-- Published: Tuesday, 28 November 2017 | Print | Disqus

By Gordon Long

THE GREAT CONUNDRUM

WHAT IS THE CONUNDRUM?

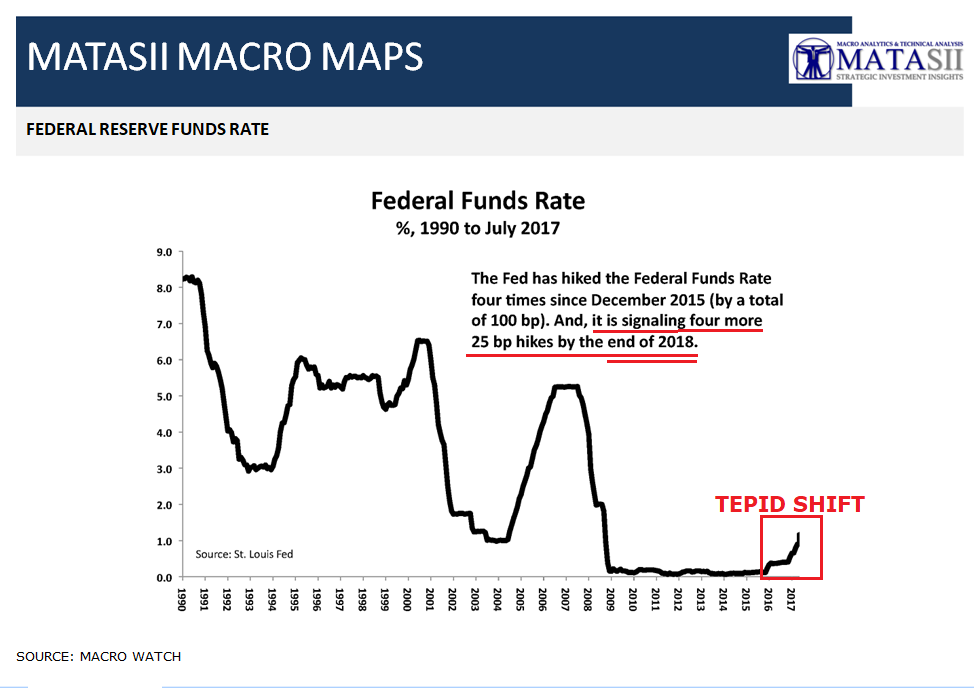

The Federal Reserve has been very clear through its' forward policy guidance that it will slowly increase the Fed Funds Rate. "Slow" however should more appropriately described here as at a "Glacier Pace"!

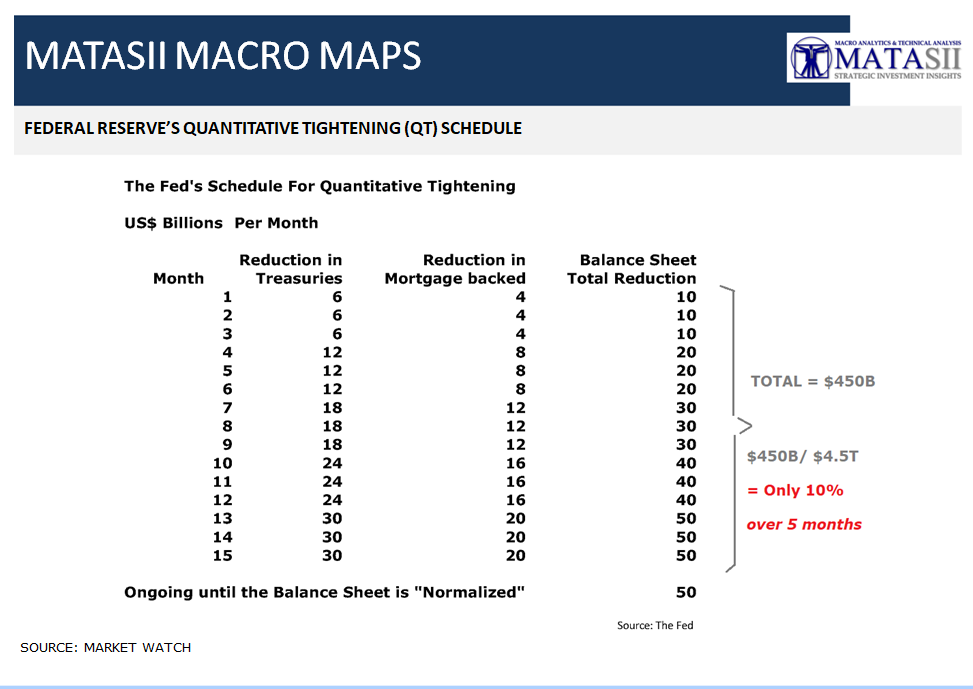

Additionally the Fed plans to gradually reduce the central banks balance sheet at a slowly increasing rate. A rate that over 15 months totals only 10% of the $4.5T growth in the Fed's Balance Sheet since the beginning of the Fed's Quantitative Easing (QE) and ZIRP.

The general perception is that going forward the Fed will either:

Raise Rates & Reduce Balance Sheet as is being presently signaled,

Do Little (in reality what they are actually doing) or Marginally Nothing Further, or

Resume another version of QE ∞, plus Negative Interest Rate Policy (NIRP) and possibly Helicopter Money.

WHY QUANTITATIVE TIGHTENING?

The expressed reasons for the requirement for "Normalization" of US Monetary Policy is that the US Economy is now over 8 years into the recovery with low unemployment rates and signs of a broad based (though weak) recovery. It is my opinion both of these conditions are not valid, however I will leave that for another day.

Instead I would like to suggest what may be a few

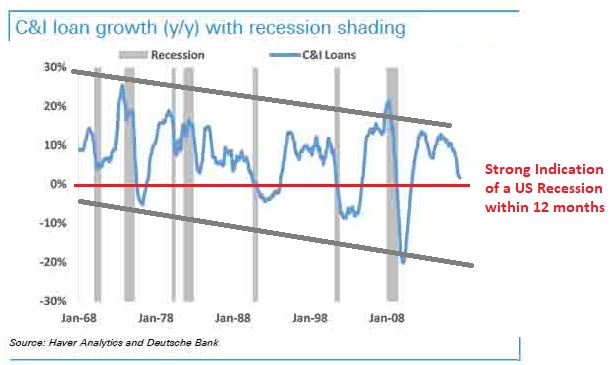

The above Fed Chart has been Extremely Accurate In Warning the Fed of Recessions (shown in grey)

WHAT THE FED SEES

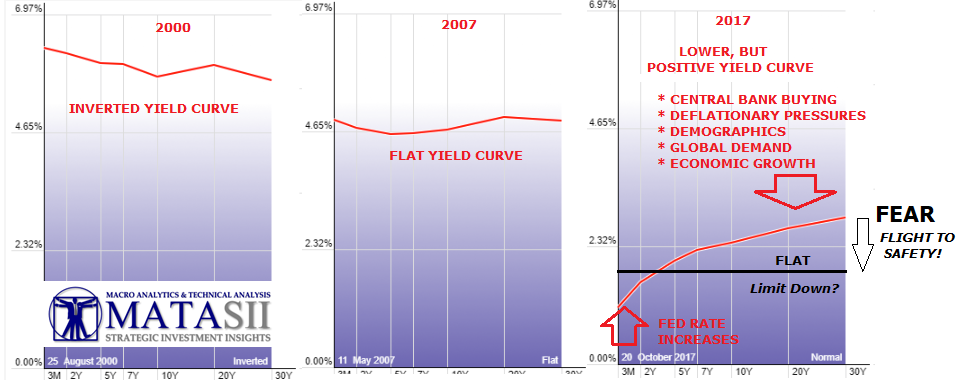

Having lived through and as an investor participated in 1987, 2000 and 2007 I learned a number of lessons. One is the importance of advanced shifts in the Currency, Credit and Yield markets prior to major reversals in the equity markets.

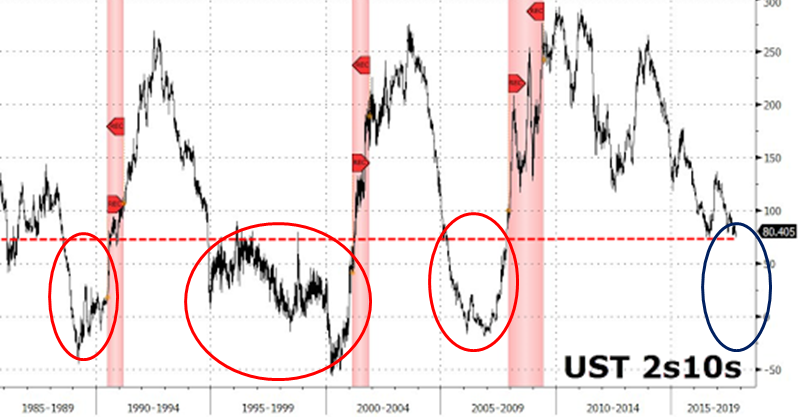

The yield curve is of particular note since it is presently almost completely ignoring the Fed and has been steadily flattening. This is problematic, especially for the Fed!

We an see that the 2-10 US Treasury spread is below the dotted red line which has always preceded a major market correction, as well as a US Recession.

What I learned was that there is always a shock or surprise (shown in Blue) which comes out of "nowhere".

What that surprise is doesn't really matter except it occurs because of hidden underlying market dislocations. Extreme valuations, low volatility, market speculation, excess leverage etc. etc. all contribute, but are not in themselves the direct cause. Together they all contribute.

The only thing you can be certain of is that market fragility will abruptly fracture. The Fed is acutely aware of this and knows it must be fully prepared!

The irony is that QT will likely contribute to this fragility and shock. There in lies the FOMC's Conundrum!

We can see the yield curve comparison prior to the 2000, 2007 tops along with today's level. Though the yield curve is not flat or inverted (yet) it is setup for exactly that to occur.

The black line shows that a couple of minor Fed rate hikes on the short end, and a shock which precipitates the normal "Flight to Safety" into the security of longer dated US Treasuries and the yield curve would be flat-to-inverted in a "New York Minute"!

What may be a conundrum for the FOMC next week, need not be a conundrum for you!

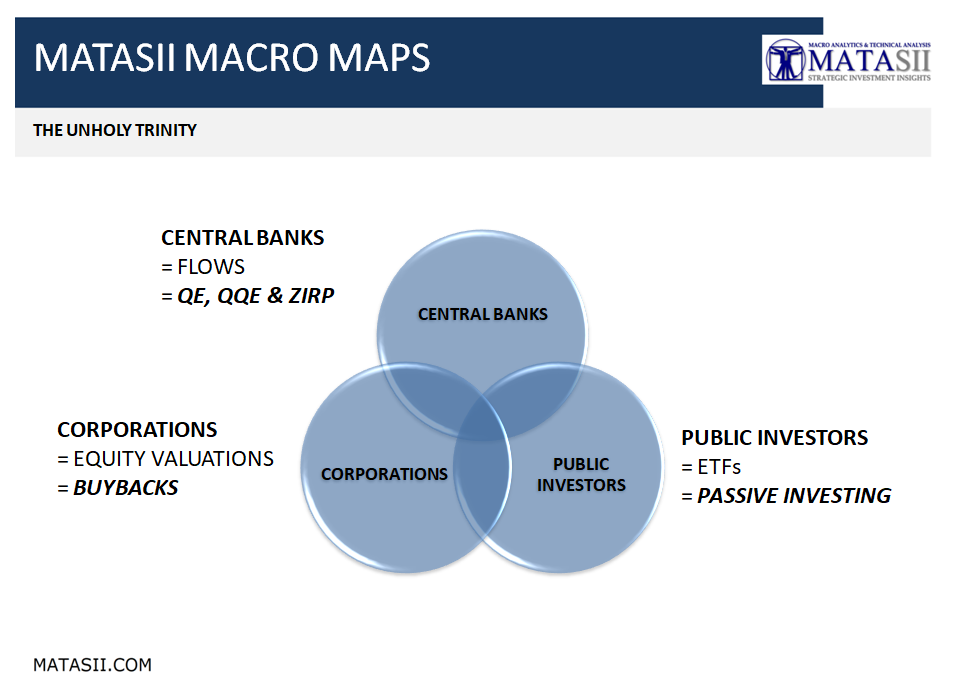

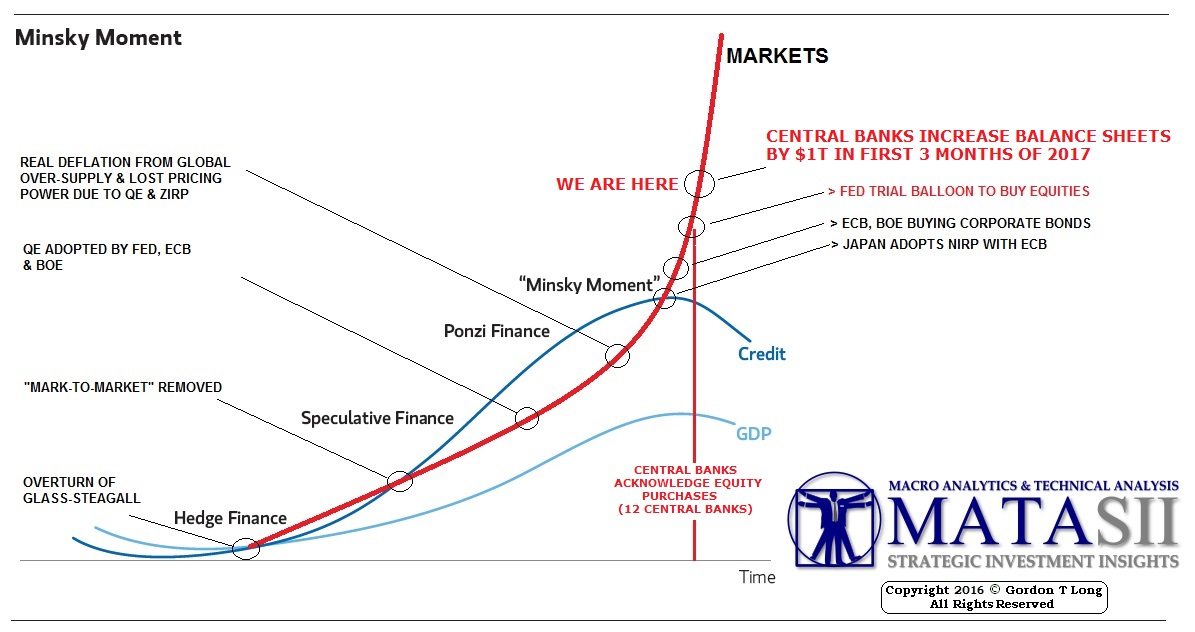

AN UNHOLY TRINITY

To fully appreciate the conundrum the Fed presently faces we need to understand the importance of three major activities operating independently yet intertwined in three different areas of investment influence.

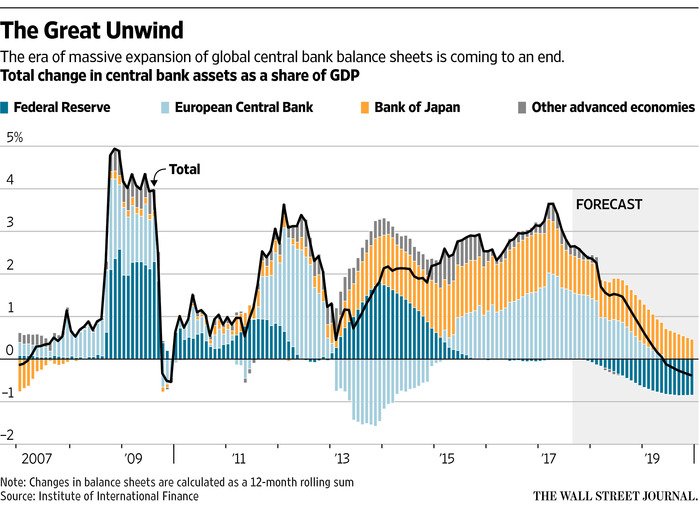

CENTRAL BANKS have been heavily committed to QE & ZIRP after the 2008 Financial Crisis. The has produced Credit & Liquidity which I will label FLOWS.

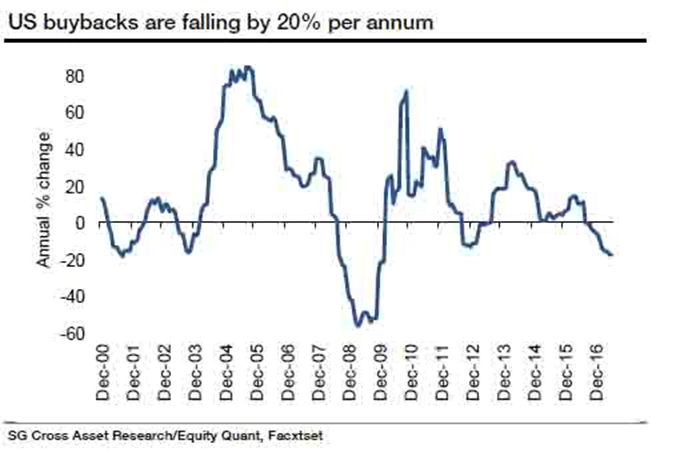

CORPORATIONS have been heavily committed to Stock Buybacks since the advent of QE & ZIRP. These activities have fostered major movements in EQUITY VALUATIONS.

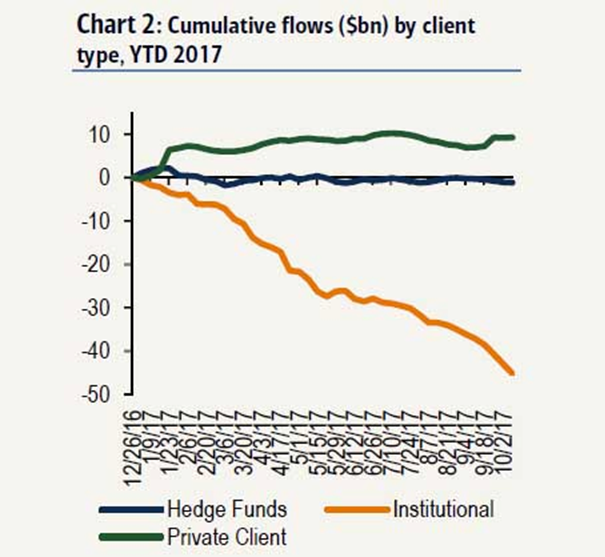

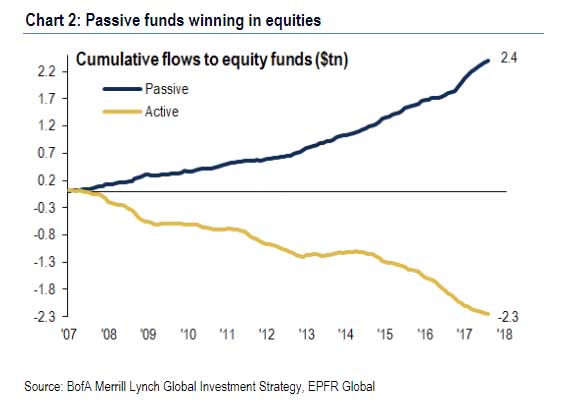

PUBLIC INVESTORS have shifted from the use of Active Managers (ie Mutual Funds) to Investments vehicles using quick entry and exit ETF's which have become dominated by those tracking the major indexes or popular assets such as the FAANGS. This shift has fostered PASSIVE INVESTING.

Unfortunately, the Unintended Consequences of these three entities has the potential to now create a perfect storm.

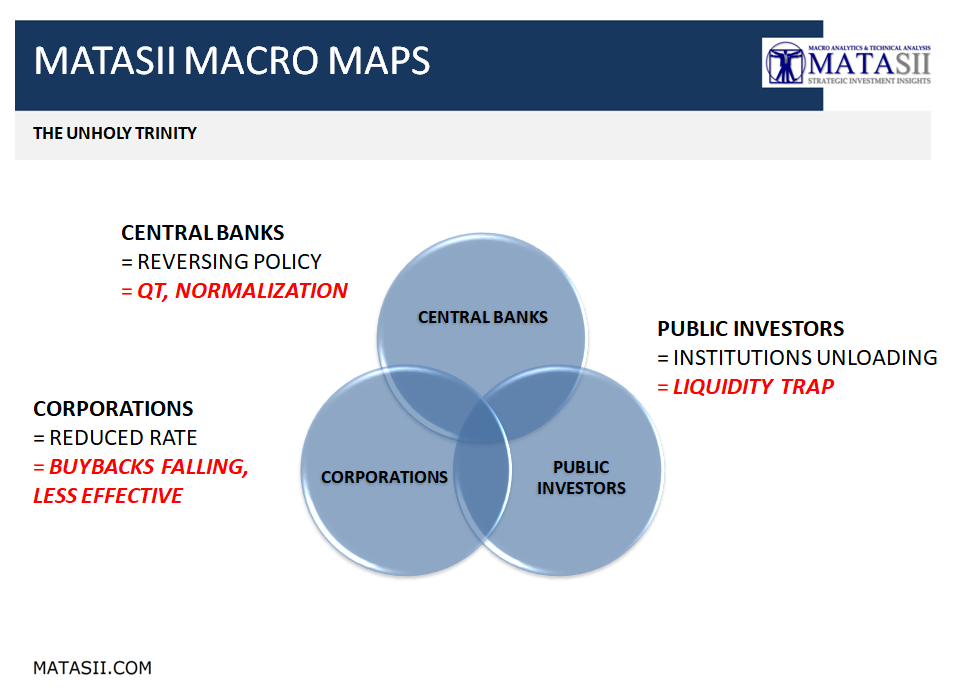

CENTRAL BANKS are REVERSING POLICY to Quantitative Tightening (QT)

CORPORATIONS are REDUCING THE RATE of Stock Buybacks,

PUBLIC INVESTORS are heavily into Passive Instruments that may LACK LIQUIDITY if aggressive selling occurs which is specifically the reason they were bought in the first instance.

Consider the degree which these shifts are occurring:

CENTRAL BANKERS: QE, QQE & ZIRP going to QT, Normalization

CORPORATIONS: SHARE BUYBACKS now Falling & Affect being Reduced

INVESTORS: PASSIVE INVESTMENT (ETF GROWTH) now seeing Professionals Leaving & Public Rushing In

The psychological issue with the collapsing Unholy Trinity will be the perception of the withdrawal of the Bernanke / Yellen PUT. The Central Bank will no longer be seen to be supporting higher asset values in its quest to stimulate consumer demand through the Wealth Effect.

This may be a bigger issue then the reality of the individual components?

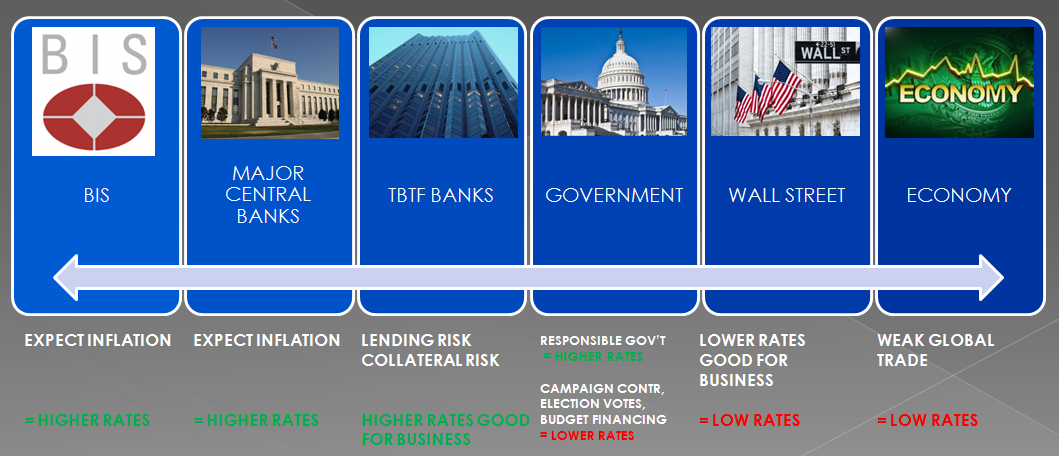

CONSTITUENTS

The Federal Reserve is being pulled in different directions by major stakeholders in the U & Global Economy.

On the one side, the Central Bankers Bank, the bank of International Settlements in Basel Switzerland is out with a major paper concerning the magnitude of the coming Inflation problem which country central banks must be aggressively prepare for. I will be talking more about the BIS research in an upcoming Macro Analytics video with Charles Hugh Smith.

The Major Central Banks of the world are all talking about various levels and time frames for QT. The question is just how much o this is nothing more than "spin" or trying to talk the markets into more fiscal discipline and prudence.

On the other side we have both the US Economy and Wall Street wanting continued low rates and stimulus for differing reasons.

In the middle we have the Government needing both for conflicting reasons.

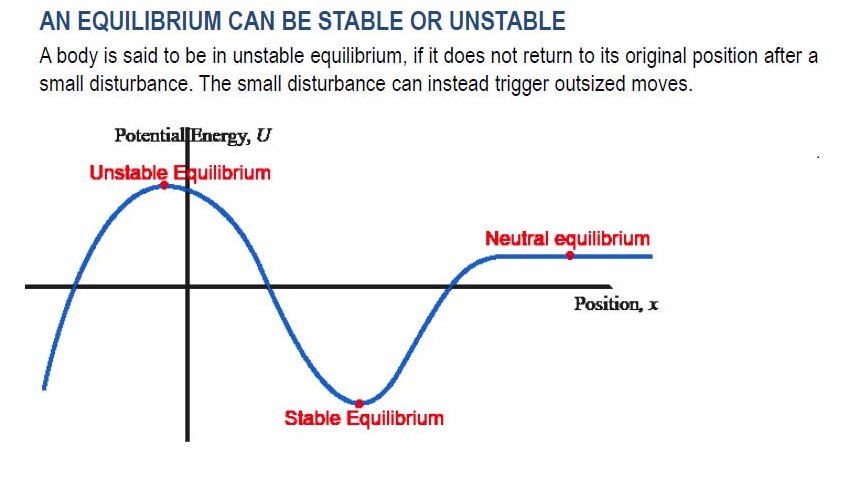

An equilibrium balance must be struck. The chances are high that the solution will be minimal, superficial change until the choice is made for them. That is the central banks will be forced to react.

However, as you would suspect that is also a problem as continuing to 'kick the can down the road' as it has been done for 8 years is quickly running out of roadway!! Our 2010 Thesis paper was entitled "Extend & pretend" as we papered over the underlying issues causing the Financial Crisis.

The content on this site is protected

by U.S. and international copyright laws and is the property of GoldSeek.com

and/or the providers of the content under license. By "content" we mean any

information, mode of expression, or other materials and services found on GoldSeek.com.

This includes editorials, news, our writings, graphics, and any and all other

features found on the site. Please contact

us for any further information.

Live GoldSeek Visitor Map | Disclaimer

The views contained here may not represent the views of GoldSeek.com, Gold Seek LLC, its affiliates or advertisers. GoldSeek.com, Gold Seek LLC makes no representation, warranty or guarantee as to the accuracy

or completeness of the information (including news, editorials, prices, statistics,

analyses and the like) provided through its service. Any copying, reproduction

and/or redistribution of any of the documents, data, content or materials contained

on or within this website, without the express written consent of GoldSeek.com, Gold Seek LLC,

is strictly prohibited. In no event shall GoldSeek.com, Gold Seek LLC or its affiliates be

liable to any person for any decision made or action taken in reliance upon

the information provided herein.