-- Published: Thursday, 21 December 2017 | Print | Disqus

By Frank Holmes

In its November report, mortgage security firm Freddie Mac called 2017 the best year in a decade for the housing market by a variety of measures. These include low inflation, strong job growth and historically-low mortgage rates. This assessment is very encouraging, not just for homebuyers and builders and the U.S. economy in general, but also for commodities, resources and raw materials as we head into 2018.

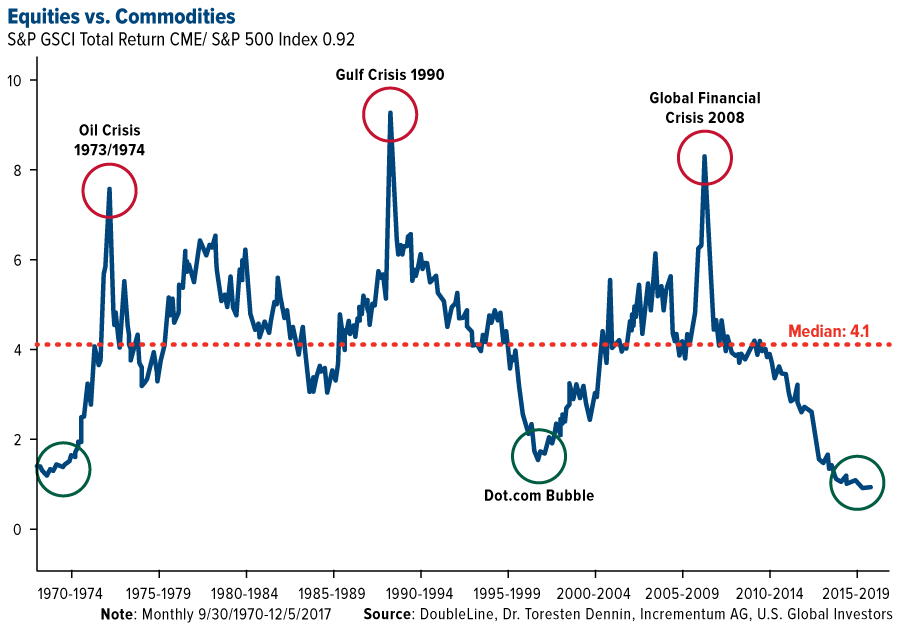

Although past performance is no guarantee of future results, its still instructive to look back at how materials performed the last time the U.S. was ramping up housing starts and mortgages. The last housing boom, which peaked in 2006, was accompanied by elevated commodity prices. We could see a return to these valuations over the next couple of years on higher demand, a stronger macroeconomic backdrop and cyclical fundamentals, as shown in the following chart courtesy of DoubleLine Capital:

click here to enlarge

Speaking on CNBCs Halftime Report last week, DoubleLine founder Jeffrey Gundlach said he thought "investors should add commodities to their portfolios for 2018, pointing out that they are just as cheap relative to stocks as they were at historical turning points.

Were at that level where in the past you would have wanted commodities in your portfolio, Gundlach said. The repetition of this is almost eerie. And so if you look at that chart, the value in commodities is, historically, exactly where you want it to be a buy.

A Wealth of Positive Housing Data

Theres more to support the commodities narrative than cyclicality.

For one, home builders right now are more confident of the future than theyve been in over 18 years. Decembers National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index (HMI) soared to 74, eight points up from the November reading and its highest report since July 1999.

click here to enlarge

NAHB Chairman Granger MacDonald chalks up the incredible improvement in optimism to new policies aimed at providing regulatory relief to the business community. Other contributing factors include low unemployment rates, favorable demographics and a tight supply of existing home inventory.

In addition, new housing starts in November rose to a seasonally adjusted annual rate of 1.3 million, up 3.3 percent from October and a strong 12.9 percent from a year ago.

This is all very constructive (no pun intended), as the market is still trying to recover nearly a decade following the subprime mortgage crisis.

Millennials, the Largest U.S. Generation, Finally Entering the Market

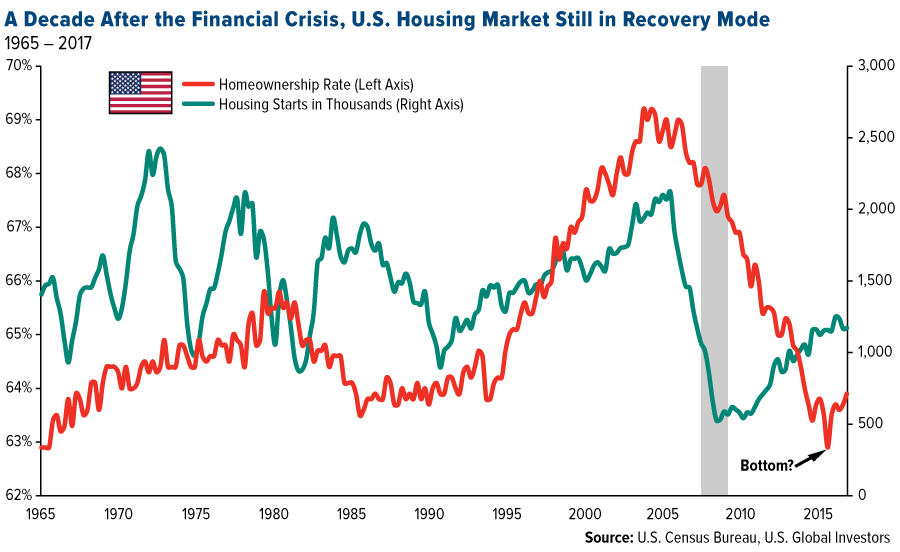

Weve seen booms and busts in new housing starts over the past several decades, but homeownership rates in the U.S. took a huge blow as a result of the Great Recession. The rate dipped to a 51-year low of 62.9 percent in the second quarter of 2016, indicating buyers, especially first-time millennial buyers, are still struggling to save up for down payments.

click here to enlarge

Economists with the National Association of Realtors (NAR) note that student debt has played a massive role in delaying homeownership for young people, by as many as seven years on average. When asked how student loan debt has impacted their life decisions, more than seven in 10 millennials (those born roughly between 1980 and 1998) ranked purchasing a home as the most affected decision, followed by taking a vacation.

Since reaching its low last year, however, the homeownership rate has steadily improved, ending at 63.9 percent in the second quarter of 2017, a three-year high. This leads me to believe that the worst is behind us and that as the economy and labor market continue to improve, so too will demand for new homes. I also have high hopes that the tax cuts President Donald Trump signed into law today will encourage even more millennials, who have until now been sidelined, to join their older cohorts in owning a home.

Time to Add Commodities?

Indeed, all of the conditions appear ripe for another housing boom. Economic growth is on the upswing. The country is at near-full employment. Inflation and 30-year mortgage rates are also historically low.

When we factor in residential fixed investment and housing services, housing as a whole contributes between 15 and 18 percent to national gross domestic product (GDP). Thats a huge slice of the pie. And as Ive pointed out before, housing has an extremely high multiplier effect. For every home thats built, 2.97 full-time jobs and $162,080 in wages and salaries are created, according to a 2014 estimate by the NAHB.

Beyond that, increased home demand is good news for resources and raw materials. According to home-construction services firm Happho, for every 1,000 square feet of new housing, nearly 8,820 pounds of steel are required, as well as 400 bags of cement, 1,800 cubic feet of sand and 1,350 cubic feet of gravel and other aggregate. This doesnt begin to touch on finishers such as brick, paint and tiles, or fittings such as windows, doors, plumbing and electrical. You can see the full infographic by clicking here.

Interested in learning how you can participate in the growing housing market? Unsure how to gain exposure to raw materials and commodities?

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

The S&P GSCI (formerly the Goldman Sachs Commodity Index) serves as a benchmark for investment in the commodity markets and as a measure of commodity performance over time. It is a tradable index that is readily available to market participants of the Chicago Mercantile Exchange.

The Standard & Poor's 500, often abbreviated as the S&P 500, or just the S&P, is an American stock market index based on the market capitalizations of 500large companies having common stock listed on the NYSE or NASDAQ. The S&P 500 index components and their weightings are determined by S&P Dow Jones Indices.

The NAHB/Wells Fargo Housing Market Index gauges builder perceptions of current single-family home sales and sales expectations for the next six months as good, fair or poor. The survey also asks builders to rate traffic of prospective buyers as high to very high, average or low to very low. Scores for each component are then used to calculate a seasonally adjusted index where any number over 50 indicates that more builders view conditions as good than poor.

| Digg This Article

-- Published: Thursday, 21 December 2017 | E-Mail | Print | Source: GoldSeek.com