdities that fill the daily economic headlines. I have gone from the occasional smile to scratching my head now and then to WTF moments several times a week.

Wondering if it was just me, I recently sent an appeal to a what became a large number of my friends and fellow writers and analysts, asking for their graphic examples of this paranormal economic activity. Suffice to say, it is not just me who sees absurdities. I received so many responses that I may have to extend this letter another week or two. (Note: This letter will print long, as there are lots of graphs.)

Some of what youll see depicted in the following charts originated a decade ago in the Global Financial Crisis or was caused by the reactions of central bankers to that crisis. The many shocking, previously unimaginable acts by central banks and governments left us so numb that I think we started to simply accept them without much thought. That was our mistake: We must confront the unthinkable, not just shrug our shoulders at it. Because when we have our next crisis, I will bet you dollars to donuts that central banks and governments will react in ways that are even more unthinkable.

Before we get our thinking caps on, let me remind you that early registration is now open for my next Strategic Investment Conference. The dates are March 6-9, 2018, at the Manchester Grand Hyatt in San Diego. Well have a wonderful time with an all-star cast including Jeffrey Gundlach, Mark Yusko, John Burbank, Niall Ferguson, and George Gilder. Im in negotiations with other well-known names, too.

This year were making a special effort to sell out the conference as early as we possibly can. I really want to focus my full attention on designing the program and working with the speakers to deliver an outstanding experience. Thats much easier when I dont have to think about whether there are still unsold seats.

To that end, were offering exceptionally generous discounts for early registration. If youve already decided to attend, you would do us both a big favor by registering now. Youll save a few hundred dollars and avoid getting stuck on the waiting list. Click here to register or get more information.

Now on to the bonfire.

Vanity of Vanities

If you work in the financial industry youve probably read, or at least know plenty about, the Tom Wolfe novel Bonfire of the Vanities. Its a great book, but its not the source of this letters headline. Im thinking back further to the original bonfire of the vanities in fifteenth-century Florence.

In 1490 the ruling Medici family brought in Dominican friar Girolamo Savonarola to serve them, but within a few years he was more or less ruling the city. In 1495, during the pre-Lenten carnival, Savonarola began hosting a bonfire of the vanities, at which people would burn objects that inspired the deadly sin of vanity: mirrors, cosmetics, musical instruments, and so on. This being Florence, they also destroyed tons of artworks, tapestries, books, furniture, and other priceless treasures. Did doing so make them any less vain? Probably not, but Im sure the bonfires were quite magnificent.

In a similar manner, we in this century routinely burn hard-won lessons (or at least expel them from our thoughts) because someone with an ulterior motive convinces us theyre useless or harmful. Thats rarely true, as we often discern too late, and then we have to learn the same lessons again.

Think about this. How often do central bankers, regulators, corporate leaders, lawyers, politicians, and ordinary investors make the same mistakes over and over again? All the time. If we would stop burning our memories, we might make better progress. But no, we must have our bonfires. And so the absurdities are perpetuated.

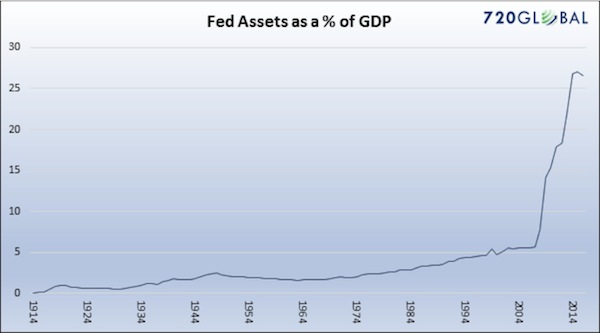

To kick off our tour of absurdities, Michael Lebowitz of 720 Global sends this chart of Federal Reserve assets as a percentage of GDP. You might notice a slight trend change along about 2008:

Not to put too fine a point on it, but this is bonkers. I understand that we were caught up in an unprecedented crisis back then, and I actually think QE1 was a reasonable and rational response; but QEs 2 and 3 were simply the Fed trying to manipulate the market. The Keynesian Fed economists who were dismissive of Reagans trickle-down theory still dont appear to see the irony in the fact that they applied trickle-down monetary policy in the hope that by giving a boost to asset prices they would create wealth that would trickle down to the bottom 50% of the US population or to Main Street. It didnt.

The Fed has left that bloated balance sheet alone for almost 10 years. And now for some reason they feel it is urgent to reduce the balance sheet even as they also raise rates. This is not model-based monetary policy; it is simply an emotional monetary policy experiment. I can understand raising rates I wish they had done that four years ago. I can even understand reducing the balance sheet. But at the same time? When you dont know what you dont know? I mean really, there is no way to know how the market is going to react to either of these events, let alone to both at the same time. This seems to me the height of monetary policy lunacy.

The Feds stimulus efforts manifested themselves, among other places, in years of near-zero interest rates, helpfully illustrated here by Peter Boockvar:

We all lived through this remarkable set of experiments, but its still amazing to think that in 20072008 the Fed chopped short-term rates by five full percentage points in just five quarters. Today we agonize over whether theyll hike rates by half as much, spread over five years or more. Note also that this gargantuan rate cut still couldnt avert a near meltdown of the banking system. You can argue that it would have been even worse to do nothing, but its hard to argue they didnt do all they could have.

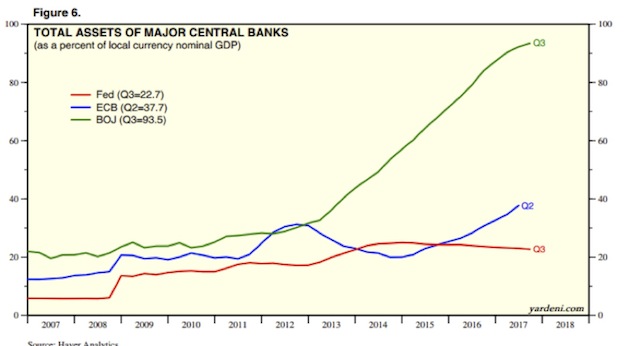

But it wasnt just the Federal Reserve. The European Central Bank and the Bank of Japan have both grown their balance sheets more than the US has. The Bank of Japans balance sheet is almost five times larger in proportion to GDP. And it is still growing. The Land of the Rising Sun has become the land of the rising central bank balance sheet. This graph is courtesy of my friend Dr. Ed Yardeni:

Those Crazy Swiss

Meanwhile, the more sober-minded (hah!) gnomes of the Swiss National Bank expanded their own balance sheet at a much steadier pace, though in percentage terms they blew it up far more than the Fed or the BOJ did theirs. The Swiss National Bank is now the worlds largest hedge fund.

My friend Dennis Gartman wrote me yesterday, saying,

We have written many times about the fact... and it is a fact... that the Swiss National Bank has effectively become both the nations central bank and one of the largest, if not indeed the very largest, hedge funds in the world. The process began several years ago when the SNB swore that it would do what it could and using what methods were available to it to weaken the Swiss franc relative to the EUR and to the US dollar. It has succeeded, until recently, creating Swiss francs out of the thinnest of air, and selling those Francs vs. the EUR and the dollar, and then taking those EURs and dollars to buy European and US equities and debt securities.

The SNBs balance sheet is a CHf 813 billion (and given that the CHf and the US dollar are effectively at parity one with the other that CHf 813 billion is the same as $813 billion) and this is very nearly 125% of the Swiss GDP. By comparison, the Feds balance sheet of $4.5 trillion is but 25% of the US GDP. In other words, if the Fed is taken to task for being expansionary, the SNB is truly explosive!

Of the CHf 813 billion on the Banks balance sheet, 760 billion of it is the form of securities, of which 90 billion are in equities. The other 670 billion are held in EUR and US debt securities.

Thus far this has been a huge, stunning, almost unimaginable profit for the SNB and theoretically for the people of Switzerland. However, the problem is that the SNB will have enormous difficulty in liquidating this massive portfolio, for once the news leaks out that the Bank is selling the bids will disappear; the CHf will soar in price while debt and equity markets melt away.

What the SNB has done here is stunning; some have even called it nearly criminal in nature. We suggest that there is nothing at all criminal in what the SNBs leaders have done and that they are well within their legal guidelines; however, what they have done is optically and philosophically wrong and very badly so. This is QE gone very badly wrong, rivaled only by the same actions taken by the Bank of Japan that openly deals in the forex, debt and equity markets in Tokyo, buying ETFs on a very regular basis and becoming one of Japans largest public shareholders. This is central banking gone very, very badly awry. It will be stopped when equity prices collapse.

As I wrote earlier this year:

The SNB owns about $80 billion in US stocks today (June, 2017) and a guesstimated $20 billion or so in European stocks (this guess comes from my friend Grant Williams, so I will go with it).

They have bought roughly $17 billion worth of US stocks so far this year. And they have no formula; they are just trying to manage their currency.

Think about this for a moment: They have about $10,000 in US stocks on their books for every man, woman, and child in Switzerland, not to mention who knows how much in other assorted assets, all in the effort to keep a lid on what is still one of the most expensive currencies in the world.

Switzerland is now the eighth-largest public holder of US stocks. And apparently they are concentrating on the largest of the large-cap stocks. The own 19 million shares of Apple (as of March 31). That is roughly 3% of the current market.

Im in Switzerland as you read this, so I am personally experiencing the reality of currency strength. Have you ever paid $12 for a Diet Coke? (Seriously!) No wonder the SNB is worried about the valuation of their currency.

I will be speaking at a conference in Lugano on Monday. The conference sponsors have asked me to give them three questions to ask the attendees during my speech. One of those questions is, do you think the Swiss National Bank will eventually hold $1 trillion in assets? And do you agree with that policy? I will be asking some of the larger asset managers what they will do and how they will react. Hedging? How do you do that in that environment?

Gartman is right: How can the SNB sell? The Swiss franc would levitate almost instantly, which is the one thing they are desperate to avoid. As long as people keep trying to convert their money into Swiss francs (at -0.75 basis points!), the natural direction for the franc will be up unless the SNB continues to intervene in foreign markets. My bet is that they will do so and that this will not end well. Or maybe theyll get lucky and their even more massive bond portfolio will offset their losses.

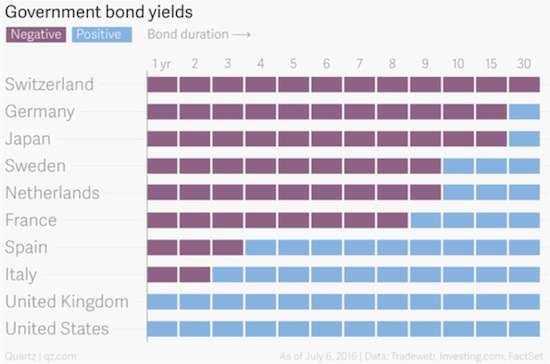

The Absurdities in the Bond Markets

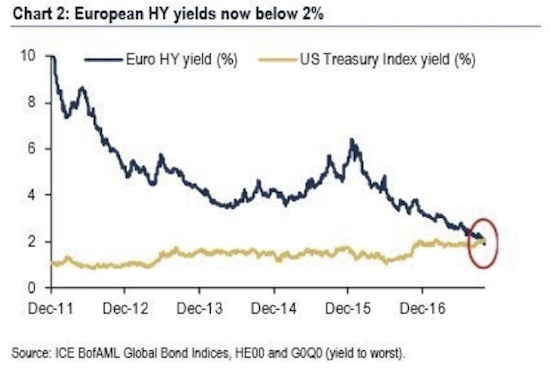

Not coincidentally, European yields are at rock bottom, or actually below that, in negative territory. And what is even more absurd, European high-yield bonds, which in theory should carry much higher rates than US Treasury bonds, actually yield below them. Heres a chart from old friend Tony Sagami:

Interest rates are supposed to reflect risk. The greater the risk of default, the higher the rate, right? Yet here we see that European small-cap businesses are borrowing more cheaply than the worlds foremost nuclear-armed government can. That, my friends, is absurd.

Understand, the ECB is buying almost every major bond it can justify under its rules, which leaves smaller investors fewer choices, so they move to high-yield (junk), driving yields down. Ugh.

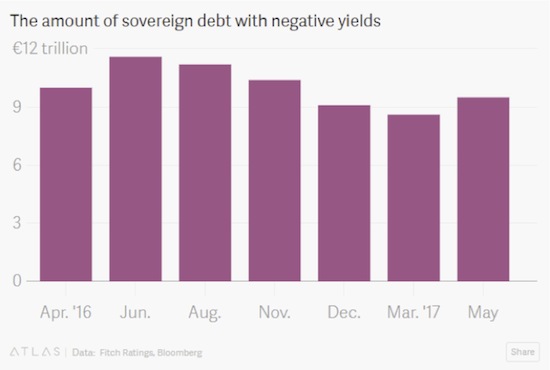

And can anything be more absurd than negative interest rates in long-term bonds?

This 2016 article on the Quartz site, under the subhead World Gone Mad, makes clear the level of ridiculousness were looking at here:

If you were to buy, at random, any government bond, there is a one in three chance youd lose money if you held onto it until it matured. That is, around a third of all developed-country government debt or more than $7 trillion [That was last summer. Its now $9 trillion, so its even worse JM], in terms of market value is now trading at negative yields, according to Citi. That means that investors are effectively paying borrowers to lend to them giving away $100 and a few years later getting back $99. In the euro zone, more than half of all outstanding bonds are priced in this upside-down way, according to Tradeweb. (source)

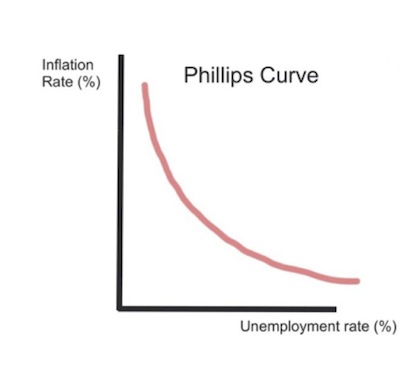

All that said, the economists who designed these interventions had their reasons. They thought lower interest rates and liquidity injections would create jobs, spur investment, and eventually produce inflation. The idea was to then reduce the stimulus before inflation got out of control. Their gauge for assessing this tricky process is the unemployment rate. An economy at full employment is one in which inflation is right around the corner. The theoretical relationship looks something like this chart from Gary Shilling.

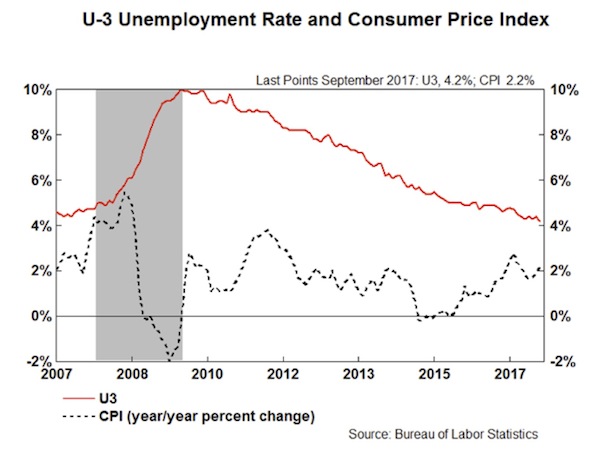

In fact, we now have very low unemployment, accompanied by stubbornly low inflation. Why is that? No one really knows. All sorts of theories are floating around, but none have yet proven helpful in restoring the Phillips Curve. Heres reality, again via Gary Shilling:

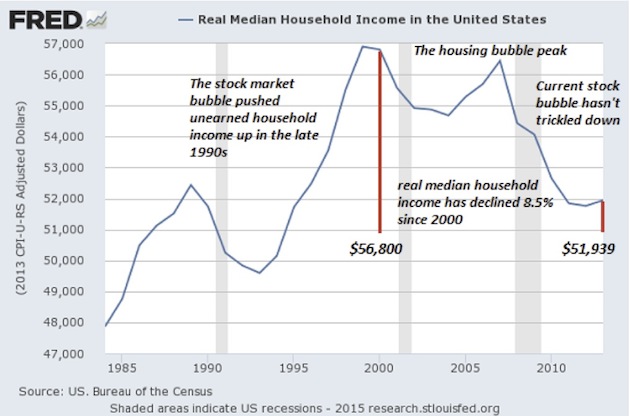

The result is a strange economy in which the people who want jobs mostly have them but remain deeply dissatisfied, stressed, overleveraged, and often angry. Consider this graph of real median household income, from my friend Murat Koprulu.

This is median, not average, household income. That means half of households are doing better and half worse. Its also inflation-adjusted, so the amounts are consistent over time. We see that the median family is roughly back where it was 20 years ago, in the mid-1990s. Worse, its still far below where it was ten years ago before the financial crisis. Is it any wonder people are mad?

One more absurdity. In the US we often think education is the key to getting ahead. Thats not necessarily the case anymore. Heres another chart Murat sent me, showing real average hourly wages by education level.

From 20072014, possessing an advanced degree enabled you to get ahead only in a relative sense. Your wages stayed flat while those of the less-educated fell.

Notice how having some college was actually more negative for wages than having only a high school education. How can that be? Possibly because going to college without obtaining a degree leaves you in debt with less practical experience than your peers who went straight to work after high school.

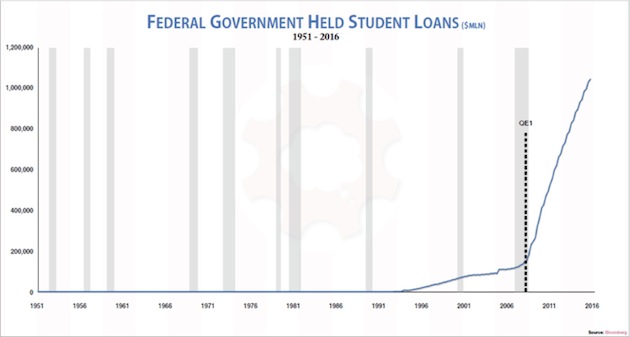

To that point, student debt is quickly becoming a problem for everyone. Look at this chart from Grant Williams on student loan debt held by the federal government. Do we add that to our national debt?

Taxpayers are on the hook for over a trillion dollars in student debt. Unlike mortgage or business debt, student debt is backed by no tangible asset you can repossess. It bought knowledge that now hopefully resides in the students brain, but it may have just gone in one ear and out the other. That makes this debt uniquely risky. You and I are taking that risk, like it or not.

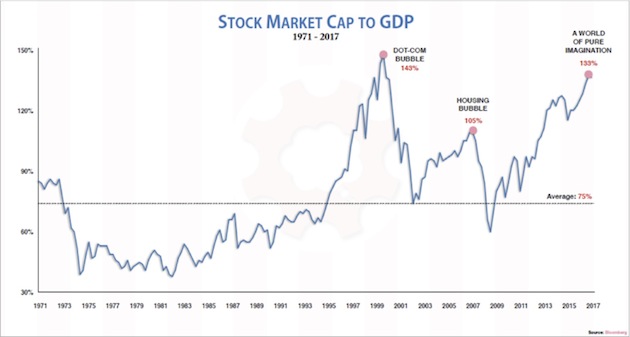

And heres another chart from Grant Williams, showing stock market capitalization to GDP. We are only another healthy bull market run away from being back to dot-com bubble levels. A run that many of my friends firmly believe awaits us.

The US stock market as a percentage of GDP is now far bigger than it was at the housing bubbles peak, and its rapidly approaching the dot-com bubble peak. That ought to make us a little nervous as we watch the Dow hit new all-time highs.

And we will close this weeks adventure into absurdities with a note I got from Louis Gave this morning. Rather than just looking for absurdities in the developed world, Louis research team at GaveKal scours the entire world in depth every day. So he gives us a few lesser-known absurdities. [My comments will be in brackets.]

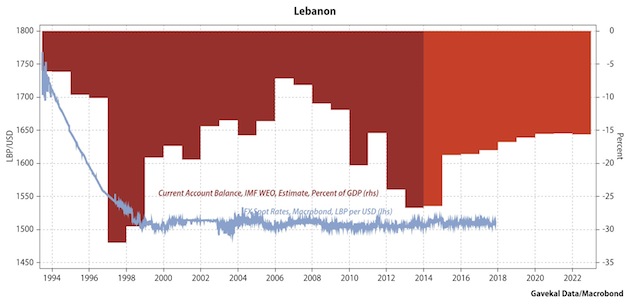

Usually currency pegs are not a bad place to start when looking for absurdities.

What are the odds of Lebanon keeping its peg now that Saudi wont bankroll it? After all, you have a pegged currency with current account deficit in double digits relative to GDP:

And once the Lebanese peg goes, will it be like Thailand in 1997 with Bahrein, Qatar, Oman, Egypt, Pakistan and ultimately Saudi all following suit?

If so, you can kiss goodbye to those large defense orders

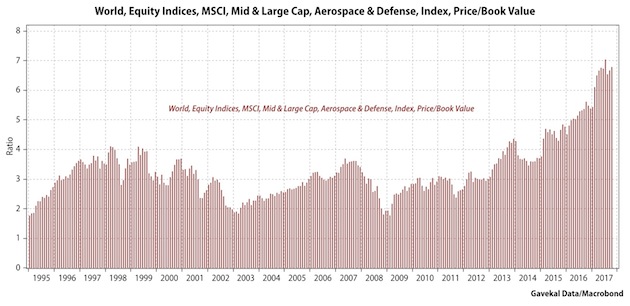

Incidentally, why pay 7x book to buy defense stocks when it seems pretty obvious that the wars of the future will either be:

low-grade terrorist events or

cyber warfare

Who will need the big destroyers, tanks, and missiles anymore? Increasingly, our wealth is not about building and factories but about zeros and ones in a computer. Yet defense stocks have never been so richly valued:

And this at a time when 95 cents out of every dollar collected by the US government goes to either pay a) interest, b) entitlement spending and c) defense. Which do you think goes first?

I dont think it is interest (hard to make them that much lower). And I doubt it will be entitlements. Which leaves you with defense. And so just like European nations before it, the US will slash defense spending to keep the welfare state alive

So why pay 7x book for defense stock?

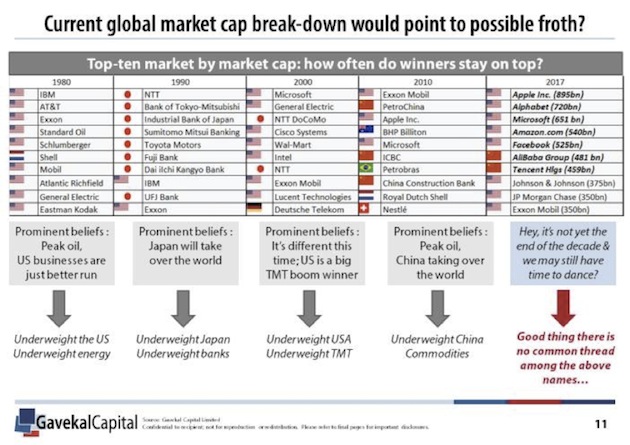

There are many other ideas. A lot of them linked to the craziness in the bond market (negative swiss yields, Italian junk below UST, etc

). But how about this one:

Okay, John back. Please note the serious level of sarcasm in the right-hand column above: Good thing there is no common thread in the above names... Its all tech and all digital in the top seven. Note, however, that Exxon Mobil keeps hanging in there.

The above is why I love Louis and read his analysis every time I get a chance. Its also one of the reasons that hes a perennial keynote speaker at my conference. Not only is he a crowd favorite, he comes up with truly investable ideas that the people in the room havent necessarily heard of. And so one last blatant bit of promotion you really do want to figure out how to get to San Diego for the Strategic Investment Conference. Dont procrastinate.

Lugano, Atlanta, and Hong Kong

As you read this letter, I am hopefully already in Lugano, Switzerland and meeting with my friend and business associate Tony Courtney at the Hotel Villa Castagnola late in the evening. I will spend the next two days in meetings and exploring the area before the conference on Monday and Tuesday. If youre in the area, its the Lantern Fund Forum. I have never been to the Italian region of Switzerland and am really looking forward to it. Ive actually been to half a dozen other areas in the French- and German-speaking parts of Switzerland, but this will be my first visit to Lugano. I guess I should know my geography better, but I was surprised that the best way to get to Lugano was to fly into the Milan airport and take a short car ride across the border. Lugano is in the Lake Como area, and I have always wanted to get there, as so many people have told me that its one of the most beautiful parts of the world. This trip also affords me the opportunity to break out my winter clothes, as it gets nippy there at night something we havent experienced in Texas for quite some time.

Shane and I will be in Hong Kong for the Bank of America Merrill Lynch conference in early January. That trip will be made even more fun because Lacy Hunt and his wife JK will be there with us. We are going to take an extra day or two and be tourists. Ive been to Hong Kong many times but have never really gotten out of the business district. Well, Louis Gave did pick me up in his old-fashioned Chinese Junk and took me around to the other side of the island to the yacht club, where we had dinner. The water got a little choppy and I got a little seasick, so I was grateful for the car ride back. But it was really quite a beautiful outing. I very much like Hong Kong.

Its time to hit the send button, as there are a lot of last-minute things to do before we board the plane for Europe, and I absolutely have to get into the gym for a bit. You have a great week! And I hope you have a fabulous Thanksgiving planned. I know we do.

Your fascinated by all the absurdities in the world analyst,

John Mauldin

subscribers@MauldinEconomics.com

Copyright 2017 John Mauldin. All Rights Reserved.

| Digg This Article

-- Published: Friday, 17 November 2017 | E-Mail | Print | Source: GoldSeek.com