-- Published: Sunday, 10 December 2017 | Print | Disqus

By John Mauldin

A Decelerating Job Picture

Robotic Wipeout

Superhuman Level

Perfect Storm

Monetary Policy Error

Home for Christmas, then Hong Kong

Almost every weekday, some arm of the US government issues some sort of economic statistic. News media and financial analysts review and report it. Then 99.9% of the adult population, and probably 90% of the financial industry, forget all about it. And theyre probably right to do so.

The monthly jobs report isnt like that. Yes, any single month doesnt tell us much. Yes, the Labor Departments methodology has some flaws, both major and minor. But imperfect as it is, the jobs report is our best look at the economys pulse. Jobs matter in a visceral way to almost all of us, as you know well if youve ever lost one. Almost any survey that asked questions around employment would reveal the angst that many Americans feel about the possibility of losing their jobs.

Image: Cristian Eslava

Right now, automation tops the list of things that might threaten our jobs. Artificial intelligence and robotics technology are rapidly learning to do what human workers do, but better, faster, and cheaper.

Ive use the following chart before, but its a compelling illustration of how technology is reducing employment. It shows the rising rig count in the oil patch since mid-2016 and yet the number of workers on those rigs is actually still falling. This is the impact of a new robot called an iron roughneck: Tasks that used to require 20 people now need only five. And the iron roughneck is not even that widely deployed in the oil and gas industry the trend will hit hard in the coming decade. Roughneck jobs are relatively high-paying; it takes a great deal of training and skill to be able to do them.

Today Ill give you some quick thoughts on the just-issued November jobs report, then take a deeper look at the automation problem/opportunity. I use both words because automation truly can be either. And then we look at the failure of the Federal Open Market Committee (FOMC) to take into account the major technological changes that are going to come our way over the next 10 to 12 years (if a host of studies are correct). I think that failure is likely to lead the FOMC to make the mother of all policy errors. And right now, a major monetary policy error is the most dangerous weapon of mass wealth destruction facing the US and the world.

Before we go on, let me briefly remind you that our Mauldin Economics VIP Program is open until December 13. VIP is our all you can eat package. For one low price, you get all our premium investment services and a few extra benefits as well. I believe our information will be invaluable as we move into a highly uncertain 2018. You can learn more about the VIP program here.

A Decelerating Job Picture

The jobs report for November was solid, with job growth above the recent average. But earnings were a disappointment, as we will see. Philippa Dunnes summed up the report in a recent commentary:

Employers added 228,000 jobs in November, 221,000 of them in the private sector. Both are nicely above their averages over the last six months, 164,000 headline and 162,000 private. Almost all the major sectors and subsectors were positive. Mining and logging was up 7,000 (slightly above the average for the last year); construction, 24,000 (well above average, with specialty trades strong and civil/heavy down); manufacturing 31,000 (well above average, with almost all of it from durables); wholesale trade, 3,000 (slightly below average); retail, 19,000 (vs. an average loss of 2,000); transportation and warehousing, 11,000 (well above average); finance, 8,000 (weaker than average); professional and business services, 46,000 (right on its average, with temp firms particularly strong); education and health, 54,000 (well above average, with education, health care, and social assistance all participating); and leisure and hospitality, 14,000 (well below average). The only major down sector was information, off 4,000, slightly less negative than average. Government added 7,000, well above average, with local leading the way.

Whats not to like about this? The answer is that we really need to review the report in terms of the trend. And the trend in employment is deceleration. As Peter Boockvar explains,

Also, we must smooth out all the post storm disruptions. This give us a 3-month average monthly job gain of 170k, a 6-month average of 178k, and a year-to-date average of 174k. These numbers compare with average job growth of 187k in 2016, 226k in 2015, and 250k in 2014. Again, the slowdown in job creation is a natural outgrowth of the stage of the economic cycle we are in where it gets more and more difficult finding the right supply of labor.

The growth in wages is also decelerating. I was talking with Lacy Hunt this morning about the jobs report. He noted that real wage growth for the year ending November 2015 was 2.8%, while for the year ending November 2016 it was just 1%. The savings rate is now the lowest in 10 years. The velocity of money is still slowing, which means that businesses have to do everything they can to hold down costs, and one of those things is to rein in wages.

And yet the Federal Reserve has a fetish for this thing called the Phillips curve, a theory that was thoroughly debunked by Milton Friedman early on and later by numerous other economists as having no empirical link to reality. But since the Fed has no other model, they cling desperately to it, like a drowning man to a bit of driftwood. Basically, the theory says that when employment is close to being as full, as it is right now, wage inflation is right around the corner. According to the Phillips curve, then, the FOMC needs to be tightening monetary policy. Later well see how the FOMCs faulty tool is likely to lead to a major monetary policy error.

Basically, the Federal Reserve looks at history and tries to conjure models of future economic performance based on it even as everyone in the financial industry goes on intoning that past performance is not indicative of future results. But all the Fed has is history, and they cling to it. My contention is that the near future is not going to look like the near or the distant past, and so we had better throw out our historical analogies and start thinking outside the box. Now lets look at some real problems that will impact the future of employment.

Robotic Wipeout

Last month I shared in Outside the Box a new McKinsey report on job automation. Actually, I shared an Axios article summarizing that report, which is 160 pages long. You can read it here if you have time. McKinsey does a good job pulling together data and forecasting its consequences.

Every year, reports like this reflect a process thats occurred many times in human history. People discover or invent something useful: fire, the wheel, iron, gunpowder, coal, oil, the steam engine, electricity, the automobile, the airplane, the computer, etc. Life changes as the new knowledge spreads. People either adapt or they dont. Those who dont adapt fade into the background. In the last few decades of their working lives, they end up taking the very lowliest of jobs in order to get some food, clothing, and shelter; but its not a comfortable life. There was no government safety net for most of our history. But most people tried hard to adapt their skills to the new changes. And as we adapted to radically disruptive inventions like the steam engine, automobile, and computer, hardly anyone had the necessary skills, and so everyone had to learn.

Today, things are different. Fifteen percent of men between the ages of 25 and 54 who should be in their most productive years of contributing to their families and society dont even want a job. Thats up from 5% in the mid-60s, and the number has been steadily rising. Fifty-six percent of these people receive federal disability payments, averaging about $13,000, which is roughly equivalent to the pay for a minimum-wage job, after taxes except that disability comes with free Medicare. Unless these people find ways to develop needed skills, there is not much financial incentive for them to look for jobs.

The rest of the people who dont want jobs are mostly early retirees, homemakers, caregivers, or students. And roughly 1/3 of the 10 million+ men who have dropped out of the workforce have criminal records, which is often a barrier to work. Only about 34% are actually discouraged workers who might take a job if a job is available. That picture should be worrying. It is one reason why GDP has not increased all that much. Remember that GDP is proportional to the number of workers available times their productivity. Taking 10 million workers out of the workforce reduces GDP.

The problem for most of us now is that we dont want to simply fade into the background like so many people have done with each major shift in technology; yet new knowledge spreads around the globe now in seconds instead of centuries. Its easy to feel that the walls are closing in, because for many of us they are. The McKinsey report makes that crystal clear. They project that technology will replace as many as 800 million workers worldwide by 2030. Displacement is not just a US or developed-world phenomenon; it will show up in the emerging and developing markets as well.

McKinsey draws a distinction that we should all remember. The problem is less about jobs disappearing than about the automation of particular tasks that are part of our jobs. In most cases, employers cant simply fire a human, plug in a robot, and accomplish all the same things at the same or better performance level but lower cost. You have to zoom in closer and look at the tasks that each job entails, and ask which of them can be automated. The roughneck jobs in the oilfield are a good example: The Iron Roughneck doesnt replace all workers on the rig, just some of them.

So when McKinsey says that 23% of US current work activity hours will be automated by 2030, thats not the same as saying 23% of jobs. The shift will affect almost all jobs to some degree. That 23% figure is their midpoint scenario, too. In the rapid scenario its 44% of US current work activity hours that will be handed over to machines.

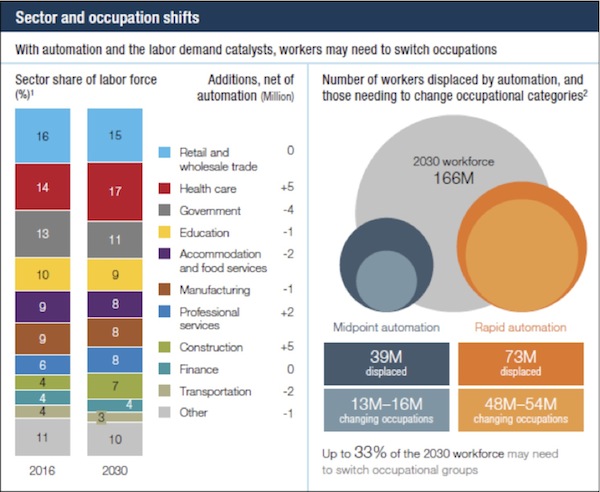

In other words, whatever your job is, some part of it will likely get automated in the next decade or so. That might be good news if the machines can take on the repetitive drudgery that you dont enjoy. Automation could free you to do things that are more interesting to you and more valuable to your employer. But outcomes are going to vary widely. Heres a chart on sector and occupation employment shifts from McKinsey. (This one is for the US; their report has sections for other countries as well.)

The circles on the right are the translation of those task-hours into numbers of workers. As you can see, in their rapid automation scenario, by 2030 just 12 years from now 73 million people out of a workforce of 166 million will have been displaced, with 4854 million of them needing to change occupations completely.

In other words, a full third of the workforce may have to change career fields. Thats going to be a problem. Yes, Americans change jobs more frequently now than they used to, but the changes tend to be evolutionary: We gain new skills, find a better place to apply them, acquire new contacts, seek out new opportunities, and so on. The personal transformation happens slowly enough to be manageable. Thats going to change.

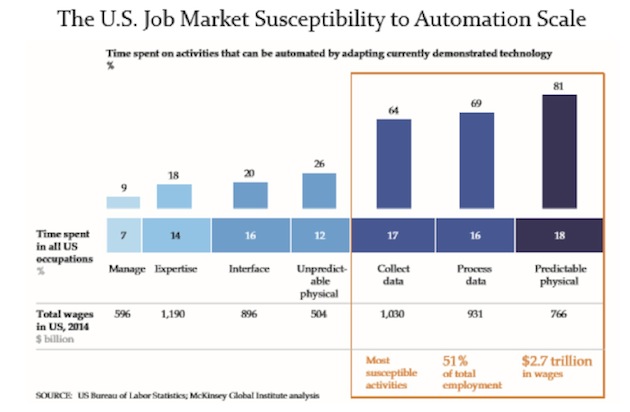

My friend Danielle DiMartino highlights another of the amazing charts in the McKinsey study, one that analyzes US job-market susceptibility to automation scale:

This chart demonstrates that its not just the low-skilled workers who are at risk. Its also mid-level and even some high-level people. There is more job risk than many of us imagine. That is why I break the world up into the Unprotected, the Protected, and the Vulnerable Protected classes. The latter group doesnt even realize their vulnerability.

Superhuman Level

Worse, I think the shift to automation may come even faster than McKinseys rapid scenario suggests. Recently I ran across an artificial intelligence story thats almost terrifying. You might have heard about AlphaGo, the AI system created by Google subsidiary DeepMind. It plays the very complex board game called Go.

In 2015, DeepMind became the first computer to beat a human professional Go player. It learned how to do this by analyzing many thousands of games played by humans. Impressive, but only the beginning.

This year, DeepMind introduced AlphaGo Zero, a new system that quickly acquired the same skills with no human help at all. The programmers simply gave it a blank board and the rules of the game. It then played millions of games against itself. Heres the chilling quote from DeepMind CEO Demis Hassabis:

The most striking thing is that we dont need any human data anymore.

It gets more unnerving. On December 5 (yes, last week), DeepMind published a scientific paper that sounds straight out of science fiction. I added the bold print.

The AlphaGo Zero program recently achieved superhuman performance in the game of Go, by tabula rasa reinforcement learning from games of self-play. In this paper, we generalise this approach into a single AlphaZero algorithm that can achieve, tabula rasa, superhuman performance in many challenging domains.

Starting from random play, and given no domain knowledge except the game rules, AlphaZero achieved within 24 hours a superhuman level of play in the games of chess and shogi (Japanese chess) as well as Go, and convincingly defeated a world-champion program in each case.

Thats startling, so let me repeat it slowly. In one day, starting from nothing at all (tabula rasa), AlphaGo Zero learned to play chess, shogi, and Go at a superhuman level, beating the same systems that had beaten the best humans in the world.

Thats how fast the technology is evolving. I suspect some of the rapid acceleration came from faster processor chips Moores law says they should double in power every two years. But this was far more than a doubling; this was exponential.

Systems like that are coming for your job. So if you think youre safe because you arent an assembly-line worker or a retail cashier and dont work at the level of rote repetition, you could be wrong. These systems will only get better and take on ever more complex jobs.

Could DeepMind build a system that reads my archives, monitors my email, and then writes Thoughts from the Frontline at a level where you couldnt tell the difference between it and me?

How do you know it hasnt?

Perfect Storm

Those who control the tech are intent on bringing the era of superautomation forward as fast as possible. I talk a lot about incentives and the way people and businesses respond to them. Identifying incentives is a key tool in analyzing trends and forecasting what different players will do next. Well, between dicey Federal Reserve policies and possible tax reforms, businesses are getting new incentives to automate sooner rather than later.

First, the Fed. Ive made the case before that I think they waited too long to end quantitative easing and begin normalizing interest rates. Their delay created our present weird situation where we have little or no inflation according to the indexes, but the cost of living for people at the median income level and below is outpacing wage growth and leaving the average household struggling to stay even.

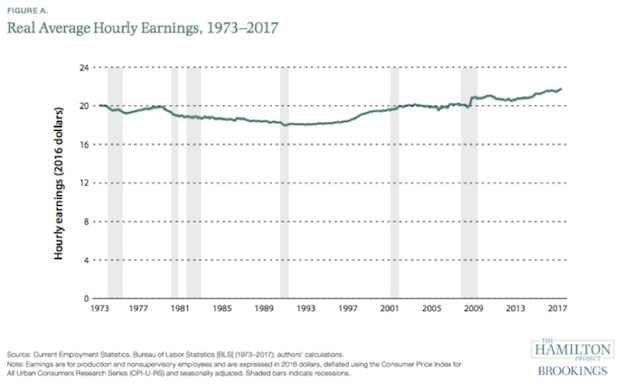

Real wages, that is wages after CPI growth, have advanced only 0.2% a year since 1973. And as I noted above, real wage growth is now decelerating.

Diminished earning power has, in turn, robbed businesses of pricing power and forced them to cut costs ruthlessly. One way you slash costs is by automating. In this weeks Outside the Box I shared a story about how Amazon is now hiring robots faster than it is human employees. Amazon is in the lead, but other companies arent far behind. This trend limits wage gains even more, and the situation is getting worse as the technology gets better and cheaper. (The fact that San Francisco has limited the number of robots per company and limited the speed of robotic delivery simply ensures that San Francisco will be behind the rest of the country in terms of growth and productivity within a few years.)

Of course, theres absolutely nothing wrong with making your business more efficient. You have to survive against the competition. But in this case the competition is not happening naturally or according to market forces. The Fed has kept market forces from working and has created an environment that would never have occurred otherwise. You can argue whether a laissez faire market would have worked better or worse, but its pretty clear we havent had one.

Now add in tax policy. I explained early this year in my open letters to the new US president that we would all be better off with a consumption tax like a VAT rather than we are currently with the income tax. Alas, I did not get my wish. Congress is right now improving the tax code in ways that may actually accelerate the automation trend.

(Incidentally, Im getting many emails with questions about the new Republican tax plan. Ill have more detailed thoughts after we see what, if anything, gets through the conference committee and becomes law. At this point its still a guessing game, and I would rather comment on what is actually extruded from the sausage grinder. Let me just say that theres something in the bill for everybody to hate.)

For instance, one proposal is to allow equipment purchases to be expensed immediately instead of amortized over time. Thats not a bad idea on its own. However, it effectively subsidizes companies to upgrade their equipment and technology to the latest state of the art. And, as we saw above, the state of the art is automated devices that need little human help.

The accelerated shift to automation may help explain a Business Roundtable survey that showed some odd results. As reported by the Wall Street Journal last week, CEOs say their plans for capital investment have risen to the highest level since the second quarter of 2011. Thats good news: Businesses see growth opportunities and want to add production capacity to meet them. But the same survey shows CEO hiring expectations going in the opposite direction. Hiring is not plummeting by any means, and many do plan to increase hiring over the next six months; but the majority say they will keep their headcount where it is or lower it. General Electric will cut 12,000 jobs from its power business, roughly 18% of that divisions total employment, in order to cut costs and reduce overcapacity.

How do we explain a situation in which capital spending rises but employment stay the same or falls? Automation is one answer. It lets you increase capacity without increasing headcount and expenses you may even reduce them.

Not coincidentally, the new tax bill may remove the Obamacare individual mandate, but the employer mandate is staying in place and healthcare costs are still rising. That too incentivizes businesses to use machines instead of people wherever possible.

So where do all these factors leave human workers? The McKinsey forecasts fall more or less at the midpoint of those in other reports I am reading. Were facing a perfect storm: Technological, monetary, and political entities are joining forces to stir up a maelstrom of change that is going to bombard all of us. Im not an exception, and neither are you.

We cant control these giant forces, but we can control our responses. Whatever your job is now, you need to think about how vulnerable it may be and what else you might do. If you need to acquire new skills, start doing it now. If you have young adult or teen children, help them with their education and career choices. That art history degree may not be much in demand in 2030. Or even in 2020.

Monetary Policy Error

Looking ahead brings us full circle, right back to considering the potential for a major monetary policy error. We may, in fact, see a little wage inflation in the near future, and I think that would be a good thing, considering how little there has been for years; but right now the Personal Consumption Expenditures Index (PCE) is hovering around annual growth of 1.5%, still well below the Feds target of 2%. What would be the danger of letting it rise to 2.5%? Seriously.

This FOMC gives every indication that they are not only going to continue to raise rates but are also going to reduce the Feds balance sheet by some $450 billion next year. The Fed thinks QE helped to bring about the rising asset prices (stocks, bonds, and housing assets of all types). Yet somehow they believe that quantitative tightening (QT) wont have any effect on the markets. Of course, there is no empirical evidence for that conclusion, unless you want to count the taper tantrum that was unleashed when interest rate increases and quantitative tightening were first mentioned.

The Fed, with their slavish fetish for the Phillips Curve, see wage inflation just around the corner, and they want to head it off at the pass. But if they are as data-dependent as they say they are, they should look at their data and see that there is no wage inflation. There is a reason why there isnt: The vast bulk of workers do not have pricing power. The labor market has changed dramatically in the last 20 years, and every study I have read as I have researched the future of work suggests that employment is going to change even more drastically in the next 20 years.

If we have 20 million workers who presumably want to have jobs but suddenly find themselves without job opportunities because of automation and other forces, that is not an environment in which we are going to see wage inflation. That is a situation in which workers will take whatever wages they can get. Think Greece.

Monetary growth is decelerating, too. The velocity of money continues to fall. Total consumer debt as a percentage of disposable income is the highest it has ever been over 26%. The savings rate has fallen to a 10-year low. Consumers are stretched, and there is just not the buying power no matter how low interest rates are to create the inflation that the Fed is so afraid of.

I could go on and on about the fragility of this economy, even though on the surface it seems to be the strongest it has been since the Great Recession. Looking ahead, 2018 should be another year for growth. So I look around and ask, what could endanger that? I think the biggest risk is a central bank policy error.

We are going into unknown territory. Beyond this point, there be dragons.

I should add that I am generally optimistic about 2018. My forecast issues this year will probably be more optimistic than they have been for a long time. Not necessarily in terms of stock market prices, but regarding the economy in general. I actually have this hope which I recognize is not a strategy that the Federal Reserve will back off sooner rather than later and we can avoid a downturn in the economy for another few years. I think nothing could make me happier than if we actually established the record for the longest recovery.

Home for Christmas, then Hong Kong

Other than a brief trip here and there and who knows what will slip into the schedule I will be home for most of December. Shane and I will be in Hong Kong for the Bank of America Merrill Lynch conference in the first week in January January. That trip will be made even more fun because Lacy Hunt and his wife JK will be there with us. We are going to take an extra day or two and be tourists. Ive been to Hong Kong many times but have never really gotten out of the business district. The last time I was there Peter church house and his son Tama took us to lunch and then on a sailing expedition through the harbor of Hong Kong. He even let Shane and me take turns at the wheel, so we could pretend to be sailors. We have a picture to prove it!

One thing I will be doing in Hong Kong is getting some new dress shirts. My workouts the past year or so have focused a lot more on my shoulders and shrugs, and I have actually added a full inch to my neck size. I have literally only one shirt that I can (barely) button to be able to wear a tie with. I have been waiting for the Hong Kong trip, because you can get a custom shirt made in just a few days, remarkably cheaply. Im not sure that will mean Ill be wearing more ties, but at least Ill be able to do so comfortably when the need arises.

It has been a busy last few months. I am launching new businesses, and of course that takes time. But amazing new opportunities have presented themselves, and Im in the process of establishing new relationships that will significantly improve my ability to serve the investment advisor community, not just here but all around the world. We are also working on some exciting new newsletters built around the resources and networks that I have compiled over the years. There is a wealth of information out there that we can bring to you that will significantly improve your ability not just to access and manage your investments but to get in control of your life. Putting all these new business relationships in place takes a team, especially management, which is not my forte. Identifying the people that can take these visions of the future and turn them into realities has been a challenge, but now all the pieces are in place and the engine is revving up.

I look forward to being able to serve you in the New Year in brand-new ways. And as a personal request, I would like to hear your ideas on what I should be writing about in my weekly letters. I really do value your feedback and ideas.

And with that, I will hit the send button. You have a great week!

Your hoping the Fed will not be as aggressive as they suggest analyst,

John Mauldin

subscribers@MauldinEconomics.com

Copyright 2017 John Mauldin. All Rights Reserved.

| Digg This Article

-- Published: Sunday, 10 December 2017 | E-Mail | Print | Source: GoldSeek.com