-- Published: Sunday, 11 February 2018 | Print | Disqus

By John Mauldin

Burn Rate

Off-Budget Game

0% Financing Ends

Lender Search

Coup de Grace

Sonoma, San Diego and SIC, and Elsewhere

Last weeks turbulence shined a harsh spotlight on the stock market. Appropriately so, if thats where your investments are. But in the hubbub many investors are missing the deeper and far more urgent bond market issues.

We already knew interest rates were rising. Recent data suggests they could rise significantly more than many expected just a few weeks ago. If so, that will be a big problem for bonds, stocks, and many other assets not to mention taxpayers who will bear the cost of swelling government debt, consumers who may face inflation, and everybody who will be hurt by a recession.

Getty Images

The combination of a falling stock market and rising interest rates is historically and statistically rare. Normally, when the stock market goes through a correction, interest rates fall. Looking back through history, we see that 1987 and 1994, two years I have been writing about in connection with 2018, were the other unusual years.

Ive been relatively optimistic on the economy this year, and I still think the year can end well. But given recent events, the path is more challenging now and the odds of a rough 2019 are growing.

Burn Rate

Sudden market moves usually have many contributing factors, but they still need a trigger. Typically, its some new piece of information that wasnt already reflected in prices. What did we learn just ahead of the drop on February 2 and then the bigger one on February 5?

I still think the key factor was the Friday unemployment report, which showed wage growth of 2.9%. It is been a long time since weve approached 3% wage growth. The markets, probably rightly, interpreted this as a sign that the Fed will turn more hawkish if that trend continues. The Feds going into inflation-fighting mode is not bullish for the market. From a recent Congressional Budget Office (CBO) statement:

Next, because the tax legislation reduced individual income taxes for most taxpayers, the Internal Revenue Service released new income tax withholding tables for employers to use beginning no later than the middle of February 2018. As a result of those changes, CBO now estimates that, starting in February, withheld amounts of individual income taxes will be roughly $10 billion to $15 billion per month less than anticipated before the new law was enacted. Consequently, withheld receipts are expected to be less than the amounts paid in the comparable period last year. In addition, the government ran a deficit of $23 billion in December, and it normally runs a deficit in the second quarter of the fiscal year.

We knew part of this. The tax bill President Trump signed in December was passed under reconciliation rules that allowed the reduction of revenue by $1.5 trillion over 10 years. That works out to $12.5 billion per month, roughly the amount CBO says tax withholding will drop. Economic growth is supposed to offset this. I think it will to some extent, but not enough and, more importantly, not soon enough.

Also on Friday, in a separate report, the Treasury Department estimated that it will borrow $955 billion in FY 2018. That estimate is based on input from a group of private banks that advise the Treasury. If the amount is correct (and it may not be), it will represent an 84% increase over the $519 billion Treasury borrowed for FY 2017. This huge increase is clearly not taking us in the right direction, and its more than can be accounted for by lower tax revenues. Nor is it a one-time blip. The same report forecasts borrowing of $1.083T in FY 2019 and $1.128T in FY 2020.

The budget that has now been passed by the Senate and is likely to pass the House and be sent to Trump to be signed will add another $300 billion to the deficit over just the next two years. We are going to exceed $1.2 trillion in average debt for the next three years, and thats just the on-balance-sheet deficit.

Whats the problem, you ask?

The answer will get us into some little-examined and perhaps arcane fiscal policy issues. They are nevertheless important. In short, the budget deficit and the amount of government borrowing (for the year) are two different things. The official deficit increasingly understates the problem

and I think markets are starting to realize that.

Getty Images

Off-Budget Games

Politicians like to talk about managing the federal budget the way you manage a family budget. This rhetoric makes for good sound bites but ignores an obvious reality: The federal government isnt like your family. It has exponentially greater powers and responsibilities and is a sprawling behemoth to boot. The same budgetary principles dont always apply.

For one, you cant set your home budget and then add additional expenses without changing your budget parameters. The government can do so, and it does. These are the so-called off-budget expenditures you may have heard about. They dont affect the official deficit that is discussed in the press. They do affect the amount of cash the government needs. Where does it get that cash? It borrows it by issuing Treasury paper.

Off-budget expenditures pay for a variety of programs: Social Security, the US Postal Service, and Fannie Mae and Freddie Mac are among the more familiar ones. But the category also includes things like disaster relief spending, some military spending, and unfunded liabilities that turn into actual costs. Federal student loan guarantees sometimes force the government to disburse cash. Thats an off-budget outlay.

Off-budget outlays have risen in part because they include Social Security benefits, and the Baby Boomer generation is retiring. But the other categories mentioned above have grown as well, and they are increasingly problematic.

The Treasury Department has the unwelcome job of juggling the governments cash flows to pay the people and businesses Congress has decided should be paid. When there isnt enough tax revenue, Treasury must borrow to meet the difference. Any unforeseen decrease in tax revenue or increase in expenses can force it to borrow more. This activity has nothing to do with the formal budget even when we have one, and we currently dont.

Do you remember a headline mentioning annual trillion-dollar increases in the US debt during the last eight years of the Obama administration? I didnt think so.

The problem has been papered over by off-budget receipts, mainly Social Security taxes, that give the US Treasury more cash it can disburse. But eventually the benefits those taxes represent come due. Then outlays go up, but revenue may not. We are rapidly reaching that point. Look at this table, which I found here and excerpted:

National Debt by Year: Compared to Nominal GDP and Major Events

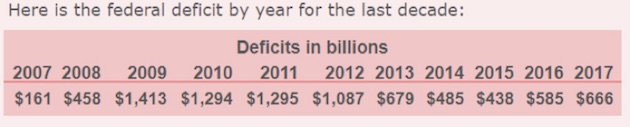

You will notice that there are many years during which the US debt rose by more than $1 trillion. Note that 2015 saw an increase of $1.4 trillion, while the on-budget deficit that year was just $439 billion.

Admittedly, 2015 was an outlier, but lately it hasnt been much of one. Look at this chart of the on-budget deficit for the last 10 years. Comparing to the above table, you can see that off-budget deficits have been running more than $500 billion recently. Some years not so much, but the general trend has been from the lower left to the upper right.

But wait, theres more.

0% Financing Ends

Since 2008 the Federal Reserve has greatly simplified Treasurys cash management task. It has kept short-term rates ultra-low, allowing the Treasury to borrow tons of cash with minimal financing costs. The Fed also bought Treasury bonds directly as part of its quantitative easing programs. Since the Fed sends most of the interest it receives right back to the Treasury, those bond purchases amounted to almost interest-free financing. The average interest paid on the US debt has been reduced to less than 2%, largely because Treasury has loaded up on short-term debt in order to reduce the interest-rate costs that must be allocated to the budget deficit each year. So rather than focusing on long-term debt with the 30-year at an all-time low, Treasury has been selling short-term bills and notes. Thats good cash management in the short run and very shortsighted in the long run.

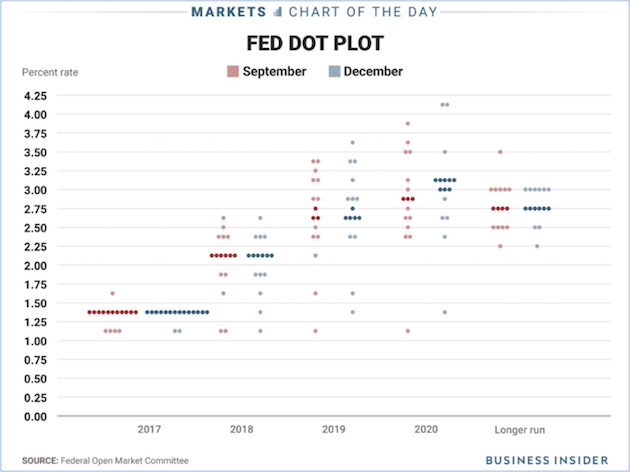

Both those factors are now changing. The Fed is actively raising short-term interest rates while also reducing its Treasury bond purchases. The FOMCs December dot plot suggests that rates will rise to 2.25% by the end of this year and to 2.75% in the longer term. This increase will raise Treasurys interest costs considerably. And the interest must itself be financed, so that requirement will drive borrowing needs yet higher. Do you think the chances are good that the Treasury will be able to finance its debt at 2% in 2019? Me neither. And with $20 trillion total debt, even a 0.5% interest rate increase will have an impact on the overall budget deficit.

Business Insider

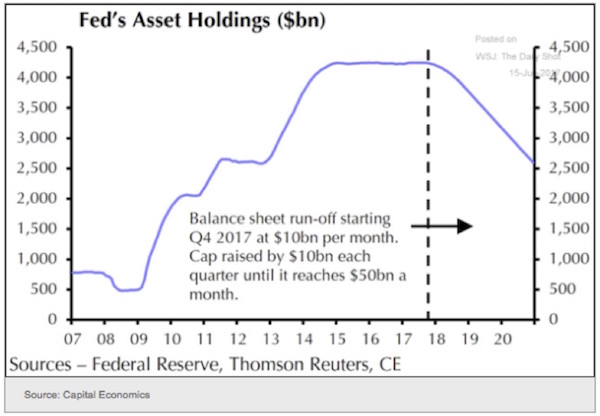

On the balance sheet unwind, here again is a chart I shared last week:

The important point here is that the Federal Reserve balance sheet reductions are just now getting started. The pace will quicken. In January the Feds Treasury bond assets dropped by $18 billion. The shrinkage will vary by month, but the combined total Treasury and mortgage bond balance is set to fall $420 billion this year and another $600 billion in 2019. The number will continue to fall at that pace until either the balance sheet reaches zero or the Fed decides to stop.

This path would be fine if the Treasurys cash needs were likewise falling. Instead, they are rising. That $1 trillion that the Fed is going to sell back to the market will cost the Treasury a minimum of 2% and probably closer to 2.5%. That increases the deficit by $20$25 billion a year.

So lets add it up. The federal deficit will be north of $1.1 trillion. Lets assume the off-budget deficit actually drops to $400 billion and that the Federal Reserve is going to want to sell $460 billion into the market. (Note: some of that will be mortgages, and the rest will be US bonds and bills.)

Simple arithmetic suggests that we will need to find about $2 trillion in additional funding to buy government debt in 2018. And candidly, that may be an optimistic projection.

Which brings us to this letters titular question: Where will we get the cash?

Lender Search

In theory, it should not be a problem for the US government to borrow all the cash it needs. Occasional political antics aside, we are the worlds best credit risk. No one worries that they wont get their T-bond principal back. The entire global financial system depends on that rock-solid guarantee.

So, the question is less whether Treasury can repay than whether potential borrowers are healthy enough to supply our needs or might see better alternatives. This question is important because Treasury is losing the Federal Reserve as a primary funding source. Who can take its place? There are several candidates. Unfortunately, each has barriers that may reduce their buying interest.

American savers and investors are prospects if they have money to lend. Unfortunately, the number who do is not growing. It may grow if unemployment stays low and wage growth accelerates, but the Baby Boomers are transitioning from savings mode to spending mode, so they wont help much.

US pension plans and other institutions that need to fund future obligations are natural Treasury buyers, too. Higher rates might entice back some buyers who have moved into corporate or other long-term bonds in the last decade. Then again, high enough rates will entice anyone back, but those higher rates come with a cost. Specifically, each 1% higher is $10 million per trillion dollars of debt issued. On our $22 trillion in total US debt (by the end of the year, give or take a few billion), that will eventually be about $220 billion in interest as rates go up and the debt has to be rolled over. Thats interest per year!

That means we are spending approximately 15% of our revenue and 12% of actual expenditures just on interest.

There is also the issue of state and local pension funds, many of which have vast future obligations that are poorly funded and will likely remain so, given these entities precarious financial condition. They should probably be buying more Treasury paper, but its not clear that they can.

Getty Images

Other natural buyers are overseas. You hear a lot about Chinas owning so much of our government debt. Its true, but to some degree they have little choice. So long as the US runs a trade deficit with China and we insist on paying for our imports with dollars, China will probably continue to use those dollars to buy dollar assets with that export revenue. It can happen indirectly: Maybe China buys raw materials from Australia with the dollars, and then the Australians buy dollar assets. But in any case, the amounts are so vast that the Chinese gravitate toward the most liquid dollar asset Treasury bonds.

China would like to convince its trade partners to deal in renminbi, and the partners are very slowly coming around. This is happening especially through Chinas gigantic One Belt, One Road infrastructure initiative. The Asian and African nations where China is building ports, railroads, and other facilities are being encouraged to accept renminbi in payment and then use the currency to buy Chinese goods. But the simple fact of the matter is that a lot of the projects for One Belt, One Road require the spending of actual dollars.

That Chinese process is unfolding slowly. I dont worry about Chinas suddenly deciding to boycott US bonds. The Chinese dont presently have that choice. However, they firmly intend to reduce their dollar dependence wherever possible. I dont see them volunteering to lend us significantly more cash than they do now. And indeed, they have been reducing their dollar purchases significantly.

OPEC is another once-reliable lender that is becoming less so. The reason isnt complicated. Growing US shale production reduces our need to buy oil from OPEC countries, in the Middle East and elsewhere. We are buying 7 million barrels per day of oil less from outside the US than we used to. If OPEC countries ship us less oil and gas, we ship them fewer dollars, and they lose capacity to buy our debt, even if they want to.

In fact, federal debt held by foreign investors rose from about $1 trillion in 2001 to around $6 trillion in 2013, but it has more or less gone sideways since that point. China and Japan are no longer buying large amounts of US debt. Theyre not selling it, either.

Look at it this way. I have a few fairly wealthy friends who are aggressive gold bugs. But when I ask them privately whether they are adding much to the actual physical gold they own, they say, Not so much. Even though they are firmly convinced that gold is eventually going to $1015,000, their appetite to increase their gold holdings seems to be sated.

In the same way, China and Japan and many other foreign countries seem to be saying, We have enough US bonds; lets see if we can find some other way to spend our money.

Please note that Japan, Australia, and Europe all have initiatives to build infrastructure and to be part of the growth that is going to be happening along with One Belt, One Road. China is entirely comfortable with those moves, since that is money they dont have to spend all they really need is the transportation infrastructure to move their products back and forth. They are perfectly willing to let Europe and Australia help build out Africa and Southern Asia.

And while the matter doesnt get much play, and the Trump White House doesnt seem to notice, the renminbi is actually quite strong. Chinese consumers are in the best shape they have been in for a long time, and they are using the strength of their currency to import goods, which typically have to be bought in dollars.

Further, many of the large state-owned enterprises have dollar-denominated debt that is essentially guaranteed by the Chinese government. Some of those dollars are going to come back to pay lenders, wherever they may be from.

You can go to this link to see how much each government around the world has actually invested in US Treasury securities. Interestingly, Ireland and the Cayman Islands are in third and fourth place behind China and Japan. At one point this past year, China actually had a little less in Treasury securities than Japan did, but they are both above $1 trillion total. The next four countries combined are up to $1 trillion+ total. And so on. You will also notice that many of the 10 largest holders are associated with major banking centers. And while their appetite is still rising, it is not growing by much.

Foreign buyers may represent another $400 billion available this year to purchase US Treasury securities. That still means we have to find at least $1.5 trillion from US sources. The smart money suggests that interest rates are going to have to go up in order to attract those buyers. That is one of the reasons we are seeing the very unusual circumstance of interest rates rising at the same time the stock market is falling out of bed.

Sidebar: The US 10-year yield is at 2.86% as I write. That is up from 2.05% last July, but is still lower than it was little over four years ago, when it hit 3%. Then, 3% 10-year yields didnt stop the bull market.

As you can see, our lender search wont necessarily be quick or easy. There is one sure way to scare up lenders

but it has a few drawbacks.

Coup de Grace

The US financial industry is extremely adept at evaluating credit risk for individual borrowers or at least it thinks it is. Most folks can get a loan if they want one, but your interest rate will reflect your creditworthiness.

Similarly, Treasury can borrow all it needs by paying higher rates. Thats not the preferred outcome, but it is probably what will happen. We are already seeing rates trend upward as the benchmark 10-year climbs toward 3% from near 2% just 8 months ago. This rise also reflects inflation expectations, but the growing supply of Treasury debt is still the key.

Last week may be just a hint of what is coming. Credit markets are nothing more than borrowers competing against each other for lenders. The Treasury competes with investment-grade corporates, who compete with high-yield issuers. Then you have municipal bond issuers and many smaller debtors. They all need cash, but there is only so much to go around.

Rising Treasury issuance will force other borrowers to pay higher rates, which will in turn make Treasuries buyers demand higher rates. The process feeds on itself. Borrowers eventually find debt service taking a bigger bite out of their income. This burden leaves them less to spend on other goods and services.

Meanwhile, as time passes, borrowers who locked in lower rates during the QE years will need to refinance and will find they must pay sharply higher rates. Some wont be able to do so and will go out of business, laying off workers and leaving their own lenders holding losses. This process will be extreme for issuers of high-yield bonds. As noted last week, there is now a drastically increasing amount of high-yield bond debt that has to be rolled over every year.

That process eventually adds up to a recession, which makes government spending rise even more as people lose jobs. How far away are we from that point? I still dont expect a recession this year, but the risks will rise as we get into 2019. From there, the picture worsens quickly.

I dont want to leave you depressed, so Ill stop here. None of this is inevitable, but neither is it unlikely. Now is the time to get ready.

Sonoma, San Diego and SIC, and Elsewhere

In three weeks Shane and I will be going to Sonoma, where Ill speak at my Peak Capital friends annual client conference. Then well come back to Dallas, where I will speak at the S&P Financial Advisors Forum in downtown Dallas on Tuesday, February 27. If you are an investment advisor, sign up and lets try to make sure we get to chat. I always like to talk to my readers.

After that, Ill continue preparations for the Strategic Investment Conference. This is really going to be the best conference we have ever done, and you dont want to miss it. We have been holding teleconferences with the various speakers on what theyre going to be presenting and how well work the moderating and Q&A panels, and Im adjusting the lineup a little to make the ideas flow better.

If the markets have been a little confusing the last week or so, there is no place better than the SIC to get a handle on whats coming. I have some of the best economists and market strategists flying in from all over the world. There will be a special emphasis this year on looking at the social and technological changes that are coming in the next 10 years.

Our Thursday night at the conference, the dinner presentation will feature Democratic pollster Pat Caddell, who saw the fragmentation of society that led to Trump before anybody else did; Neil Howe, who understands the Millennial generation better than anyone else; Steve Moore; and myself, discussing what we all see as the coming fragmentation of society. And I guarantee you, it will have significant meaning for your investment portfolios. It is time to position yourself for a world that is going to be transforming.

And we have so much more at SIC this year. We have just finalized the last couple of speakers, who will address the recent volatility. I always try to leave a spot or two open to cover the questions that are currently most on the minds of attendees.

As Ive said before, conferences are my artform. You dont simply gather a bunch of speakers. You find the right speakers and put them in the right order in order to build on the information presented from the very beginning to the very end.

You wont want to miss the presentations by Niall Ferguson and David McWilliams, nor their discussion/debate right after. Im looking for a joke that begins something like, A Scotsman and an Irishman walk into a bar and sit down next to an American.

And let me close with something from the Ministry of Silly Indicators (located down the hall from the Ministry of Silly Walks). A friend (whom I cannot name) began to muse about whether the world would feel better on Monday morning after the Winter Olympics opening ceremony. He went back and looked at the last four Winter Olympics. Going into each of them, the market was in either a downturn or a serious correction. And on every occasion the market turned back around on Monday and went on to make new highs. He did admit that this was a ridiculous indicator, but he thought it was amusing.

And with that brief bit of levity, it is time to hit the send button. Let me wish you a great week! And stop procrastinating! Sign up for the SIC and see me in San Diego in a month.

Your wondering who is going to buy $2 trillion worth of Treasury securities analyst,

John Mauldin

subscribers@MauldinEconomics.com

Copyright 2018 John Mauldin. All Rights Reserved.

| Digg This Article

-- Published: Sunday, 11 February 2018 | E-Mail | Print | Source: GoldSeek.com