Happy 2nd Birthday Bail-in Tool! We Suggest Gold As The Perfect Gift

-- Published: Friday, 29 December 2017 | Print | Disqus

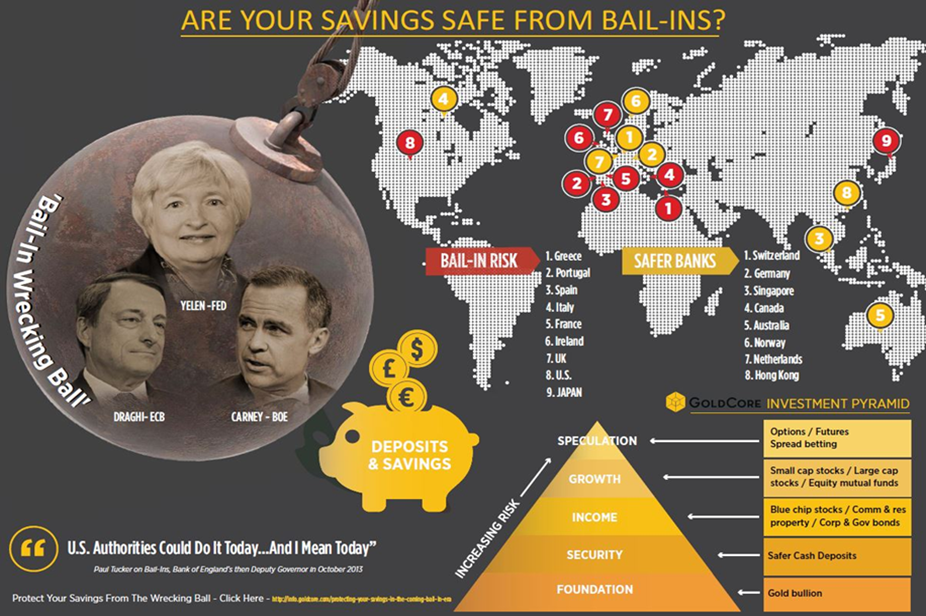

Two years since bail-in rules officially entered EU regulations EU bail-in rules have wiped out billions for savers and and businesses, with more at risk Future of many failing banks now rests on depositors who may no longer be protected by deposit insurance Physical gold enables savers to stay out of banking system and reduce exposure to bail-ins For more listen to our Goldnomics Podcast: What does 2018 have in store for financial markets?

Ah, New Years resolutions, what fun. For some reason we opt to commit to fairly big life changes at some point between Christmas and New Year. This is a time when the real world seems a lifetime away from the cosiness of the holiday season. We often make a resolution when we have had too much of something, perhaps booze, perhaps food or perhaps it is based on regrets from the previous year. Despite best intentions, rarely do we stick to them.

May we make a suggestion? If youre going to make any resolutions this year make one that is pretty easy to stick to and that wont make too much of a short-term impact on your life: resolve to pay attention to and to protect yourself from the threat that is ECB bail-in tools. In the long-term youll be more grateful you did this than if you had given up cursing or drinking for a month.

On the 1st January 2018 the ECB bail-in tool will be two years old. Thats right just over two years ago the ECB decided that it was better to force the financial burden of banks failures away from the state and instead onto bondholders and creditors i.e. those with money in the bank.

The ECB was following in the footsteps of the US where bail-ins have been part and parcel of financial legislation since the crisis of 2007-08. Canada has more recently joined the party.

We have relentlessly covered the threat of and developments in bail-in legislation over the last two years. It is perhaps the most shocking decision to come out of regulators and central banks since the financial crisis. It is even more shocking when one considers the lack of uproar from the financial media who continue to peddle the myth that the financial system is more secure than pre-financial crisis.

The bail-in legislation has been put in place because the EU, along with the rest of the world, has been through a horrendous financial crisis. It exposed such dangers in the banking system that it has taken nearly a decade for global regulators to agree to post-banking crisis rules. Just this month Basel III was agreed. The whole aim of the agreement is to protect governments by having private investors suffer losses first during banking crises.

One has to ask, if politicians are so keen for us to believe in the stability of the financial system in those problem areas why the need for legislation that not only places depositors at risk but has been updated continuously to put them at even more of a disadvantage?

2018 should be a time when investors and savers resolve to take charge of their wealth and hold it outside of the banking system. Physical gold that is allocated and segregated is able to offer this, as well as zero exposure to the bail-in regime. You can hear more about our expectations for 2018 in our new Goldnomics podcast.

A bail-in is when regulators or governments have statutory powers to restructure the liabilities of

distressed banks and nancial institutions, and impose losses on both bondholders and depositors.

Simply stated, a bank bail-in is an attempt to resolve and restructure a bank as a going concern, by creating additional bank capital (recapitalisation) via forced conversion of the banks creditors claims (potentially bonds and deposits) into newly created share capital (common shares of the bank).

This is really the crux of the Cyprus template depositors internationally now have to think of their uninsured deposits as liable to potentially being con scated and transformed into bank shares.

Bank depositors have traditionally viewed their bank deposits as one hundred percent secure, with an inalienable right to have their deposits returned in full. However, this has never been the case in legal terms, as a bank depositor is just an unsecured creditor of the bank.

The original bail-in legislation stated that a bail-out using public funds was not an option until creditors accounting for at least 8% of the lenders liabilities had paid up (the bail-in). At the moment 100,000 or £75,000 is protected per depositor, this amount is known as a covered deposit.

Deposits soon to be more exposed, as decided by bureaucrats

In terms of who pays what it is no longer down to the sovereign government, the introduction of bail-in legislation made clear that that responsibility now lies with the Single Resolution Mechanism.

So not only are your government unable to act in your best interests when it comes to a bail-in but you are now at the mercy of the ECB who will decide on a bail-in based on the Unions best interests.

This was most recently reminded to us when the ECB proposed that covered deposits should be replaced to allow for more flexibility. Essentially under the new proposals depositors and savers will no longer be guaranteed any amount of money should a bank go under.

covered deposits and claims under investor compensation schemes should be replaced by limited discretionary exemptions to be granted by the competent authority in order to retain a degree of flexibility.

To translate the legalese jargon of the ECB bureaucrats this could mean that the current 100,000 (£85,000) deposit level currently protected in the event of a bail-in may soon be no more.

But worry not fellow savers as the ECB is fully aware of the uproar this may cause so they have been kind enough to propose that:

during a transitional period, depositors should have access to an appropriate amount of their covered deposits to cover the cost of living within five working days of a request.

So thats a relief, youll only need to wait five days for some competent authority to deem what is an appropriate amount of your own money for you to have access to in order eat, pay bills and get to work.

Quick and dangerous fixes to cover loopholes and prevent further insubordination

Unsurprisingly bailing-in has been politically tricky, to say the least.

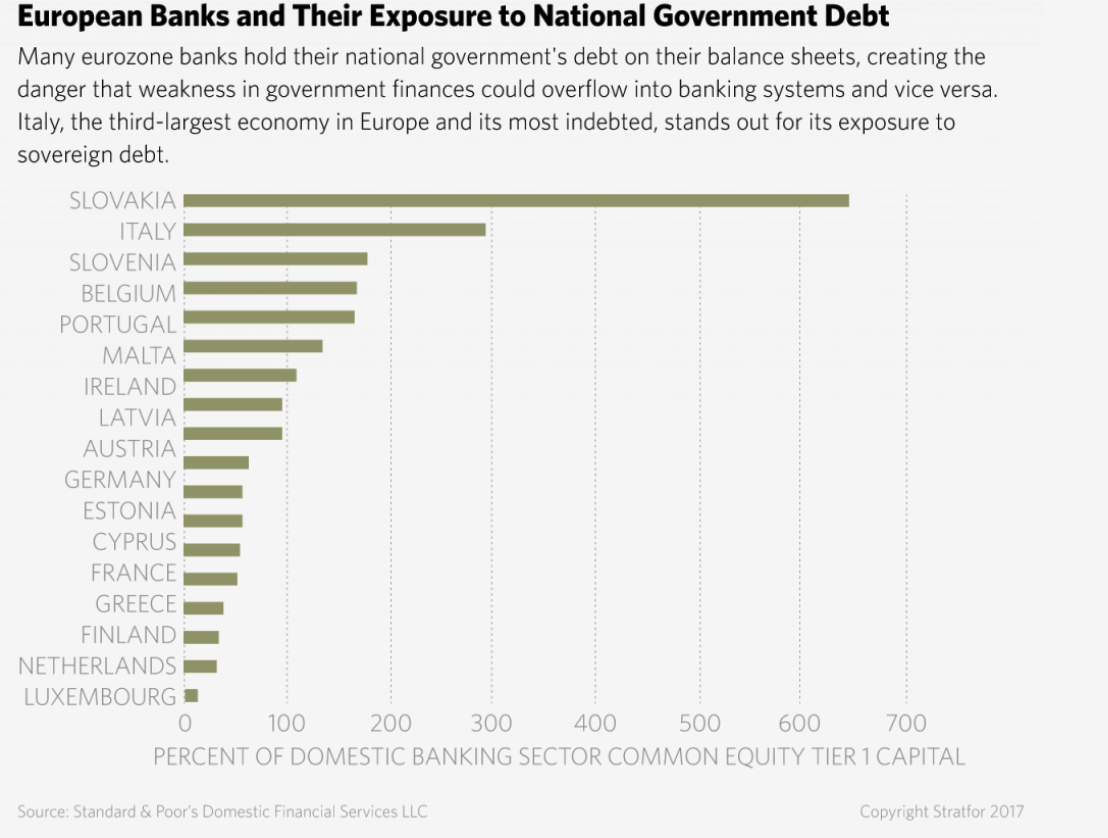

Efforts of governments to avoid any awkwardness when it comes to bail-ins has most prominently been seen in Italy.

Earlier this year the countrys clean-up of the two largest lenders, Banca Popolare di Vicenza SpA and Veneto Banca SpA, saw the government enact a loophole. Rather than use the EUs Bank Recovery and Resolution Directive (which would have put the EU in control of the rescue attempt and forced even more losses on more bondholders) domestic insolvency laws were used.

The EU had been hoping for a success story as seen with Banco Popular Espanol SA. This saw the bank sold to a bigger competitor in June 2017. The sale promptly wiped out shareholders and about 2 billion euros ($2.3 billion) owed to bondholders (who are often Joe Bloggs depositors).

Needless to say the EU were not happy when the Italian bank rescues did not go the same route. They have no doubt since been working on amendments to ensure that such insubordination cannot happen again. Italys moves did not stop savers from being hurt, the banking meltdown in Veneto Italy destroyed 200,000 savers and 40,000 businesses.

Meanwhile, since the financial crisis regulators have been so busy putting in place rescue agendas and items like Basel III they have lost control of what now puts the financial market at risk.

As GoldCore CEO Stephen Flood reminds us:

The actual cause for a banking collapse is reckless lending policies of banks, the build up of leverage and beckoning inflation rates. The central banks should be focused on stability and not economic growth at all costs and the wholesale confiscation of assets.

There are two key issues that place the bail-in agenda at even greater likelihood of being enforced in a more extreme way, across the EU. These are so great that last month the removal of covered deposits was suggested (see above and read more here) as a means to prevent a run on the banks should depositors get wind of how dangerous a situation many banks find themselves in.

These two issues are thanks to sovereign government debt and the rapid growth of the shadow banking system.

What lies in the shadows

There is a doom-loop in existence. In need of safe assets, banks often hold lots of government debt, which is generally deemed risk free. Risk-free? As my 14 year old cousin would say Mega-lolz.

This refers to the danger that if financial or economic crisis hit a country whose banks owned large amounts of sovereign debt, solvency problems would be transmitted from the banks to the government and back, leading to an insoluble self-reinforcing death spiral.

It was actually the doom-loop which originally inspired the bail-in legislation, launched to prevent such a scenario. The concern now is that it might be too little too late or just the wrong tool for the job.

The second issue is the shadow banking system. Despite the heralding in of Basel III it has done little to restrict the growth of the lesser regulated shadow banking system. The system involved financial intermediaries ranging from hedge funds to special purpose vehicles. Generally they have to abide by by less regulation and lower liquidity requirements than their banking contemporaries.

As a result of this relaxed stance on the shadow banking system, outpaced regular lenders in international credit growth for most of the past decade. Here in the EU they are estimated to hold more than 40 trn on assets.

So far, no one has asked what will happen when this bubble bursts. The loop will no doubt tie-in with the banking system, putting depositors once again at risk. However, as with government debt, we are more likely to see greater restrictions on savers and depositors than we will on additional controls on the shadow banking system.

There is no short-term panacea, prepare for the long-term

Sadly the EU seems to believe that a banking system can be propped up by control of and reduction in the rights of hardworking savers when it comes to their money. This is instead of actually dealing with the crux of the matter too much debt in the system.

For a long time we have explained to readers about how it is not worth trusting that the ECB and governments have our best interests at heart. Whether you are a saver, a business or a pensioner with limited funds government institutions have shown blatant disregard for your wealth.

Whilst the ECB works shamelessly to protect the bigger picture, you must make a few changes to prepare for the realistic picture.

By way of reminder the ECB is proposing that in the event of a bail-in it will give you an allowance from your own savings. An allowance it will control:

during a transitional period, depositors should have access to an appropriate amount of their covered deposits to cover the cost of living within five working days of a request.

i.e. no-one is saying if you will ever get that £10,000, £75,000 or 100,000 back.

Savers should be looking for means in which they can keep their money within instant reach and their reach only. At this point gold and silver is the clear option.

Physical, allocated and segregated gives you outright legal ownership. There are no counterparties who can claim it is legally theirs (unlike with cash in the bank or shares) or legislation that rules they get first dibs on it.

Gold and silver are the financial insurance against bail-ins, political mismanagement, and overreaching government bodies. As each year goes by it becomes more pertinent than ever to protect yourself from such risks.

This year make sure youre not ignoring the birthday of the bail-in era, instead you are resolving to fight against it by buying gold to celebrate.

To read more about how you can protect your savings in the bail-in era then read our free guide here.

The content on this site is protected

by U.S. and international copyright laws and is the property of GoldSeek.com

and/or the providers of the content under license. By "content" we mean any

information, mode of expression, or other materials and services found on GoldSeek.com.

This includes editorials, news, our writings, graphics, and any and all other

features found on the site. Please contact

us for any further information.

Live GoldSeek Visitor Map | Disclaimer

The views contained here may not represent the views of GoldSeek.com, Gold Seek LLC, its affiliates or advertisers. GoldSeek.com, Gold Seek LLC makes no representation, warranty or guarantee as to the accuracy

or completeness of the information (including news, editorials, prices, statistics,

analyses and the like) provided through its service. Any copying, reproduction

and/or redistribution of any of the documents, data, content or materials contained

on or within this website, without the express written consent of GoldSeek.com, Gold Seek LLC,

is strictly prohibited. In no event shall GoldSeek.com, Gold Seek LLC or its affiliates be

liable to any person for any decision made or action taken in reliance upon

the information provided herein.

{kind=link}